Dune: The On-Chain Overview of Latin America's Crypto Financial Payment Ecosystem

TechFlow Selected TechFlow Selected

Dune: The On-Chain Overview of Latin America's Crypto Financial Payment Ecosystem

Stablecoins are the backbone of Latin America's on-chain economy.

Original: Dune

Compiled by: Will Wang

In Latin America, millions have turned to cryptocurrency/stablecoins out of necessity rather than speculation due to long-standing inflation, currency volatility, and limited access to traditional banking services. Cryptocurrency has evolved into a practical financial tool used for daily savings, remittances, and spending. Against this backdrop, Dune's report is groundbreaking in both breadth and depth, offering the first comprehensive view of Latin America’s crypto-financial ecosystem backed by on-chain data, with a focused lens on the most urgent and impactful application layer: crypto as payment.

Before you prosper, build roads. Similarly, we need to construct our analytical framework through four dimensions: exchanges, stablecoins, on/off ramps, and payment applications. Together, they form the infrastructure linking real-world use cases (such as remittances, salaries, savings, and payments) with crypto finance.

Dune’s report focuses primarily on an on-chain perspective, making it difficult to cover some large-scale real-world trade scenarios (e.g., import/export goods trade and the vast service trade in Latin America). Nevertheless, we can still observe from its on-chain data analysis the ecological niches and early development trajectories of local stablecoins, on-chain payment protocols, and DEXs within this active market—an insight valuable for participants in stablecoin payments.

As highlighted in Lemon Cash’s "2024 State of Crypto Report," Latin America is massive, rapidly changing, yet largely unmapped, with significant differences in usage patterns across countries: Brazil is driven by institutional flows and retail speculation; Mexico’s on-chain activity centers around remittances; Venezuela and Argentina heavily rely on stablecoins as hedges against inflation. Thus, Dune focuses on common and practical use cases rather than treating Latin America as a single market.

“The report shows that Ethereum and stablecoins are being used at scale for everyday savings, remittances, and consumption, with Brazil, Mexico, and Argentina leading an unprecedented wave of adoption. On-chain data provides hard evidence for this narrative, rarely revealing how the Latin American crypto market truly operates.” — Nathan, Devconnect Lead at Ethereum Foundation

Dune’s report is an exploratory, collaborative effort aimed at presenting key trends in Latin American crypto adoption, focusing on the “crypto as payment” use case. Given the region’s diversity in nations, languages, economic environments, and regulatory frameworks, the report does not aim to be a comprehensive market map but instead offers a scenario snapshot centered on real on-chain financial activities. Priority is given to projects primarily serving Latin American users and applying crypto to daily life (e.g., remittances, salaries, savings, payments), rather than “Latin American teams targeting global markets.”

Key Takeaways

Exchanges remain core financial infrastructure. They support retail adoption, institutional activity, and cross-border value transfer across Latin America: annual volume surged ninefold from 2021 to 2024, reaching $27 billion. Ethereum handles large settlements, Tron enables low-cost USDT payments, while Solana and Polygon carry growing retail traffic.

Stablecoins are the backbone of Latin America’s on-chain economy. Payment apps and stablecoins represent the region’s product-market fit, driven by distrust in traditional financial systems and economic crises. By July 2025, USDT and USDC accounted for over 90% of tracked exchange trading volume. Meanwhile, local-currency-pegged stablecoins are rising: BRL stablecoin volume increased +660% year-on-year, MXN stablecoins surged +1,100x YoY, becoming new tools for domestic payments.

Payment apps are evolving into “crypto-native digital banks.” Crypto has become backend infrastructure, with strong demand for payments and savings. Platforms like Picnic, Exa, and BlindPay integrate stablecoin balances, savings, and real-world spending into a single interface. Whether or not users have bank accounts, a young, mobile-first demographic increasingly uses crypto to meet daily financial needs.

1. The Four Pillars of Latin American Crypto Finance

Latin America is one of the most active regions globally for crypto adoption, driven by economic instability, financial exclusion, and daily necessity. Faced with persistent inflation, continuous currency depreciation, and inadequate traditional banking services, millions of people in the region have turned to cryptocurrency—not for speculation or novelty, but for survival, stability, and efficiency.

In the 12 months ending June 2024, the region received $415 billion in crypto value, with Brazil, Mexico, Venezuela, and Argentina ranking among the world’s top 20 (Chainalysis, 2024). Behavioral shifts are evident: in Argentina and Colombia, stablecoins have replaced Bitcoin as the most frequently purchased crypto asset; transaction volumes spike around payday each month as users convert salaries into digital dollars to preserve value (Bitso, 2024).

Within this ecosystem:

-

Stablecoins—whether pegged to the dollar or local currencies—are vital financial lifelines across Latin America, helping people save, send remittances, and maintain purchasing power. In 2024, over 70% of crypto purchases in Argentina were stablecoins (Lemon, 2024).

-

Exchanges (Lemon, Bitso, Ripio, etc.) are key liquidity gateways. Centralized platforms account for 68.7% of regional crypto trading volume, comparable to North America (Chainalysis, 2024).

-

On/off ramps (ZKP2P, PayDece, Capa, etc.) connect crypto with local economies, especially critical in countries underserved by traditional finance.

-

Payment apps (Picnic, Exa, BlindPay, etc.) make crypto truly usable, integrating wallets, remittances, exchanges, and even yield-generating features within mobile-native interfaces designed for local users.

These pillars together build a parallel financial system in Latin America—one often more stable, accessible, and practical than traditional alternatives.

2. Centralized Exchanges (CEX)

Centralized exchanges remain the primary gateway into crypto for Latin Americans, accounting for 68.7% of regional activity in 2024—slightly below North America but far above other emerging markets (Chainalysis, 2024). Users prefer regulated, fiat-onramp-enabled trusted platforms. These exchanges have expanded beyond basic trading into payments, savings, and cross-border transfers, becoming crucial entry points to the crypto economy.

The market is highly concentrated. According to Lemon’s 2024 report, Binance dominates with 54% of CEX trading volume in Latin America. Among regional competitors (Bitso, Foxbit, Mercado Bitcoin, etc.), Lemon leads with a 15% share, highlighting how local apps fill gaps left by global platforms (Lemon, 2024).

Use cases are also upgrading. On the retail side, exchanges offer increasingly rich functionality: in 2024, Bitso Pro (professional version) matched classic version trading volume despite fewer users, indicating outsized influence from advanced traders (Bitso, 2024). Institutionally, Brazil leads: from Q4 2023 to Q1 2024, transactions over $1 million rose 48.4% quarter-on-quarter (Chainalysis, 2024), driven by traditional finance interest, ETF demand, and the Drex central bank digital currency pilot. Major banks like Itaú and BTG Pactual have launched crypto investment services, blurring lines between exchanges and banks. SMEs also use exchanges for cross-border settlement and FX hedging; in Brazil, businesses pay Asian suppliers via crypto to avoid high bank fees, where local Bitcoin and stablecoins are widely accepted (Frontera, 2024).

