Deep Dive into OpenAI’s Pre-IPO

TechFlow Selected TechFlow Selected

Deep Dive into OpenAI’s Pre-IPO

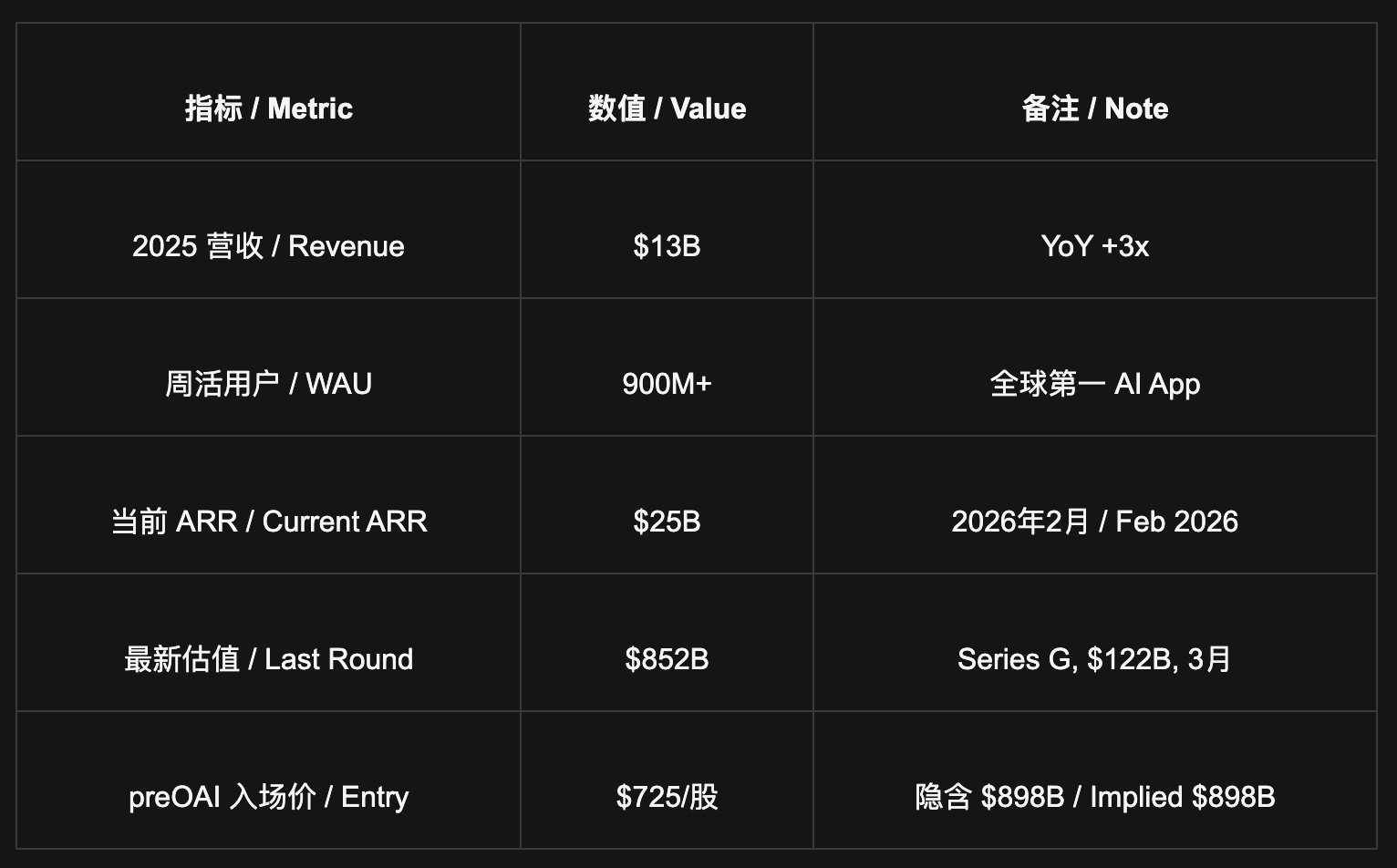

Bitget’s pre-OAI offering has an entry price of $725 per share—the only channel currently available to retail investors without requiring accredited investor status—and will be directly pegged to the public market price post-IPO.

