JPMorgan Research Report Analysis: $19.2 Billion Power Chip Goldmine, AI Infrastructure's Most Overlooked Bottleneck

TechFlow Selected TechFlow Selected

JPMorgan Research Report Analysis: $19.2 Billion Power Chip Goldmine, AI Infrastructure's Most Overlooked Bottleneck

A value chain obscured by the GPU glow is surfacing.

Written by: Rita

TechFlow Guide

JPMorgan Chase used first principles to deduce the complete power supply chain for AI data centers. Core conclusion: The AI power semiconductor market will be approximately $2.7 billion in 2025, surging to $19.2 billion in 2028, with a three-year CAGR of 82%. A larger variable is the 800V high-voltage direct current architecture revolution, replacing traditional electromechanical equipment with silicon carbide solid-state transformers and gallium nitride converters, causing semiconductor content per watt to jump from $175 to $260. This means a value chain obscured by the glow of GPUs is emerging.

Behind 80 GW of Computing Power, Every Watt Must Run a Five-Stage Relay

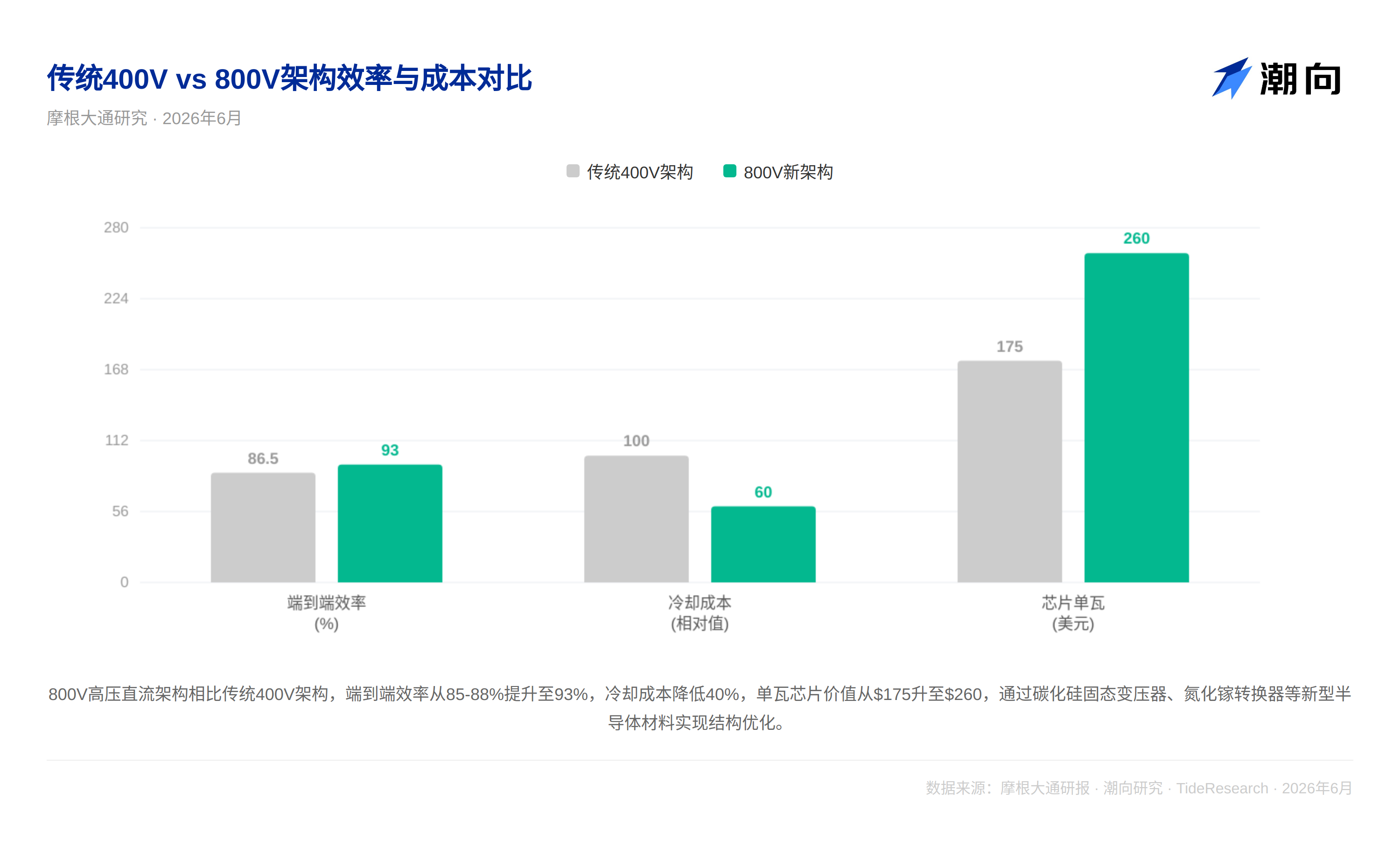

Everyone is calculating GPU shipments, but few are calculating electricity. Currently, data center power supply is a long chain with low efficiency: 10-35kV AC from the grid is first stepped down to 400-480V via transformers, then enters UPS uninterruptible power supply, passes through PDU power distribution units, to server power supplies converting AC to DC, and finally regulated by VRM to the sub-volt level voltage required by the GPU core. Five stages of conversion, each losing 2-5%, result in end-to-end efficiency of only 85-88%. For a single rack of 100kW, 15kW becomes waste heat, all of which must be carried away by the cooling system.

