The stablecoin sector is undergoing dramatic changes

TechFlow Selected TechFlow Selected

The stablecoin sector is undergoing dramatic changes

Exploring the turbulent developments in the stablecoin space amid changing regulatory and interest rate environments.

By: Tanay Ved, Coin Metrics

Translated by: AididiaoJP, Foresight News

Key Takeaways

-

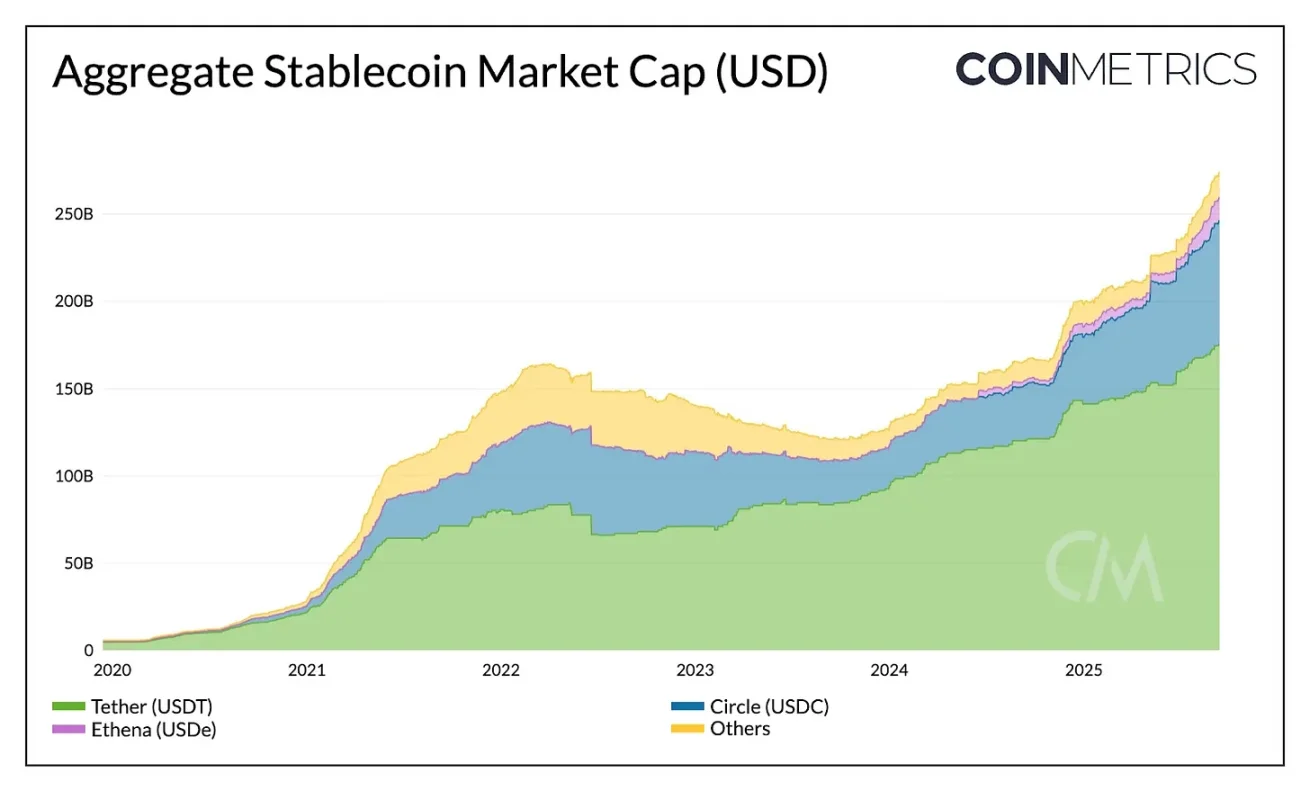

The total stablecoin market cap has reached $280 billion, up 40% year-to-date. USDT (64%) and USDC (25%) still hold the largest market shares, while USDe expanded by 133% after the GENIUS Act passed, becoming the third-largest stablecoin.

-

The GENIUS Act standardizes reserve backing with U.S. Treasuries, shifting competitive differentiation toward distribution, ecosystem reach, and ability to expand market adoption.

