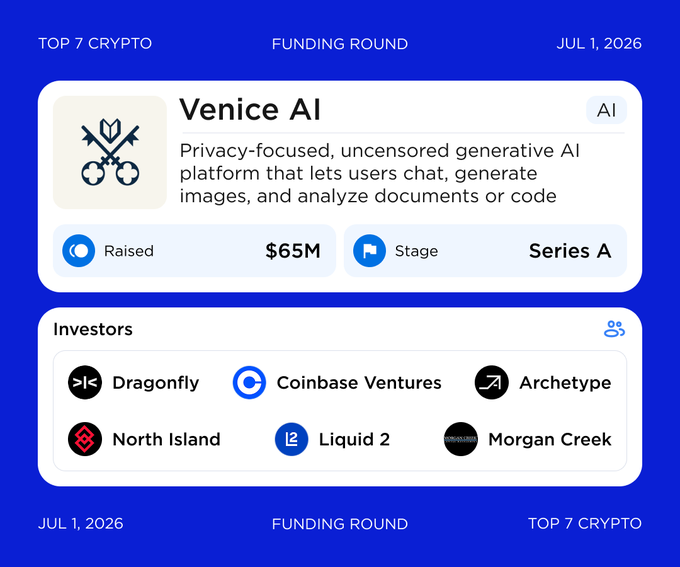

Venice AI Completes $65 Million Funding Round at $1 Billion Valuation, Founder Vows "No Token Sales", Will $VVV See a New Catalyst?

TechFlow Selected TechFlow Selected

Venice AI Completes $65 Million Funding Round at $1 Billion Valuation, Founder Vows "No Token Sales", Will $VVV See a New Catalyst?

Crypto projects raise funds to build their own data centers.

Author: Claude, TechFlow

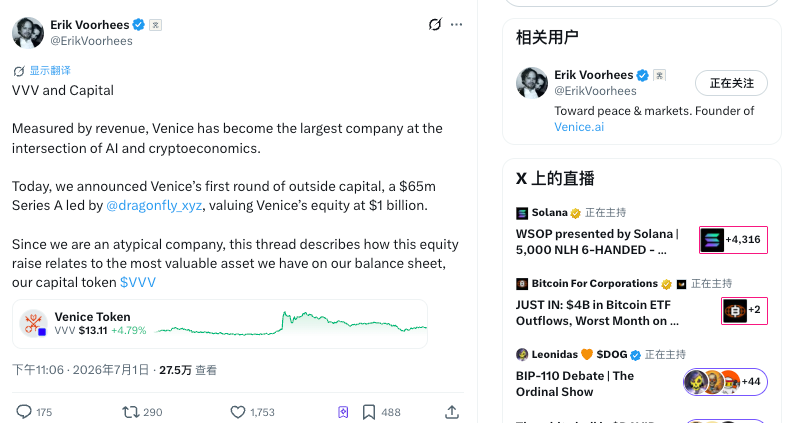

TechFlow Insight: Privacy AI platform Venice completed its first external funding round of $65 million, reaching a $1 billion valuation to become a unicorn, led by Dragonfly with Coinbase Ventures participating. For VVV holders, the real highlight is not the money, but the equity + token hybrid structure of this round: Founder Erik Voorhees emphasized that the team has not sold a single coin, will continue to buy back and burn, and reduce issuance; however, investors hold warrants to buy 5 million VVV within 8 years, exercisable starting after one year, with about 6,000 new coins entering the market daily. After the news was announced, VVV rose accordingly, and the market interpreted it as positive.

Erik Voorhees' Venice has secured its first external funding since inception.

According to The Block, this privacy AI platform built by ShapeShift founder Voorhees completed a $65 million Series A funding round at a $1 billion valuation. Crypto VC Dragonfly led the investment, with Coinbase Ventures, North Island Ventures, F-Prime, Archetype, Liquid2 Ventures, Morgan Creek, and others participating. This is the first time Venice has introduced external capital since launching two years ago; previously, it neither conducted VC private placements nor monetized the VVV tokens in its treasury.

