Hotcoin Research | How Long Can the DAT Flywheel Spin: A Feast of Crypto Wealth or a Bubble Trap?

TechFlow Selected TechFlow Selected

Hotcoin Research | How Long Can the DAT Flywheel Spin: A Feast of Crypto Wealth or a Bubble Trap?

After standardization and natural selection, the DAT model is expected to bring new opportunities and profoundly impact the cryptocurrency market landscape.

1. Introduction

2025 can be regarded as the breakout year for DAT. An increasing number of publicly traded companies are following Strategy's model by adding cryptocurrencies such as BTC, ETH, SOL, and BNB to their balance sheets as core reserves, and continuously increasing their holdings through stock financing. This has led to a synchronized rise in token and stock prices: investors gain indirect long-term exposure to cryptocurrencies by purchasing these companies' stocks, while the companies leverage stock price premiums to raise funds and buy more digital assets, forming a self-reinforcing financial flywheel.

This article analyzes the phenomenon from three dimensions: first, systematically unpacking the logic and flywheel effect of the DAT model, explaining why it enables a self-reinforcing cycle of "token and stock rising together" during bull markets; second, using case studies to illustrate differences and outcomes in corporate practices involving emerging public chain tokens like BTC, ETH, SOL, and BNB, revealing institutional strategic intentions and funding methods; third, exploring the risks and challenges DAT faces amid tightening regulation, intensifying market competition, and macroeconomic volatility, while also outlining its potential evolutionary paths. The article aims to help investors understand how this emerging model affects token prices, stock prices, and capital market dynamics, while highlighting the hidden risks behind the flywheel effect. DAT is not merely corporate asset allocation—it is a new bridge connecting crypto and traditional financial markets, reshaping market narratives, redirecting capital flows, and gradually influencing macro-level capital allocation logic.

2. The DAT Flywheel Effect: A Positive Feedback Loop of Rising Tokens and Stocks

1. Definition and Growth Logic of DAT

DAT (Digital Asset Treasury) refers to listed companies, private enterprises, or investment vehicles that strategically and long-term incorporate crypto assets such as Bitcoin and Ethereum into their balance sheets or equivalent holding entities, amplifying per-share crypto exposure and capital efficiency through a closed loop of equity/bond financing → spot crypto purchases → information disclosure and valuation reflection. At its core, it is an asset allocation framework linking "company equity" with "on-chain assets."

The essence of the DAT model lies in a financial flywheel of "raising equity to buy on-chain assets," which can self-reinforce during bull markets, driving both token and stock prices upward. This flywheel effect was first validated by Strategy founder Michael Saylor in 2020, with the following basic logic:

-

Holding crypto assets: Companies use raised capital to heavily purchase digital assets such as BTC and ETH as primary reserves.

-

Stock price premium increases: Due to providing convenient and compliant crypto exposure, company stock prices begin trading above their net asset value (NAV) tied to held tokens. Investors pay premiums for these stocks, effectively recognizing the future appreciation potential of the crypto assets held.

-

Leveraging premium for further fundraising: Higher stock prices grant companies greater financing capacity. They can issue new shares at high valuations or low-interest convertible bonds to raise additional capital.

-

Buying more tokens: Most of the newly raised funds are reinvested into purchasing more cryptocurrencies, expanding reserve size.

-

Reinforcing the narrative cycle: Continuous growth in token holdings strengthens the market story of being a "crypto asset proxy stock," further boosting stock price premiums and setting the stage for the next round of financing.

2. Manifestations of the DAT Flywheel Effect

In bull markets, this cycle creates strong positive feedback—an "infinite bullets" model: buy tokens → token price rises → stock price rises → fundraise → buy more tokens, repeating endlessly. This allows investors to enjoy not only token price gains but also leveraged returns via stocks. For example, between 2023 and 2025, Bitcoin’s price rose about 110%, while Strategy’s stock surged over 910%. Capital leverage and stock price premiums enable DAT stocks to deliver far higher returns than direct token holding during bull runs.

-

Strategy's BTC treasury strategy: Since adopting its Bitcoin treasury strategy, Strategy's stock has skyrocketed over 2200% in five years. Its Bitcoin holdings have grown from zero in 2020 to 639,835 BTC today, worth over $73 billion, making it the world’s largest publicly traded Bitcoin holder and pushing its market cap far beyond its original software business value.

