Morgan Stanley Research Report Analysis: NAND Industry AI and Consumer Divergence, Target Prices for Three Stocks Significantly Raised

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: NAND Industry AI and Consumer Divergence, Target Prices for Three Stocks Significantly Raised

Whether short-term NAND price hikes can translate into individual stock rating upgrades hinges on whether the company is moving towards areas with greater pricing power, such as AI servers and enterprise storage.

By: Rita

TechFlow Guide

Morgan Stanley updated its NAND industry supply and demand model on July 2, judging that AI demand will continue to create a shortage, which will last until 2027, but the situation on the consumer electronics side is already quite different. After several rounds of price increases in the second quarter, Morgan Stanley has begun to see actual order cuts from smartphone and PC clients, and pricing for consumer-grade products may soon hit a ceiling.

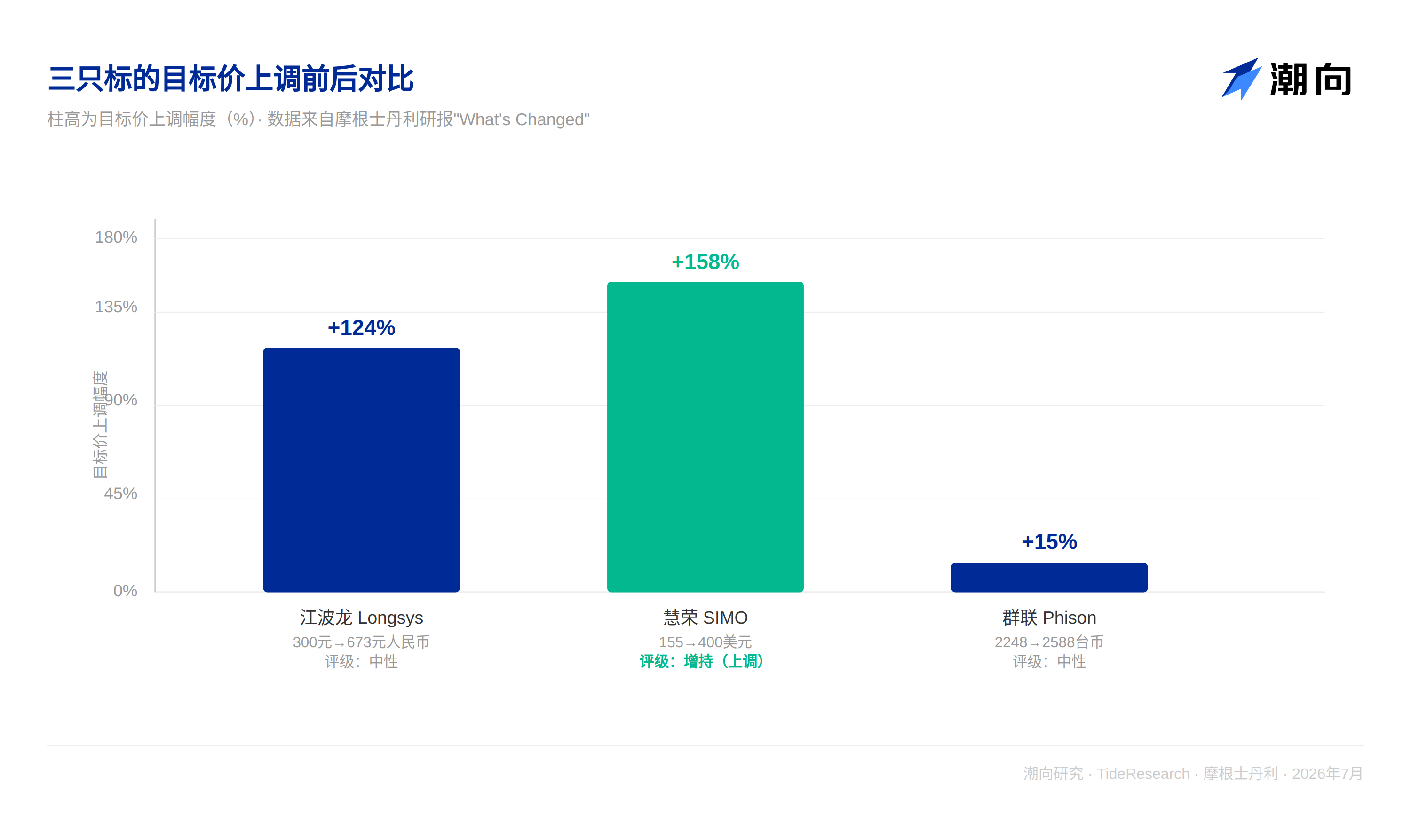

The most direct signal in this update is that the target prices for three targets were significantly raised: Shenzhen Longsys (Longsys) target price raised from 300 RMB to 673 RMB, Silicon Motion (Silicon Motion, SIMO) from 155 USD to 400 USD, and Phison (Phison) from 2248 TWD to 2588 TWD. Morgan Stanley maintained a Neutral rating for Longsys and Phison; the target price went up, but the rating judgment didn't change, the logic is worth dissecting.