-

Circle’s revenue is driven by interest income from USDC reserves, primarily earned on Ethereum and Solana. However, most transaction activity revenue from USDC accrues to Coinbase (via sequencer revenue on Base) as well as to Ethereum and Solana (through fees and MEV).

-

These dynamics indicate that app-specific stablecoins and chains focused on stablecoins are emerging, aiming to capture and internalize more value across the entire tech stack.

Introduction

Momentum in the stablecoin space shows no signs of slowing down. In May, we analyzed various stablecoins, reserve models, and issuers across networks. In recent months, we've seen the U.S. introduce stablecoin regulation through the passage of the GENIUS Act, while Circle's IPO has brought the stablecoin business model into the mainstream. The competitive landscape is intensifying and appears to be in constant flux, with Tether announcing its entry into the U.S. market via USAT, fierce battles over the USDH ticker on Hyperliquid, and a series of payment-chain-focused launches from companies like Stripe and Circle.

In this context, this article explores the evolving dynamics in the stablecoin sector amid regulatory and interest rate shifts. With the GENIUS Act standardizing reserve backing for payment stablecoins, competition is increasingly shifting toward participants who control and capture distribution channels. We track Circle’s revenue from USDC across different blockchains to understand the forces driving the rise of proprietary stablecoins and dedicated networks.

Competitive Landscape: The Market After the GENIUS Act

Current Market Structure

The GENIUS Act was signed into law on July 18, creating a regulatory framework for dollar-backed payment stablecoin issuers. Key requirements include 100% backing by safe, liquid assets (cash, short-term U.S. Treasuries, and money market funds), and a prohibition on issuers offering yield or interest on issued stablecoins. This creates a new environment where collateralization of stablecoins is more standardized across issuers.

Before examining its impact, it's useful to assess the current state of the market. The total stablecoin market cap now exceeds $275 billion, up 40% year-to-date. Tether’s USDT leads with a 64% market share ($177 billion), primarily distributed across Ethereum (50%) and Tron (47%), while Circle’s USDC ranks second with a 25% share ($71 billion), spread across Ethereum, Solana, Arbitrum, and other networks.