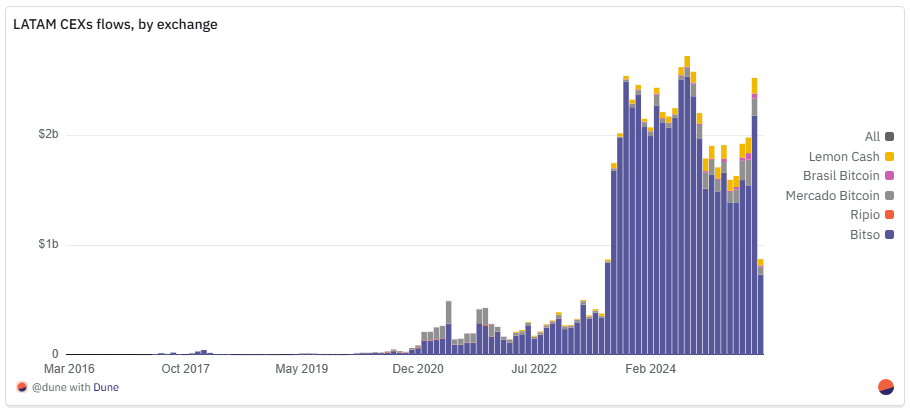

2.1 On-Chain Fund Flows Analysis of Latin American Exchanges

This analysis tracks asset movements into and out of exchange hot wallets, showing actual inflows and outflows at these platforms. Unlike “trading volume,” which reflects order book activity, on-chain flows record user deposits, withdrawals to external wallets, and settlements with other counterparties—thus providing a more accurate reflection of exchange usage, liquidity demand, and their role as on/off ramps between crypto and the real economy. Due to data availability limitations, native Bitcoin network activity is excluded, meaning total trading volume is underestimated, with BTC only represented via wrapped assets on other chains (e.g., BTCB).

From early 2021 to mid-2025, fund flows through Latin American centralized exchanges trace a clear curve of “growth–maturity–integration”: annual tracked transfer volume grew from $3 billion in 2021 to $27 billion in 2024.

-

In 2021, Bitso processed less than $2 billion, Mercado Bitcoin about $1.2 billion, and Brasil Bitcoin, Ripio, etc., merely tens of millions—the market was fragmented across OTC desks, informal brokers, and a few formal exchanges.

-

Diversification began in 2022, with newcomer Lemon Cash recording $90 million in its first year.

-

2023 marked a true inflection point, with trading volume quadrupling year-on-year: Bitso jumped from $2.5 billion to $13.6 billion; Lemon Cash nearly tripled to $260 million. Exchanges became deeply embedded in payment ecosystems, remittance corridors, and corporate treasuries. Inflation and currency depreciation in Argentina and Brazil boosted demand for stablecoins, making exchanges key USD on/off ramps.

-

Liquidity peaked in 2024: Bitso reached $25.2 billion, Mercado Bitcoin tripled to $915 million, Lemon Cash hit $870 million. Notably, this growth did not depend on a sustained bull market, reflecting real demand from cross-border trade, remittance settlement, and FX hedging.

-

Early 2025 saw a brief dip, hitting a recent low in January before steadily recovering, with monthly volume reaching a new high since September 2024 by July. Bitso recorded $11.2 billion in the first seven months, lower than its 2024 pace but still multiple times any pre-2023 year; Mercado Bitcoin $990 million; Lemon Cash $890 million—nearly matching last year’s record in just half a year.

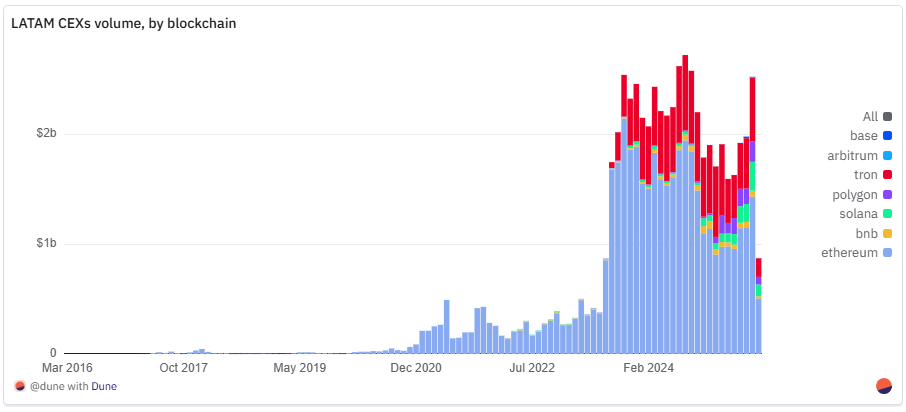

Beneath these transactions, the blockchain technology landscape is equally clear:

-

Ethereum has remained the backbone of exchange activity in Latin America. From January 2021 to July 2025, cumulative volume reached $45.5 billion, about 75% of total tracked volume, dominating large settlements, stablecoin, and tokenized asset flows.

-

Tron ranks second with $12.5 billion, benefiting from its lowest-cost USDT channel, widely used for remittances and cross-border payments.

-

Solana ranks third with $1.45 billion, slightly ahead of Polygon’s $1.17 billion. Since 2025, Polygon’s share has steadily risen, surpassing Solana’s 7.1% in July with 7.2% monthly share.

-

BNB Chain totals $963 million; Base ($23.6 million) and Arbitrum ($11.2 million) start small but grow fast: Base processed $22 million in the first seven months of 2025, compared to just $1 million in all of 2024; Arbitrum matched its entire 2024 volume by July.

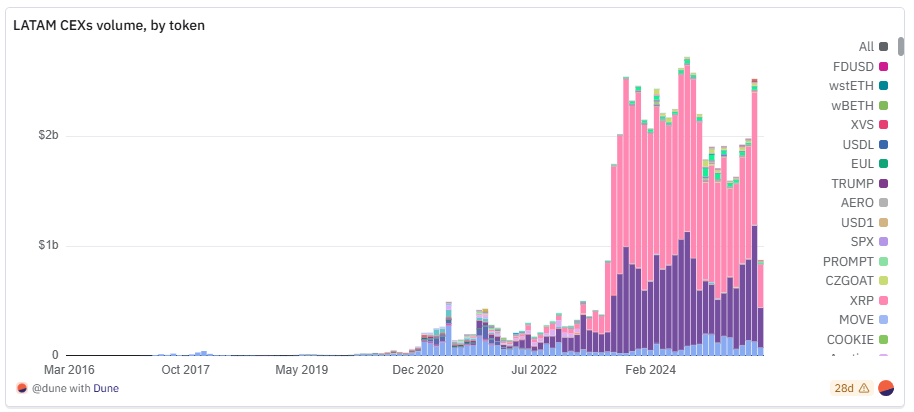

At the token level, stablecoins dominate overwhelmingly: in July 2025, USDT+USDC accounted for nearly 90% of transfer volume. From January 2021 to July 2025, USDT totaled $32.4 billion, almost twice USDC’s $18.36 billion, a gap mainly due to Tron’s dominance in USDT transfers. ETH itself ranked third with $4.74 billion; SOL made up about 1% of monthly volume in July 2025, totaling $660 million since 2021.

Structural changes are significant: from 2021–2022 and much of 2023, ETH trading volume often rivaled stablecoins, with BTCB, MATIC, etc., also on the leaderboard. Since late 2023, USDT/USDC share has sharply expanded, signaling a shift from speculation toward payments, remittances, merchant settlements, and dollar savings.

The evolution of blockchains and tokens points to maturity in the Latin American exchange ecosystem: Ethereum remains the main settlement rail, Tron monopolizes low-cost stablecoin transfers, and Polygon steadily gains share through payment use cases. Exchanges are increasingly becoming rails for payments and value transfer, not just speculative venues.