Continuous Shortage on AI Side, Consumer Side Has Started to Brake

Morgan Stanley updated the global NAND supply and demand forecast for 2026 to 2027, and conducted a scenario test for greenfield expansion and AI demand growth for 2028. The calculation results show that a significant supply shortage will continue until 2027; entering 2028, with process migration and new capacity release, the gap is expected to narrow. If AI-related NAND demand grows 60% year-on-year and capacity expansion meets the current baseline scenario, the gap can narrow to around 5%, but in a pessimistic scenario where China restrictions relax and supply discipline loosens, there is instead a risk of oversupply.

Overall demand on the server side remains strong, and Long-Term Agreements (LTA) provide downside protection for prices. The situation on the consumer side is clearly differentiated: inventory levels at module manufacturers and distributors are rising, and smartphone and PC clients are under increasing pressure to balance shipment volumes and profit margins. Morgan Stanley points out that this is not a new change, but after price increases in the second quarter, actual order cuts are beginning to be seen, and pricing for consumer-grade products may really peak in the short term. Suppliers are still tilting capacity towards AI, and consumer-side shipment volumes will continue to be suppressed.

Supply and Demand Model: 2027 Gap Not Eliminated, 2028 Depends on the YMTC Card

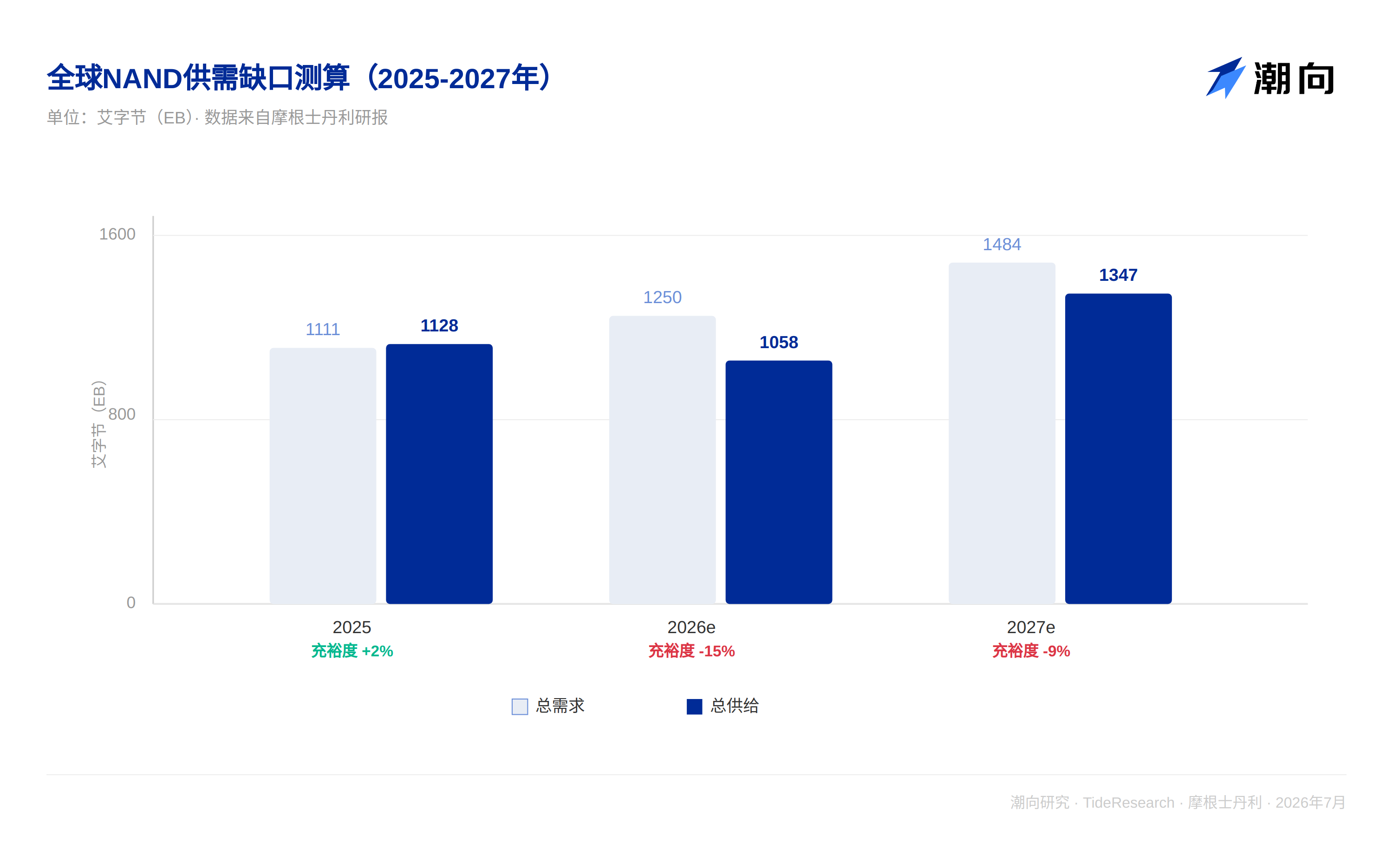

Morgan Stanley calculates that AI-related NAND demand growth rate in 2027 will be about 60% year-on-year, bringing a 9% supply-demand gap. According to the report's model, global NAND total demand will grow from 1111 exabytes to 1484 exabytes from 2025 to 2027, while total supply will grow from 1128 exabytes to 1347 exabytes during the same period. Supply sufficiency will slide from positive 2% in 2025 to negative 15% in 2026 and negative 9% in 2027. AI's share of total NAND demand will also rise from 18% to 41%.

Morgan Stanley believes the biggest variable in 2028 is YMTC. This Chinese NAND manufacturer is currently building two factories, Fab4 and Fab5, each with a planned capacity of 100,000 wafers/month. If all allocated to NAND, plus the five already announced factories, theoretically it could capture 24% of the global NAND industry market share. Scenario testing shows that if YMTC capacity is controlled at the baseline level of 310,000 wafers/month and AI-related SSD demand grows 60% year-on-year, the supply gap can be maintained at around 6%; but if the five factories' capacity is fully maximized to 470,000 wafers/month, while AI demand growth slows to 30%, there would instead be an oversupply of close to 9%. Whether supply is tight largely depends on whether Chinese manufacturers are willing to hit the brakes.

Target Prices for Three Targets Surge, Ratings Remain Unmoved

Longsys target price was raised from 300 RMB to 673 RMB, due to pricing trends being better than expected, and Morgan Stanley has higher confidence in the judgment of the 2027 gap, expecting its EPS for 2026 to 2028 to be raised 299%, 247%, 244%. Phison target price was raised from 2248 TWD to 2588 TWD, Q2 performance greatly exceeded expectations, Q3 is expected to be the yearly high, but Morgan Stanley believes this strength is more cyclical. In Q4, as low-cost inventory is exhausted and consumer electronics weaken, revenue and gross margin will both decline significantly. Morgan Stanley maintained a Neutral rating for both companies, reasoning that module manufacturers have limited bargaining power in this cycle, suppliers have already tilted capacity towards cloud vendors, and module manufacturers' shipment growth is limited.