-

BitMine's ETH treasury strategy: U.S.-listed BitMine launched its Ethereum treasury strategy in 2025, with its stock surging over 1100% within one month. About 60% of the gain stemmed from a sharp increase in per-share token holdings (+330%), 20% from ETH price appreciation (rising from $2,500 to $4,300), and another 20% from mNAV premium expansion.

DAT has become a major buyer in the crypto market. According to Coinbase Research, companies focused on Bitcoin now collectively hold over 1 million BTC—about 5% of Bitcoin’s circulating supply—while Ethereum-focused DAT firms hold approximately 4.9 million ETH, around 4% of ETH’s circulating supply. The total value of digital assets held by global DAT companies exceeds $100 billion. DAT has become a significant buying force in the crypto market. According to Coinbase Research, companies focused on Bitcoin now collectively hold over 1 million BTC—about 5% of Bitcoin’s circulating supply—while Ethereum-focused DAT firms hold approximately 4.9 million ETH, around 4% of ETH’s circulating supply. The total value of digital assets held by global DAT companies exceeds $100 billion.

3. Review of Key DAT Strategies: From BTC to Diversified Asset Allocation

As the DAT concept expands beyond Bitcoin into other sectors, various companies are adopting diversified strategies across different crypto assets.

1. Bitcoin Treasury Pioneers: The Offensive and Defensive Playbook of BTC "Hodlers"

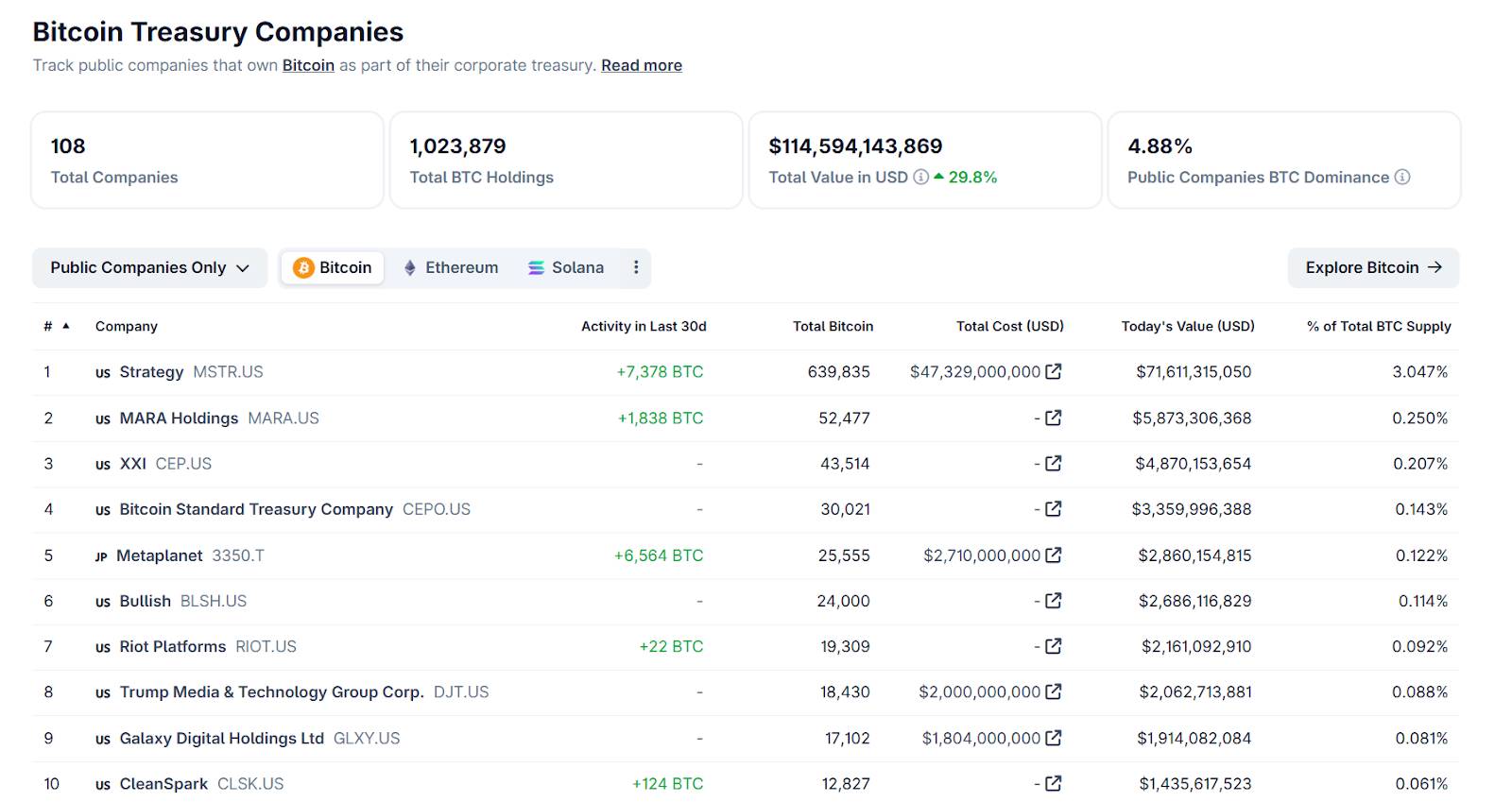

Bitcoin was the first domain where DAT emerged. Strategy’s bold move in 2020 set the precedent for BTC treasuries, after which many companies joined the "hodl Bitcoin" trend. According to the latest data from CoinGecko, 108 public companies now hold BTC, with total holdings exceeding 1 million BTC—4.88% of BTC’s total supply.

Source: https://www.coingecko.com/en/treasuries/bitcoin/

-

Strategy: Since August 2020, Strategy has continuously invested revenue and raised funds into Bitcoin, currently holding nearly 640,000 BTC—about 3% of total supply. By raising capital through multiple equity and bond offerings to buy BTC, Strategy achieved exponential growth in both stock price and assets during the crypto bull market. Its success demonstrated the feasibility of BTC as a corporate reserve asset.

