CICC: What changes have occurred in the crypto industry over the past year?

TechFlow Selected TechFlow Selected

CICC: What changes have occurred in the crypto industry over the past year?

Short-term digital asset prices are certainly subject to significant volatility due to factors such as market liquidity, but in the long run, digital assets and blockchain-based financial services are expected to achieve sustained growth.

As 2020 comes to a close, we have witnessed significant changes in the ecosystem surrounding digital assets such as Bitcoin (the crypto industry). A direct observation is that Bitcoin's price has nearly tripled over the past year, reaching a record high of $27,000, while the total issuance of stablecoins has grown 3.5-fold, hitting a new high of $27 billion.

We believe the following three factors are key internal drivers behind the development of Bitcoin and stablecoins:

(1) Regulatory policies on digital assets are becoming increasingly clear across countries;

(2) The emergence of financial products and channels such as GBTC and PayPal has lowered the entry barrier for traditional investors to access digital assets;

(3) The rise of blockchain-based decentralized financial services.

In the short term, prices of digital assets are certainly subject to volatility due to market liquidity and other factors. However, in the long run, digital assets and blockchain-based financial services are expected to achieve sustained growth.

Traditional investors continue to join, driving Bitcoin’s price up nearly 3-fold in one year

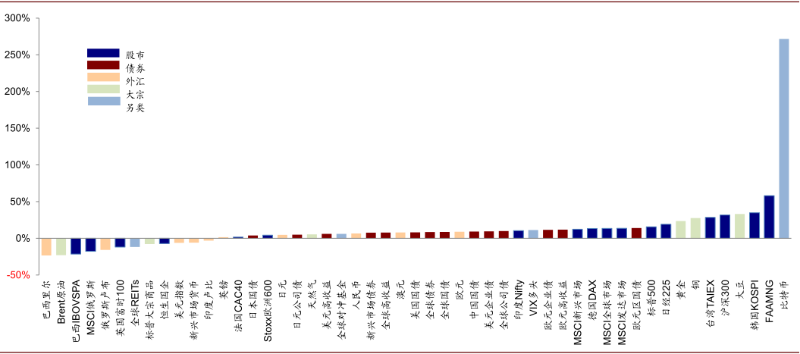

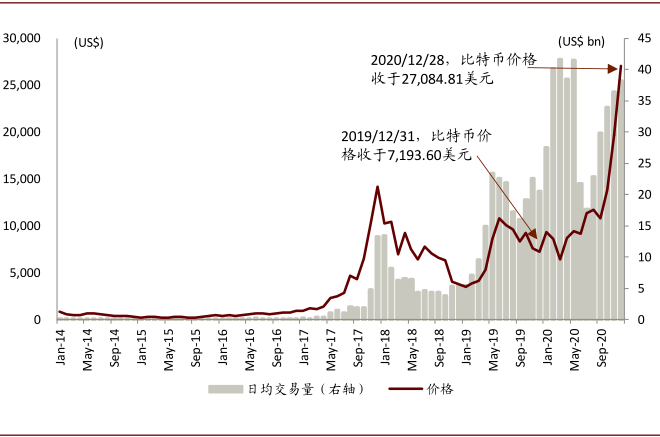

► Bitcoin price surged nearly 3-fold. From around $7,200 at the end of 2019 to $27,084 (as of December 28, 2020), Bitcoin achieved a near-tripling in value, making it the top-performing asset class year-to-date—outperforming even the FAAMNG tech giants index. Beyond the impact of global liquidity easing, we believe structural drivers behind this surge include financial innovations by institutions such as PayPal, Robinhood, and Grayscale, which have broadened access to digital assets over the past year. While short-term price movements may be influenced by liquidity flows and speculative trading, leading to high volatility, the expanding base of traditional investors bodes well for the long-term steady appreciation of digital assets like Bitcoin.

