The Era of Hyper-Speculative Capitalism: Liquidity Becomes the Decisive Factor, Could BTC Peak in September?

TechFlow Selected TechFlow Selected

The Era of Hyper-Speculative Capitalism: Liquidity Becomes the Decisive Factor, Could BTC Peak in September?

A rebound may occur in September, followed by a potential liquidity-driven pullback.

Author: arndxt

Translation: AididiaoJP, Foresight News

Welcome to the era of hyper-speculative capitalism.

Pay close attention to M2 money supply in mid-September.

In today’s irrational economic environment, hyper-speculation has become a natural response.

Fiscal and monetary policies, once tools anchoring markets to some stable state, are now showing cracks:

-

The U.S. is running a 7% GDP deficit despite being at full employment.

-

Interest rates remain at 5%, yet Bitcoin approaches all-time highs.

-

Monetary policy has been overtaken by fiscal dominance, with stimulus continuing even during periods of economic "boom".

Markets no longer reflect fundamentals—they reflect liquidity.

Bitcoin's Frenzy: Is It Rational in a Chaotic World?

Bitcoin no longer needs a weak economy or rate cuts. In fact, the best macro backdrop may be one without new shocks, where liquidity conditions remain favorable.

Liquidity is surging:

-

Global M2 money supply remains high and may have already peaked.

-

If Bitcoin rises 10%, over $13 billion in short positions will be liquidated—indicating ample fuel remains for parabolic moves.

-

Bitcoin typically peaks 525–530 days after halving, suggesting late September 2025 could be pivotal.

@MintedMacro offers a clear roadmap based on historical halving cycles:

Liquidity-driven cycle: Bitcoin performs strongly when M2 grows. Currently, M2 shows a double-top formation, with the second peak lower than the first.

Peak timing predictions:

-

2013: 525 days post-halving

-

2017: 530 days post-halving

-

2021: 518 days post-halving

-

2025: around September 21

Expected peak range:

Bitcoin could reach $135,000–$150,000

However, upside potential may be constrained by macro tightening.

Key takeaway:

A rebound may occur in September, followed by a liquidity-driven pullback.

Amid distorted fundamentals and liquidity as the dominant force, market participants are adapting.

