Stablecoin's Decade: From Wilderness to Empire, a War Without End

TechFlow Selected TechFlow Selected

Stablecoin's Decade: From Wilderness to Empire, a War Without End

This article analyzes the development of the stablecoin market, from early experiments to the current dominance of USDT and USDC, exploring the strengths and weaknesses of different stablecoin models and their role in global financial strategy.

Author: Luke, Mars Finance

Introduction: The New Battlefield—A War of Dollars and Code

Circle CEO Jeremy Allaire’s recent comments on USDC's competitive edge within emerging ecosystems such as the decentralized exchange Hyperliquid, along with his grand vision of exporting the "digital dollar" as a technological and geopolitical tool, offer a highly relevant entry point into understanding the stablecoin market. By defining stablecoins as “technological weapons” in competition against nations like China to reinforce the global dominance of the U.S. dollar, Allaire immediately elevates the discussion from mere crypto trading tools to the level of global financial strategy.

The current state of the stablecoin market—a multi-front battlefield with a total market cap exceeding $283 billion—is not something that emerged overnight. It is an epic shaped over a decade by brilliant innovation, arrogant failures, regulatory maneuvering, and ideological conflicts over the nature of money. This report will deconstruct that history, revealing the forces that built today’s giants and the ghosts of fallen empires. We will follow a chronological journey from the flawed genesis of early stablecoins, to Tether’s rise through opacity, to USDC’s compliance-driven challenge, Terra’s algorithmic apocalypse, BUSD’s regulatory takedown, PayPal’s push into mainstream adoption, and finally to new frontiers opened by decentralized and synthetic designs.

To provide readers with a clear framework, the table below outlines the core stablecoin models explored in depth throughout this report. This table will serve as a key reference for understanding the technological evolution and design philosophies that have defined the stablecoin landscape.

Overview of Core Stablecoin Model Comparisons

Chapter One: Genesis—Early Explorations and Failures in the Quest for Stability (2014–2017)

The birth of stablecoins stemmed from a fundamental problem: the extreme volatility of early cryptocurrencies like Bitcoin made them unreliable as mediums of exchange or stable units of account. For traders wishing to "park" funds during market turbulence without fully exiting to traditional finance, this volatility was unacceptable. It was precisely this demand that sparked the first generation of stablecoin experimentation.

The First Experiment: BitUSD (2014)

On July 21, 2014, the world’s first stablecoin, BitUSD, launched on the BitShares blockchain, marking the dawn of the stablecoin era. The project had intellectual pedigree from future industry titans, including Cardano founder Charles Hoskinson and EOS founder Dan Larimer.

BitUSD used a crypto-collateralized model, backed by BitShares’ native token BTS. Its stability relied on a “seigniorage arbitrage” mechanism—a system later nearly replicated and amplified by Terra/UST. In theory, when BTS prices fell, users could buy cheaper BTS with BitUSD, thereby supporting BTS’s price. However, this mechanism had a fatal flaw: while it included protocols to handle declines in collateral (BTS) value, it lacked effective mechanisms to counter drops in BitUSD’s own value or manage extreme volatility in BTS. The root cause of failure lay in the low liquidity and high volatility of the collateral itself. Ultimately, BitUSD broke its dollar peg in 2018 and never recovered.

The Second Attempt: NuBits (2014)

Also launched in 2014, NuBits attempted to improve upon BitUSD’s model by using a more mature and liquid cryptocurrency—Bitcoin—as collateral. Yet this did not solve the core issue. Despite having greater market depth than BTS, Bitcoin remained too volatile to reliably support a stablecoin. NuBits’ collapse was dramatic: in 2016, amid a Bitcoin bull run, many holders sold NuBits en masse to chase BTC gains, breaking the peg.

These early failures revealed a profound lesson that echoes through stablecoin history: unstable assets cannot support stable ones. Relying on a single, highly volatile crypto asset as collateral—even with sophisticated arbitrage mechanisms—is inherently fragile.