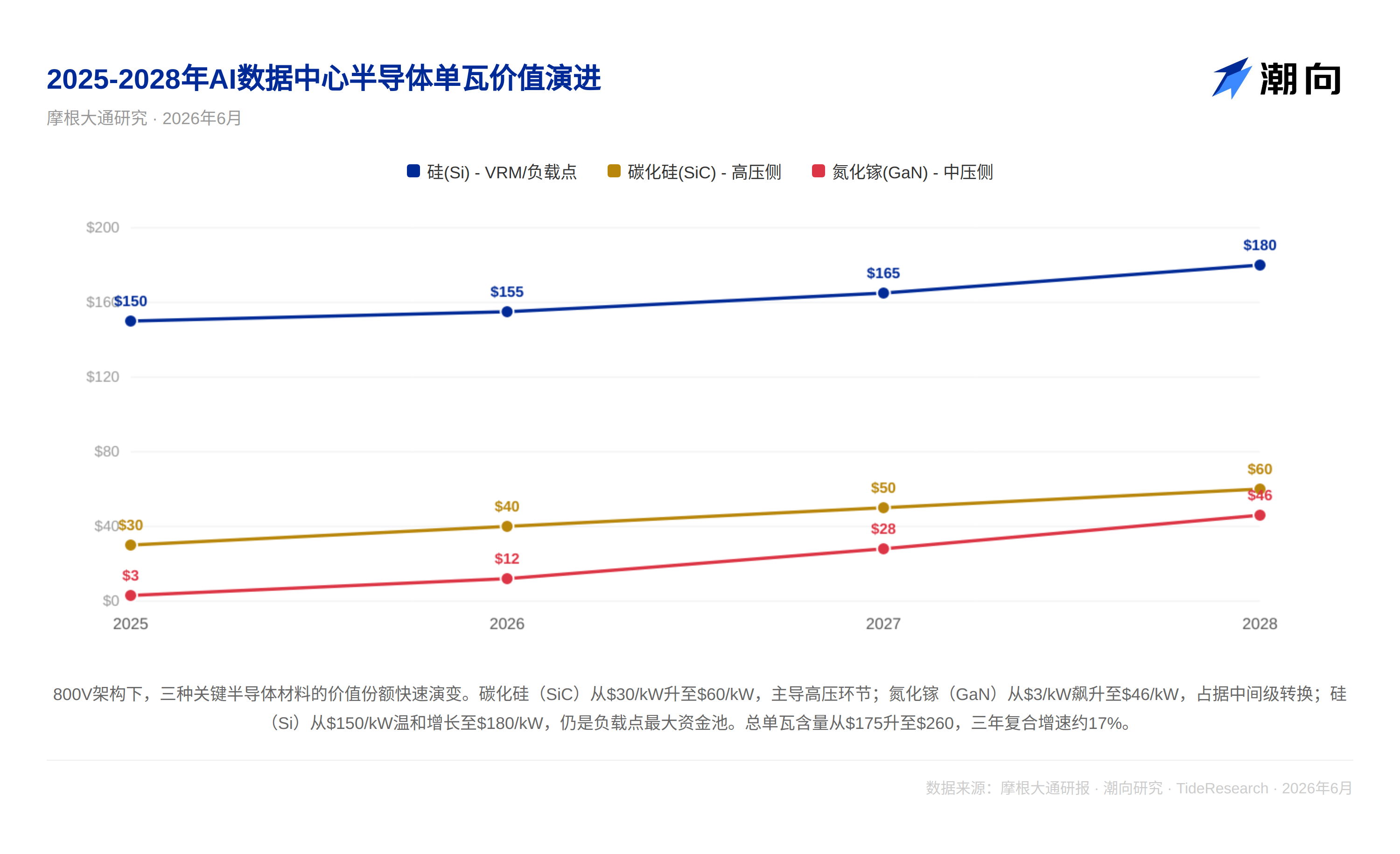

Based on internal AI server model calculations, JPMorgan Chase estimates that by 2028, global AI data centers will add approximately 81 GW of installed capacity, including about 63 GW of new construction and 18 GW of replacements. AI chip power consumption accounts for about 54 GW, reaching the final figure after adding network equipment and PUE coefficients. For the power semiconductor market supporting this 81 GW, the report estimates semiconductor content per watt will rise from the current $175 to $260, driving the total market to $19.2 billion.

800V Architecture Revolution: Voltage Doubles, Chips Triple

The report's core technical insight is the replacement of traditional AC architecture with 800V high-voltage direct current (HVDC) architecture. The physical logic is simple: power equals voltage times current, and heat loss is proportional to the square of the current. Increasing voltage from 400V to 800V halves the current, reducing copper loss to one-quarter. However, the true significance of the architecture switch lies in the qualitative change in semiconductor content.

In traditional architecture, many links are electromechanical equipment, with semiconductor concentration focused on PSU and VRM. The 800V architecture introduces four new nodes: silicon carbide (SiC) solid-state transformers replacing traditional copper-wound transformers; silicon carbide solid-state circuit breakers achieving microsecond-level fault interruption; DC-native battery backup units with bidirectional DC-DC converters and BMS chips; and rack-level 800V to low-voltage DC-DC conversion.

The report provides a clear timeline: 2026-2027 will still be dominated by traditional 400V architecture, but renovations have begun, with sidecar power racks and power racks appearing successively. From the second half of 2027 to 2028, Nvidia Kyber racks (600kW per rack) will drive the scaled deployment of 800V native solutions. After 2028, solid-state transformers will mature, merging sidecar power racks plus transformers into a single SST device.

SiC Takes High Voltage, GaN Takes the Middle, Silicon Holds the Last Line