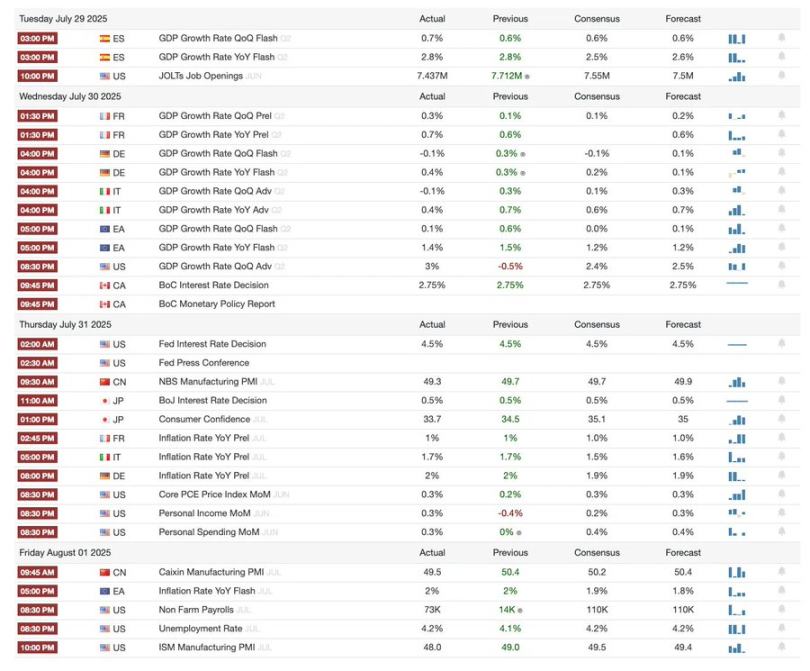

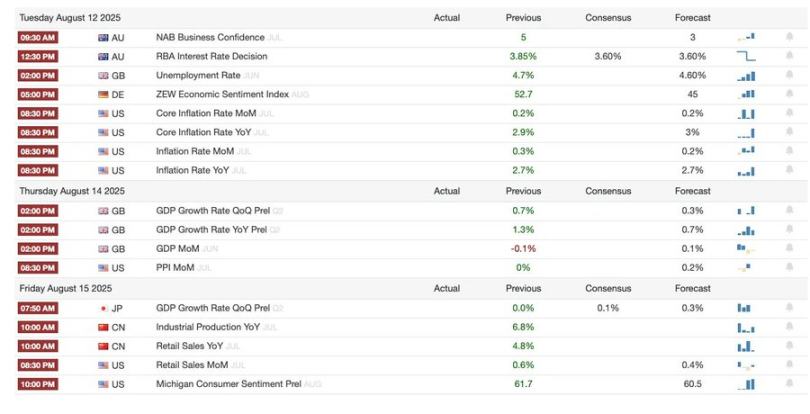

Macro analysis updated as of August 3, 2025, covering the following topics:

-

This week’s macro events

-

Bitcoin sentiment indicators

-

Market overview

-

Key economic indicators

-

India focus

This Week’s Macro Events Summary

Bitcoin Sentiment Indicators

Banking & Regulatory Developments:

-

The U.S. Securities and Exchange Commission (SEC) launched its "Crypto Initiative" to strengthen regulation and enhance U.S. leadership in digital finance.

-

PayPal rolled out "crypto payments," allowing U.S. businesses to accept 100 cryptocurrencies.

-

Visa expanded stablecoin settlement capabilities, adding supported tokens and blockchains.

-

BNB hit an all-time high, driven by institutional demand and corporate treasury inflows.

Institutional Investment & Project Developments:

-

Tron Inc. filed a $1 billion securities statement, becoming the largest holder of TRX.

-

Strategy Inc. acquired $739.8 million worth of Bitcoin, expanding holdings to $43 billion, and launched a preferred stock IPO.

-

Tether reported $4.9 billion in Q2 profits, fueled by strong demand for Bitcoin and gold.

-

SharpLink Gaming acquired $295 million in Ethereum, becoming the second-largest holder with 438,017 ETH.

-

Syntetika Hub launches: a learning, contribution, and rewards center within the ecosystem.

NFT & Digital Collectibles Market:

-

NFT sales surged to $574 million in July—the second-highest of 2025—driven by whale demand.

-

CryptoPunks floor price reached $208,000, a three-year high, boosted by Ethereum's rally.

Market Overview

U.S. Economy: Broader Signs of Slowdown

-

This week’s economic data sends a clear and consistent signal: U.S. growth momentum sharply decelerated in the first half of the year.

-

Consumer behavior is shifting. Despite healthier household balance sheets, tighter credit card usage reflects rising uncertainty rather than optimism.

-

Housing affordability hits a record low: even with modest home price declines, soaring mortgage rates and carrying costs (taxes, insurance, maintenance) have made ownership unattainable. The Atlanta Fed reports that owning a median-priced home now consumes 53% of middle-class income—the highest ever—highlighting structural barriers to homeownership.

Global Central Banks: Diverging Policy Paths

-

Policy divergence is emerging: central banks in Japan, Canada, Brazil, Colombia, and Singapore held rates steady, while Chile and South Africa cut by 25 basis due to slowing inflation and weak growth.

-

Eurozone Q2 GDP slightly exceeded expectations with 0.1% quarter-on-quarter growth, but core inflation remained sticky at 2.3% year-on-year, indicating the ECB will stay cautious.

-

China’s July PMI softened, signaling its recovery is fading faster than expected, potentially dragging regional demand and supply chains.