- OpenAI’s 1.3 billion monthly active users (MAU) are forming the most valuable consumer entry point in human history—users open it voluntarily every day, deeply embed it into their workflows, and face extremely high switching costs. Its current $898B valuation reflects only extrapolated “visible revenue” from subscriptions and API usage; new revenue streams—including advertising (projected at $25B by 2029), consumer-platform repricing, and the GPT-6 re-rating effect—remain significantly underpriced. Bitget’s preOAI offering, priced at $725 per share, is currently the sole retail-accessible channel requiring no accredited investor qualification; post-IPO, it will directly track OpenAI’s public market price.

What Is OpenAI? Three Revenue Streams, One Actively-Opened Consumer Empire

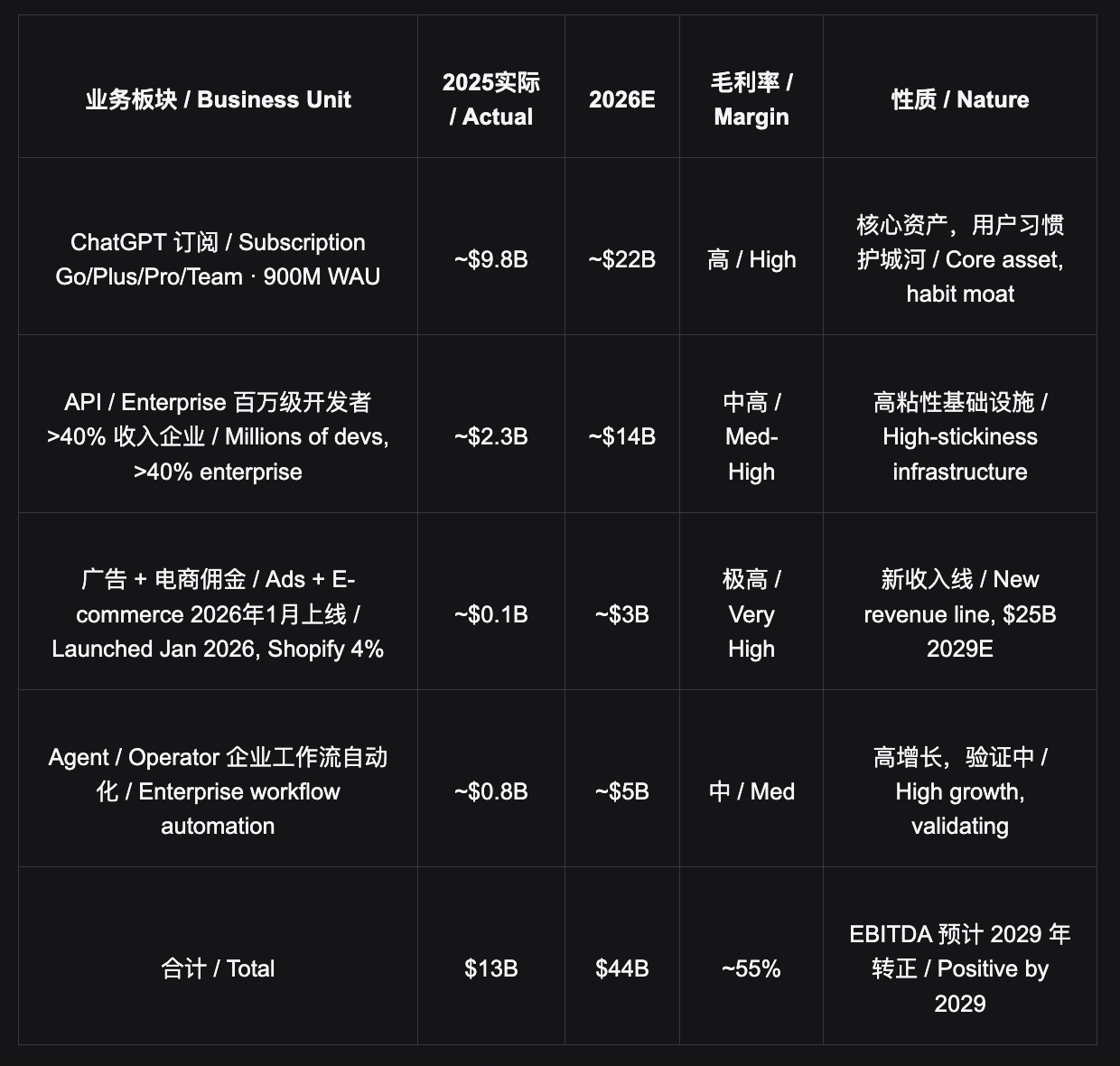

OpenAI cannot be understood solely through the lens of an “AI company.” It operates simultaneously as a consumer subscription platform (ChatGPT, with 900M weekly active users/WAU), developer infrastructure (API, relied upon by millions of developers), enterprise software provider (Enterprise, contributing over 40% of revenue), and an emerging advertising and e-commerce platform—four distinct identities unified vertically around a single core: the consumer entry point.

ChatGPT is an app users actively open—not a feature embedded within someone else’s product. This fundamentally distinguishes it from Google Gemini (distributed via search and its ecosystem) and Anthropic (API-only). The daily act of 1.3 billion MAU voluntarily opening ChatGPT constitutes, to date, the hardest-to-replicate distribution moat in the AI space.

Switching cost goes beyond merely downloading another app—it entails cognitive restructuring. A user who habitually turns to ChatGPT for answers has undergone behavioral rewiring far deeper than switching streaming platforms. Such habitual moats have historically belonged to only a handful of platforms: Google Search, the iPhone, and WeChat—all of which ultimately joined the trillion-dollar valuation club.

Why OpenAI Is Worth >$1T Short-Term and ~$2T Long-Term

Short-Term Catalysts

The current frontier AI benchmark landscape remains fragmented: different models lead across knowledge work, scientific reasoning, coding, multimodal generation, and other dimensions. For much of the past year, the market’s central concern has been whether OpenAI is losing its “absolute technological leadership” narrative premium.