Chart: Year-to-date performance of major asset classes

Source: Bloomberg, CICC Research

Chart: Bitcoin price and daily average trading volume since January 2014

Source: CoinMarketCap, CICC Research

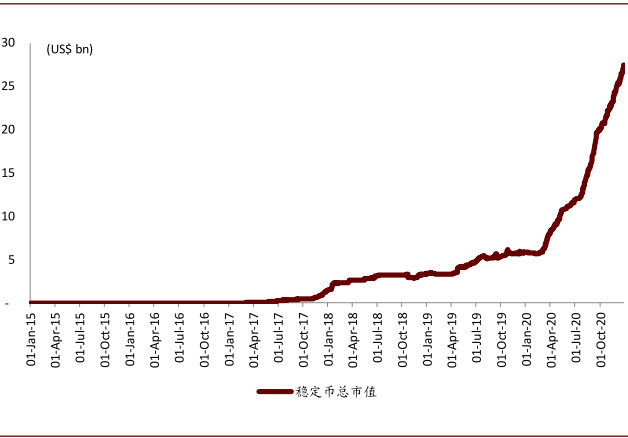

► Stablecoin supply expands 3.5-fold. Over the past year, the total issuance of stablecoins represented by USDT rose from $6 billion at the end of 2019 to $27 billion—an increase of 3.5 times. We believe this growing demand has been driven by the rapid development of Ethereum-based decentralized applications (DApps), particularly financial services such as collateralized lending (MakerDAO) and decentralized exchanges (Uniswap). Looking ahead to 2021, we expect stablecoins like USDT will further consolidate their role as a universal payment method within digital asset transactions. However, whether global stablecoins like Libra will achieve large-scale commercial adoption remains to be seen.

Chart: Stablecoin market size since January 2015

Source: Coin Metrics, CICC Research

Digital asset regulations become clearer; new rules in Hong Kong and Singapore may accelerate the growth of compliant exchanges

Regulatory frameworks for digital assets are becoming increasingly defined. Over the past year, the G20 has led efforts to establish a regulatory framework for global stablecoins (GSCs) such as Libra to mitigate financial risks. In Hong Kong, the Securities and Futures Commission (SFC) introduced regulatory guidelines in 2019 for licensed asset management firms investing in virtual assets, and in December 2020 issued the first cryptocurrency exchange license (Type 1 – Securities Dealing, and Type 7 – Automated Trading Services) to OSL. Meanwhile, Singapore passed the Payment Services Act, laying the foundation for the development of digital asset-related financial services—including exchanges, asset managers, and OTC platforms—within its jurisdiction.

Chart: Current regulatory attitudes toward crypto assets by country (as of December 2020)