Yet the significance of this history goes deeper. The arbitrage mechanisms of BitUSD and NuBits were not merely failed experiments; they were the genetic ancestors of later algorithmic stablecoin models. The idea of maintaining a peg not through 1:1 real-world reserves but via economic incentives guiding market arbitrage was born here. BitUSD’s “seigniorage arbitrage” model was functionally identical to Terra/UST’s later “burn-and-mint equilibrium.” BitUSD failed due to “extreme volatility” in its collateral, directly foreshadowing the “death spiral” UST would experience when LUNA collapsed under massive selling pressure. Thus, Terra’s crash was not a “black swan” arising from a novel concept, but the inevitable outcome of a ten-year-old, known-fragile model amplified to catastrophic scale by unsustainable yields and market frenzy. The industry, it seems, failed to fully learn the lessons of 2014.

Chapter Two: Reign Supreme—Tether’s Controversy and Hegemony (2014–Present)

From the ashes of BitUSD, a project called Tether learned a lesson and chose a radically different path. It abandoned complex algorithms and volatile crypto collateral, proposing a simple, brute-force solution: for every USDT issued, one dollar would be held in a bank account. This model directly addressed the core problem of “unstable backing.”

Origins and Early Development

Tether began as “Realcoin,” founded in July 2014 by Brock Pierce, Reeve Collins, and Craig Sellars, built on the Mastercoin protocol (later renamed Omni) atop the Bitcoin network. In November 2014, the project rebranded as Tether. In January 2015, USDT debuted on the Bitfinex exchange—an association that would become central to its story and controversy. Tether Limited and Bitfinex are both owned by iFinex, a relationship that facilitated early growth but sowed seeds of conflict of interest.

Bull Market Engine and King of Global Liquidity

USDT’s explosive growth stemmed from its role as the critical “bridge” between fiat and crypto worlds. In the early days, many crypto exchanges lacked stable banking relationships, limiting fiat on/off ramps. USDT perfectly filled this gap, becoming the de facto “on-chain dollar,” providing essential liquidity to global crypto markets and underpinning the majority of trading volume. Its use cases quickly expanded beyond trading to cross-border remittances and value storage. In countries with unstable fiat currencies, USDT became an attractive alternative due to its lower fees and faster settlement compared to traditional banking systems.

Persistent Clouds: Reserve Concerns

Yet accompanying its hegemony were unending controversies, centering on the authenticity of its 1:1 dollar reserves. Although Tether consistently claimed full reserve backing, it never provided a complete, independently audited report from a top-tier accounting firm.

In 2021, the U.S. Commodity Futures Trading Commission (CFTC) fined Tether $41 million, finding that from 2016 to 2018, it held sufficient fiat reserves only 27.6% of the time—confirming long-standing market suspicions that its “100% backed” claims were often false. Since then, Tether’s reserve composition evolved from initially claimed pure cash to a mix including “cash equivalents,” commercial paper, and other assets, further increasing opacity. However, in recent years, Tether significantly shifted its reserve strategy, allocating heavily to U.S. Treasury bonds, making it one of the largest holders of Treasuries—a move that has enhanced asset quality and bolstered market confidence.

Resilience Amidst Controversy and Dominance

Despite being mired in controversy, USDT not only survived but became the undisputed market leader. By the end of 2024, its market cap approached $120 billion, serving over 350 million users, and grew further to over $159 billion by July 2025. It demonstrated remarkable resilience through multiple market crises, briefly depegging during the panic sell-off triggered by Terra’s collapse but quickly recovering stability.

