GameStop CEO Sells Socks: $56 Billion Acquisition of eBay Crumbles from a Single Pair of Socks

TechFlow Selected TechFlow Selected

GameStop CEO Sells Socks: $56 Billion Acquisition of eBay Crumbles from a Single Pair of Socks

GameStop CEO’s New Script: Leveraging a Screenshot of Being Banned from eBay for “Selling Socks” to Secure a $56 Billion Acquisition Deal

By Ada, TechFlow

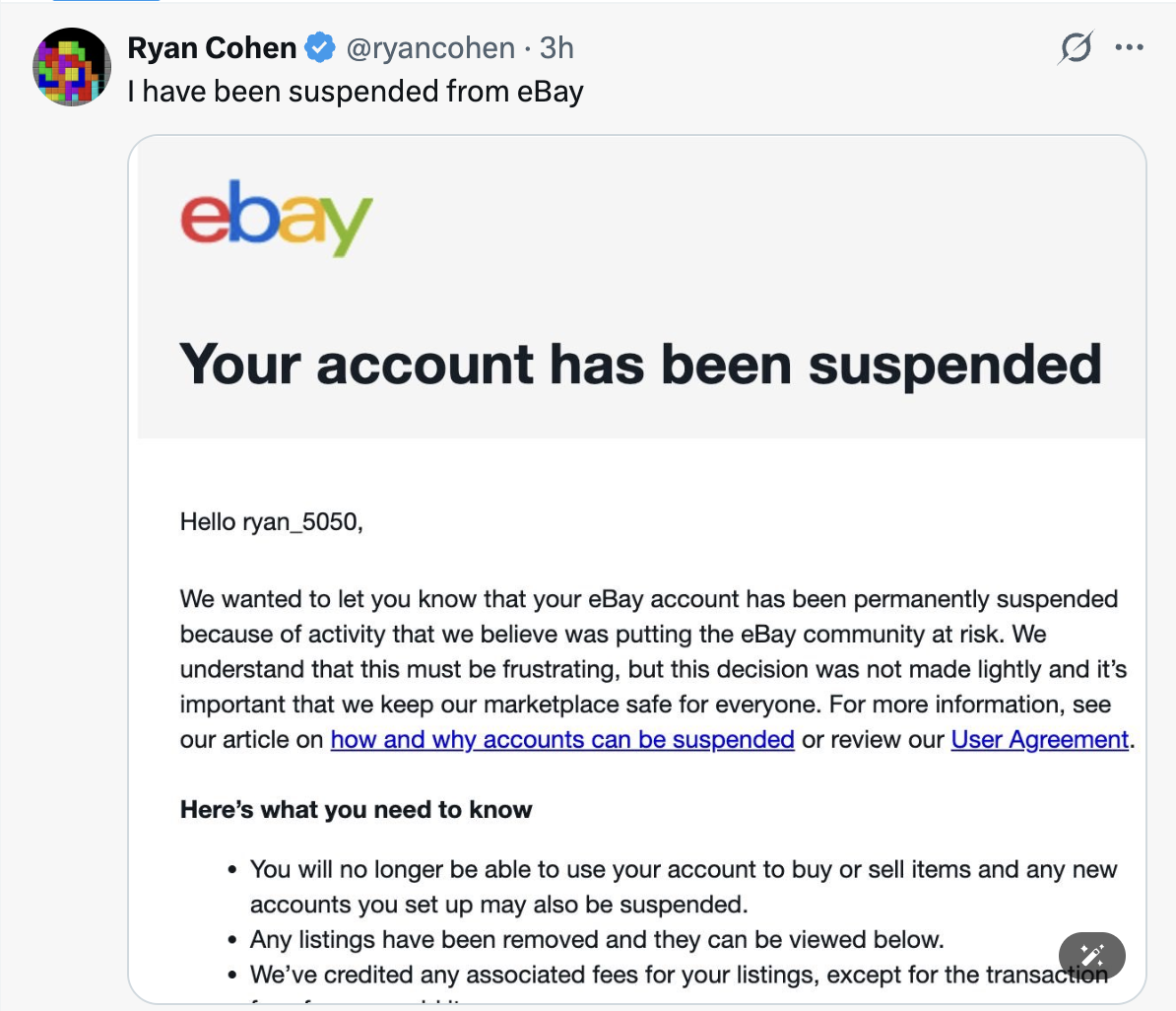

In the early hours of May 7, GameStop CEO Ryan Cohen posted a screenshot on X.

eBay had notified him that his account had been permanently suspended, citing “activities we believe pose a risk to the eBay community.”