Lemon Cash is a typical microcosm: proof-of-reserves shows it held about $100 million in assets by mid-2025, mostly stablecoins, with stablecoin balances typically maintained between $20–30 million over the past year—highlighting its “retail dollar pipeline” positioning. Network activity spans multiple chains: most active withdrawal chains are Tron, BNB, and Ethereum; top deposit chains are BNB, Tron, and Stellar, with emerging L2s like Polygon and Base growing rapidly from small bases. This illustrates how regional exchanges dynamically adapt based on fees, speed, and accessibility, while Ethereum remains dominant for regional settlements.

Overall, blockchain and token data reinforce a structural narrative: Latin American exchanges have scaled massively on an “Ethereum-first, stablecoin-driven” foundation, with occasional speculative surges briefly reshaping rankings. Practical adoption coexisting with cultural vibrancy will define the future of exchange activity in the region.

2.2 Key Conclusions

-

Exchanges have upgraded to financial infrastructure: tracked annual flow volume grew from $3 billion in 2021 to $27 billion in 2024—a ninefold increase—evolving from fragmented OTC operations into large-scale platforms serving both retail and institutions.

-

Bitso’s flows rose from $1.96 billion in 2021 to $25.2 billion in 2024 (+1,185%), capturing the bulk of Latin America’s tracked volume; in the first seven months of 2025, it handled $11.2 billion, 44% of its full-year 2024 total.

-

Lemon tripled volume in 2023, reaching $870 million in 2024; already processed $840 million in the first seven months of 2025.

-

From January 2021 to July 2025, Ethereum accounted for ~75% (~$45.4 billion) of Latin American exchange flows, dominating large stablecoin and token transfers; Tron ($12.5 billion) monopolizes low-cost USDT remittances; Solana cumulatively $1.5 billion, though surpassed by Polygon in July 2025, which captured 8% that month.

3. Stablecoins

Stablecoins are the financial cornerstone of crypto adoption in Latin America, extending far beyond speculation. Across the region, they serve as savings tools, payment channels, remittance vehicles, and inflation hedges—the most practical and widely recognized form of cryptocurrency.

Latin America currently leads globally in “real-world stablecoin adoption”: Fireblocks’ “2025 State of Stablecoins” shows 71% of institutional respondents already using stablecoins for cross-border payments, 100% having launched, piloted, or planned stablecoin strategies; 92% claim wallet and API infrastructure readiness, underscoring demand and technological maturity. For millions, stablecoins are digital dollars—hedging against inflation, bypassing capital controls (Frontera, 2024)—often the only viable way to hold USD.

In Argentina, Brazil, and Colombia, stablecoins have overtaken Bitcoin as daily favorites due to price stability and direct dollar pegging (Fireblocks, 2025). This aligns with prior exchange data: USDC+USDT account for over 90% of transfer volume. In 2024, 72% of crypto purchases on Bitso Argentina were stablecoins, versus just 8% for Bitcoin; Colombia reached 48%, driven by restricted USD accounts and FX volatility; Brazilian local exchanges saw stablecoin trading volume rise +207.7% YoY, outpacing all other assets (Chainalysis, October 2024). In 2024, stablecoins made up 39% of regional purchase volume, up from 30% in 2023.

3.1 Local Stablecoins

A. Brazilian Stablecoins

Dollar-pegged assets still dominate, but local-currency-pegged stablecoins have grown rapidly over the past two years. Tokens pegged to the Brazilian real and Mexican peso are increasingly used for domestic payments, on-chain commerce, and integration with local financial systems. This eliminates repeated USD-to-local conversions, reducing costs for merchants and users while accelerating settlement.

For businesses, direct integration with systems like Brazil’s PIX enables bank-free, instant transfers compliant with accounting and tax requirements. In high-inflation economies, they act as “bridge assets,” allowing users to transact in stable local terms while quickly converting to USD or other stores of value when needed.

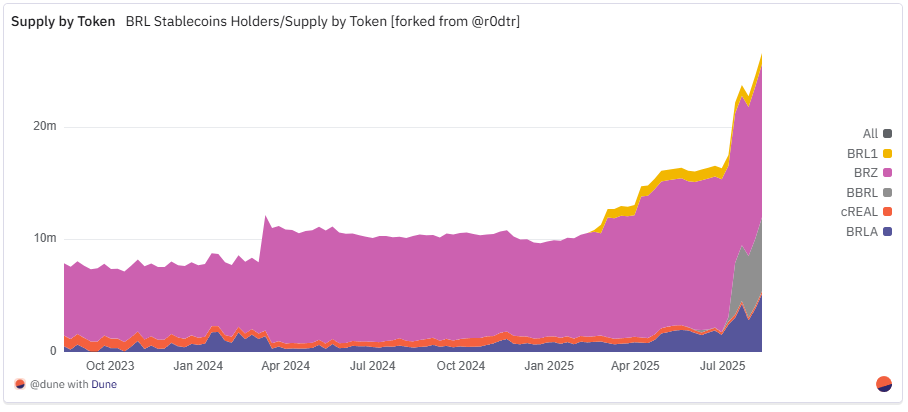

Brazil is the clearest example of this trend: BRL stablecoin transfer count grew from just 5,000 in 2021 to over 1.4 million in 2024, maintaining 1.2 million in the first seven months of 2025—a 230-fold increase in four years. Unique sender addresses rose from under 800 to over 90,000 in 2025, an 11-fold increase since 2023 alone. Native transfer value climbed from ~110 million BRL (~$20.9 million) in 2021 to nearly 5 billion BRL (~$900 million) in July 2025, approaching 2024’s full-year level; including August, 2025 has already surpassed last year. What began as niche experiments has in just years become a core pillar of Brazil’s on-chain economy, with transfer count, user base, and transaction value growing multiples—or hundreds of times.

As of June 2025, five different BRL-pegged stablecoins are actively circulating, with decreasing concentration—signaling ecosystem maturity. Despite rapid growth, BRL stablecoins remain in early stages, with current circulation around $23 million. Moreover, the market continues evolving rapidly. Iporanga Ventures’ latest “BRL Stablecoin Report” notes no absolute leader has emerged yet, but project-level data reveals distinct front-runners:

-

BRZ—issued by Transfero, which provides blockchain financial infrastructure for banks, fintechs, and payment firms. In terms of native transfer value, BRZ led by a wide margin until mid-2024; cREAL surged afterward, taking the lead. In early 2025, Celo’s volume advantage receded as BRLA steadily grew; by July, BBRL made a “dramatic” entrance—after launching on XRPL, its monthly native transfer value accounted for ~65% of the entire market, though active sender addresses remain relatively low.

-

cREAL—issued on the Celo chain, emphasizing mobile DeFi integration. cREAL leads significantly in transaction count, indicating first-mover advantage in retail and micro-payment use cases.

-

BRLA—launched by BRLA Digital/Avenia, focusing on compliant fiat-crypto bridging. BRLA has the most “unique senders,” suggesting broadest retail reach.

-

BRL1—backed by an alliance including Mercado Bitcoin, Bitso, and Foxbit, aiming to establish an industry-wide standard.

-

BBRL—released by Braza Group, targeting regional commercial and payment use cases.

Unlike dollar-pegged stablecoins, BRL stablecoin issuance and transfers concentrate on Layer 2s and alternative chains rather than Ethereum mainnet.

