Goldman Sachs Research Report Analysis: ASML Target Price Raised to 2,000 Euros, Memory Capital Expenditure Becomes Major Driver

TechFlow Selected TechFlow Selected

Goldman Sachs Research Report Analysis: ASML Target Price Raised to 2,000 Euros, Memory Capital Expenditure Becomes Major Driver

Goldman Sachs simultaneously raised the valuation multiple from 40x to 43x for the 2027 expected P/E ratio, citing a more optimistic outlook on demand for memory and advanced process nodes.

Written by: Rita

TechFlow Digest

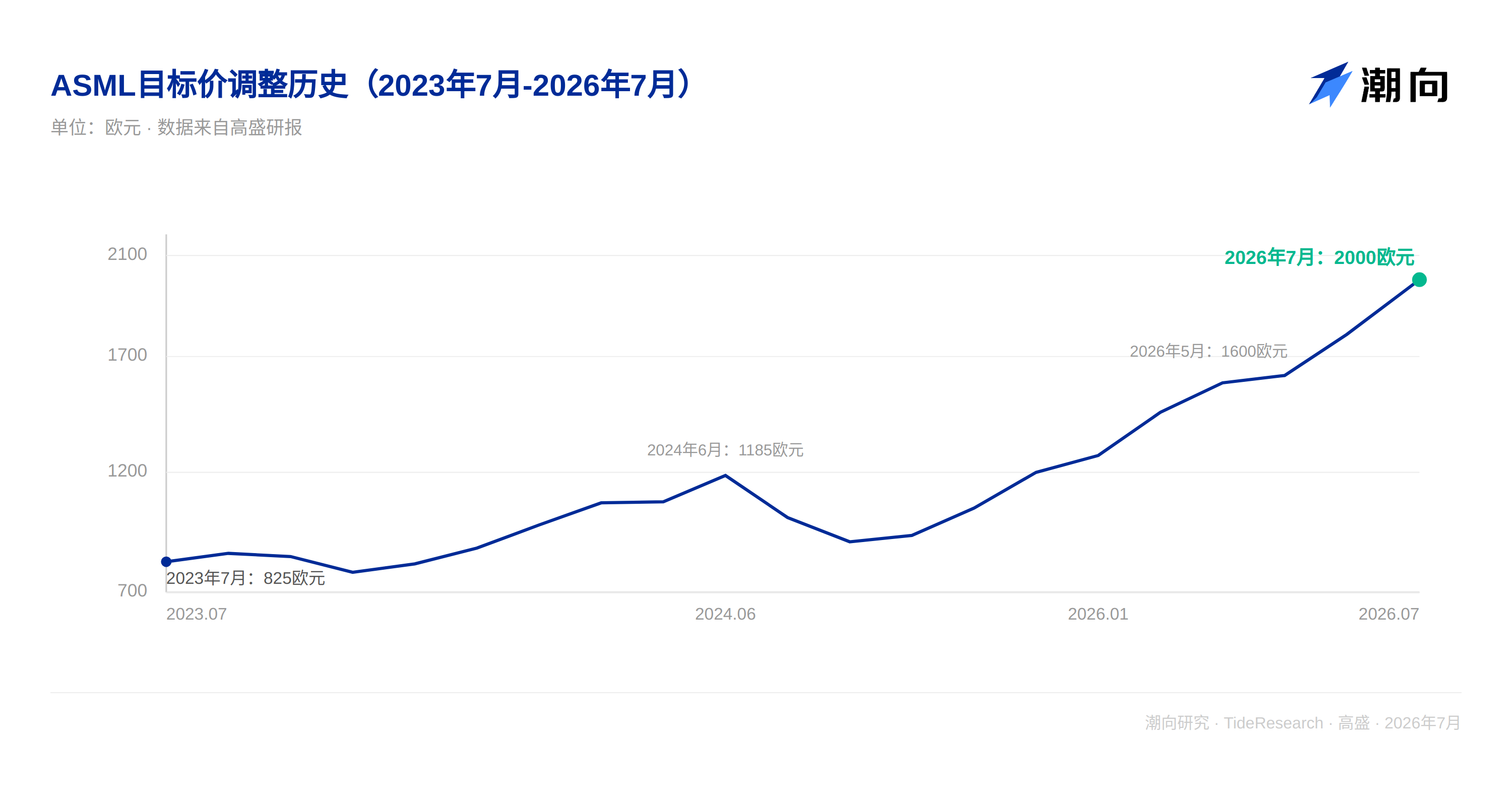

On July 1, Goldman Sachs raised the 12-month target price for ASML from 1,770 euros to 2,000 euros, maintaining a Buy rating. This upgrade did not wait for the Q2 financial report on July 15; the direct trigger was the upward revision of capital expenditure expectations by memory chip manufacturers. Micron and Samsung's latest announced capital expenditure plans were incorporated by Goldman Sachs into its forecasts for ASML's equipment orders over the next few years.