Just 24 hours earlier, he had listed a pair of socks on his personal eBay account, captioning it: “Selling stuff on eBay to raise money to buy eBay.”

It sounds like a joke—but he was serious. Because just three days earlier, he had delivered a non-binding $56 billion acquisition offer to eBay’s board.

A Bid That Doesn’t Hold Water

On May 4, GameStop announced a non-binding acquisition proposal for eBay at $125 per share.

In its statement, GameStop said the offer would be paid half in cash and half in GameStop common stock—representing a 20% premium over eBay’s Friday closing price of $104.07, and a 46% premium over its closing price on February 4—the day this video-game retail giant began accumulating shares in eBay.

On Monday, eBay’s stock rose roughly 5%, to around $109—still far below GameStop’s $125 bid. Meanwhile, GameStop’s stock fell about 10%, signaling investor skepticism about the deal’s viability.

GameStop’s current market capitalization stands at approximately $11.2 billion—just a fraction of the proposed $56 billion transaction value. Although the company has secured a $20 billion letter of intent from TD Bank, a massive funding gap remains.

So how will the rest be covered? Cohen answered on CNBC: “We’re offering half cash, half stock—and we have the capacity to issue additional shares to complete this transaction.”

In other words: print stock. Use the equity of an $11.2 billion company to acquire a firm valued at $55.5 billion. For eBay shareholders to accept GameStop stock as consideration, GameStop’s share price would first need to surge fivefold.

What does the market think?

Traders on Kalshi assign only a 26% probability that GameStop will complete the acquisition by 2026—even though trading volume on the new contract is extremely low, barely exceeding $2,000.

Traders on Polymarket are even more pessimistic, pricing in just a 15% chance of completion.

According to a Semafor report citing insiders, eBay’s board met this week to review the proposal—but the deal “appears already stillborn,” with Cohen failing to win public support from any major shareholder.

A Meticulously Staged Performance

Forty-eight hours after submitting the offer on May 6, Cohen began listing items—including socks, odds and ends, and personal effects—on his personal eBay account. Bids totaled tens of thousands of dollars.

He also launched a barrage of Twitter attacks against eBay’s board, accusing them of poor management. That same day, he first received notice from eBay stating he’d hit his monthly listing limit—then his account was suspended.

The suspension notice’s line—“activities we believe pose a risk to the eBay community”—takes on surreal irony when applied to someone actively trying to acquire eBay.

But this is pure theater. Since his bid failed to intimidate the board, Cohen turned to noise to activate GameStop’s retail investor base. Get the stock price flying first—only then can stock serve as viable consideration.

Why did Cohen launch this acquisition attempt?

Here’s the context: In early 2026, GameStop’s board revised Cohen’s compensation plan—granting him up to $35 billion in stock incentives if the company reaches a $100 billion market cap. With GameStop currently valued at only ~$11.2 billion, hitting $100 billion through selling physical game discs is virtually impossible. The only plausible path is growth via acquisition.

And Cohen’s entire “sell socks to buy eBay” script was never intended for eBay’s board—it was written for GameStop’s retail investors on Reddit’s WallStreetBets (WSB) forum.

From Bitcoin to eBay

Zoom out, and you’ll see Cohen’s script has remained consistent—from Bitcoin to eBay.

In February 2025, he flew to meet Michael Saylor. Three months later, GameStop announced its Bitcoin entry. According to Reuters, GameStop spent $513 million to acquire 4,710 BTC, averaging ~$108,917 per coin.