Tether’s success was no accident—it reflected the “original sin” of the early crypto industry. Its dominance was not built on transparency and compliance, but paradoxically on regulatory ambiguity and operational opacity. In crypto’s wild west era, exchanges widely struggled with banking access, making fiat deposits and withdrawals difficult. USDT offered a perfect workaround: a digital dollar that could freely circulate among exchanges operating in regulatory gray zones, avoiding the friction of interfacing with traditional banks for every transaction. Its relatively lax KYC/AML requirements and registration in jurisdictions like the British Virgin Islands made it the path of least resistance for a global, often pseudonymous user base. Thus, Tether’s success can be seen as a direct product of the early crypto market’s semi-lawless nature. It thrived in a regulatory vacuum. Meanwhile, the rise of a regulation-embracing competitor like USDC represents the inevitable response as the industry matures and seeks legitimacy.

Chapter Three: The Challenger’s Grand Strategy—USDC and the Path of Compliance (2018–Present)

In 2018, the stablecoin market welcomed a radically different challenger. The Centre Consortium, co-founded by Circle (led by Jeremy Allaire) and Coinbase, launched USD Coin (USDC). From day one, USDC’s strategy stood in stark contrast to Tether’s: it embraced regulation, pursued transparency, and aimed to win institutional trust.

The “Compliant” Stablecoin

USDC’s core competitive advantage lies in its “compliance” label. Circle actively collaborated with regulators, securing money transmission licenses across U.S. states and implementing strict anti-money laundering (AML) and know-your-customer (KYC) protocols. In sharp contrast to Tether’s opacity, USDC committed to maximum transparency. It regularly publishes attestation reports from top accounting firms (initially Grant Thornton, later Deloitte), publicly verifying that its reserves consist of 100% cash and short-term U.S. Treasuries. This was not just a direct challenge to Tether’s model, but also paved the way for institutional investors seeking a safe, reliable on-chain dollar.

Growth Engine: DeFi and Institutional Adoption

If Tether is the lifeblood of centralized exchanges, USDC found its “product-market fit” in the booming decentralized finance (DeFi) sector. Due to its high transparency and credibility, USDC rapidly became the preferred collateral and trading pair on major DeFi protocols like Aave and Uniswap. This regulation-first strategy made it the go-to stablecoin for institutions, corporate treasuries, and fintech companies entering crypto, helping them effectively avoid the reputational risks associated with USDT.

Fire Test: Silicon Valley Bank (SVB) Collapse (March 2023)

USDC’s journey wasn’t smooth—the toughest test came in March 2023. When Silicon Valley Bank (SVB) collapsed, Circle disclosed that approximately $3.3 billion of its cash reserves were held at SVB, representing a significant portion of its total reserves. The news instantly triggered market panic, shattering USDC’s image as the “safest” stablecoin, causing its price to depeg and fall as low as ~$0.87.

This crisis served as an extreme stress test for USDC’s model. Market panic and mass redemption requests tested Circle’s liquidity management. Ultimately, the resolution depended on external intervention: the U.S. government announced deposit guarantees for all SVB customers, enabling Circle to fully recover its funds and swiftly restore USDC’s 1:1 peg to the dollar.

This depegging event seemed like a severe blow, but its outcome paradoxically reinforced the validity of USDC’s model. It revealed a profound truth: while deep integration with regulated traditional finance introduces new risks (like bank failures), it also means access to that system’s ultimate safety net. The risk originated in traditional finance (bank failure), and so did the solution (government guarantee). A purely crypto-native or offshore entity like Tether, if its Bahamian partner bank failed, would likely face permanent loss with no hope of similar government rescue.

This event forced the market to reassess risk. Which is worse: Tether’s risks—opaque reserves, offshore operations, unaudited status—or USDC’s risks—transparent reserves held in U.S. banks that might fail but are subject to government intervention? For institutional players, the answer was clear: the risks of a regulated U.S. banking system represent a known, manageable risk, far preferable to the unknown counterparty risk of an offshore, unregulated entity. Thus, rather than destroying USDC, this crisis ultimately validated, in the long run, Circle’s core strategic bet on regulatory integration from the very beginning.