That narrative is now being rewritten. OpenAI has released GPT-5.5—officially positioned as its “smartest model yet”—with enhanced capabilities for coding, research, and data analysis. More critically, Image2 / ChatGPT Images 2.0 has exceeded market expectations across image generation, editing, text rendering, multilingual support, and practical creative use cases—delivering strong, user-perceptible differentiation.

Together, GPT-5.5 and Image2 constitute a new product cycle: one that restores the market narrative of OpenAI’s technical leadership while driving increased consumer engagement, enterprise budget reallocation, and higher-tier subscription conversions through superior multimodal capabilities.

1. GPT-5.5 Has Launched: Technical Leadership Narrative Restored

GPT-5.5 is more than a routine model upgrade—it is OpenAI’s direct response to the past year’s narrative that its lead had been eroded by Gemini and Claude. By emphasizing gains in complex tasks, research, coding, and data analysis, OpenAI reaffirms its dominance in core knowledge work scenarios.

Image2 Exceeds Expectations: Image generation and editing improvements are more perceptible to average users—and more shareable on social media—than pure-text benchmarks. Image2 may become the key trigger for renewed acceleration in ChatGPT’s WAU growth.

2. Media Cycle Surge → WAU Continues Upward Trajectory

When GPT-4 launched, ChatGPT’s DAU surged tenfold within one week. GPT-5.5 strengthens retention among power users; Image2 drives re-engagement among mainstream users. Their combined effect is likely to lift ChatGPT’s active user base further.

3. Enterprise Budgets Re-Concentrating at OpenAI

GPT-5.5 covers professional workflows in research, coding, and data analysis; Image2 supports marketing, design, e-commerce, and content creation. OpenAI’s platform strength deepens, giving enterprises stronger justification to consolidate fragmented AI budgets back into OpenAI.

4. Free/Plus → Pro ($200/month) Upgrades Accelerating

Model capability leaps are the strongest driver of user conversion to paid tiers. Each additional 1 million Pro users adds $2.4B in annual recurring revenue (ARR). If GPT-6 launches in the coming months with full-dimensional superiority, it will further reinforce OpenAI’s “#1” narrative ahead of IPO.