-

Polygon is currently the most active primary channel, leading in both native transfer value and user count: in July 2025, ~74,000 transfers occurred on this chain from 14,000 unique users, with monthly value reaching 500 million BRL—a record high.

-

Celo ranks second, with the highest historical cumulative transaction count: in December 2024, cREAL’s early breakout in retail and micro-payments drove a single-month peak of 213,000 transactions. In 2025, despite fewer unique senders, Celo maintains substantial volume through repeated large transfers from merchants, aggregators, and corporate treasuries.

-

XRPL, as a new entrant, performed strongly: with BBRL’s launch, transfer volume jumped from mere hundreds in May to ~3,000 in July 2025, while native value soared to ~1.16 billion BRL, revealing an emerging high-value corridor.

-

Base maintained steady growth in 2025, peaking in June; BNB Chain saw sharp declines in transaction count and sender addresses after 2022, shrinking its share. Ethereum mainnet plays a limited role, occasionally used for large, low-frequency transfers, although BRZ briefly led on this chain from late 2023 to early 2024.

Iporanga Ventures’ report emphasizes that actual adoption is driven by pragmatic, high-value use cases: B2B payments dominate, with companies paying overseas suppliers or employees, then settling locally via PIX; inbound flows convert USD into BRL stablecoins for domestic distribution. They are becoming key infrastructure in Brazil’s tokenized asset ecosystem, enabling bank-free on-chain settlements. In gig economy and SME sectors, stablecoins are used for payouts, hedging, and capital preservation; integrations like CloudWalk’s BRLC and Mercado Pago’s dollar stablecoin further expand mainstream reach.

B. Mexican Stablecoins

Brazil boasts the most diverse and mature local-currency stablecoin ecosystem, while Mexico’s peso-pegged market is forming, currently led by Juno/Bitso’s MXNB and Brale’s MXNe, each following distinct adoption paths. MXNB shifted from “one-time issuance scale” pulsing use in late 2024 to more continuous, decentralized daily circulation by 2025.

In 2025, MXNB showed a clear shift toward “everyday” use. In July 2025, the token recorded 179 transfers from 70 unique senders—far higher than 46 transfers and 21 users a year earlier, representing 339% and 290% YoY growth respectively. While volume peaked in January 2025—at 14.5 million MXN (~$750k)—with few transactions, July’s 480k MXN (~$25k) came from more numerous, smaller payments. Average transaction size dropped from ~28,700 MXN in July 2024 to 3,600 MXN. Accompanying this shift was a decisive migration to Arbitrum: ~99% of transfers occurred on Ethereum mainnet in 2024, but since Q2 2025, ~94% moved to Arbitrum, making low-fee L2 the default choice.

MXNe, issued by Brale, took another path: it has become the largest peso-pegged stablecoin in Mexico, operating entirely on Base chain. In March 2025, activity peaked with 3,367 transfers from 274 senders; even as transaction count declined, volume continued rising, hitting a record ~637.7 million MXN in July 2025 from 2,148 transfers and 158 senders, averaging ~297,000 MXN per transaction—indicative of high-value and possibly institutional use.

In contrast, the landscape is clear: MXNB now dominates small, retail-style payments; MXNe focuses on large settlements. Compared to Brazil’s diversified, multi-chain real ecosystem, Mexico’s market remains concentrated on two issuers and fewer chains—but this hasn’t hindered liquidity growth. Since mid-2025, peso pairs have rapidly climbed into the top tier of DEX trading volume, signaling maturing market structure.

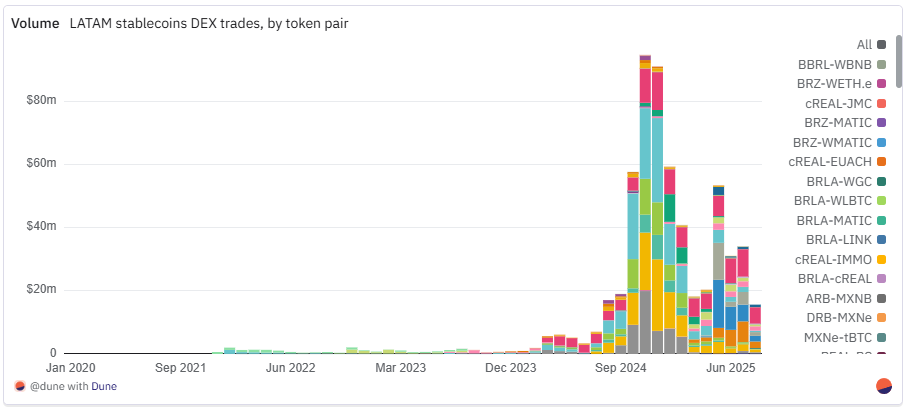

3.2 Decentralized Exchanges (DEX)

The rise of BRL- and MXN-pegged stablecoins in Latin America has gone beyond “payments,” now providing substantial liquidity to decentralized exchanges (DEXs) and forming foreign exchange corridors between local currencies and global stablecoins on-chain.

BRL Assets

cREAL remains the trading hub. Its largest pair, CELO–cREAL, has cumulatively traded ~$126 million, leveraging deep liquidity on Celo’s native DEX; it also acts as a “benchmark currency” for multi-asset swaps, with sizable pairs like cREAL–USDT ($87.7M), cREAL–cUSD ($59.1M), cEUR–cREAL ($48.6M), and cKES–cREAL ($24.9M). However, cREAL’s monthly DEX volume peaked at $80M in November 2024 (85% of monthly stablecoin volume) before declining continuously, dropping to $5M in July 2025—back to year-earlier levels.

BRLA is emerging as the main USD gateway, with BRLA–USDC ($97.5M) and BRLA–USDT ($21.3M) as core pairs. Since March 2025, BRLA–USDC has almost consistently been the largest USD-denominated pair in the dataset (briefly surpassed by an MXNB pair in May). Though BRLA hasn’t reached cREAL’s peak, its total trading pairs reached $9M in July 2025—nearly double cREAL’s that month and triple its own July 2024 volume.

BRZ has the broadest liquidity distribution, with pairs like BRZ–USDC ($15.1M), BRZ–USDT ($14.7M), and BRZ–BUSD (~$9.1M) spread across multiple chains; volume, though modest, has grown steadily from $26k in July 2024 to $3M in July 2025, peaking at $4.77M in April.

MXN Assets

MXNB’s largest pairs are MXNB–WAVAX ($29.7M) and MXNB–USDC ($18.6M), spiking in May 2025 due to large transactions and liquidity inflows; afterward, peso pairs remained strong, with the top three MXN pairs staying firmly in the top tier of local stablecoin DEX volume—showing growth isn’t “one-off.”

MXNe operates solely on Base, concentrating on MXNe–USDC (~$18.3M). DEX volume grew steadily from $1.13M in March to $6.6M in July, aligning with Base’s push for “local stablecoins integrated with deep USD pools.” Interestingly, MXNe leads MXNB in on-chain transfer value, but MXNB has higher DEX volume, suggesting MXNe leans toward high-value transfers and USD integration, while MXNB suits active on-chain trading.