Source: Coin Metrics Network Data Pro

Tether Enters the U.S. Market

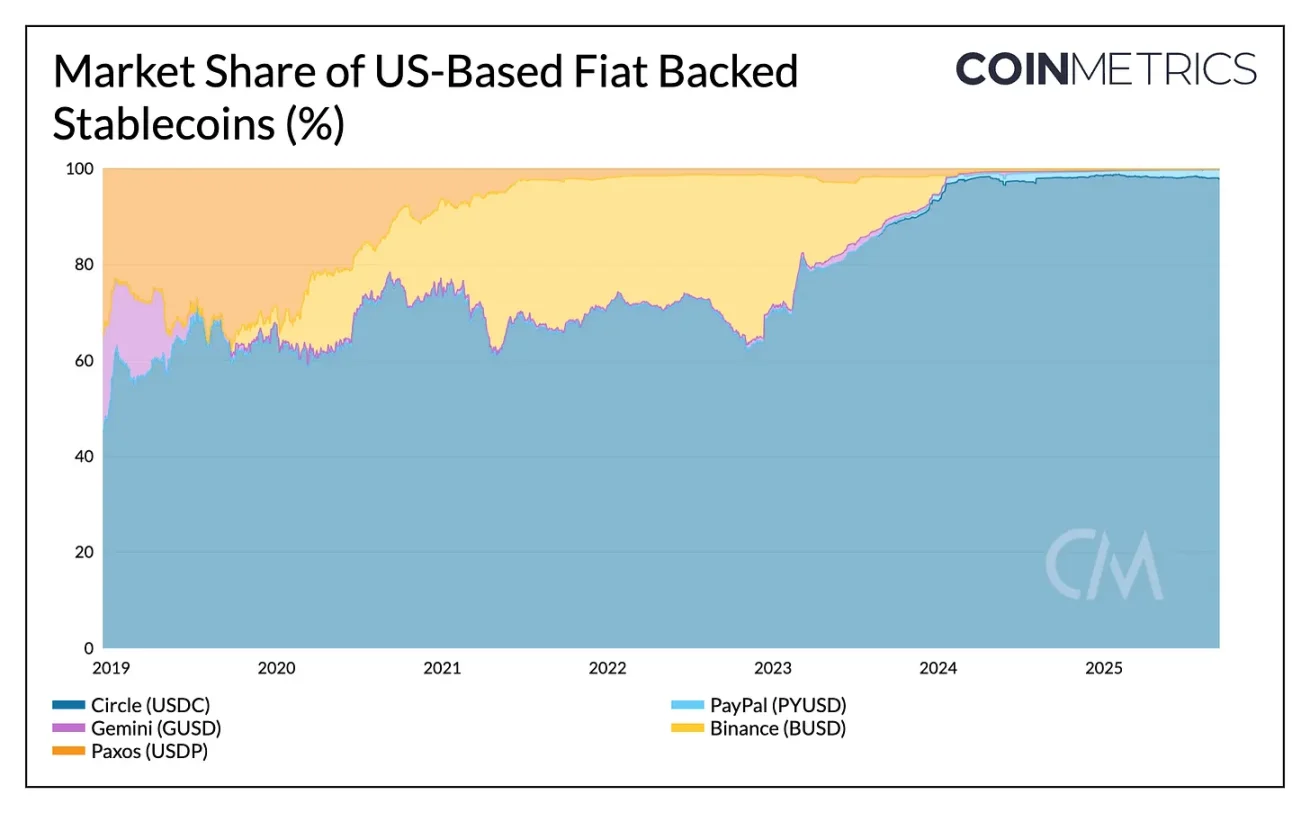

To date, Tether has operated as an offshore issuer headquartered in El Salvador, with USDT primarily serving demand in emerging markets. In contrast, Circle’s USDC benefits from a strong onshore regulatory position and currently accounts for 97% of domestic U.S. stablecoin supply.

In 2025, USDC’s market share grew by approximately 6%, while USDT’s declined by about 7%. However, Tether’s launch of USAT—a U.S.-compliant stablecoin—could erode USDC’s onshore dominance. Issued by Anchorage Digital and with reserves managed by Cantor Fitzgerald, USAT will need to gain traction in exchange listings and liquidity to match USDC’s multi-chain coverage and distribution achieved through partners like Coinbase.

Source: Coin Metrics Network Data Pro

Interest Rates and Yield Dynamics

The GENIUS Act’s ban on yield, along with changing interest rate environments, may also significantly impact the competitive landscape. Since stablecoin holders are prohibited from receiving direct compensation, interest income from U.S. Treasury reserves continues to accrue to issuers. Tether and Circle together hold over $145 billion in Treasuries, with Tether retaining all earnings, while Coinbase indirectly passes interest from USDC reserves to holders.

