Bernstein Analysis: Does Meta Really Have Excess Computing Power to Sell? Nearly Half of CoreWeave's Orders Held by "Future Rivals"

TechFlow Selected TechFlow Selected

Bernstein Analysis: Does Meta Really Have Excess Computing Power to Sell? Nearly Half of CoreWeave's Orders Held by "Future Rivals"

Placing the arguments of both the long and short sides on a timeline, the disagreement is actually not at the factual level.

Author: Claude, TechFlow Research

The news of Meta building a cloud business has been digested by the market; after CoreWeave's 14% drop, the real question has surfaced.

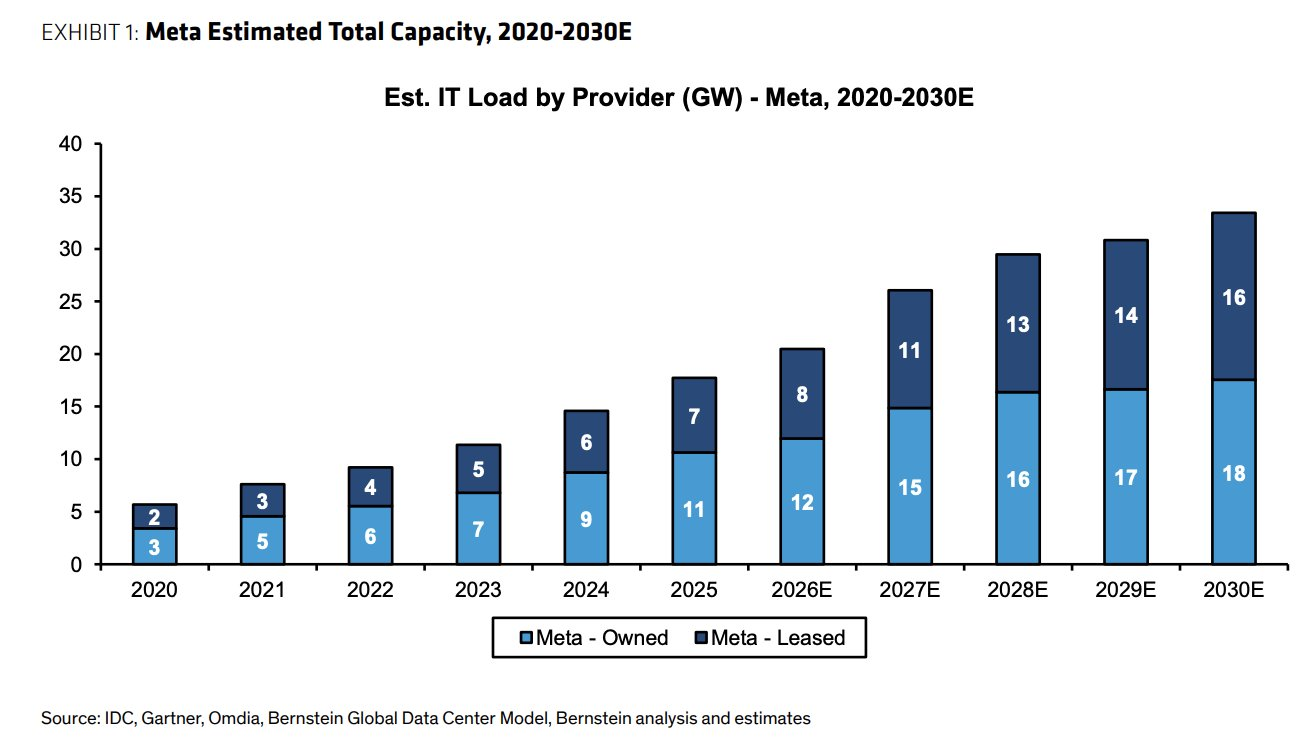

Bernstein estimates Meta currently has about 20GW of data center capacity, with approximately 14GW more to be added in the coming years, a scale comparable to major cloud providers. However, the fact that Google has restricted Meta's Gemini usage since March casts doubt on the premise that "Meta holds excess computing power."

Does Meta actually have excess computing power to sell, and how much is CoreWeave's order book worth in a world where "customers become competitors"? Bernstein analyst Madison Rezaei's latest report puts these two accounts on the table.

20GW Existing, 14GW Under Construction: Meta's Scale is Enough to Launch a Cloud Provider

Rezaei estimates Meta's current global data center footprint is about 20GW, with approximately 14GW coming online in the coming years, spanning both owned and leased assets. According to Bernstein's model, Meta's IT load has expanded from 5GW in 2020, reaching about 18GW in 2025, and is estimated to reach 34GW by 2030, of which 18GW is owned capacity and 16GW is leased capacity.

What does this figure mean in the context of the industry?