Chapter Four: The Great Crash—Terra/UST’s Algorithmic Inferno (2022)

On the stablecoin map, Terra and its founder Do Kwon were once hailed as pioneers of “true decentralization,” promising a stablecoin free from fiat-backed constraints. Its core mechanism was the UST-LUNA “burn-and-mint equilibrium”: 1 UST could always be exchanged for $1 worth of LUNA, and vice versa. This design relied on arbitrage incentives to maintain UST’s dollar peg.

Growth Flywheel: The Temptation of Anchor Protocol

However, arbitrage alone was insufficient to drive mass adoption. Terra’s true catalyst was the Anchor Protocol, a lending platform offering near 20% annual percentage yield (APY) on UST deposits. This wildly unsustainable, above-market yield created massive artificial demand for UST.

The logic of its growth flywheel was as follows: users attracted by high yields bought LUNA, burned it to mint UST, then deposited UST into Anchor. This process reduced LUNA’s circulating supply, driving up its price. Rising LUNA prices enhanced perceived ecosystem value and stability, attracting more users. It was a classic positive feedback loop. At its peak, of the $18 billion UST supply, $16 billion was locked in Anchor, underscoring its pivotal role in the entire system.

Crash: Timeline of the Death Spiral (May 2022)

In May 2022, this seemingly perfect system collapsed. The trigger occurred between May 7 and 9, when large withdrawals from Anchor and the decentralized exchange Curve Finance caused UST’s price to drop below $1 for the first time.

Once depegged, the arbitrage mechanism reversed and rapidly turned into disaster. Arbitrageurs bought UST below $1, exchanged it for $1 worth of LUNA via the protocol, then immediately sold LUNA for profit. This process caused LUNA’s supply to explode at an alarming rate, creating immense downward pressure on its price. As LUNA’s value plummeted, exponentially more LUNA needed to be minted to redeem each UST, further fueling LUNA’s sell-off—this was the infamous “death spiral.”

To save the system, Terra’s nonprofit Luna Foundation Guard (LFG) deployed its multi-billion-dollar Bitcoin reserves to defend the peg, but this effort was futile against overwhelming market pressure and only intensified panic across the broader crypto market. Within a week, over $45 billion in market value evaporated from the Terra ecosystem.

Aftermath: Market Contagion and Regulatory Alarm

Terra’s collapse triggered a chain reaction across the crypto industry, leading to the bankruptcies of prominent entities like Celsius and Three Arrows Capital, dragging the entire market into a prolonged “crypto winter.” The event also brought algorithmic stablecoins under intense global regulatory scrutiny, tragically demonstrating their inherent fragility and potential systemic risks. The lesson of BitUSD in 2014 was forgotten—and this time, the cost was an industry-wide catastrophe.

At a deeper level, the Terra ecosystem was essentially a financial perpetual motion machine, destined to fail from the outset. The 20% yield offered by Anchor was not derived from any sustainable economic activity, but subsidized by Terra’s reserves and LUNA token inflation. The entire system was a closed loop, entirely dependent on continuous inflows of new capital and sustained LUNA price appreciation to pay existing depositors. Despite being automated via smart contracts, its function resembled a Ponzi scheme.

A stable system cannot sustainably pay 20% returns in a near-zero risk-free rate environment. That yield must come from somewhere. When Anchor’s lending income proved insufficient to cover interest payments, the shortfall was covered by Terra’s reserves. The system’s value rested on LUNA’s price, which depended on UST demand, which in turn was driven by Anchor’s high yields. It was a completely self-referential, inward-looping system requiring constant growth to survive. Once demand for UST wavered (as with the large withdrawals), the growth flywheel reversed, and the system’s internal logic forced its self-destruction. The “death spiral” was not a bug—it was the inevitable outcome of the core design under stress.

Chapter Five: Divergent Fates—The Hammer of Regulation and the Embrace of Traditional Finance (2023)

2023 was a watershed year for the stablecoin market. Two landmark events—BUSD’s forced delisting and PYUSD’s high-profile launch—clearly outlined two divergent paths for stablecoins, heralding a new era.