Source: Interconnection Pulse, CICC Research

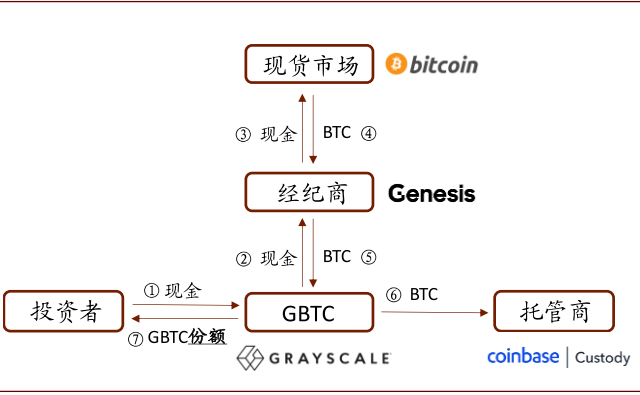

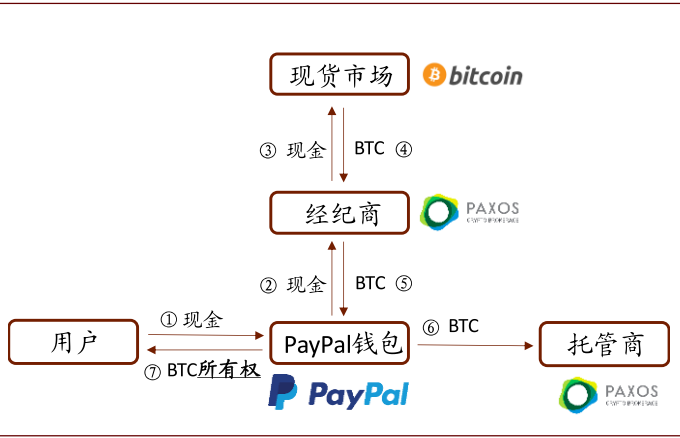

Digital asset investment channels: from Coinbase and Huobi to GBTC and PayPal

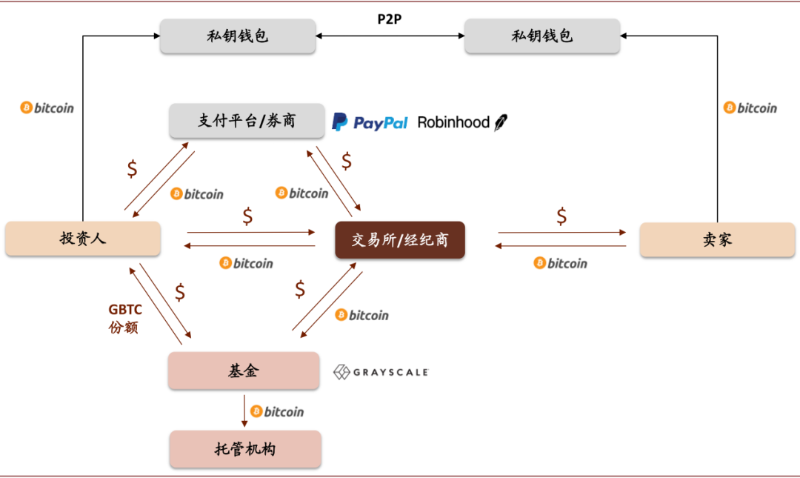

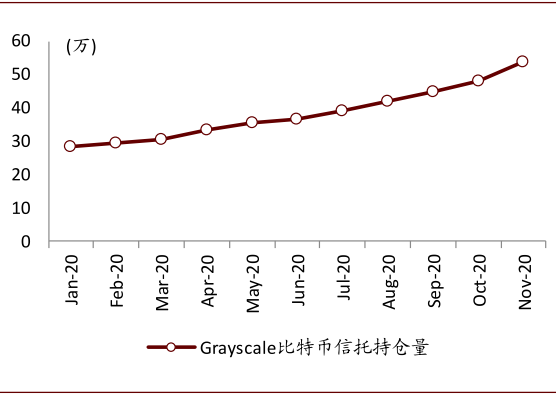

Previously, buying and selling digital assets required using specialized exchanges like Coinbase, presenting high entry barriers and insufficient investor protections. Over the past year, however, we have seen the emergence of investment vehicles such as Grayscale’s Bitcoin Trust (GBTC) and Bitcoin trading services launched by well-known platforms including PayPal and Robinhood. These developments have significantly lowered the barrier for both institutional and retail investors to enter the digital asset space. According to Grayscale’s official website, GBTC’s AUM has reached $14 billion. Between the end of 2019 and November 30, 2020, GBTC accounted for 65% of all newly mined Bitcoins globally. Traditional financial institutions such as Fidelity and DBS have also begun establishing digital asset service platforms. As a result, traditional financial players are gradually becoming key participants in the Bitcoin investment landscape.

► The emergence of trust-like investment products such as Grayscale’s GBTC allows investors to participate without worrying about custody or security issues. Additionally, GBTC trades over-the-counter and files regular disclosures with the SEC, enhancing liquidity and transparency, and providing U.S. investors with a convenient access point;

► End-user platforms with strong influence in financial payments—such as PayPal (payment app) and Robinhood (trading app)—have partnered with regulated crypto brokers to open trading interfaces and provide custodial services for users’ crypto assets. This enables millions of users to access cryptocurrencies instantly without opening additional accounts, dramatically lowering the entry threshold.