CoreWeave's contracted power as of the end of the first quarter was about 3.5GW, with activated capacity just over 1GW, targeting 1.7GW by the end of the year. Meta's incremental part alone for the coming years is equivalent to ten times CoreWeave's current scale. Rezaei judges based on this that Meta's infrastructure "can be directly compared to major cloud providers." Once it decides to open this capacity to the outside and compete head-on with AWS, Azure, and GCP, it is structurally bad news for CoreWeave.

Capacity is the entry ticket, but an entry ticket does not equal chips on the poker table. The other side of this account is Meta's current computing power situation.

Restricted by Google on One Side, Claiming Surplus on the Other: The Two Things Don't Add Up

According to the UK "Financial Times", due to its own insufficient computing power, Google has restricted Meta's purchase usage of the Gemini model since March. Some of Meta's internal AI projects have been delayed as a result, and the company has asked employees to conserve AI tokens.

Meta signed a six-year, over $10 billion cloud agreement with Google in August 2025, yet now it cannot even fill the capacity within the agreement. Additionally, Meta signed with Crusoe in June this year to lock in 1.6GW of new AI computing power, and first-quarter capital expenditure guidance was adjusted upward simultaneously.

One company is doing three things simultaneously: scrambling to buy computing power externally, being rate-limited by suppliers, and planning to sell computing power externally. Rezaei believes this set of contradictions precisely constitutes a challenge to the claim of "excess capacity"; Meta may not truly have a surplus now.

The reconciling explanation in the market is layered scheduling. Meta reserves the latest generation clusters for frontier model training, what is brought out for monetization is capacity freed up by previous generation GPUs and non-core loads, and what is bought from Google is inference services for off-the-shelf models like Gemini; the three are not in the same pool. Morgan Stanley calculates based on this logic that if Meta rents out 250MW, priced at $40 per watt, it could add about $2.97 to earnings per share for 2028, corresponding to about 8% upside.

The position implications pointed to by the two interpretations are completely different.

If Rezaei's suspicion holds, Meta's cloud business will not land in the short term, and CoreWeave's sell-off is an overshoot; if layered scheduling holds, Meta uses old computing power to earn new money, and pressure will continue to weigh on the valuation of the entire emerging cloud sector. The only way to distinguish is to wait for Meta's official announcement and look at two details: whether what is opened is raw computing power or hosted models, and whether the pricing competes closely with CoreWeave or is significantly higher.

CoreWeave Order Book Breakdown: Nearly Half of Backlog Held in Future Competitors' Hands

More worth looking into than "whether Meta sells" is the structure of CoreWeave's order book itself.