Part One: The Fall of BUSD

Binance USD (BUSD) was a stablecoin issued by Paxos, a New York-regulated trust company, but branded and primarily used by Binance, the world’s largest crypto exchange. This partnership enabled its rapid rise to become the third-largest stablecoin.

However, in February 2023, the regulatory hammer fell. The New York Department of Financial Services (NYDFS) ordered Paxos to cease issuing new BUSD. Regulators cited Paxos’ failure to conduct adequate due diligence on its partner Binance, which was found to have systemic AML compliance failures and processed substantial illicit transactions. Paxos was subsequently fined $26.5 million. This regulatory action effectively sentenced BUSD to death.

Following the ban, Binance began phasing out BUSD support and encouraged users to migrate to alternatives like the newly launched FDUSD, causing BUSD’s market cap to rapidly shrink.

Part Two: The Rise of PYUSD

In stark contrast to BUSD’s quiet exit, payment giant PayPal launched its stablecoin, PayPal USD (PYUSD), in August 2023, with Paxos again as the issuer. This event was historic: a mainstream, publicly traded, strictly regulated U.S. fintech powerhouse officially entered the stablecoin arena. It marked the beginning of a new phase where stablecoins, driven by traditional finance (TradFi) and fintech, aim for mass mainstream adoption.

PayPal’s strategy was clear and powerful: leverage its vast user base (over 426 million active accounts) and merchant network to promote PYUSD in everyday payments, cross-border remittances, and in-app scenarios, aiming to bypass traditional card networks to reduce costs and increase efficiency.

The contrasting fates of BUSD and PYUSD in the same year profoundly illustrate the “great divergence” in the stablecoin market. BUSD’s model relied on distribution through a massive global crypto exchange operating in regulatory gray areas. Regulators (NYDFS) proved they could kill such models by targeting their U.S.-based, regulated issuers, regardless of the exchange’s size. PYUSD’s model, conversely, relies on distribution through a massive, strictly regulated global payment company.

This shift indicates that future stablecoin success will depend less on crypto-native network effects and more on the ability to access mainstream distribution channels within regulatory frameworks. Power is shifting from offshore crypto exchanges to onshore, regulated financial institutions. This is precisely the future Jeremy Allaire and Circle have long bet on.

Chapter Six: Innovation Frontier—Decentralized and Synthetic Alternatives

While fiat-collateralized stablecoins dominate, another parallel innovation track continues exploring alternatives to eliminate reliance on centralization. From early decentralized stablecoins to the latest synthetic dollars, this front remains fiercely competitive, embodying deep considerations of risk, efficiency, and the spirit of decentralization.

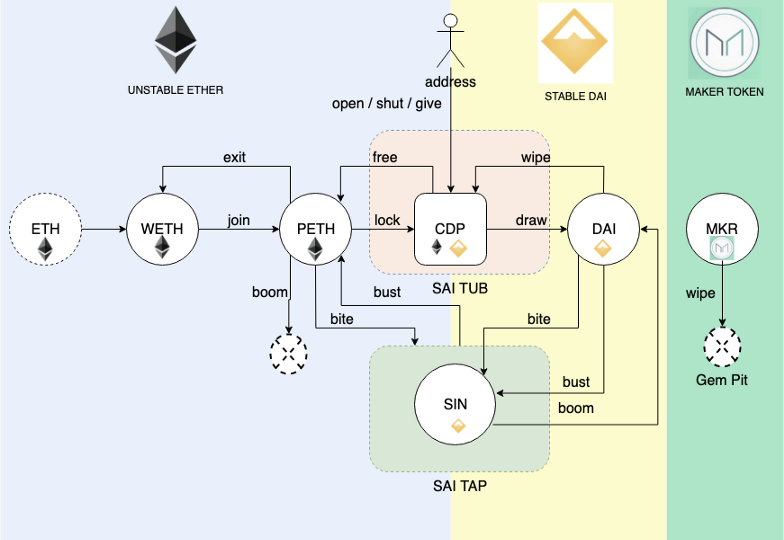

The Resilient Decentralized Option: MakerDAO (DAI)