5. IPO Roadshow Valuation Uplift → $1T Target by Q4 2026

OpenAI’s capital markets story has evolved—from “waiting for GPT-6 to regain leadership” to “GPT-5.5/Image2 already prove the product cycle has restarted; GPT-6 is upside.” This narrative is more robust—and more valuation-supportive—than betting purely on future model releases.

Long-Term Bullish Outlook · Consumer Super-Platform

OpenAI is not just an AI company—it is becoming the “default interface between humans and information and tasks.” Historically, only a few products have occupied this position: Google Search, the iPhone, and WeChat—all of which ultimately entered the trillion-dollar valuation club.

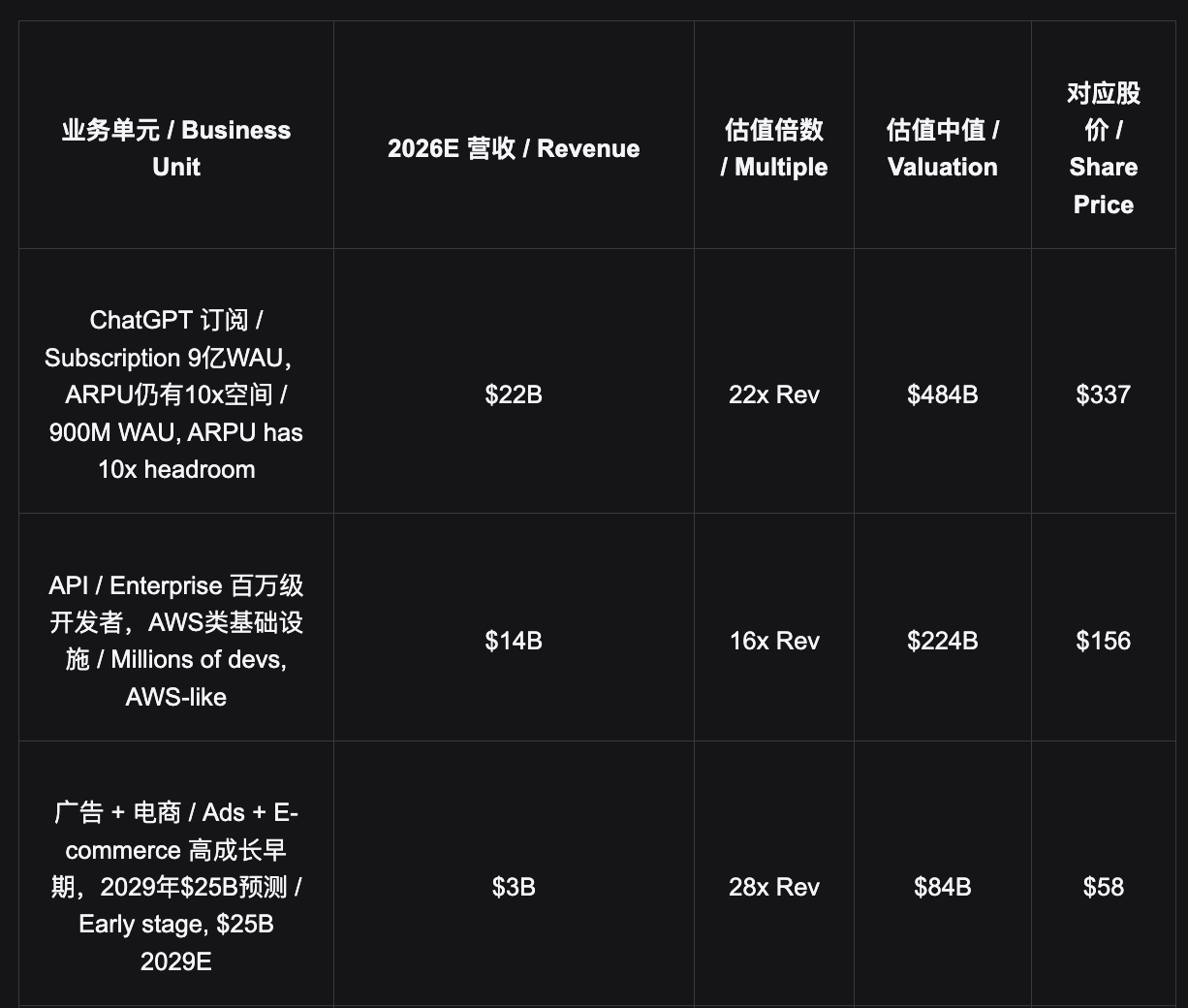

- ARPU Comparison: Full Monetization Headroom. OpenAI’s blended ARPU stands at ~$1.5/month ($25B ARR ÷ 1.3B MAU); Netflix: $15/month; Microsoft 365: $10–25/month; Spotify: $10/month; Instagram ads (global average): $3.3/month. ChatGPT’s usage depth and frequency match or exceed any subscription service—yet its monetization is only one-tenth that of Netflix. This gap is not a ceiling—it’s headroom.

Advertising Business: The Overlooked New Revenue Line. Ad testing launched in January 2026; full rollout to U.S. users occurred in February. Internal projections forecast $1B ad ARR in 2026 and $25B by 2029. The Shopify partnership has already validated the closed-loop model: in-chat shopping generated >$100M ARR within six weeks, with a 4% commission. With 900M WAU, ad inventory—valued at Facebook’s global average—implies latent value exceeding $300B. This revenue line was almost entirely omitted from the $898B valuation model.