Goldman Sachs also raised the valuation multiple from 40x to 43x the expected P/E ratio for 2027, citing a more optimistic view on demand for memory and advanced processes. Based on the latest closing price of 1,721.40 euros, the target price corresponds to approximately 16.2% upside potential.

Memory Capital Expenditure Significantly Revised Upward

The core data point triggering this upgrade comes from Micron. In its latest quarterly results, Micron provided a fiscal year 2027 capital expenditure guidance of approximately $50 billion. Goldman Sachs calculates this figure is significantly higher than previous expectations, with about half of the incremental amount coming from construction-related capital expenditures. Goldman Sachs believes memory demand continues to outpace supply; such upward revisions in capital expenditure will drive a multi-year capacity expansion cycle, which is positive for semiconductor equipment manufacturers. ASML benefits more significantly due to its relatively higher exposure in the memory sector and EUV equipment delivery cycles exceeding 12 months. Samsung also announced an investment plan of approximately 2,450 trillion Korean won over the next 15 years (2026 to 2040), with about 76% directed towards semiconductors. Although Samsung did not disclose the specific breakdown between capital expenditure and R&D, Goldman Sachs believes this long-term investment constitutes a substantive benefit for ASML.

China Market to Digest This Year, Expected to Rebound Next Year

Goldman Sachs believes the company's statements regarding the China market this year may be conservative, as demand in the region remains strong and statements from other semiconductor equipment peers are also relatively positive. However, Goldman Sachs also acknowledges that part of the capacity shipped to China last year needs time to be digested this year. Looking ahead, tight supply and demand in traditional memory gives Chinese manufacturers room to grab share in the overseas basic memory market, which will drive further capacity expansion; once the digestion period ends, the China market is expected to see additional spending in 2027, bringing a new round of equipment orders in conjunction with local fab construction plans.

Customer Structure Improving, EUV Demand Also Rising

Goldman Sachs points out that advanced process customers outside of TSMC are accelerating their catch-up, which is consistent with the logic in previous reports judging ASML's stock price as undervalued. AI-driven new players may also bring additional demand increments, especially some large-scale infrastructure construction projects, where the implied equipment procurement scale could be considerable. Additionally, as advanced processes complete the transition to Gate-All-Around (GAA) transistors, the number of EUV layers will continue to increase. Micron recently signed a multi-year EUV supply agreement with ASML for the 1-delta process node and subsequent generations, which also confirms the judgment that EUV demand is rising.

Goldman Sachs lists four issues investors will continue to focus on: First, the 2027 EUV and DUV capacity planning; the company historically prepares the supply chain for 90 units of equipment, and if cycle time and delivery progress are further optimized, output could slightly exceed 90 units; Second, whether there are new developments in 2028 orders; Third, the latest situation in the China market; Fourth, the adoption pace of High NA equipment. Goldman Sachs believes memory customers may adopt High NA faster than logic chip customers, and seeing relevant order evidence would be a positive signal.