-

Metaplanet: This former Japanese metaverse tech company pivoted to a Bitcoin treasury model in April 2024, adopting BTC as a core reserve to hedge against risks such as yen depreciation. As of September 25, 2025, Metaplanet holds 25,555 BTC at an average purchase price of ~$106,065. Its total cost is approximately $2.71 billion, already slightly in the green. Thanks to its scale, Metaplanet has become the world’s fifth-largest publicly traded BTC holder. This achievement drove its stock up over 140% year-to-date, elevating it from a small-cap to mid-cap stock and earning inclusion in the FTSE Japan Index.

-

MARA, RIOT, and other miners: U.S.-based Bitcoin mining firms like Marathon Digital (MARA) and Riot Platforms (RIOT) serve dual roles as mining stocks and treasury entities. They accumulate BTC through mining and tend to hold rather than sell all mined coins during bull markets. MARA and RIOT hold over 50,000 and 19,000 BTC respectively. Their advantage lies in converting operational profits directly into BTC accumulation—effectively exchanging electricity for Bitcoin. However, their stock prices are highly correlated with BTC, making them de facto stock-based tools for BTC exposure.

-

Other followers: Numerous small-cap firms from traditional industries have transformed into "crypto stocks" by aggressively purchasing tokens. For instance, Hong Kong-based Mingcheng Group (NASDAQ: CREG), originally in construction subcontracting, spent $483 million buying BTC in August 2025 and announced digital assets as a core strategy, triggering a sharp stock surge upon announcement.

Notably, as the number of BTC treasury companies grows rapidly, market "scarcity premium" is declining. Strategy’s early success stemmed from rarity, but the narrative of "buy BTC to boost stock price" is no longer novel. Amid homogenized competition, mNAV premiums relative to token holdings among some BTC treasury firms are gradually narrowing.