Chart: Commercial landscape of digital asset access channels

Source: CICC Research

Chart: Grayscale Bitcoin Trust holdings since January 2020

Source: The Block, CICC Research

Chart: How GBTC works

Source: ChainHill Capital, CICC Research

Chart: Illustration of purchasing Bitcoin via PayPal

Source: PayPal, CICC Research

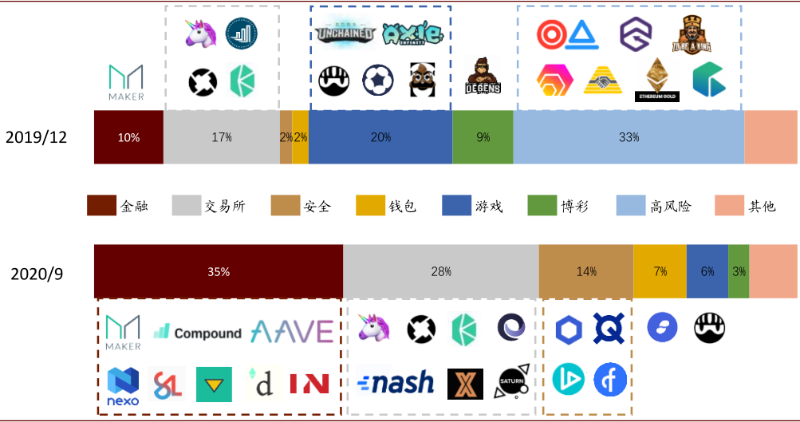

Ethereum enters a new phase of development, emerging as the most active public blockchain network

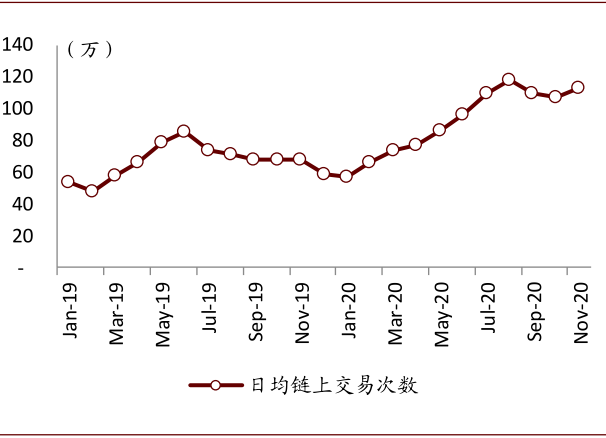

The Ethereum ecosystem is maturing rapidly, with financial applications becoming dominant. Unlike Bitcoin, which is primarily used as a digital asset, Ethereum supports smart contracts and PoS mechanisms, making it ideal for developing blockchain-based decentralized applications (DApps). Over the past year, the Ethereum ecosystem has advanced quickly, with daily transaction volumes rising 90%. Financial services such as MakerDAO (decentralized lending) and Uniswap (decentralized exchange) have become mainstream applications on the Ethereum network. Although the legal status of decentralized finance (DeFi) remains unclear, its technological advantages—efficiency and transparency—have been evident over the past year. Whether DeFi can serve as a meaningful complement to traditional finance remains an open question.