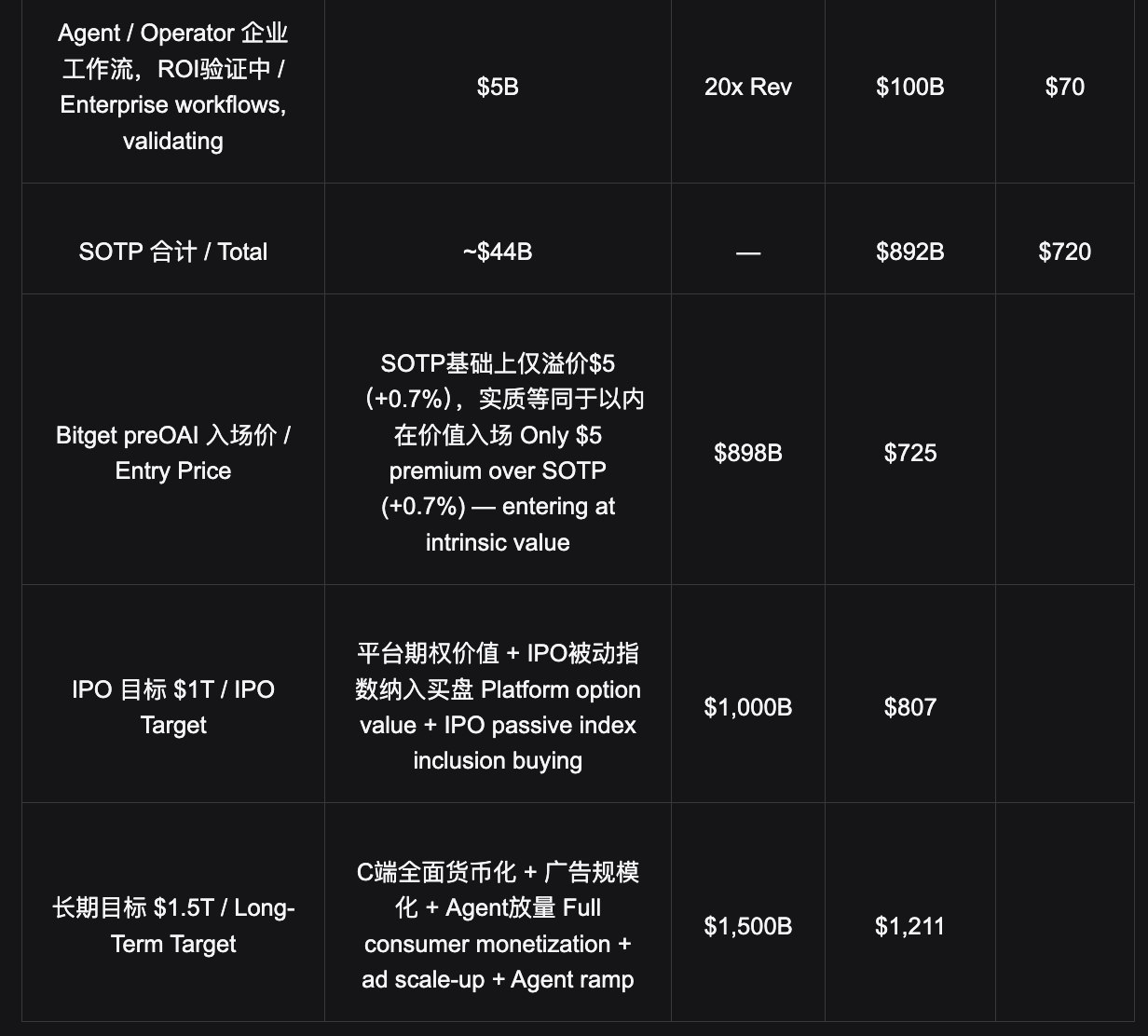

Segmented Valuation: $898B Already Below Intrinsic Value

Forward valuation is based on projected 2026 financials, aiming to assess whether Bitget’s preOAI entry price of $725 falls within a reasonable range—and identify sources of upside potential.

- Core Valuation Conclusion: The $725 entry price aligns nearly exactly with the SOTP median of $720—meaning you enter at a price close to “visible business only,” while the $300B+ implicit option value of advertising, AGI optionality, and consumer-platform premium repricing remain unpriced. $898B isn’t overvaluation—it’s underpricing of new revenue curves.

Pre-IPO Entry: Channel Comparison & Pricing Analysis

OpenAI remains a private company; ordinary investors cannot purchase its equity directly on any public market. Key fact: Series G institutional round implied price = $687.7 (at $852B valuation), with minimum subscription threshold of $100M—an inaccessible scale for individual investors regardless of net worth. Bitget’s preOAI at $725/share corresponds to the latest market valuation of $898B—the only accessible, liquid channel available to retail investors.

Access Channel Comparison

Series G · $687.7

Institutional Round · Closed

Implied $852B · Closed · Min $100M

To IPO Low End +17.3%

To LT Target $1.5T +76.1%