2. Rise of Ethereum Treasuries: From Reserve to Yield-Bearing Assets

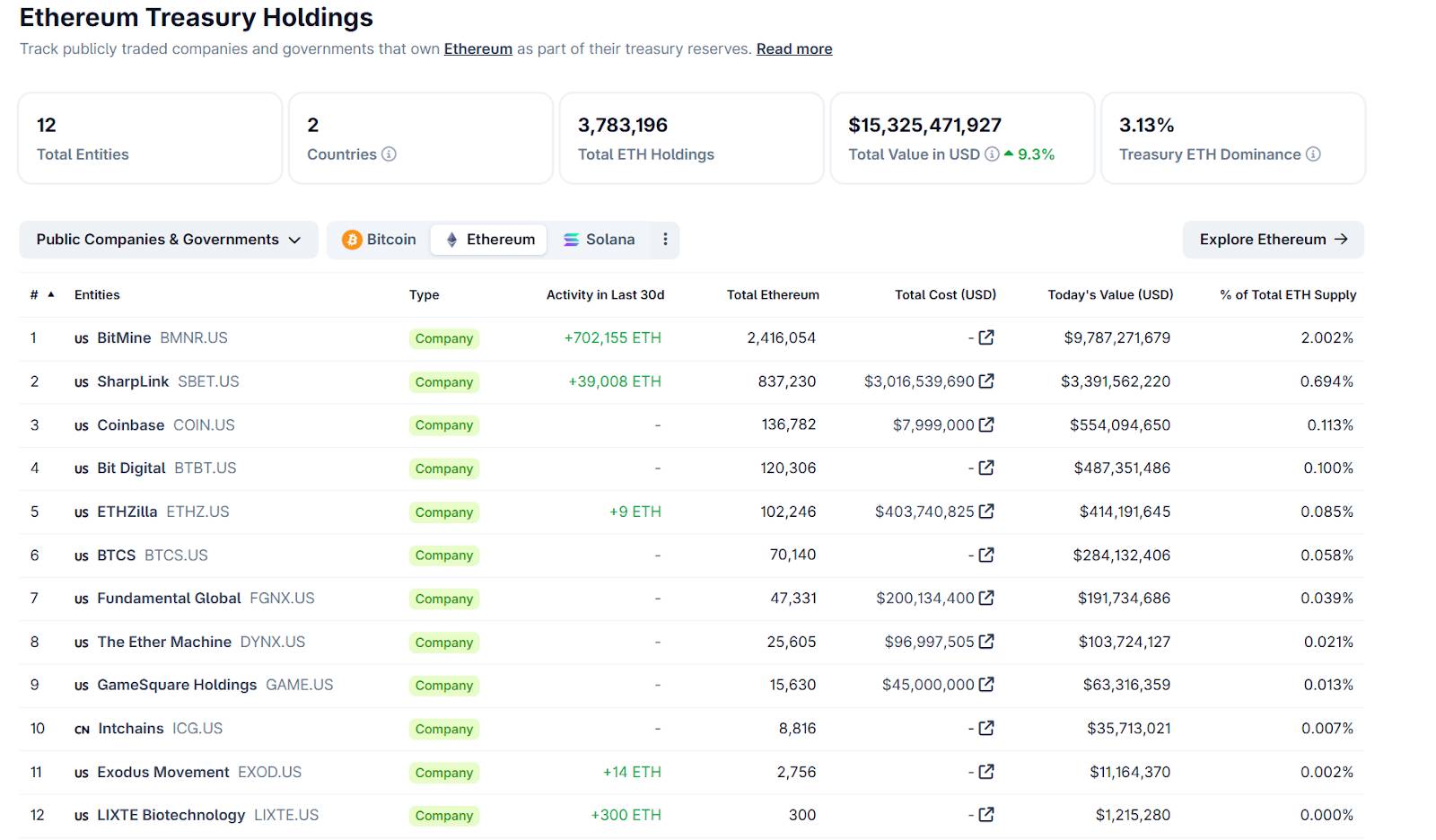

2025 is seen as the inaugural year for Ethereum treasuries. Previously, corporate ETH holdings were typically for operational needs rather than strategic reserves. But starting this year, multiple institutions have prominently added ETH to their reserves and innovatively leveraged Ethereum’s staking yields to create a "hodl-and-earn-interest" model. According to CoinGecko, 12 public companies now hold ETH, totaling over 3.78 million ETH—3.13% of ETH’s total supply.

Source: https://www.coingecko.com/en/treasuries/ethereum

-

BioNexus: In March 2025, Southeast Asia-based BioNexus announced ETH as its primary reserve asset, becoming the first public company to adopt an Ethereum treasury strategy. This landmark move marked ETH’s formal entry into corporate balance sheets. Unlike Coinbase, which holds ETH for business reasons, BioNexus explicitly treats ETH as a strategic reserve and investment asset, signaling institutional recognition of ETH’s store-of-value status.

-

BitMine Immersion (BMNR): In mid-2025, BitMine announced a major ETH initiative, aiming to hold 5% of global ETH supply long-term. As of September 25, 2025, it holds 2.416 million ETH—around 2% of circulating supply—making it the world’s largest ETH holder. Using convertible bonds and share issuance, BitMine expands its balance sheet, driving a flywheel of "fundraising → buying tokens → valuation rise → re-fundraising" to push both stock and asset values higher, emerging as one of 2025’s standout DAT stars. Most of its ETH is staked on-chain, converting Ethereum’s productive features into corporate cash flow.