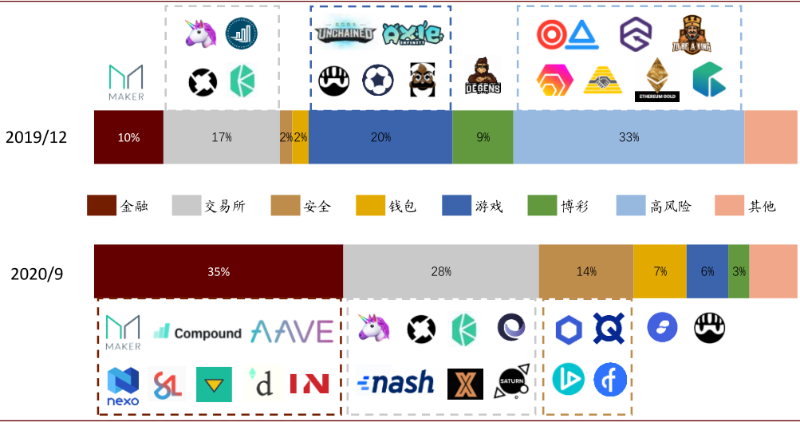

Chart: Shifting application mix on Ethereum since December 2019

Source: State of the DApps, CICC Research

Chart: Top 10 Ethereum applications from October 2019 to December 2020

Source: State of the DApps, DAppTotal, CICC Research

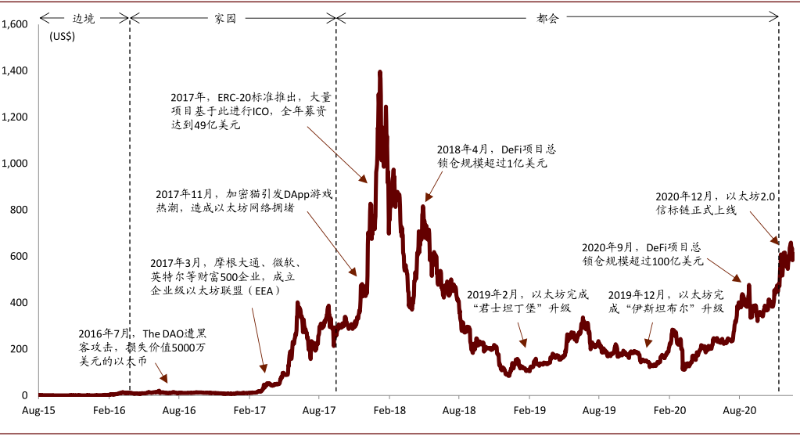

Chart: Major milestones and historical price of Ethereum

Source: CoinDesk, CICC Research

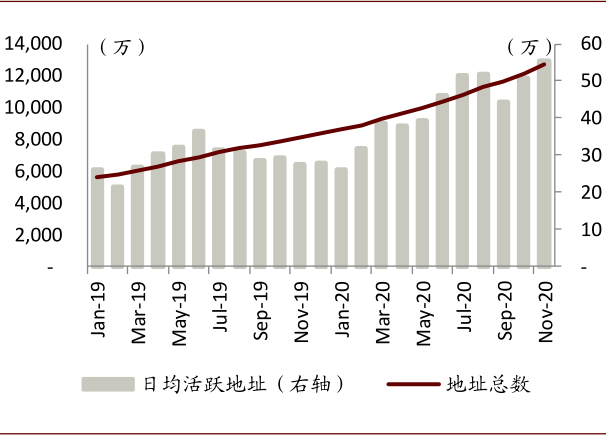

Chart: Total number of Ethereum addresses and daily active addresses since 2019

Source: Etherscan, Coin Metrics, CICC Research

Chart: Daily on-chain transaction count on Ethereum since January 2019

Source: Etherscan, CICC Research

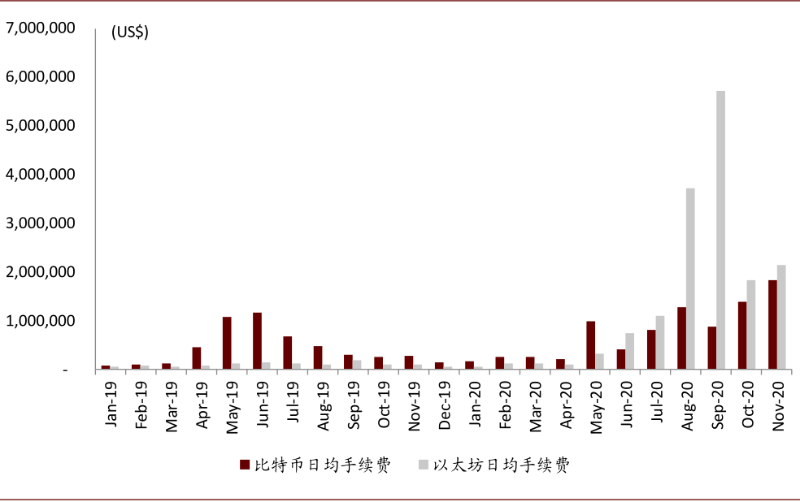

Chart: Ethereum transaction fees have exceeded Bitcoin’s for six consecutive months