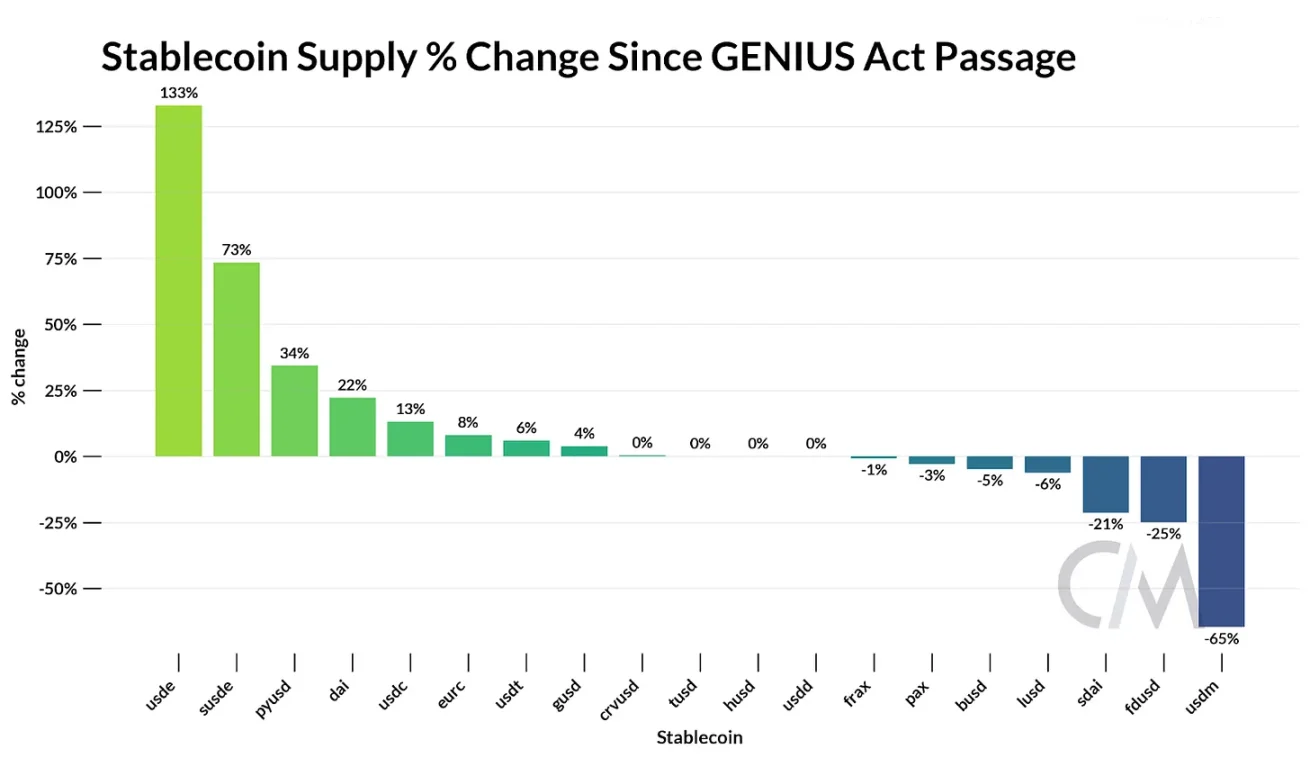

This gap could make interest-bearing alternatives and on-chain yield sources through staking or lending more attractive. Since the passage of the GENIUS Act, Ethena’s USDe has grown by 133%, while its staked version sUSDe has increased by 73%, making USDe the third-largest stablecoin with a market cap of $13.6 billion. By tokenizing basis trades using a delta-neutral strategy involving staked ETH and perpetual futures, Ethena can offer competitive yields even as interest rates decline.

Source: Coin Metrics Network Data Pro

Together, these dynamics highlight how competition is shifting from reserve models to distribution, yield, and ecosystem growth.