Earnings Forecast and Valuation

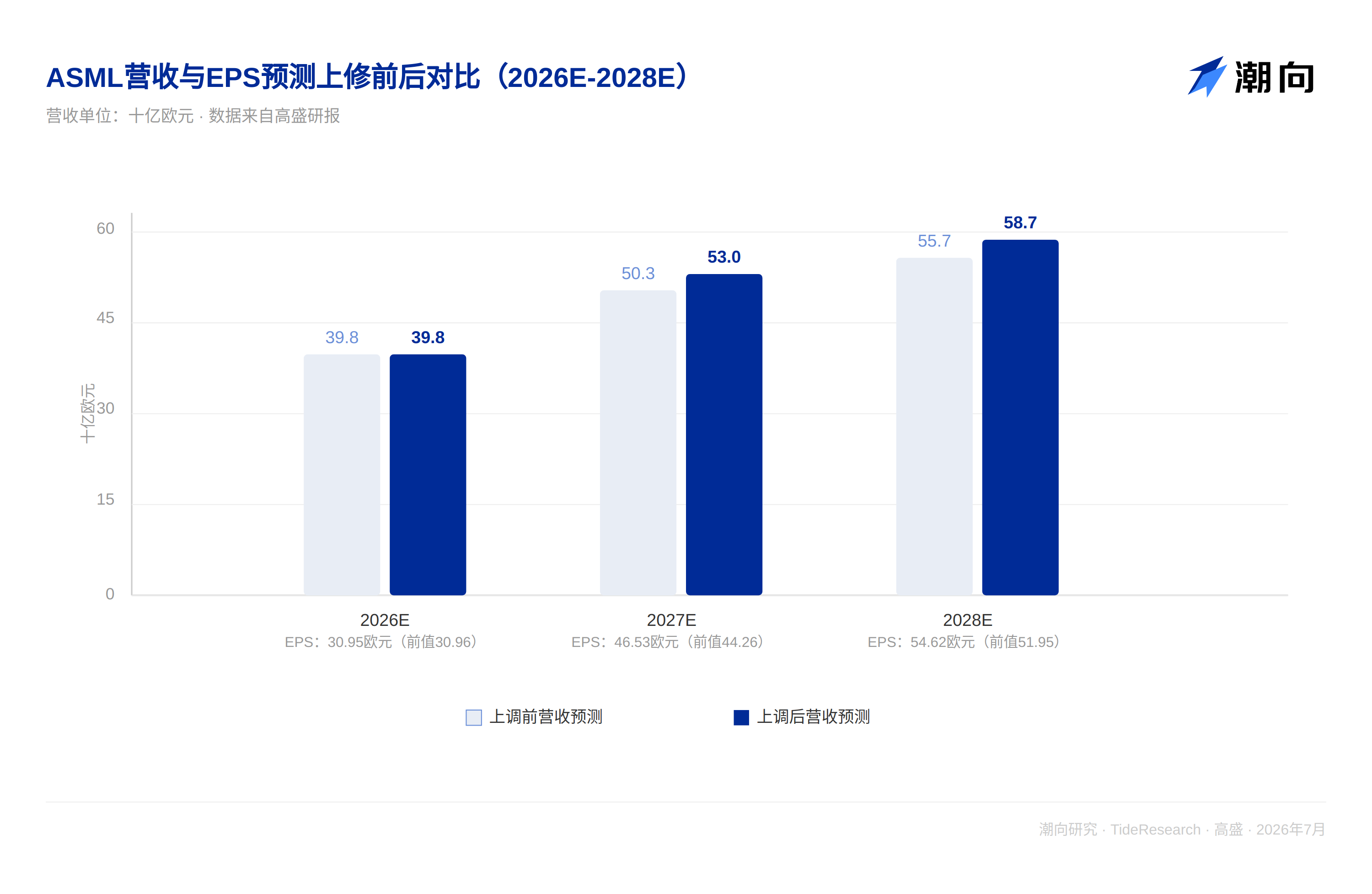

Goldman Sachs maintains its fiscal year 2026 revenue forecast unchanged but raises the revenue forecast for fiscal years 2027 to 2030 by 5% to 9%, reflecting a more positive judgment on advanced process demand (especially memory capital expenditure), and is also more optimistic about ASML's DUV business, reasoning that the China market is expected to recover in 2027. Correspondingly, the EBIT forecast for fiscal year 2026 remains unchanged, while the EBIT forecast for fiscal years 2027 to 2030 is also raised by 5% to 9%; earnings per share forecast is raised by 5% to 8% within the fiscal year 2027 to 2030 range.

Goldman Sachs gives a target price of 2,000 euros, previously 1,770 euros, corresponding to 43x the expected P/E ratio for 2027 (previously 40x). The upward revision of the valuation multiple reflects a more optimistic judgment on growth prospects for the next few years. Based on the latest forecasts, ASML's current stock price corresponds to approximately 32x the expected P/E ratio two years later, within the long-term historical range of 25x to 35x. Main risks include EUV equipment delivery delays, cyclical fluctuations in capital expenditure, and unfavorable changes in market share.

TechFlow Perspective

Behind this upgrade, actually two lines are at play. One is that Goldman Sachs incorporated Micron and Samsung's capital expenditure expectations into its own revenue model; such capital expenditure commitments spanning over a decade themselves have great elasticity, and there is still considerable uncertainty whether Micron and Samsung's actual investment progress will be realized according to plan. The other is that Goldman Sachs itself raised the valuation multiple from 40x to 43x; this part belongs to paying a higher price for the same earnings forecast, not entirely supported by earnings upward revisions. The Q2 financial report will be published on July 15; this adjustment is essentially digesting external industry signals into the model before the performance announcement, and true validation still awaits the order and outlook data in the financial report.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of third-party securities firm research reports. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the securities firm's analysts, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market carries risks; decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News