-

SharpLink (SBET): SharpLink, a Nasdaq-listed sports betting tech firm, actively transitioned to an ETH treasury in 2025. Through an "at-the-market" (ATM) small-scale issuance mechanism, it raises funds almost weekly and immediately discloses ETH purchases. It has accumulated over 830,000 ETH, nearly 100% of which is staked for staking rewards. This aggressive strategy gives it not only massive unrealized gains but also steady income. While concerns exist about its "full-stake" approach increasing exposure to protocol security and liquidity risks, supporters see it as a best practice in turning ETH into a productive asset to enhance DAT returns.

-

BTCS Inc: U.S. blockchain firm BTCS launched an "Ethereum dividend + loyalty reward" program, periodically distributing ETH dividends to shareholders and offering extra ETH rewards to those who register shares with a designated registrar and hold until early 2026. This incentivizes long-term holding, improves shareholder stickiness, and somewhat deters short-selling. Though the sustainability of "paying dividends in ETH" remains debated, BTCS demonstrates flexibility and creativity in DAT financial engineering.

The rise of Ethereum treasuries indicates DAT is evolving from passive hodling to active value creation. Firms are no longer just holding tokens—they’re exploring staking, DeFi, and other methods to generate yield from on-chain assets, creating greater value for shareholders. As a result, some analysts believe ETH treasury firms have stronger advantages than BTC counterparts. During market downturns, staking income may cushion mNAV declines better than pure BTC treasuries.