Tracking Circle’s Revenue Across Blockchains

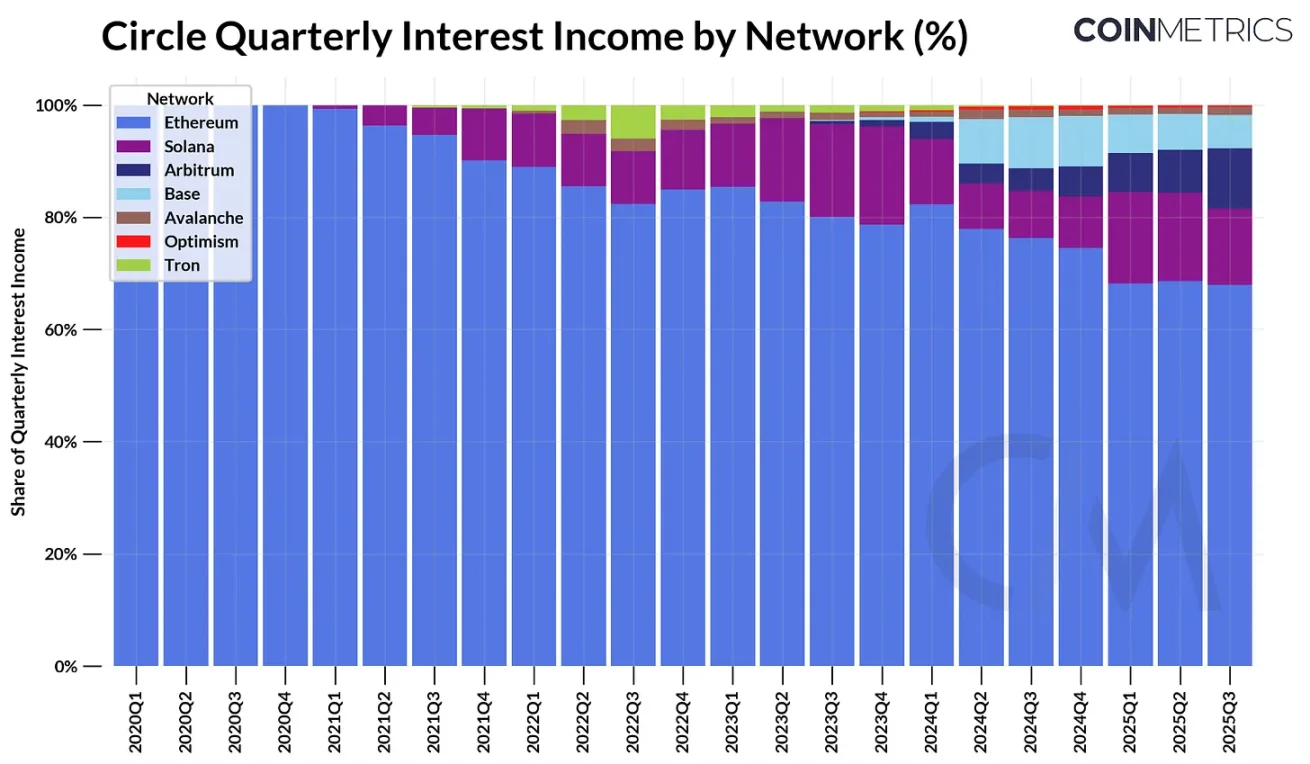

As a public company, Circle provides a clear blueprint for understanding the stablecoin business model. Its current revenue is straightforwardly driven by interest income from reserves supporting the outstanding USDC supply.

In Q2 2025, Circle earned approximately $634 million in interest income, based on its then $61 billion USDC supply and returns from short-term U.S. Treasuries backing it. Breaking this down by chain, Ethereum contributed the most at $423 million (68%), followed by Solana at $97 million (15%), while Arbitrum emerged as the fastest-growing source of supply and revenue (up 24% since Q1).

