Morgan Stanley Research Report Analysis: Core of Meta Cloud Plan is Leasing Idle Compute Capacity, Overweight Rating, Target Price Raised to $775

TechFlow Selected TechFlow Selected

Morgan Stanley Research Report Analysis: Core of Meta Cloud Plan is Leasing Idle Compute Capacity, Overweight Rating, Target Price Raised to $775

The report points out that Morgan Stanley has assigned an Overweight rating to Meta, supported by the company's structural shift towards multi-year user engagement and efficiency improvements, while cloud computing itself is not the core rationale for the rating.

Written by: Rita

TechFlow Guide

Bloomberg recently cited sources stating that Meta is planning a cloud computing business, covering two areas: model hosting APIs and bare-metal compute rental. Morgan Stanley's judgment on July 1 was direct: the part of this plan involving renting out idle compute is far more reliable than a full cloud service benchmarking AWS. The former does not require large-scale hiring and an enterprise sales team, while the latter carries significantly higher execution risk.

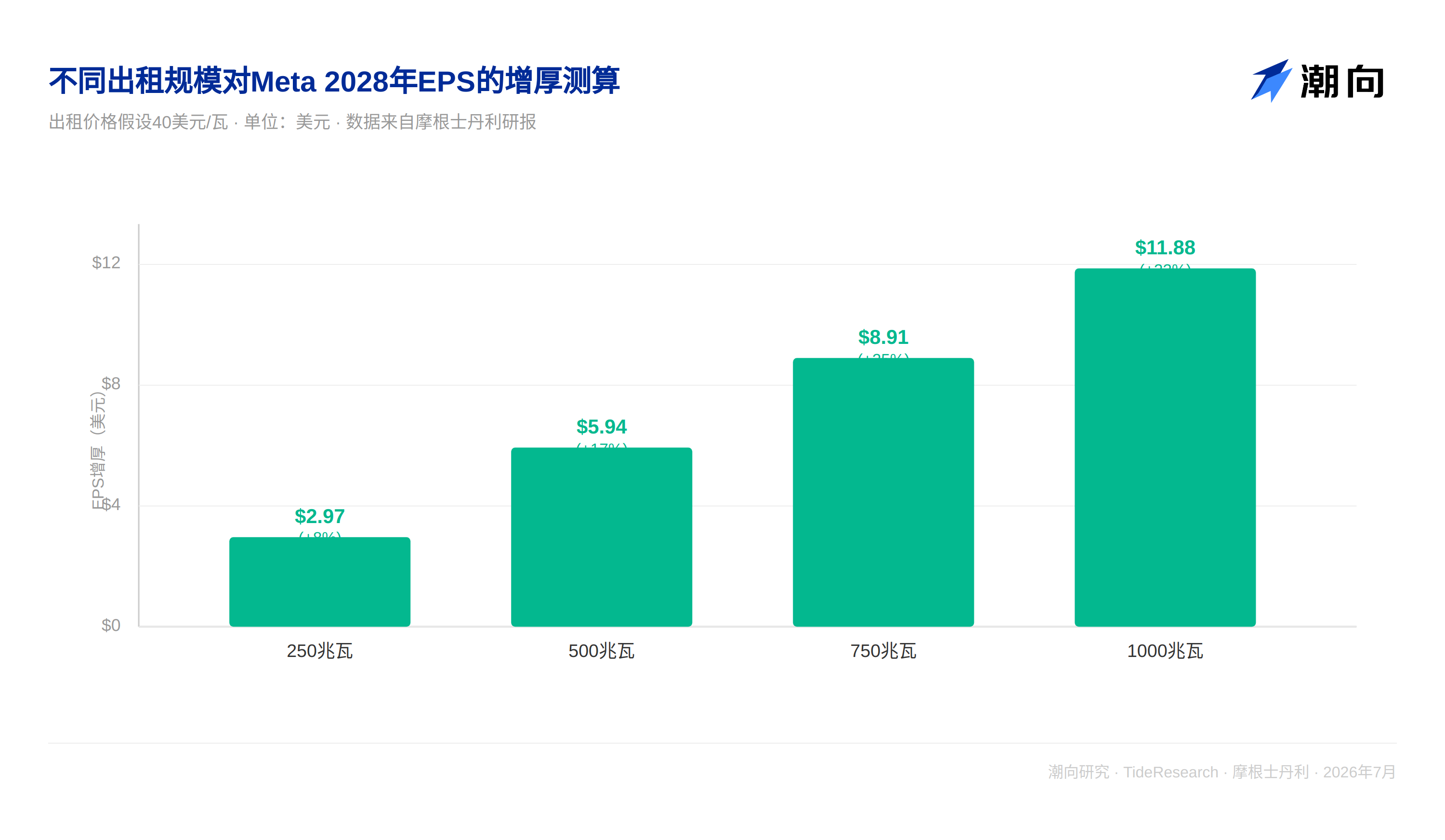

More crucial are the numbers. Renting out 250 MW of compute for a year at a price of $40/watt could boost 2028 earnings per share (EPS) by approximately 8%. When the scale increases to 1000 MW, the boost surges to 33%. However, Morgan Stanley made it clear: the Overweight rating for Meta is not based on optimism about its cloud ventures. The core logic supporting the $775 target price remains structural improvements in efficiency and user engagement.