Launched in 2017, DAI is the oldest and most successful decentralized stablecoin. It uses an over-collateralized crypto model: users lock volatile crypto assets like Ethereum (ETH) in smart contracts (“vaults” or CDPs) to borrow DAI. To buffer against collateral price drops, the collateral value must significantly exceed the borrowed DAI (e.g., collateral ratios typically above 150%).

DAI is governed by a decentralized autonomous organization (MakerDAO), where MKR token holders vote on risk parameters such as stability fees and eligible collateral types. DAI has also evolved significantly: from accepting only ETH as collateral to supporting multiple crypto assets. More controversially, to enhance stability and scale, MakerDAO later began accepting centralized stablecoins (like USDC) and real-world assets (RWA) as collateral. While this increased DAI’s robustness, it sparked intense community debate over whether it compromised its decentralization ideals.

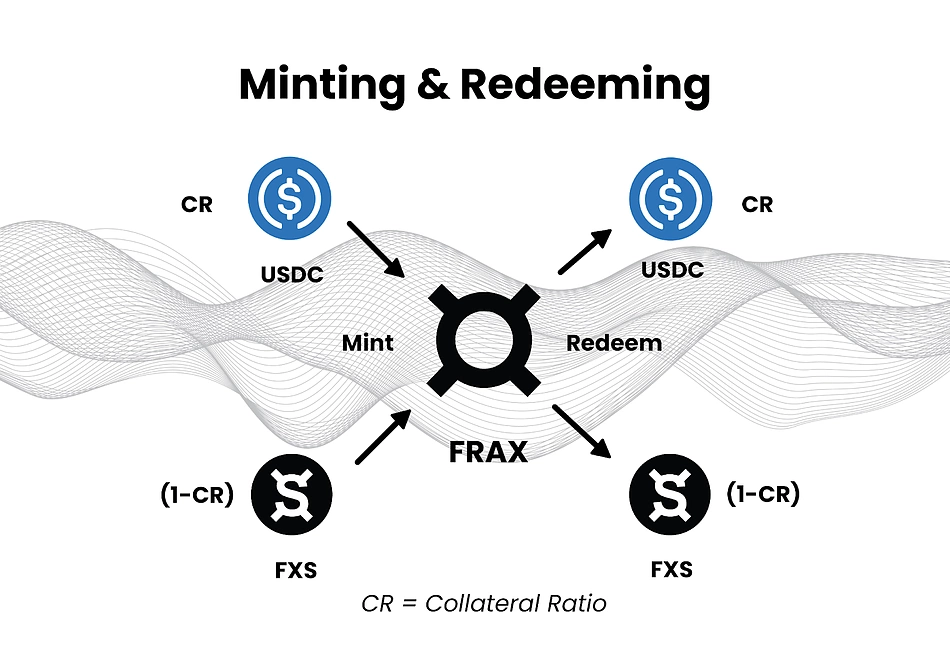

The Hybrid Experiment: Frax Finance (FRAX)

As the first “partially algorithmic” stablecoin, Frax attempts to balance capital efficiency and security. FRAX’s peg mechanism is a unique hybrid: partially backed by real collateral (like USDC), partially stabilized algorithmically via its governance token, Frax Shares (FXS).

Its core is a dynamic collateral ratio (CR). When market confidence in FRAX strengthens, the protocol lowers the CR, leaning more algorithmic to boost capital efficiency. When users mint FRAX, the algorithmic portion requires burning FXS tokens of equivalent value. Though Frax’s model is more complex and resilient than pure algorithmic stablecoins, avoiding Terra’s fate, its long-term stability under extreme market stress remains an open question.