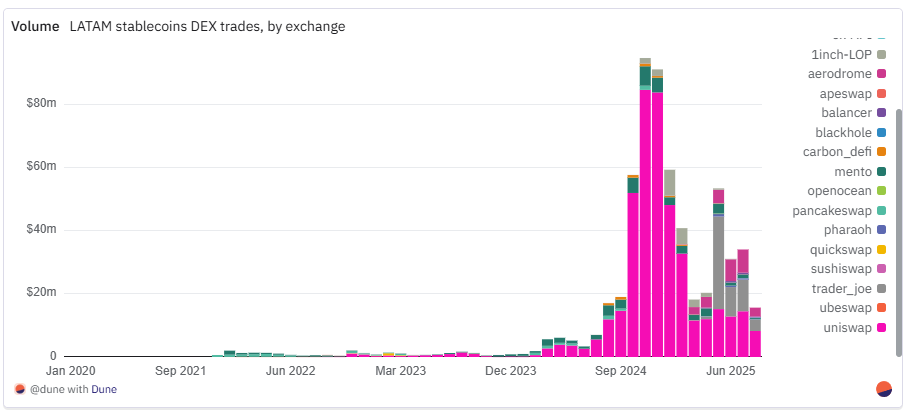

Volume concentrates on a few DEXs, each deeply tied to specific local stablecoin ecosystems. Uniswap remains the liquidity giant with $426M total volume, dominating BRL- and MXN-pegged stablecoin markets on Ethereum and its L2s. Chain-native DEXs hold decisive shares in their own stablecoins: Avalanche’s Trader Joe ($52.8M) and BNB Chain’s PancakeSwap ($13.3M) absorb most BRZ liquidity; Celo’s Mento ($50.8M) is cREAL’s exclusive home. 1inch Limit Order Protocol works differently, acting more like an aggregation settlement layer, often appearing in one-off large swaps rather than maintaining deep pools.

The most notable new trend in 2025 is Aerodrome’s rise: powered by the MXNe–USDC pair, its cumulative volume reached $25.8M, almost entirely from Q2 onward. As a core anchor for local stablecoins on Base, Aerodrome’s role mirrors Mento in the Celo ecosystem. Smaller but noteworthy are Carbon DeFi ($4.8M), Pharaoh ($1.95M), and Balancer (~$1.8M), serving fragmented or niche cross-asset pools.

Overall, local stablecoin liquidity continues expanding absolutely, increasingly relying on chain-native DEX infrastructure—with Aerodrome’s rapid ascent standing as the clearest example of 2025.

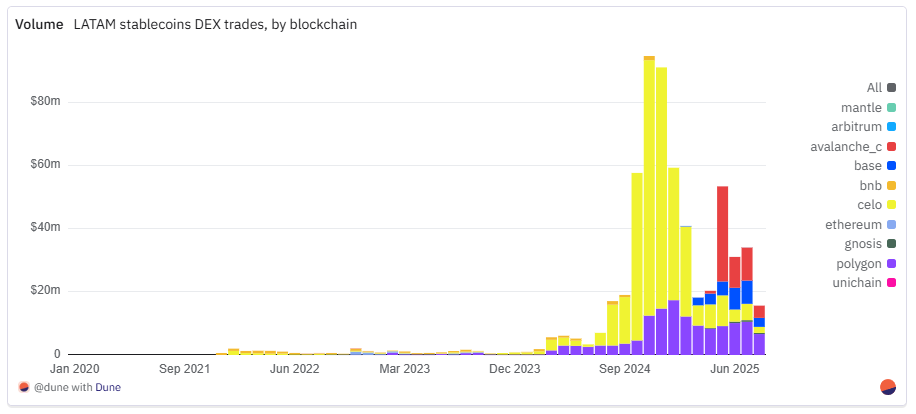

Liquidity structure remains tightly coupled with each stablecoin’s “home” blockchain and its leading DEX:

-

Celo leads with $363M total volume, almost entirely from cREAL–cUSD/USDC pairs on Mento, consistently topping USD-denominated volume from July 2024 to February 2025.

-

Polygon follows with $136M, aggregating multiple real stablecoins like BRLA and BRZ via Uniswap and QuickSwap, catering to both transfers and DeFi/payment use cases.

-

Avalanche ranks third (~$54.8M), with Trader Joe’s MXNB–WAVAX pair spiking in May 2025 due to large inflows, while Uniswap, Pharaoh, and 1inch Limit Order Protocol jointly provide depth for BRL/MXN markets.

-

Base (~$26.2M), nearly all from the MXNe–USDC pair on Aerodrome, aligning with Base’s 2025 push for local stablecoins.

Core conclusion: DEX liquidity for local stablecoins follows “ecosystem as home,” with each major public chain pairing flagship assets with a few dominant exchanges. The two breakout cases of 2025—Trader Joe on Avalanche for MXNB, Aerodrome on Base for MXNe—show that when a local stablecoin gains strategic importance, on-chain adoption and exchange dominance reinforce each other.

Beyond Brazil and Mexico, other Latin American countries have experimented with local-currency stablecoins, but most remain early-stage or in pilot:

-

Argentina: With volatile pesos, Transfero’s ARZ and Num Finance’s nARS struggle to gain traction.

-

Colombia: Multiple options exist—nCOP (Num Finance), cCOP (Celo/Mento), COPM (Minteo), COPW (Bancolombia)—targeting remittances and local payments, but adoption remains moderate.

-

Chile’s CLPD (Base) and Peru’s nPEN (Num Finance), sPEN (Anclap, Stellar) remain niche, mostly used in pilots or specific payment channels.

These projects reflect rising regional interest, but limited volume again highlights the decisive roles of currency stability and regulatory clarity in determining whether local stablecoins can scale.

3.3 Key Conclusions

Stablecoins are the “spine” of Latin America’s on-chain economy. Dollar- and local-currency-pegged stablecoins have replaced high-volatility assets as the core of crypto applications, sustaining double- or even triple-digit growth.

In July 2025, USDT and USDC accounted for over 90% of exchange transfer volume, up from ~60% in the same period in 2022.

Brazil leads in both number of active local stablecoins and total activity. In the first seven months of 2025, BRL stablecoins processed $906 million—almost matching 2024’s full-year total ($910 million), implying an annualized run rate of ~$1.5 billion.

In Mexico, peso-pegged stablecoins (MXNB + MXNe) totaled ~$34 million in July 2025, versus just 1 million MXN (~$53k) in July 2024—a ~638x YoY increase.

Main on-chain corridors for local stablecoins: Polygon (BRLA, BRZ), Celo (cREAL), Base (MXNe), and Arbitrum (MXNB).

4. On/Off Ramps

Coexisting centralized and peer-to-peer on/off ramps serve as the most critical “connective tissue” between Latin America’s crypto economy and traditional finance. In countries like Argentina, Brazil, and Mexico, users often convert their salaries into stablecoins on payday—treating crypto as a “buffer” rather than a bet—to protect against local currency fluctuations.

-

Brazil: The government-backed Pix payment system has become the primary fiat→crypto on-ramp, offering instant settlement and near-zero fees.

-

Argentina: Due to capital controls and economic uncertainty, informal “cuevas” (underground exchanges) remain major outlets, even as formal platforms grow substantially.

Behavioral data from Bitso (2024) shows on-chain activity spikes at specific days and times each week, closely aligned with pay cycles—again proving crypto is a “preservation tool,” not a speculative toy.

New players in the infrastructure layer—PayDece, zkP2P, Takenos, etc.—are introducing non-custodial, mobile-first solutions targeting groups overlooked by traditional finance, enhancing financial self-sovereignty, signaling a shift toward “decentralized, censorship-resistant” ramps.