While Saylor leveraged Strategy’s entire balance sheet—issuing debt and buying weekly—Cohen stopped after $513 million, representing just 10.4% of GameStop’s cash reserves at the time. Strategy bought almost every week; GameStop added zero BTC thereafter.

Then, around January 23, 2026, GameStop transferred all 4,710 BTC to Coinbase Prime—preparing to liquidate.

After the transfer, Cohen granted back-to-back interviews with multiple international media outlets. He spoke passionately about acquisition plans, vowing to transform GameStop into an investment holding platform “akin to Berkshire Hathaway.” When pressed on Bitcoin strategy, he delivered the oft-quoted line: “This strategy is more attractive than Bitcoin.”

What “more attractive strategy”? As it turns out: the $56 billion eBay acquisition.

The logic chain now closes: First, use Bitcoin narrative to lift stock price and attention; once paper losses emerge, pivot to the next grander story—mergers & acquisitions, building a Berkshire-like holding conglomerate worth hundreds of billions. Each story dwarfs the last—but none ever materializes.

Saylor embodies conviction; Cohen embodies performance. He doesn’t need transactional closure—narrative closure suffices. Once the Bitcoin story runs its course, he moves on to eBay. Once eBay fades, what’s next? No one knows—but there will always be a next.

Why eBay?

eBay boasts stable cash flow, steady GMV, and reliable shareholder returns. It’s a company with $31 billion in annual revenue. If the merged entity maintains eBay’s valuation multiples, its market cap could easily breach critical thresholds.

So what does Cohen stand to gain?

One interpretation: He needs a story bigger than Bitcoin.

GameStop’s core problem has never been lack of cash—the $9.4 billion in cash reserves is real firepower. But as a retailer built on physical stores, boxed games, and secondhand trade, GameStop’s legacy business has long been eroded by digital downloads, platform-owned storefronts, and subscription services—making its $11.2 billion market cap fundamentally unsustainable.

Retail investors aren’t buying GameStop—they’re buying Cohen, memes, and the possibility of “the next Berkshire Hathaway.”

But possibilities require constant feeding.

The Bitcoin treasury narrative fed the flame—for a while. Once momentum reversed, a more explosive story was needed. Acquiring a publicly traded company five times its size? That’s explosive enough.

Will the deal happen? Irrelevant.

What matters is that, once the offer is submitted, CNBC invites him on air, the Wall Street Journal publishes a profile, Reddit erupts again, and GME’s stock experiences several days of violent volatility. Within that volatility, options buyers profit, retail investors feel the illusion of “winning again,” and Cohen himself can monetize some of his equity incentives.

And selling socks—and getting banned—generates massive free traffic.

When Performance Art Meets Capital Markets

Note: Cohen is a proven serial entrepreneur—his Chewy sold to PetSmart for $3.35 billion. He knows eBay’s board won’t sell to a rival worth just one-fifth its own market cap; he knows the $20 billion from TD Bank falls short; he knows issuing new shares would trigger immediate rejection by eBay shareholders.

Yet he doesn’t care—he only needs to perform.

The true audience for this performance? Liquidity itself—the attention economy. In an era where all assets are priced on narrative, whoever generates the loudest noise captures the most liquidity—fast.

Getting banned for listing socks works a hundred times better than a formal press release. Overnight, every financial outlet covers Cohen; every social platform circulates that suspension screenshot. Free global exposure dwarfs the sales value of those listed items.

Today’s capital markets increasingly blur the line between performance art and investment action. In the past, offers were made to close deals. Today, offers are made to move prices. Price movement creates profit—and profit is the exit path. This is the game Cohen and his peers know best.

Cohen never truly bets; he’s always rehearsing for the next act. But one thing is clear right now: When a publicly traded CEO must list socks on eBay to prove his seriousness about acquiring it—and gets permanently banned by eBay for “posing a risk to the community,” that moment alone is the most precise footnote this era has written on capital markets.

When the tide recedes, the fastest to flee are always the opportunistic trend-chasers—while true believers may well dismiss the whole spectacle with disdain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News