Source: Coin Metrics Network Data Pro

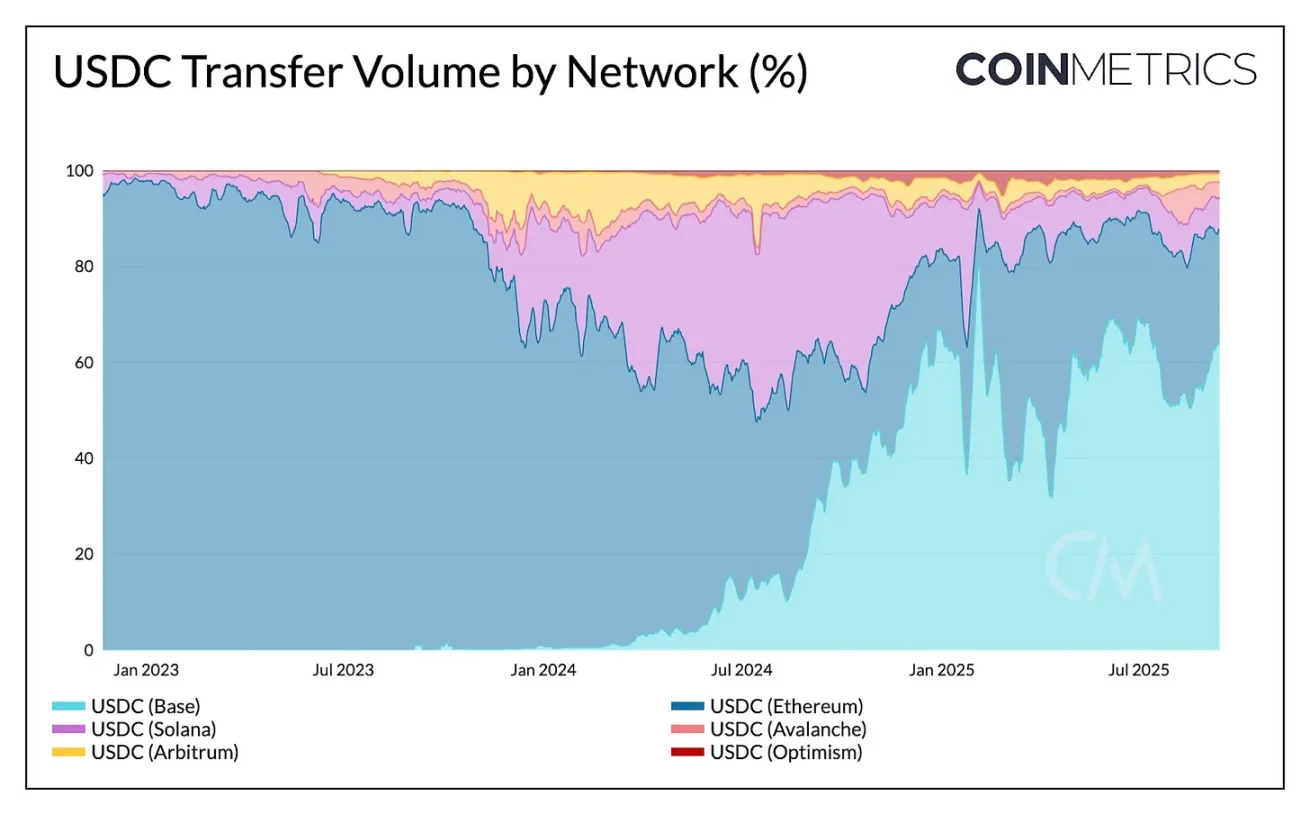

While USDC supply generates interest income for Circle, inter-chain transfers of USDC do not generate revenue. When analyzing the share of USDC transfer counts and volumes across networks, Solana dominates in transaction frequency, while Base (64%) and Ethereum (23%) account for the majority of total transaction volume. As a result, transaction activity revenue from USDC accrues to Coinbase (via sequencer revenue on Base) and to validators on Ethereum and Solana—not to Circle itself.

Source: Coin Metrics Network Data Pro

This underscores how Circle’s revenue is tied to outstanding USDC supply, while blockchains capture value from transfer activity through sequencing, fees, and MEV. The emergence of app-specific stablecoins like Hyperliquid’s USDH illustrates how platforms aim to internalize reserve income within their ecosystems. Meanwhile, Circle’s launch of its Layer-1 chain Arc signals its effort to capture transaction-based revenue from payments and FX-related use cases—activities that may not fully align with those currently dominant on existing networks.