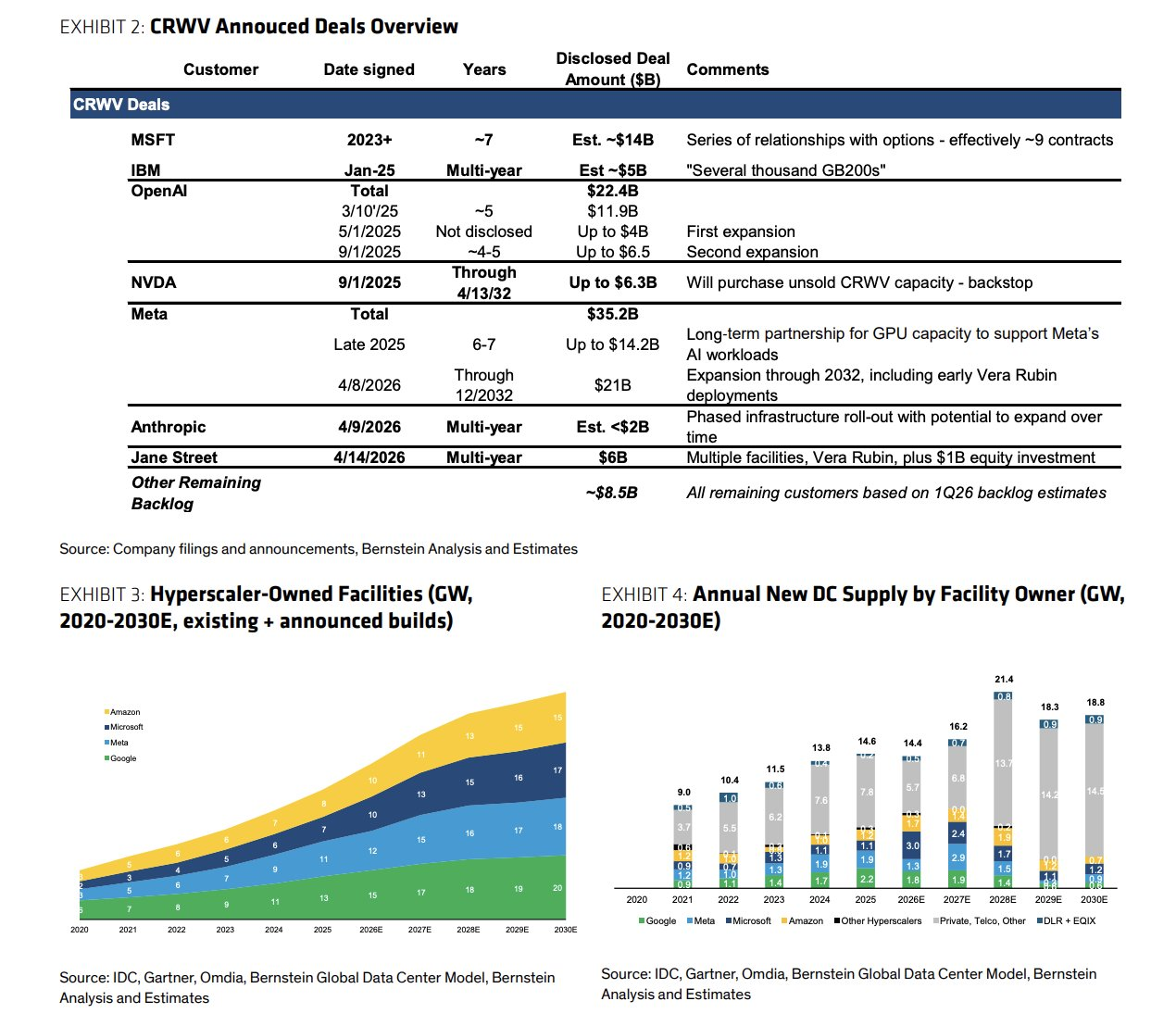

According to CoreWeave's disclosure, as of March 31, its backlog was about $99.4 billion. Bernstein's breakdown shows Meta alone accounts for about $35.2 billion ($14.2 billion in September 2025 plus $21 billion expansion in April 2026, contract until December 2032, including early deployment of Nvidia Vera Rubin), accounting for over one-third; Microsoft accounts for about $14 billion, spread across about 9 contracts. Added together, nearly half of the backlog comes from clients who are highly likely to be direct competitors at the time of renewal.

The rest of the order book includes OpenAI at about $22.4 billion, Jane Street at $6 billion (plus another $1 billion equity investment), Nvidia's $6.3 billion backstop agreement (take-or-pay acquisition of unsold capacity before 2032), and Anthropic's multi-year contract with an undisclosed amount, estimated by Wall Street in the $4 billion to $7 billion range.

Another analyst, McPeake, stated that Meta does not have the contractual right to resell capacity rented from CoreWeave before 2032. Before 2032, CoreWeave's cash flow is locked.

The problem lies after 2032. Rezaei's deduction is that by then, Meta and Microsoft's self-built capacity will be fully online; those sitting across the renewal negotiation table will no longer be clients eager to buy computing power, but competitors who are also selling computing power. CoreWeave will face both the loss of old clients, and new order pricing power will be suppressed by deeper pockets.

She summarizes this as another example of her consistent argument: "It is only a matter of time before better-capitalized big players enter the GPU rental market; CoreWeave's business model is unsustainable in the long term." The bulls' counterargument is channel data: GPU procurement behavior has not changed, and the industry is still short on cards. McPeake, holding a buy rating, gives a $250 target price, stating the sharp drop provides a buying opportunity.

The Valuation Risk Period Starts Now

Putting the arguments of both bulls and bears on a timeline, the divergence is actually not at the factual level.

Before 2029, CoreWeave has no debt maturity, contracts are locked, first-quarter revenue increased 112% year-over-year, and short-term financial risk is limited; even the bears do not deny this.

From 2031 to 2032, the first batch of large contracts enters the renewal window. Meta and Microsoft's self-built capacity will have reached over 30GW and corresponding scale respectively by then according to Bernstein's estimates. Renewal prices and renewal rates are the real stress test. And market pricing for renewal risk usually starts one to two years in advance, meaning around 2029, the "order quality discount" will begin to be reflected in the valuation.

The current 14% drop can be understood as a rehearsal for this repricing. For CoreWeave holders, track two signals in the short term:

1. The form and pricing of Meta's cloud business official announcement,

2. The proportion of non-mega clients in CoreWeave's subsequent new orders

The latter determines whether the narrative of "half the orders held in competitors' hands" will be diluted or reinforced. For Meta holders, the story of selling computing power has limited financial flexibility; Morgan Stanley's calculated 8% upside is built on a 250MW rental scale, and the reality of being rate-limited by Google indicates that the capacity that can be freed up in the short term probably cannot support a larger narrative.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News