SoftBank-led $122B round; $100M minimum; exclusive to large institutions. Institutional cost basis: $687.7 ($852B). Current preOAI $725 reflects updated $898B market pricing—market has repriced OpenAI upward, delivering ~5.4% paper gain to early institutional entrants.

Hiive · $608

Real Equity · Accredited Investors Only

Implied $873B · Secondary Transfer

To IPO Low End +32.7%

To LT Target $1.5T +99.2%

Requires accredited investor status (net worth ≥$1M) and minimum investment of $25,000. Private equity transfer, no secondary market, transfer timelines measured in weeks—no real-time responsiveness to catalyst events.

preOAI · $725

Bitget IPO Prime · Tokenized · Only Tradeable

$898B · Latest Market Price · No Accreditation Required

To IPO Low End +11.3%

To LT Target $1.5T +67.0%

The only channel with secondary-market liquidity. Tokenized structure, no accreditation requirement, no minimum investment. Fully tradable anytime—immediate execution on catalyst events such as GPT-6 launch or IPO announcement. Post-IPO settlement directly tracks OpenAI’s public market price.

- Liquidity Is the Core Differentiator: preOAI is a tokenized product with secondary-market access, enabling instant trading—GPT-6 announcements can be capitalized on within days. Hiive involves private equity transfers without secondary liquidity; institutional rounds offer no exit path. preOAI’s $725 price sits ~5.4% above the institutional $687.7, reflecting the market’s updated consensus on OpenAI’s value.