For Latin America’s growing freelance and remote workforce, crypto off-ramping has become an essential part of their tech stack: they receive international income in stablecoins, bypassing volatile local currencies and banking barriers (Frontera, 2024).

4.1 ZKP2P

ZKP2P is a decentralized, minimally trusted P2P on/off ramp protocol leveraging advanced cryptography like zkEmail and zkTLS to enable direct, intermediary-free, zero-additional-verification, zero-fee exchanges between fiat and crypto assets. Launched at end-2023, upgraded to V2 in 2024, it now supports multiple chains (Ethereum, Solana, Base, Polygon) and various assets—from USDC, ETH to popular local tokens and even meme coins.

Argentina: ZKP2P integrates with Mercado Pago, enabling near-instant conversion between Argentine pesos (ARS) and USDC.

-

The dedicated Latin America channel has completed over 100 on-ramps, totaling over 3,000 USDC, averaging $30 per transaction, ranging from $1 micro-transactions to $356 large ones.

-

In the past week, median settlement time was ~30 minutes—“blazing fast” by P2P standards.

Global data:

-

V2累计 4,861 入金,金额超 190 万美元(V1+V2 合计 208 万美元)。

-

全支付通道流动性 11.4 万美元;头部走廊:Venmo(55.9 万)、Revolut(47 万)、Wise(39 万)、Cash App(32.7 万)。

-

全球平均单笔 385 美元,为拉美均值 12 倍,显示后者仍有巨大放大空间。

Next steps: Upcoming integration with more local rails like Brazil’s PIX will expand low-barrier, high-frequency use cases. A prime example—Daimo Pay × ZKP2P × World Account: users can one-click convert Worldcoin’s $WLD into pesos within the World App, fully on-chain and non-custodial, arriving in 15 minutes, turning “UBI airdrops” into “disposable income.”

“ZKP2P turns stablecoins into daily pocket money—you can convert USDC to Argentine pesos in minutes, fully on-chain and transparent, without the friction of traditional banks.” — Ben, Growth Lead at ZKP2P

4.2 PayDece

PayDece is a P2P crypto on/off ramp platform built on Web3 principles (decentralization, privacy, self-custody). Using smart contracts, it enables secure and anonymous transactions without centralized intermediaries or mandatory identity verification (KYC).

To date, PayDece has processed over 44,000 transfers across all supported chains, involving an estimated 15,000 unique users. Activity is highly concentrated in stablecoins: $19.17 million in USDT, $7.74 million in USDC. Chain distribution is led by BNB Chain ($19.5 million), followed by Polygon ($6.3 million), Avalanche ($1.68 million), and Base ($830k).

Since late 2023, PayDece has shown strong early growth: monthly volume rose from under $300k in November 2023 to $1.79 million in July 2025, peaking above $2.4 million at end-2024. Transaction count and user numbers rose in tandem, with clear spikes in April 2024, November–December 2024, and June–July 2025. Current volume remains well above early adoption levels, indicating a stable base of returning users and sustained transaction flow.

With its privacy-first design, multi-chain support, and growing on-chain liquidity, PayDece is emerging as a major decentralized alternative for Latin American users seeking censorship-resistant, self-custodied on/off ramp solutions.

4.3 Capa

Capa is a financial infrastructure provider focused on “making crypto seamlessly work in Latin America.” Through a unified API, it allows fintechs, enterprises, and payment apps to embed stablecoin rails, conduct fiat-crypto exchanges, and drive cross-border transactions directly within their services. By prioritizing liquidity, compliance, and multi-chain networks, Capa solves pain points of fragmented payment systems and high cross-border remittance costs in Latin America.

User on-chain distribution

-

As of July 2025, Capa had accumulated over 900 unique addresses, with transactions highly concentrated on “low-cost + fast settlement” chains: Polygon (68%), Base (10%), Arbitrum (7%), Ethereum (4%), Solana (4%). Compared to December 2024 (Solana 20%, Polygon 33%), the migration trend is evident.

Fund flows

-

Retail (B2C): 1,173 cumulative on-ramps, 809 off-ramps; both demands have significantly increased since 2025.

-

Average monthly retail on-ramp amount rose from $200 in July 2024 to $1,300 in July 2025; off-ramp amount rose from $336 to $1,200, reflecting rising stablecoin exchange and withdrawal demand as the platform connects with more regional partners.

Total volume and chain breakdown

-

Since launch: 5,501 transactions, $29.9 million total value. – Polygon: $14.1 million – Solana: $6.95 million – Tron: $2.73 million – Optimism: $2.52 million – Arbitrum: $1.26 million – Base: $1.11 million – Ethereum: $1.06 million – Rest from BNB Chain, etc.

Flagship case

-

Capa is the sole platform offering fully compliant 1:1 Mexican peso ↔ MXNe (Base-chain peso stablecoin) on/off ramps, supporting MXNe issued by Etherfuse, powered by Brale’s infrastructure, and listed on Coinbase Wallet—setting a benchmark for “local-first” financial tools.

Positioning

-

Though not面向终端用户,Capa has become a key底层 player in Latin America’s crypto economy, delivering compliant, efficient, and scalable crypto capabilities to wallets and fintechs across the region via its dual engines of on/off ramps and real-time settlement.

“For Latin America, crypto means opportunity. Capa connects fragmented economies, enabling seamless access to the global financial system.” — Jonathan Herrera, Head of Capital Markets at Capa

4.4 Key Conclusions

On/off ramps are narrowing the “gap” between on-chain and local economies. Permissionless protocols and compliant infrastructure advance in parallel, making movement between Latin American fiat and crypto faster, cheaper, and simpler.

-

ZKP2P opens a novel on/off ramp path via non-custodial, cryptographic solutions, enabling near-instant swaps between stablecoins and local currencies. Global V2 has surpassed $1.87 million, but Latin America accounts for only ~$3,000; with upcoming integrations like Brazil’s PIX, growth potential is immense; median settlement time is ~41 minutes, making frictionless P2P fiat⇄crypto exchange a reality.

-

PayDece is growing into a decentralized, reusable stablecoin transfer platform: 15,000 users, $27.8 million cumulative volume, 6x growth since late 2023, and stable monthly volume of $1–2 million—indicating maturing demand for “censorship-resistant entry points” in Latin America.

-

Capa facilitated $29.9 million in on/off ramps and cross-border stablecoin settlements via API, with rapid growth on Polygon and Solana, highlighting its role as a key enabler for “cross-border expansion of fintech and B2B applications under compliant conditions.”

5. Payment Applications

Crypto-powered payment apps and “crypto-native digital banks” are becoming among the most effective distribution channels in Latin America. Exchanges like Lemon, Belo, Buenbit, and Ripio issue both physical and virtual cards usable for daily spending; platforms like Picnic, BlindPay, and Exa offer USD-denominated balances, yield features, and stablecoin payments within a single app, positioning themselves as “crypto-native neobanks.” Demand is accelerating: according to Lemon, Latin American crypto app downloads doubled YoY in Q2 2024, showing user motivation shifting from “hype” to “necessity.”

-

Argentina: Lemon Cash’s crypto card lets users spend in stablecoins with bills settled in pesos, while earning Bitcoin cashback—integrating savings and spending into one incentive loop.

-

Unbanked populations: In rural or financially excluded areas, crypto apps aren’t supplements—they directly replace TradFi.