Equity + Token Dual-Layer Structure, Investors Take Nearly 9% Equity Plus Two Batches of VVV

Voorhees disclosed the full consideration of this round in a long post on X. $65 million bought three things: 8.98% equity in Venice company, vesting rights to 1.5 million VVV tokens, and warrants to buy another 5 million VVV at an agreed price within the next 8 years (warrants).

A warrant is a right to purchase tokens at a future time at an agreed price. According to Voorhees' calculations, if investors exercise all 5 million warrants, they will need to pay Venice another approximately $66.5 million, bringing the actual total fundraising for this round to about $131.5 million. Both token vesting rights and warrants have a one-year lock-up period, followed by linear unlocking over the subsequent three years.

What investors get now is equity, plus an option to "buy coins at an agreed price later," rather than immediately tradable tokens. This structure, bundling equity, token vesting, and token warrants together, is not common in crypto financing; most projects are either pure equity or directly sell coins to VCs.

Founder "Build Product and Token First, Then Bring in VC," Going Against Industry Convention

Voorhees emphasized that Venice chose to sell equity rather than sell tokens from the treasury for financing. He stated that Venice is still the largest holder of VVV, holding over 30 million out of the current total supply of over 80 million; the company and team have not sold a single VVV to date, even though the token has risen over 700% this year.

Venice's financing pace is exactly opposite to industry convention. Most projects presell tokens to VCs under non-public terms, promising to build products and find users later; Venice launched products and tokens first, generated users and revenue, and then introduced external investors.

This strategy is backed by business data. According to company disclosures, Venice reached 3 million users in April and achieved profitability in the first quarter; multiple media outlets cited Voorhees saying its annualized revenue (run-rate) has exceeded $70 million. It is unusual for a Series A-stage AI startup to be profitable before financing.

Warrants Are Future Selling Pressure for VVV, But Pace Calculated by Founder as "Negligible"

For token holders, those 5 million warrants are an unavoidable issue. They are potential future inflation; once exercised, they become new circulating supply, meaning selling pressure.

According to Voorhees' calculations, if investors exercise in full, starting from about one year later, about 6,000 VVV will enter the market daily, equivalent to approximately 0.2% of current daily trading volume. This magnitude is not large relative to market depth. The portion of warrants not exercised corresponds to tokens that remain on Venice's balance sheet and do not enter circulation.

On the token strategy end, Venice states it remains unchanged, continuing to use a portion of revenue to buy back and burn VVV, while gradually reducing token issuance. Burning reduces stock, warrants increase potential supply; the two forces move in opposite directions. Which direction VVV's net supply goes depends on whether the intensity of buyback and burn can outweigh warrant unlocking and regular issuance. This is the core variable token holders need to watch next, more worth tracking than the financing itself.

A reminder here: the figures "6,000 coins daily, accounting for 0.2% of daily trading volume" come from Voorhees' own calculations, belonging to the financing party's self-reporting; TechFlow currently has no independent data for cross-verification, readers should treat this as reference rather than conclusion.

Funds to Be Used for Building Own Compute, Pointing to GPU and First Data Center

According to the founder, the use of this financing round is to build own compute infrastructure, including Venice's first data center, to reduce reliance on leased GPUs.

The logic he gave is that building own compute can lock in capacity amidst "upcoming resource shortages" and increase gross margins, thereby making "larger-scale VVV burning possible."

The implication is that building own compute lowers costs and raises profits, and profits are then used to buy back and burn VVV. Besides compute, Venice also plans to use this money to enter new markets, acquire "synergistic" businesses, hire people, and expand its customer base.

On the product side, Venice is positioned as a privacy, anti-censorship alternative to ChatGPT, claiming not to store user prompts on its own system; requests are forwarded through external proxies after encryption, and paid subscriptions also provide end-to-end encryption. The platform claims to have accessed over 200 AI models, including both self-hosted open-source models and closed-source models like OpenAI and Anthropic called anonymously via API. Besides VVV, Venice also has a DIEM token: users stake VVV to get sVVV, then lock a portion of sVVV to mint DIEM, each DIEM corresponding to $1 worth of API credits on the platform that never expire.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News