Incentive Launches and Control Over Distribution

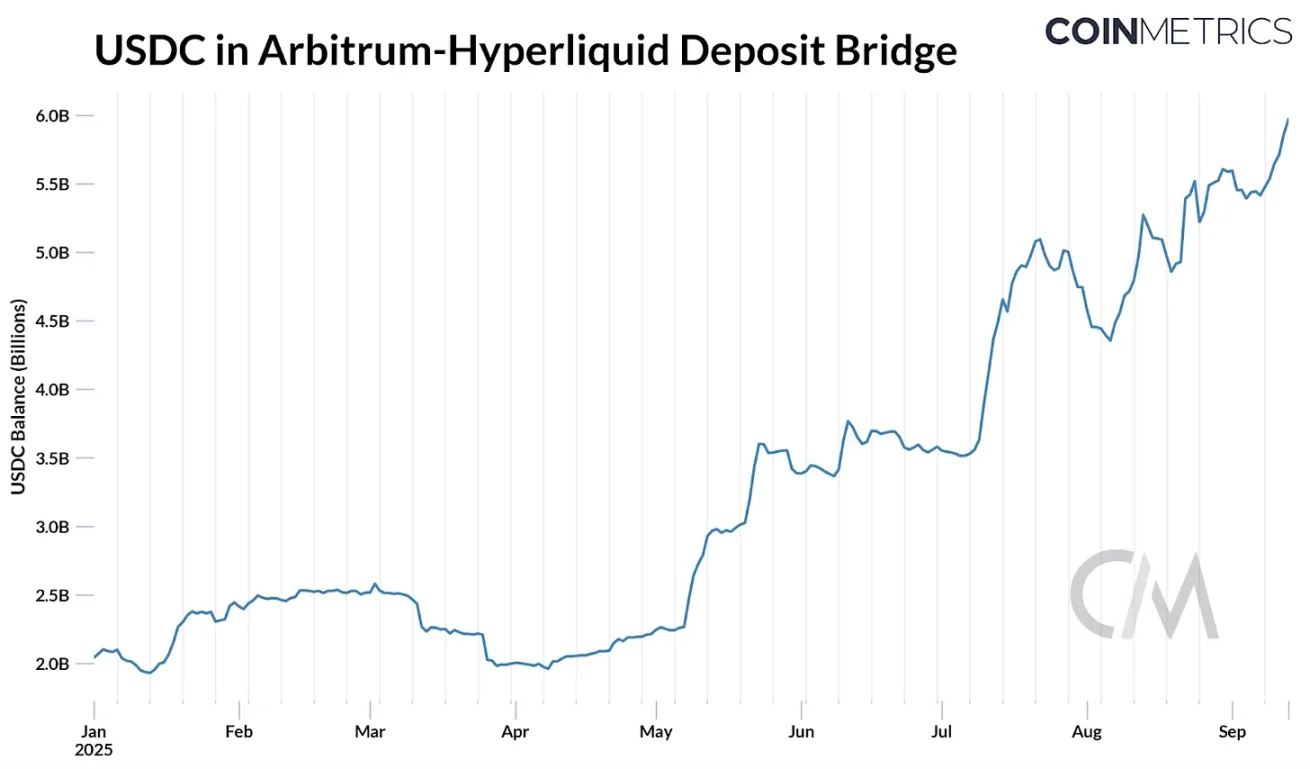

Recent events around Hyperliquid’s USDH ticker contest highlight why platforms want to reduce reliance on external sources and internalize economic benefits. Last week, Hyperliquid opened a governance vote to assign the USDH ticker to an issuer that is “Hyperliquid-first, aligned with Hyperliquid, and compliant.” Approximately 8% of all USDC supply (around $5.9 billion) sits in Hyperliquid’s Arbitrum bridge; at a 4.1% reserve return rate, this represents roughly $247 million in interest income flowing to Circle (and, via revenue-sharing agreements, to Coinbase).

Source: Coin Metrics ATLAS

This triggered a bidding war, drawing proposals from major issuers like Paxos, Ethena, Agora, and Sky, as well as newcomers like Native Markets. Issuers proposed terms to make USDH attractive to the Hyperliquid ecosystem, offering to return up to 95% of interest income, proposing favorable revenue-sharing models, or enhancing compliance alignment and distribution.

In the end, Native Markets won the USDH ticker through on-chain voting. Native Markets’ USDH will be fully backed by cash and U.S. Treasury equivalents, with off-chain reserves initially managed by BlackRock and on-chain reserves managed by Superstate via Bridge, owned by Stripe. In response, Circle is preparing to launch native USDC on Hyperliquid’s HyperEVM, underscoring that distribution on evolving platforms remains critical in the race for stablecoin dominance.

Other recent stablecoin launches also illustrate why apps, wallets, networks, and even states are moving in the same direction: issuing their own proprietary stablecoins to capture interest income and recycle it into ecosystem growth.

Conclusion

The stablecoin space appears to be undergoing simultaneous top-down and bottom-up transformation. At the macro level, the GENIUS Act standardizes requirements, tying stablecoin reserves to U.S. Treasuries and making distribution paramount. Competition between established players Tether and Circle enters a new phase, with USAT poised to challenge USDC on its home turf. With issuers banned from passing on yield, declining interest rates may elevate the role of alternatives like Ethena’s USDe, as demand for yield persists. At the micro level, the economics of reserve income and transaction activity are pushing platforms to internalize more value.

From the saga of Hyperliquid’s USDH to Circle’s Arc chain, this trend points toward greater control over the tech stack—whether by internalizing reserve income or capturing transaction-based revenue. These efforts also reflect anchoring stablecoins in payments and settlements. But the path forward raises important questions. Will a new wave of proprietary stablecoins fragment liquidity, or will distribution advantages concentrate demand around a few winners? As specialized payment chains with more centralized architectures emerge, will they complement general-purpose L1s or compete for activity? The evolution of this space is far from over, and how these forces play out will define the next chapter of stablecoin adoption.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News