3. Solana Treasury Boom: A High-Stakes Race

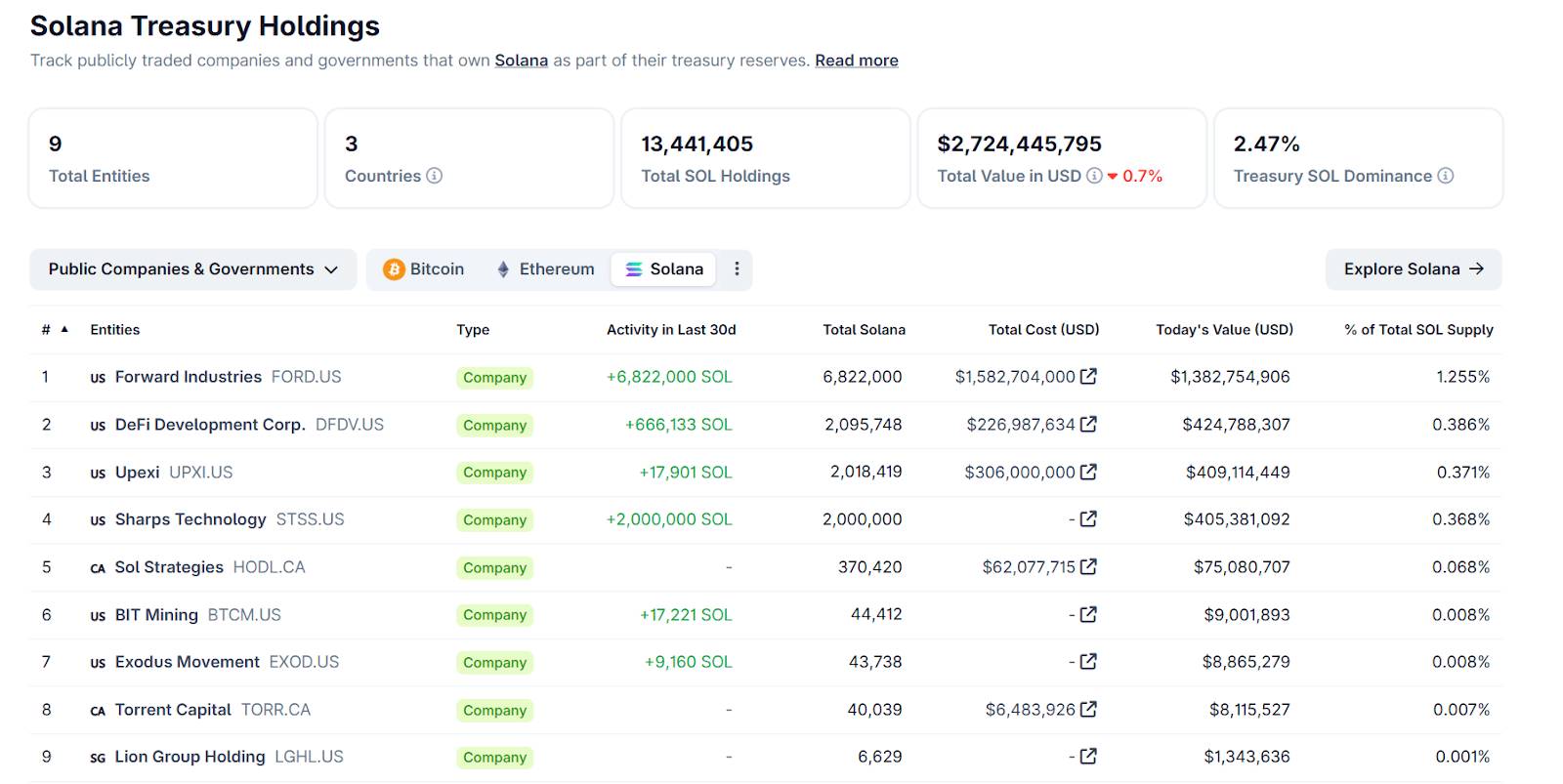

In the second half of this year, Solana has become the focal point of the DAT space. After BTC and ETH, SOL is accelerating into institutional adoption: nine public companies have now taken positions in SOL, investing a total of $2.7 billion and accumulating over 270 million SOL—2.47% of SOL’s total supply.

Source: https://www.coingecko.com/en/treasuries/solana

-

Forward Industries (FORD): Formerly a provider of design/manufacturing solutions for medical and tech clients, Forward Industries officially shifted to a "Solana treasury company" narrative in September 2025. Its treasury strategy is backed by a $1.65 billion PIPE investment led by Galaxy Digital, Jump Crypto, and Multicoin, aiming to "build the world’s largest Solana treasury." The company emphasizes on-chain execution and full staking to earn native yield, disclosed plans for continuous ATM funding (up to $4 billion), and is exploring tokenizing its stock on Solana.

-

DeFi Development Corp. (DFDV): DFDV clearly designates SOL as its core treasury asset and uses "SOL per Share (SPS)" as its key management and communication metric. Its strategy includes long-term holding, diversified staking across multiple validators, and operating its own Solana validator node to capture fees and staking rewards. It recently announced that newly acquired SOL will be held long-term and fully staked.

-

Upexi (NASDAQ: UPXI): Originally a multi-brand consumer goods company, Upexi began transitioning in 2025 into a dual focus of "SOL treasury + asset management": using PIPE and convertible bonds to fund large-scale SOL purchases, nearly all of which are staked, while also using discounted locked staking to enhance embedded yield and bringing in industry advisor Arthur Hayes to strengthen institutional outreach.

-

Sharps Technology (STSS): A medical device company, Sharps announced in September 2025 the completion of its first SOL acquisition and formal adoption of a digital asset treasury strategy centered on SOL, funded by recent PIPE investments. The company emphasizes regular disclosures and manages along the core principle of "capital market fundraising → holding SOL → earning on-chain yield."

-

Sol Strategies (HODLF): A Canadian-listed Solana ecosystem investment and infrastructure firm, Sol Strategies focuses on accumulating SOL and operating validators, while divesting non-core crypto assets to further concentrate holdings on SOL, aligning with its long-term strategy and node operations.

The Solana treasury boom reflects institutional capital broadening its scope to more diverse public chains. SOL is emerging as the third most favored asset among DAT firms after BTC and ETH. Compared to BTC and ETH, Solana offers superior technical performance and a vibrant ecosystem, leading institutions to bet on its future price and ecosystem growth. Massive inflows caused SOL’s price to surge past $250 in August–September 2025. However, Solana treasury firms are still few in number and unproven—their future performance remains to be seen. The success or failure of Solana treasuries may directly determine whether the chain can join the ranks of true mainstream assets.

4. Emerging Asset Treasuries: BNB, TRON, SUI, ENA, and Others

Signs of corporate treasury adoption are also appearing for BNB. On August 10, BNB Network Company (BNC) announced a $160 million purchase of 200,000 BNB tokens, becoming the largest corporate BNB holder. It has since made multiple additional purchases, aiming to hold 1% of BNB’s total supply by end of 2025 and positioning itself as the "Strategy of BNB." Its total holdings have now reached 418,888 BNB, valued at about $368 million. CEO David Namdar (former partner at Galaxy Digital) stated BNC sees itself as the world’s largest corporate BNB holder and aims to deepen participation in the Binance Smart Chain ecosystem. Driven by these announcements, BNC’s stock has repeatedly risen, lifting its market cap.