5.1 Picnic

Picnic is a decentralized investment platform on blockchain, aiming to simplify digital asset access. Its Smart Wallet uses Safe contracts and ERC-4337 account abstraction, allowing users to sign up with just an email while retaining self-custody. Beyond investing in curated crypto portfolios, Picnic extends into real-world payments via “Picnic Pay”—partnering with Gnosis Pay to launch Brazil’s first stablecoin debit card.

-

Users can top up Gnosis Pay cards via Pix (Brazil’s instant payment system), with BRL automatically converted to USD and settled on-chain.

-

The card supports online and offline spending and can be linked to Apple Wallet / Google Wallet.

-

Picnic Pay connects directly to DeFi protocols, e.g., allowing Aave funds or yield-bearing BRL stablecoins to be used directly for card payments.

All USDC.e activity generated by Picnic comes from Gnosis Pay’s operations in Brazil, currently accounting for ~7% of Gnosis Pay’s weekly transaction volume but nearly 15% of weekly payment count—indicating low average ticket size but very high transaction frequency.

Since launch, Picnic has exceeded 350 daily active users, processing 45,000 payments weekly, with weekly transaction value exceeding $150k. Activity remained strong after its debut at Rio Web Summit in April 2025: averaging 800–1,000 daily transactions, peaking above 1,100. End-July user balance was $80k, below the monthly peak of $200k, showing funds are actively rotated rather than stored long-term—consistent with its “spending tool” rather than “long-term savings” positioning.

Picnic partnered with Avenia to launch a BBRL yield product, expanding savings offerings to include interest-bearing versions stBRLA and yBRLA, yielding ~12% APY, indexed to Brazil’s CDI rate. Beyond savings, Picnic integrates with major DeFi platforms like Aave and Morpho, enabling BTC lending in Brazil, further expanding multi-use cases of local stablecoins—“earning, trading, credit.”

By integrating Picnic Pay with DeFi yields, the platform bridges asset management and daily payments. Embedding stablecoin debit cards into investment apps and connecting interest-bearing, self-custodied assets directly to spending is still an emerging model in Latin America—local payment rails like Pix serve as bridges between fiat and on-chain settlement.

“Picnic lets Brazilians spend foreign currency at exchange rates 4% cheaper than Wise, while offering non-custodial token purchases, yield, and free BRL on/off ramps via BRLA integration (Pix).” — João Ferreira, Co-founder & CEO of Picnic

5.2 Exa App

Exactly Protocol is a decentralized, non-custodial interest market offering both floating and fixed-rate borrowing, with rates determined by fund utilization across multi-term pools.

Exa App brings this model to mobile: users deposit assets like USDC, ETH, wstETH, WBTC, OP, keeping funds self-custodied while earning continuous floating yields until spent. After completing KYC (to meet Visa compliance), users receive the Exa Card—a blockchain-based payment card supporting two spending modes:

-

Pay Now (immediate payment): deducts directly from yield-bearing balances.

-

Installments (installment payment): borrows from Exactly’s lending pool at a fixed rate at time of purchase, repayable over up to six installments.

Latest data shows Exa App user balances at $1.62 million (TVL ~$1.08 million), with ETH and USDC each around $650k, WBTC about half that, and other tokens minor.

Exa Card has cumulatively processed $5.04 million in payments, with the vast majority being Pay Now transactions; Installments account for $793k. In contrast, lending remains small: 69 loans, 30 borrowers, totaling $47.4k.

Overall, current usage is dominated by card spending, with lending volume limited. The combination of “yield-bearing deposits + fixed-rate consumer loans” forms a unique on-chain payment model—the user’s net cost or gain depends on the spread between deposit yield and loan rate.

“Crypto adoption in Latin America isn’t a trend—it’s a necessity. Exa App is building tools that make this adoption useful, accessible, and real.” — Gabriel Gruber, Founder & CEO of Exa App

5.3 BlindPay

BlindPay provides API infrastructure enabling businesses to send and receive payments globally in fiat and stablecoins. It encapsulates compliance, regulatory requirements, and integration with diverse payment rails (Pix, SPEI, PSE in Latin America; ACH, Wire, RTP, SWIFT in the U.S.) at the backend, while supporting Ethereum, Arbitrum, Base, Polygon, and Tron on the blockchain side—enabling interoperable settlement between crypto and local fiat systems. Core features include:

-

API-first integration: developer endpoints to embed global payments into any app.

-

Infrastructure-layer compliance: built-in KYC/KYB, anti-fraud, and regulatory alignment.

-

Local + cross-border payments: supports both regional instant payment systems and stablecoin transfers.

-

Settlement speed: drastically faster than traditional channels.

Since launch, BlindPay has processed $93 million across all operational regions (U.S., Brazil, Mexico, Argentina, Colombia), with most concentrated in Latin America; beyond June data, the team disclosed an additional ~$70 million in July–August. On-chain, Polygon accounts for $91.86 million (~99%), Arbitrum $7.56 million, Base $4.26 million; monthly volume grew from millions mid-2024 to tens of millions monthly in 2025, showing expanding API adoption and payment corridors.

By stitching stablecoin rails with local payment infrastructure, BlindPay fills the operational gap between blockchain settlement and real-world disbursement—especially suitable for Latin American businesses spanning multiple currencies, banking systems, and jurisdictions.

“We reduced Latin American cross-border remittance costs from 1.5% to 0.1% and cut settlement time from 2–3 business days to seconds; simultaneously, virtual dollar accounts democratize USD access, allowing any individual or business to hold and trade USD without a U.S. bank account.” — Bernardo Simonassi Moura, BlindPay CEO

5.4 Key Conclusions

Payment apps are transforming into “crypto-native digital banks.” One-stop integration of savings, yield, and daily payments, mobile-first and stablecoin-driven, serving both banked and unbanked populations.

-

Picnic processes 45,000 payments weekly via Gnosis Pay, offering ~12% APY yield products on local stablecoins.

-

Exa App card payments total $5.04 million, with 85% in “Pay Now” mode, funds continuously earning yield.

-

BlindPay has processed $93 million, 99% on Polygon, integrating Pix (Brazil), SPEI (Mexico), PSE (Colombia) for compliant, second-level disbursement.

-

Lemon Cash, Nubank, Mercado Pago, etc., are embedding crypto directly into consumer banking stacks—e.g., Lemon’s stablecoin card offering BTC cashback, Mercado Pago’s self-developed dollar stablecoin Meli Dólar.