The report provides a quantitative path for share changes of different semiconductor materials. Silicon carbide content per watt will rise from the current $30 to $60 long-term, dominating the high-voltage link from grid to rack. Gallium nitride (GaN) will surge from $3 to $46, winning out in the intermediate stage conversion from 800V to low voltage. Silicon will grow moderately from $150 to $180, still occupying the largest capital pool of VRM/load point, defending its position via cost-performance ratio.

The key player landscape is also taking shape. Infineon (strongest full-chain layout), MPS (VRM leader, Nvidia core supplier), and Renesas occupy the largest share in intermediate stage conversion and load point links; Nvidia has selected several of them as suppliers. The report covers 12 core companies one by one: Infineon, MPS, Renesas, TI, STMicroelectronics, Navitas (GaN technology leader), ADI, onsemi, ROHM, Innoscience, AOS, and Wolfspeed.

TechFlow Perspective

The core value of this JPMorgan Chase report lies in framework building, rather than giving a specific target price. The scale of $19.2 billion is not large in the overall AI infrastructure, but the key point is: without enough power semiconductors, no matter how many GPUs, they cannot run.

The report has two assumptions that are not fully expanded. First, there is a serious mismatch between the delivery cycle of grid expansion (median 3-5 years in the US) and the two-year construction cycle of data centers; the 2028 installed capacity forecast of 81 GW may face execution risks on the grid side, meaning the US grid's upgrade capability cannot keep up. Second, Nvidia holds the pricing power over the entire value chain; whoever it selects as the power supplier for the Kyber rack directly affects the competitive landscape. JPMorgan Chase itself has investment banking relationships with covered companies such as Infineon and STMicroelectronics, and this background should be considered when looking at specific company recommendations.

Disclaimer

This article is a compilation and interpretation of third-party brokerage research reports by TechFlow Research. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, represent only the position of their affiliated institutions, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News