Source: Coin Metrics, CICC Research

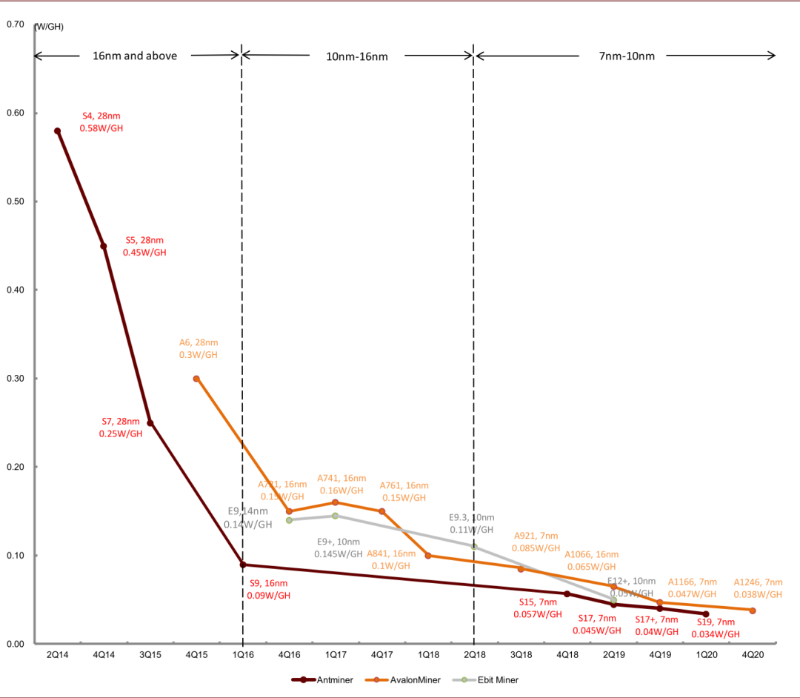

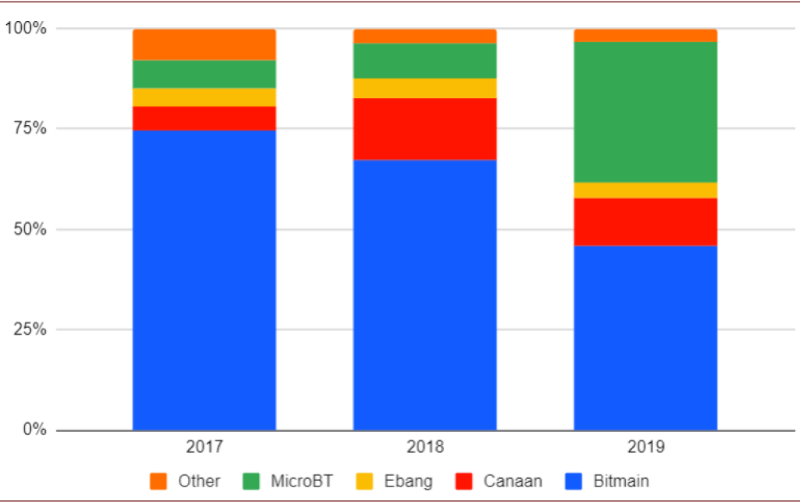

Mining hardware: from 16nm to 7nm, from monopoly to duopoly plus multiple strong players

Chart: Evolution of mainstream mining hardware performance

Source: Zhongguancun Online, CICC Research

Chart: Market share of ASIC mining equipment manufacturers (by TH/s sold), 2017–2019

Source: BitMEX Research, CICC Research

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News