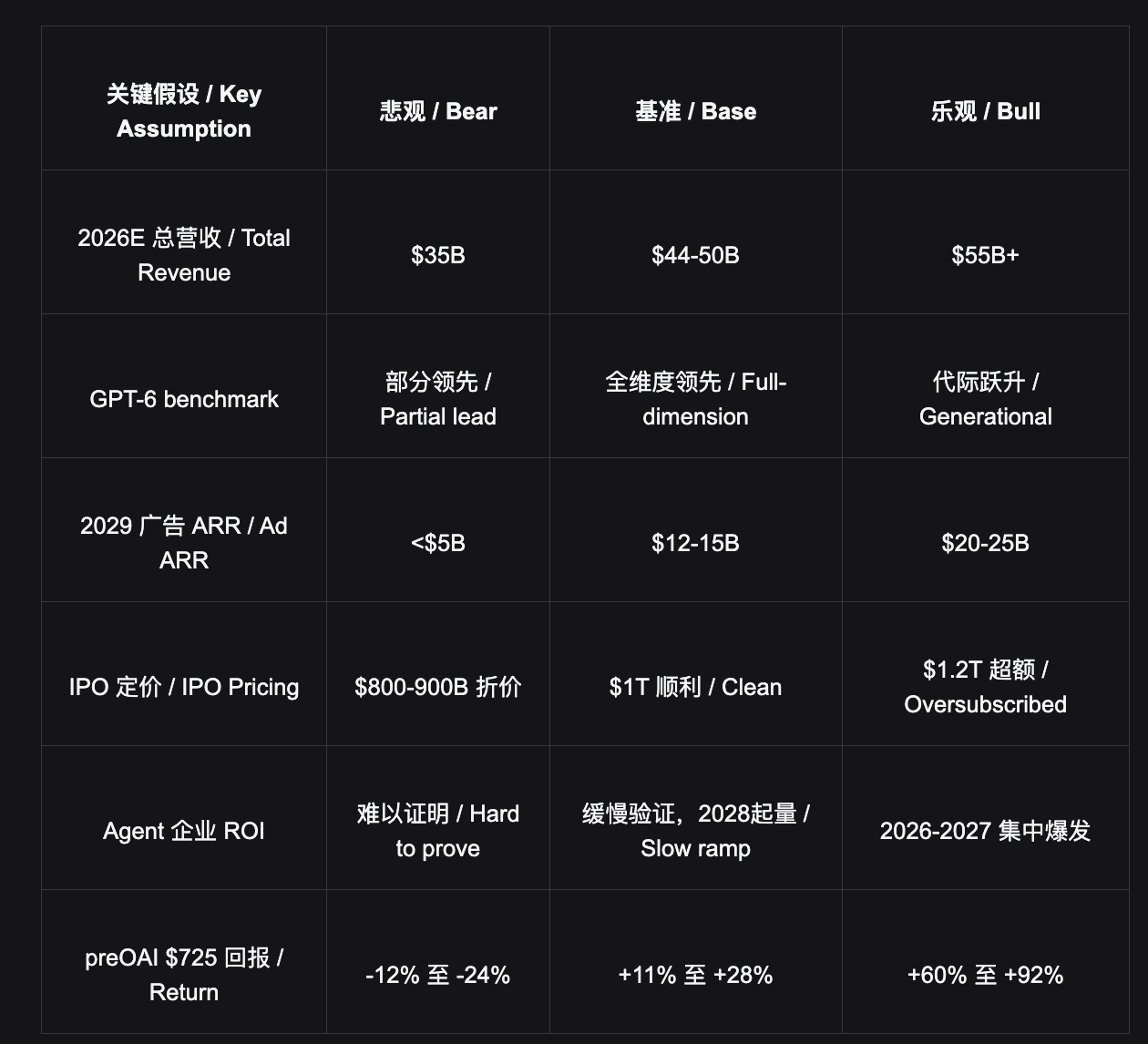

Scenario Analysis & Key Assumptions

Scenario Analysis

Bear Case $475–$550 → $682B–$790B

GPT-6 underperforms; Gemini materially erodes share; ad monetization damages user trust; IPO priced at discount. From preOAI $725: downside of ~12%–24%. Bottom support anchored by ChatGPT’s 1.3B MAU.