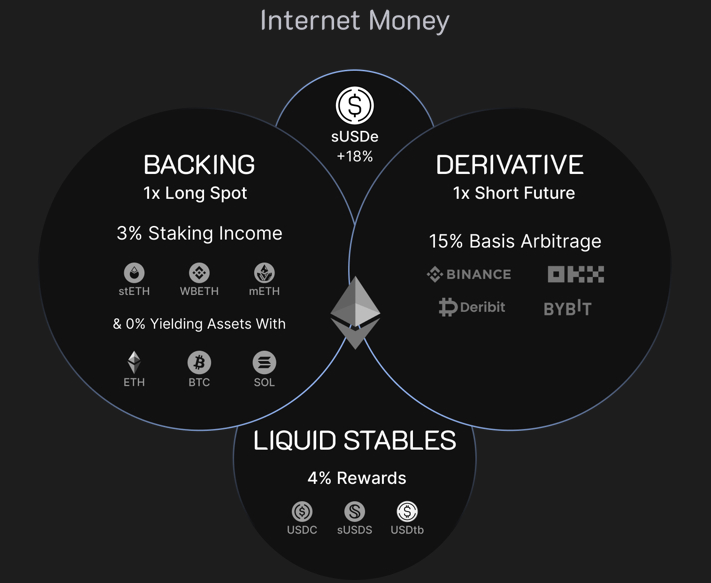

A New Paradigm: Ethena’s Synthetic Dollar (USDe)

Ethena’s USDe represents a more radical innovation—not a traditional stablecoin, but a “synthetic dollar.” USDe is not directly backed by dollars but aims to synthetically replicate dollar value on-chain through financial engineering.

Its core mechanism is a “delta-neutral” hedging strategy: for every dollar of collateral received (e.g., staked ETH like stETH), Ethena opens an equivalent short perpetual futures position on a derivatives exchange. This way, whether ETH rises or falls, gains or losses in the spot position are offset by opposite movements in the futures position, keeping the total portfolio’s dollar value stable.

USDe’s high yields primarily stem from funding rates in perpetual markets. In bull markets, strong long sentiment means longs typically pay funding fees to shorts. As a short holder, Ethena continuously collects these fees and distributes them as yield to users staking USDe.

From USDT to DAI, and onward to Frax and USDe, the evolution of stablecoin design is, in essence, a history of risk transfer and reshaping. Each new model does not simply eliminate risk, but transforms one type of risk into a new kind.

USDT/USDC eliminated BitUSD’s collateral volatility risk but introduced massive centralization and counterparty risk (Is Tether’s reserve real? Will SVB collapse?).

DAI, through on-chain collateral and decentralized governance, solved the centralization risk of USDT/USDC, but reintroduced collateral volatility risk (managed via over-collateralization), added smart contract and oracle risks, and suffered from extremely low capital efficiency.

Frax attempted to address DAI’s low capital efficiency with its partial-algorithmic model, but in doing so introduced reflexivity and algorithmic risk—milder versions of the risks that destroyed Terra.

Ethena (USDe), through delta-neutral hedging, simultaneously addresses DAI’s capital inefficiency and direct collateral volatility. However, it introduces a suite of new, potentially more systemic risks: funding rate risk (what if funding rates stay negative long-term?), exchange counterparty risk (what if derivative exchanges like Binance collapse?), and custody risk from its off-chain settlement partners. Risk does not disappear—it merely shifts from balance sheets to derivatives markets.

The Present State and Future of the Stablecoin War

Looking back over the past decade, stablecoins have evolved from fragile early experiments in 2014 into a multi-billion-dollar industry of profound geopolitical and economic significance. After a brutal selection process, the market has consolidated around fiat-collateralized models, with USDT and USDC capturing nearly 90% of market share, while the ghost of algorithmic stablecoins serves as a permanent warning.