Two Paths for the Cloud Plan, Significant Difference in Difficulty

The rumored Meta cloud plan falls under the Meta Compute department established this January. It consists of two pieces: one is a model hosting API service for developers, similar to AWS's Bedrock, covering models like Muse Spark; the other is a bare-metal service closer to compute rental. Meta has not commented on this officially so far.

The report points out that the model hosting API business has higher requirements for technology, hiring, and execution. Meta's Muse series models performed averagely on TerminalBench and SWE Bench Verified, two key tests measuring programming and third-party invocation capabilities. There is still a gap to catch up with frontier models like Gemini. Meta also lacks a mature enterprise sales team like AWS, Azure, or GCP. Morgan Stanley believes that a full suite of model-plus-application API services is more like a proof of concept, with risks significantly higher than established cloud providers that have already succeeded. In contrast, short-term rental of idle compute does not require large-scale hiring or building new teams, representing a path with much less resistance.

The Window for Compute Surplus is Just These Two Years

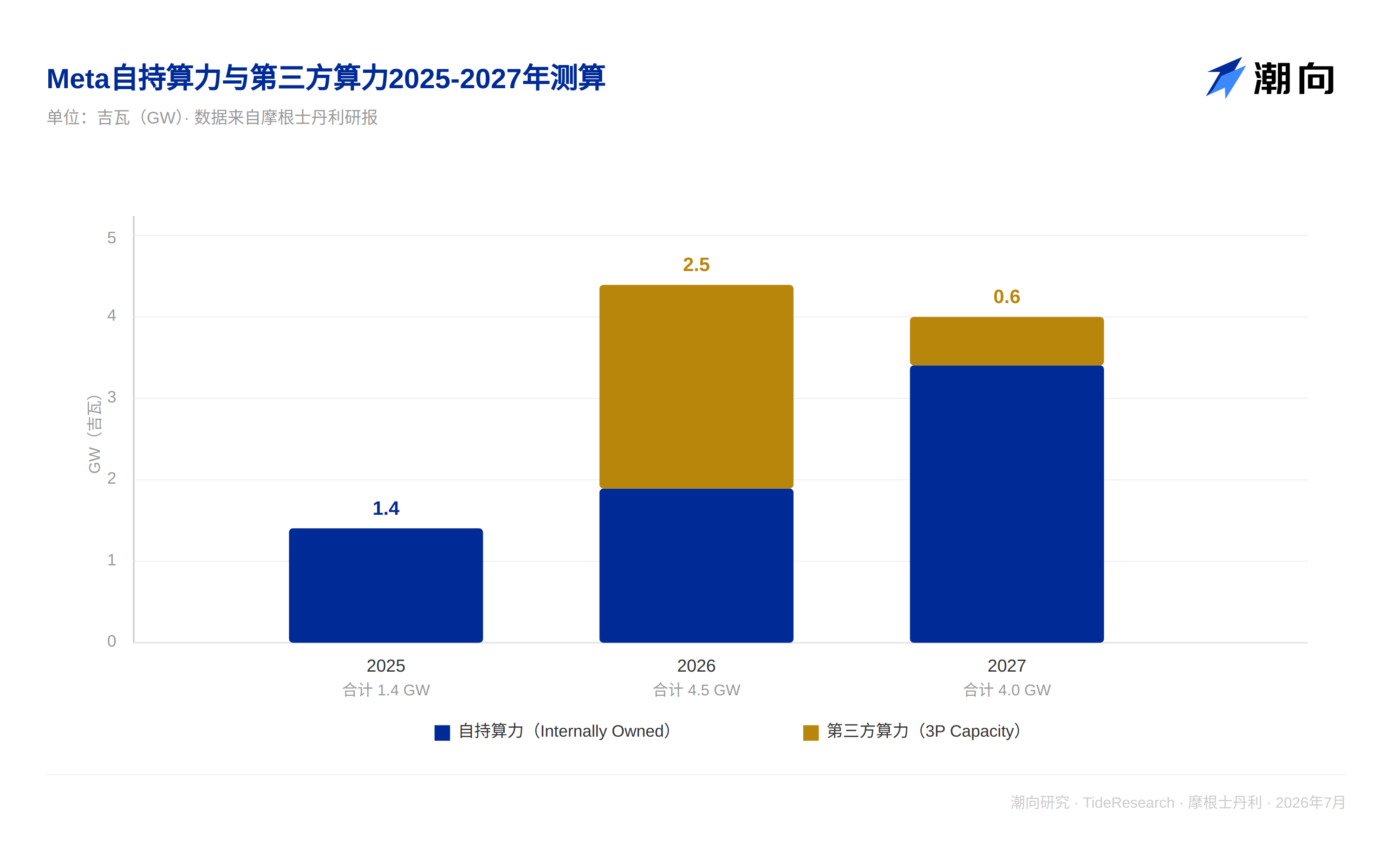

Morgan Stanley estimates that Meta's owned compute capacity will expand from 1.4 GW in 2025 to 1.9 GW in 2026 and 3.4 GW in 2027. For comparison, Amazon and Google are expected to add 5 GW and 9 GW of compute capacity respectively in 2027 alone, which is also the reason Meta theoretically has room for rental. The report estimates that Meta currently rents about 2.5 GW of compute capacity from third parties such as Coreweave, Nebius, GCP, and Oracle. In 2026, this third-party capacity will bring Meta's total callable capacity to 4.5 GW. In 2027, the third-party portion will narrow to 0.6 GW, with a total capacity of about 4.0 GW. Morgan Stanley believes that Meta cannot sublet the third-party compute capacity it rents, but this also indicates the company has retained more flexibility in compute allocation, creating conditions to temporarily rent out the owned portion.

How Much Does Renting Compute Boost Earnings Per Share

Morgan Stanley's sensitivity analysis shows that renting out 250 MW of compute for a year at a price of $40/watt could bring about $3 to 2028 EPS, a boost of nearly 8%. If the rental scale increases to 1000 MW, the boost could reach $11.88, equivalent to 33% upside. The higher the price and the larger the scale, the more obvious the elasticity. Even at a lower price point of $20/watt, renting 250 MW could bring about $1.49, a 4% accretion.

How Capital Expenditure is Calculated

Morgan Stanley's current model assumes Meta's capital expenditure will rise from $145 billion in 2026 to $175 billion in 2027 and $205 billion in 2028, corresponding to approximately 3.5 GW of new compute capacity in 2027. This premise assumes these capacities are mainly used for Meta's own business rather than building a full cloud service system. The report mentions that if Meta truly scales compute rental into a business, there is a possibility of further upward revision in capital expenditure.