The situation for Silicon Motion is different. Target price raised from 155 USD to 400 USD, corresponding to a 2027 expected P/E ratio of 23 times, higher than its historical average of 20 times since 2019. Morgan Stanley is optimistic about Silicon Motion's expansion from consumer controllers towards enterprise SSDs and AI server boot drives, expecting boot drive and related SSD business to account for 23% and 26% of its total revenue in 2026 and 2027 respectively. The share of enterprise SSD business MonTitan will increase from 5% in 2026 to 19% in 2028. This is also the only one of the three targets where Morgan Stanley raised both the rating and target price simultaneously.

Who Morgan Stanley Is Most Bullish On

In the DRAM camp, Morgan Stanley lists Samsung Electronics as the Asian Tech Team's top pick, due to market leadership and stronger shareholder return potential; in the NAND camp, Kioxia is the Japan Semiconductor Team's top pick. Morgan Stanley expects its annualized free cash flow for fiscal years 2027 to 2028 to reach 400 billion to 500 billion yen, and management has also hinted that a significant portion of accumulated cash flow may be returned to shareholders. Macronix is the Greater China Semiconductor Team's top pick, benefiting from continued tight supply of SLC/MLC NAND. Morgan Stanley simultaneously maintains Overweight ratings for Micron, SK Hynix, SanDisk, and names Phison as SanDisk's key enterprise SSD controller supplier, believing it is turning from a recovery story to a structural growth story.

TechFlow Perspective

The most worth pondering part in this adjustment is that Morgan Stanley handled the rating and target price as two separate things. Longsys and Phison target prices both rose by double digits, but ratings remained unchanged, indicating Morgan Stanley acknowledges short-term pricing is indeed better than expected, but does not believe this can change the bargaining position of module manufacturers in the industry chain. The only one with synchronized rating and target price upward adjustment is Silicon Motion. The core supporting its rise is the expansion of new businesses like enterprise SSDs and AI boot drives, not just riding the tailwind of this round of NAND price increase cycle. For investors, the signal conveyed by this report is: whether short-term NAND price increases can be realized into individual stock rating upgrades depends on whether the company is moving towards directions with more bargaining power like AI servers and enterprise storage, rather than simply capturing benefits by following the industry cycle price increases.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of third-party brokerage research reports. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, represent only the position of their affiliated institutions, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions need to be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News