Current Market Landscape

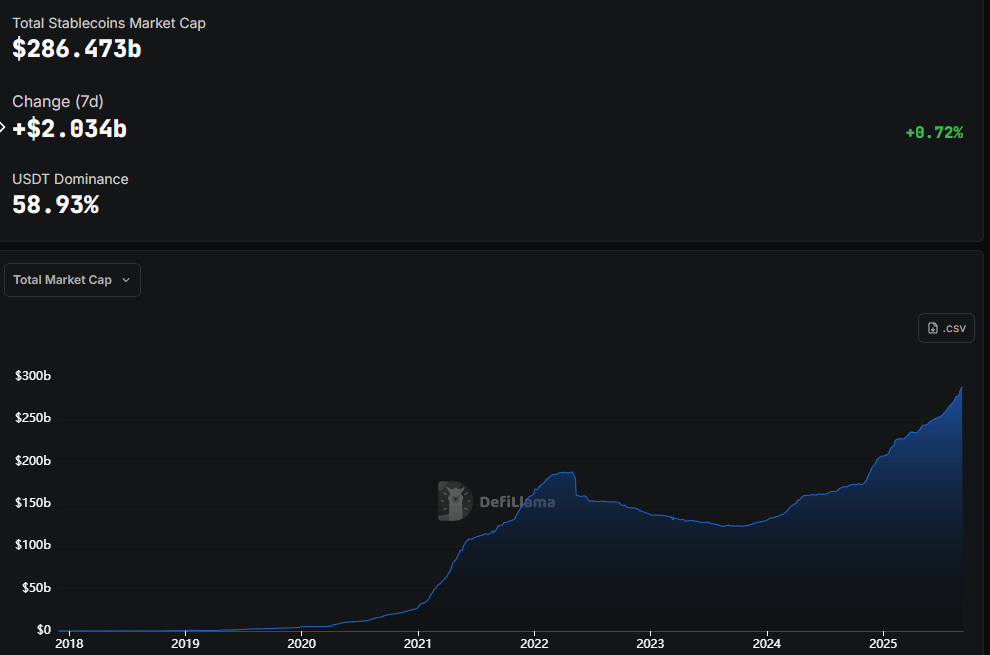

By the end of 2025, the total stablecoin market cap had surpassed $283 billion, a 128% increase since the beginning of the year. The chart below clearly illustrates the historical market share evolution of major stablecoins, vividly narrating this game of power.

The Future Battlegrounds

The first decade of the stablecoin war was about finding product-market fit within the crypto ecosystem. The next decade will be about breaking those boundaries and becoming the foundational rails of a new, internet-native global financial system. This war will unfold across several key fronts:

Regulatory Moats: With regulatory frameworks like the U.S. GENIUS Act and the EU’s MiCA coming into force, compliance is no longer optional but a prerequisite for any stablecoin aiming for mass adoption. This gives early movers like Circle and PayPal, who’ve already built compliance advantages, a significant head start.

The Trillion-Dollar Payments Market: Industry focus is shifting from crypto trading to real-world applications, especially cross-border payments and remittances. Here, stablecoins hold overwhelming advantages in speed and cost over traditional systems. This is precisely PayPal’s main thrust.

The Soul of DeFi: Despite the dominance of centralized stablecoins, the demand for a truly decentralized, censorship-resistant store of value remains a core ideal of the crypto world. The competition among models like DAI, Frax, and Ethena will determine who becomes the native currency of a decentralized internet.

The Blockchain Platform War: Competition exists not only between stablecoins but also among the Layer 1 and Layer 2 networks that host them. Currently, most stablecoins circulate on Ethereum and Tron, but with the rise of new public chains and Layer 2 solutions, the battle for the preferred settlement layer is intensifying.

The stablecoin saga is far from over. With traditional financial giants and sovereign nations now entering the arena, future competition will be fiercer than ever, with unprecedented stakes. The outcome of this war will not only decide which token becomes the reserve currency of the digital world, but may also reshape the global financial order for decades to come.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News