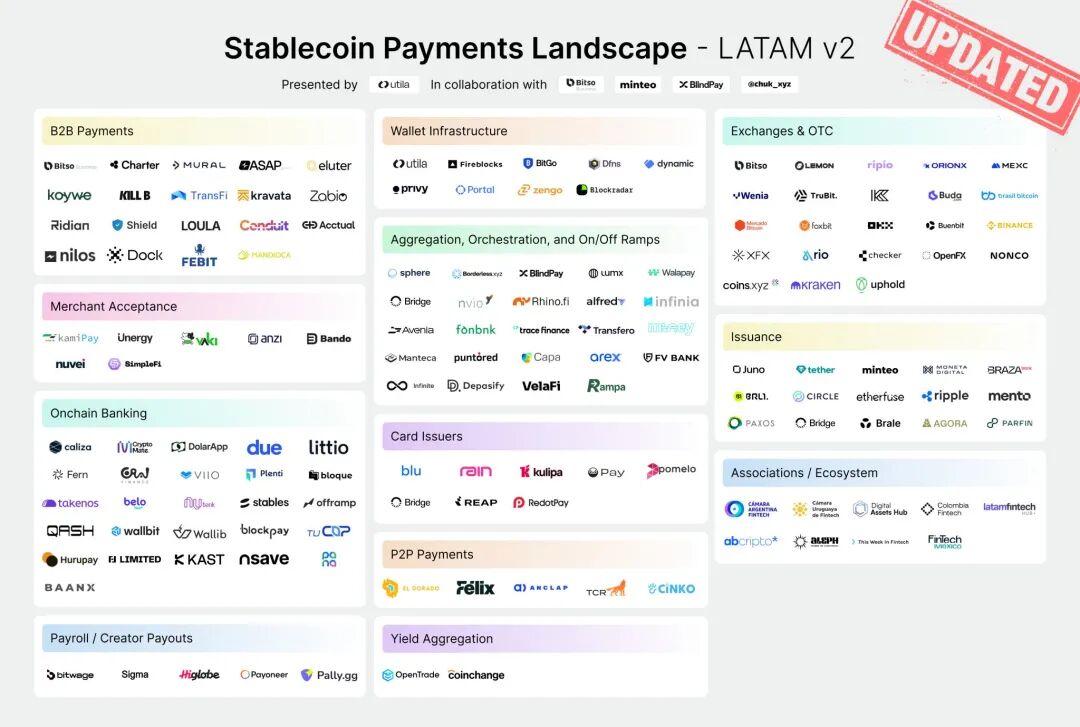

6. The Broader Crypto-Financial Ecosystem Beyond On-Chain Reports

This report focuses on projects with verifiable on-chain data available on Dune, but the breadth of Latin America’s crypto ecosystem extends far beyond current coverage. Numerous mature and innovative platforms operate actively in the region, which we cannot yet track with verifiable on-chain metrics.

Below is Chuk Okpalugo’s overview of the Latin American crypto-financial ecosystem; we’ll continue exploring this map in follow-up pieces.

Abroad – Open-source payment infrastructure connecting USDC with real-time fiat networks, supporting local systems like Pix (Brazil), PSE (Colombia), enabling low-cost cross-border and instant offline payments. Recently partnering with wallets like Beans and Decaf, focusing on compliance and the Latin American market.

Amero – Fintech connecting Latin America’s traditional payment rails with digital asset ecosystems, supporting 100+ payment methods and 350k cash locations, integrating Circle’s programmable wallet (Ethereum / Avalanche / Polygon), soon launching reloadable USDC prepaid Master/Visa cards in Mexico, and partnering with MoneyGram for remittances and self-service cash pickup—targeting the unbanked, merchants, and freelancers.

Argiefy – Argentine fintech app helping users save money and make better financial decisions amid inflation; offers currency conversion, coupons, community-shared discounts, and integrates crypto-fiat exchange via partners like zkp2p.

Bando – On-chain spending protocol enabling direct use of cryptocurrencies/stablecoins to buy real goods and services without fiat conversion. Covers 100+ countries, 6,000+ merchants (Amazon, Uber, Airbnb, etc.), supports mobile top-ups, bill payments, digital goods, and integrates with wallets like MiniPay, Binance Wallet, Base App.

Buenbit – Cross-regional platform originating in Argentina, offering 40+ coin trading, daily yield savings, crypto-backed loans, and international Mastercard payments in Mexico, Peru, etc.; supports Ethereum, Polygon, over 700k users.

Coinsenda – Wallet + exchange, supports 18 digital assets convertible to local currencies, active USDT OTC desk; 2,900+ monthly active users, $546k monthly volume, 90% on TRON, mainly used for payroll and remittances.

El Dorado – P2P stablecoin marketplace connecting a network of 10k merchants, 180k monthly active users, $18M monthly transfer volume, 60% on TRON, covering Brazil, Colombia, Argentina, Peru, Bolivia.

KAST – Stablecoin payment platform supporting global credit card spending; 500k total users, ~$5B cumulative volume, 55% on TRON, Brazil’s monthly spending up 112% QoQ in H1 2025.

Kripton – Since 2019, applying Bitcoin’s decentralized philosophy to commercial payments; in April 2025, designated USDT (TRON) as official digital dollar, 70% TRON usage, serving retail, merchants, and payment platforms.

Muney App – Based on Polygon, provides plug-and-play infrastructure connecting digital dollars with local cash networks, enabling cash deposits/withdrawals, P2P transfers, compliant off-ramps, focusing on multi-country remittance corridors to Venezuela.

Mural Pay – Stablecoin payment API designed for B2B, offering global receivables/payables, invoicing, virtual accounts, and compliance tools, integrated into 40+ markets, recently partnering with Taxbit to expand stablecoin invoicing and cross-border payments across Europe, U.S., and Latin America.

Orionx – Chilean exchange and infrastructure provider, offering 20+ coin trading in Chile, Peru, Colombia, Mexico, minimum purchase 10,000 CLP; in June 2025 secured Series A investment from Tether to expand stablecoin remittance, payment processing, treasury, and on/off ramp infrastructure.

Sphere – “Operating system” for digital economies, focused on inclusive finance, operating in Latin America and the U.S., 45% on TRON, platform total volume up 68% QoQ.

Swapido – Non-custodial platform based on Lightning Network, enabling second-level BTC→Mexican peso conversion and transfer to any local bank account, planning to add stablecoin support in 2025.

Takenos – Argentine digital wallet + Web3 neo-bank, targeting freelancers, gamers, influencers with cross-border income, supporting USD/EUR receipts, crypto or cash withdrawals, debit cards, global transfers.

Ugly Cash – Stablecoin financial services app offering high-yield accounts, free instant cross-border transfers to 60+ countries, 1% cashback Visa card, supporting virtual accounts in USD, EUR, MXN.

Traditional Fintech “Crypto-ification”

Latin American native “super apps” like Nubank, Mercado Pago, PicPay, RappiPay have followed Revolut and PayPal, embedding crypto assets directly into banking stacks, serving hundreds of millions:

-

Mercado Pago launched **Meli Dólar** (2024), pegged 1:1 to USD, and integrated e-commerce payment processing;

-

PicPay added BTC, ETH, USDP trading, plans to issue BRL stablecoin and integrate with Binance;

-

RappiPay launched crypto payments, layered with wallet, credit card, savings account;

-

Nubank offers BTC, ETH purchases and demand yield.

By embedding crypto capabilities into familiar, compliant apps, these giants provide low-friction, trustworthy digital asset access for millions in volatile economies.

7. Conclusion

As demonstrated by Dune’s report, Latin America’s crypto narrative is about “building a parallel financial infrastructure people actually use.” From Mexico to Argentina, on-chain adoption is driven not by concepts but by real needs: fighting inflation, sending remittances, settling supplier payments, paying salaries, daily shopping.

Over the past four years, the region has developed a multi-chain, stablecoin-centric parallel financial system deeply integrated with local payment rails like Pix/SPEI. It now performs most functions of traditional banking—often faster, cheaper, and more accessible.

Challenges remain: data gaps, inconsistent regulation, insufficient liquidity depth for local stablecoins. But the trajectory is clear: evolving from speculative trading into a multi-layered resilient ecosystem—crypto is no longer an “investment target,” but the “default way to save, transfer, and spend.”

If the past decade proved crypto’s feasibility, the next will amplify what’s already proven viable. The next chapter of Latin America’s on-chain economy will be written by builders, analysts, and communities together.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News