Corporate treasuries are also emerging for newer public chain and protocol tokens. Many receive backing from project teams and top-tier VCs, entering public markets via "backdoor listings" or reverse mergers before conducting large-scale token accumulation: In June, the TRON Group completed a reverse merger with Nasdaq-listed small-cap SRM Entertainment, enabling a U.S. listing channel, later renamed Tron Inc., providing a funding source and compliant vehicle for future TRX treasury strategies. Mill City Ventures (MCVT) announced in July a $450 million private placement, allocating 98% of proceeds to buy SUI tokens, transforming into a firm with SUI as its primary reserve. StablecoinX made consecutive large purchases of ENA tokens in September, leading the community to suspect it might be an "ENA treasury company."

In summary, the DAT model is evolving from Bitcoin’s dominance to a competitive landscape across multiple chains and tokens. BTC treasuries remain dominant, ETH treasuries are catching up fast, SOL treasuries are aggressively expanding, and BNB is joining the race. More crypto assets are likely to be framed with "treasury stories" in the future. For each asset, long-term institutional lockups undoubtedly boost market confidence and scarcity; conversely, the asset’s own fundamentals determine how far the treasury strategy can go. If the underlying asset lacks intrinsic value or ecosystem support, simple hodling won’t sustain investor conviction.

4. Risks and Challenges of the DAT Model

Despite its impressive power in bull markets, the DAT model harbors procyclical risks and external challenges that cannot be ignored. The DAT sector has entered a competitive phase, with quiet elimination already underway. Key risk factors include:

1. Regulatory scrutiny tightening, limiting fundraising: In early September 2025, Nasdaq suddenly strengthened oversight of "crypto-buying listed companies." New rules require that if a listed company seeks to raise funds via new share issuance to purchase cryptocurrencies, it must first obtain shareholder approval through a general meeting. This aims to curb frequent equity issuance for token accumulation and stock price inflation. Regulators worry DAT could become a regulatory arbitrage tool—achieving ETF-like outcomes with lower listing barriers. Nasdaq’s new rules and SEC attention signal that the DAT model will face greater regulation, though in the short term, reduced fundraising efficiency may slow the flywheel.

2. mNAV discount and selling pressure: The market-to-net-asset-value ratio (mNAV) measures a DAT company’s stock price relative to the value of its held tokens. In bull markets, most DAT firms trade at mNAV significantly above 1, reflecting investor growth premiums. But if the market turns or confidence wavers, mNAV may quickly fall below 1—meaning stock price drops below the on-book value of crypto assets, resulting in discount trading. Since September, many DAT stocks have sharply declined, with mNAV collapsing alongside. Markets now question whether these firms can keep issuing and buying. When companies trade at persistent discounts, management faces intense pressure and may opt to sell underlying tokens to repurchase shares, attempting to push stock prices back toward NAV. If multiple DAT firms engage in such fire sales simultaneously, downward pressure on token prices could trigger a negative feedback loop.

3. Leverage and debt risks: To accelerate balance sheet expansion, DAT firms widely use high-leverage instruments such as convertible bonds, short-term credit, and reverse mergers. In bull markets, leverage magnifies gains smoothly. But when token prices plummet, leverage turns destructive, potentially triggering chain reactions. A sharp drop in underlying asset values could activate debt repayment clauses or margin calls, forcing companies to liquidate tokens to meet obligations or avoid default. The collapse of some crypto firms in 2022 could replay in the DAT space. Especially SPAC- or reverse-merger-listed DAT firms, which rely entirely on follow-up fundraising, may face rapid cash flow depletion if funding windows close.

4. Homogenized competition and risks of niche tokens: The surge in DAT firms this year has triggered signs of internal competition. As similar players flood in and "scarcity premium" fades, DAT firms face divergent fates. Weaker imitators with undifferentiated strategies may struggle to maintain high valuations or even face elimination. This is especially true for DAT firms focused on obscure altcoins, which may lose appeal once regulated products like ETFs emerge. Future performance of different DAT types depends on three factors: fundraising ability, holding scale, and yield generation. Firms with weak funding, small size, and no staking income may end up acquisition targets. Overall, the DAT sector is shifting from chaotic growth to survival of the fittest. Without differentiated strategies and strong execution, firms won’t survive PvP competition.