Viewed in a broader industry context, Morgan Stanley estimates that the combined capital expenditure of cloud providers and emerging cloud computing companies will expand from $246 billion in 2024 and $433 billion in 2025 to $834 billion in 2026 and $1.2 trillion in 2027. Broken down by 2027, Amazon is approximately $225 billion, Google approximately $350 billion, Meta approximately $175 billion, Microsoft approximately $276 billion, Oracle approximately $108 billion, Coreweave approximately $41 billion, and Nebius approximately $31 billion.

Valuation Level

The report points out that Morgan Stanley gives Meta an Overweight rating. The support point is that the company is structurally shifting towards multi-year user engagement and efficiency improvements; cloud computing itself is not the core reason for the rating. Renting compute is more like a transitional EPS buffer. What truly supports valuation is whether new products like MetaAI, business agents and messaging, and diffusion models can continue to scale, and whether subscription revenue can open new growth curves. A target price of $775 is given, corresponding to 23.1 times the expected 2027 EPS of $34.16, representing approximately 37.6% upside compared to the closing price of $563.29 on June 30. Bull case target price is $1000, corresponding to 28 times; bear case is $450, corresponding to 14 times. The report also mentions that Meta currently trades at a P/E discount of approximately 35% compared to Google, about 2 standard deviations below the long-term mean, approaching multi-year lows.

TechFlow Perspective

The weakest link in Morgan Stanley's calculation is defaulting compute rental as a temporary business that Meta will execute stably over the long term. Meanwhile, Bloomberg's news itself has not been officially confirmed by Meta. Key variables such as rental price, lease term, and specific customers are still hypothetical values. No matter how detailed the sensitivity table is, the underlying premise has not yet materialized. For investors, what is more worth paying attention to is the hidden line of capital expenditure. Once Meta truly makes cloud computing a serious business, rather than staying at the stage of renting out idle compute, the $175 billion to $205 billion capital expenditure range currently given by Morgan Stanley is likely to be broken. This will simultaneously affect expectations for free cash flow and the market's judgment on whether Meta's valuation discount can narrow.

Disclaimer

This article is a compilation and interpretation of third-party brokerage research reports by TechFlow Research. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, representing only their affiliated institution's stance. They do not represent the views of TechFlow Research, nor do they constitute any investment advice.

The market carries risks; decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News