Base Case (Primary) $807–$928 → $1T–$1.15T

GPT-6 re-establishes leadership; IPO closes Q4 2026 at $1T; advertising scales gradually; 2026E revenue of $44B–$50B delivered as expected. From preOAI $725: upside of ~11%–28%, visible within 12 months.

Bull Case $1,000–$1,200 → $1.44T–$1.72T

GPT-6 achieves generational leadership; enterprise agent ROI proven and adoption accelerates; IPO oversubscribed; advertising hits $25B by 2029. From preOAI $725: upside of ~60%–92%.

※ Primary Downside Risks: ① Google Gemini achieves massive catch-up via ecosystem distribution (20% probability); ② Ad monetization harms user trust, shrinking WAU (10%); ③ Agent delivery delays impair enterprise renewal (15%); ④ Governance controversies (10%). These risks are largely independent and limited in impact individually. Floor support: ChatGPT’s 1.3B MAU habitual moat remains intact.

LLM Competitive Landscape: Strategic Divergence & Long-Term Coexistence Among the Big Three

Competition at the LLM layer is not zero-sum—it is multi-oligopolistic, with each player targeting nearly non-overlapping user pools. OpenAI’s 1.3B active users, Anthropic’s 1–2M high-paying developers, and Google’s 3B+ ecosystem users represent three distinct AI-era infrastructure paradigms.

Competitive Landscape

OpenAI

$852B (Institutional Round)

▸ Strengths

1.3B MAU consumer entry point—actively opened, habitual moat; the only entity capable of “national-scale” fundraising; bottom-up culture enables generational talent leaps

▸ Challenges

Coding lead eroded by Anthropic; internal project count >300, execution diluted; C-side traffic creates pretraining overhead

▸ LT Ceiling

>$1.5T (Consumer Platform Grade)

Anthropic

Legacy shares imply ~$800B; next round expected $800–850B

▸ Strengths

Abandoned C-side, all-in on coding—organizational execution is its moat; 1–2M core developers generate more revenue than OpenAI’s 50M C-side subscriptions; API evolving toward Agent OS

▸ Challenges

No consumer platform; ceiling is “best developer tool,” not “largest consumer platform”

▸ LT Ceiling

>$1.5T (Developer OS Grade)

Google / Gemini

Alphabet $2T (AI upside not separately priced)

▸ Strengths

Unmatched compute, largest dataset, unrivaled distribution (3B+ ecosystem users); fully mature ad infrastructure

▸ Challenges

Benchmark inflation; coding lagging by 3–4 months; complex internal politics, weak PM culture; perpetually chasing, perpetually half-a-step behind

▸ End-Game

Coexistence: Google dominates distribution; OpenAI dominates active entry

- Core View: Both OpenAI and Anthropic are long-term $1.5T+ companies—different paths, similar endpoints. OpenAI follows the consumer platform path (like Apple/Google); Anthropic follows the developer OS path (like AWS). Their core user bases barely overlap—not zero-sum, but parallel evolution of two dominant AI infrastructure models. Yet OpenAI’s consumer platform premium remains significantly underpriced by the market—this is the core thesis for entering at $725, and represents a structural mispricing relative to Anthropic.

Disclaimer

This report is for internal research reference only and does not constitute investment advice. Tokenized products (preOAI) confer no shareholder rights, voting rights, or dividends; economic returns are linked to a reference index, and settlement depends on platform creditworthiness. Private equity (Hiive) is restricted to accredited/institutionally certified investors, carries 3–5% fees, and features lock-up periods dependent on share structure. OpenAI’s S-1 filing is in preparation; IPO valuation, timing, and structure remain subject to change. All financial projections are analyst estimates and not official disclosures from OpenAI.

OpenAI — $122B Funding Announcement · CNBC — Series G $852B · Sacra — OpenAI Equity Research 2026 · Business of Apps — ChatGPT Statistics 2026 · Hiive — OpenAI $608.06 (April 2026) · Polymarket — GPT-6 Release Odds · IndexBox — OpenAI IPO $1T Target 2026 · ALM Corp — ChatGPT Ads $25B 2029 Projection

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News