5. Macro and liquidity shocks: The DAT model links traditional equity markets and crypto spot markets, but under extreme conditions, it may cause a "double whammy." In scenarios like global liquidity tightening and simultaneous equity-bond selloffs, DAT stock prices and their held crypto assets could fall together, amplifying each other. Panicked investors may dump both risky equities and crypto simultaneously, subjecting DAT firms to dual selling pressure. If multiple DAT firms hold concentrated positions and face tight funding, coordinated sell-offs could easily trigger stampedes, causing severe crypto market volatility. As nodes of cross-market capital flow, DAT firms may exacerbate liquidity stress during crises.

In sum, the DAT model is inherently high-leverage and strongly procyclical—soaring like rockets in bull markets, free-falling in bear markets. 2025 will be a critical test period as the DAT narrative transitions from hype to stability. If the first half was dominated by flywheel myths, the second half marks a reality check driven by regulators and the market—only DAT firms with healthy capital structures, prudent asset allocation, diversified operations, and compliance awareness will survive the cycles.

5. Opportunities and Future Outlook for DAT

Despite numerous challenges, the digital asset treasury—as an innovative bridge between traditional finance and the crypto economy—remains promising. After maturing through standardization and natural selection, the DAT model could unlock new opportunities and profoundly reshape the crypto landscape:

1. A New Bridge for Traditional Capital: DAT offers many traditional institutional investors—unable to directly hold crypto—a regulated and convenient alternative. For example, pension funds, insurers, and family offices restricted by charters from buying tokens can instead invest in NYSE/Nasdaq-listed stocks. DAT gives them indirect crypto exposure. With the rollout of crypto ETFs, institutional access to crypto is diversifying, yet DAT retains unique appeal: active management and potential yield enhancement. ETFs passively hold tokens, while DAT managers can pursue returns beyond mere token holding via leverage, staking, and other strategies. This may attract more aggressive capital to quality DAT stocks. Long-term, DAT could coexist with ETFs and trusts, collectively increasing institutional allocation to crypto assets.

2. From Passive Hodling to Active Management: Most current DAT firms follow a "buy and hold" strategy. Looking ahead, they may evolve into more active digital asset managers—for example, generating yield via on-chain staking, lending, and market-making; gaining influence by participating in DeFi and node operations; or even entering RWA, tokenizing real-world assets to enrich portfolios. In the future, we may see DAT firms issuing structured products, deeply integrating with DeFi protocols, or emerging as proto-"on-chain banks."

3. Market Impact: Accelerating Crypto Financialization and Institutionalization: The DAT boom has directly lifted major token prices. This year, spot buying by DAT firms has been a key driver behind BTC and ETH price movements. Meanwhile, DAT accelerates crypto financialization: equity investors gain crypto exposure via DAT, on-chain assets become scarcer and more institutionally distributed due to treasury effects, possibly reducing volatility. Additionally, interaction between DAT and derivatives markets is growing—some hedge funds now conduct arbitrage based on DAT stock premiums/discounts, or go long on DAT stocks while hedging with futures. This draws traditional financial capital deeper into crypto market mechanics.

4. Long-Term Questions and Potential Directions: For DAT to achieve lasting success, several long-term issues must be addressed: effective private key and on-chain asset security management; balancing token holdings with core business development; maintaining investor confidence during crypto bear markets; and whether central bank digital currencies (CBDCs) or sovereign wealth funds might adopt DAT-like models in the future. Answers to these questions will unfold in coming years. If the industry consolidates, we might see the emergence of a "Crypto Berkshire"-style conglomerate holding multiple tokens and related businesses. In such a scenario, the DAT sector would mature, and its market impact would grow even more profound.

Looking ahead, as high-quality DAT firms stand out, the link between the crypto world and traditional finance will strengthen. Crypto price fluctuations will increasingly reflect corporate earnings reports and shareholder behavior; meanwhile, traditional stock markets may develop a "crypto asset概念股" segment whose performance closely tracks crypto market trends. Investor education and market awareness will also improve thanks to DAT—one clear example being retail investors learning about and embracing Bitcoin’s value through investing in Strategy. In this sense, DAT firms act as evangelists and value discoverers for crypto assets.

In 2025, DAT evolved from early experimentation to fierce competition, with opportunities and risks from the flywheel constantly intertwining. Going forward, only participants who understand financial fundamentals, rigorously manage risks, and embrace compliance will prevail in this new paradigm and lead the industry into its next phase. Regardless, the emergence of DAT signals broader acceptance of cryptocurrencies: from corporate balance sheets to investment portfolios, crypto assets are integrating into the real-world economy like never before. The idea of crypto as corporate reserves is now deeply rooted. The DAT model advances through twists and turns, and its long-term impact is irreversible.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News