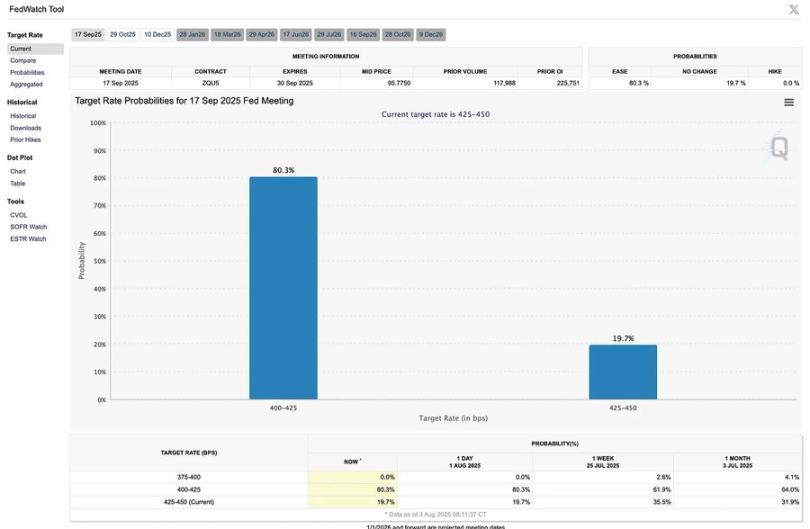

Federal Reserve: The Data-Dependence Dilemma

-

The Fed held rates at 4.25%–4.50% for a fifth consecutive meeting, reinforcing its cautious stance amid mixed signals.

-

A rate move at the September meeting remains possible—but not certain. Officials stressed the need for clearer evidence from labor, inflation, and consumer data before acting.

-

The outlook hinges on the depth of the slowdown and whether inflation continues easing without triggering recession.

Key Economic Indicators

U.S.-Japan Deal:

New tariff agreement: below threatened levels but still high

-

The U.S. announced 15% tariffs on all Japanese imports—up from 10%, and far above the 2.5% earlier this year.

-

Auto and parts tariffs previously at 27.5% are now unified at 15%, boosting Japanese automakers and equities.

Inflation risk from higher import prices

-

Though avoiding the extreme 25% rate, 15% tariffs will still push up consumer prices for Japanese goods, increasing inflationary pressure and eroding U.S. household purchasing power.

-

A broader shift in trade policy could further raise import costs from other regions.

Japan’s $550 billion investment pledge: terms unclear

-

Trump claimed Japan will invest $550 billion in the U.S., with 90% of profits going to America, calling it a "signing bonus."

-

Japanese negotiators said the figure is an upper limit, not a guaranteed amount, and expect shared risk and financing.

-

The lack of a written agreement raises doubts about enforceability, setting the stage for future disputes.

U.S. manufacturing push faces labor constraints

-

The deal aims to shift more manufacturing to the U.S., but how to fill jobs remains unclear amid labor shortages and tighter immigration policies.

-

This contradiction undermines the strategy of reducing trade deficits through reshoring.

Auto sector rebound: unfair competition

U.S. automakers face higher costs than Japanese importers due to:

-

25% tariffs on imported parts.

-

50% tariffs on imported steel and aluminum.

-

Complex refund processes under NAFTA/USMCA.

Industry leaders warn the deal favors Japan over U.S. manufacturers and workers, fearing it sets a precedent for future trade deals.

Agreement in doubt: negotiation vs. contract signing

-

No formal treaty was signed; both sides already differ on interpretation.

-

Raises broad concerns about U.S. reliance on non-binding trade commitments, potentially undermining trust and stability in future negotiations.

Labor Market:

New graduates face unprecedented hiring slump

-

Unemployment among recent college graduates hit a ten-year high, just one percentage point below that of all young workers—an abnormally narrow gap.

-

Historically, college grads enjoyed much better job prospects. This convergence is a warning sign for white-collar employment trends.

AI isn’t the main culprit—at least not yet

-

Though generative AI is blamed for eliminating entry-level roles, its impact remains confined to specific sectors like tech.

-

Broad-based effects are insufficient to explain the widespread weakness in graduate hiring.

Policy uncertainty cools the market

-

Uncertainty around trade policy, Fed rate direction, and immigration restrictions may be deterring hiring, especially for technical roles.

-

This uncertainty also affects employee behavior: low quit rates reflect hesitation to switch jobs in volatile markets.

-

Fewer quits = fewer vacancies = slower labor market churn.

Relief in skilled labor shortage

-

The long-standing shortage of college graduates, a key driver of high wage premiums, is easing.

-

As more workers enter the technical labor pool, wage premiums are flattening or declining, potentially further dampening innovation in traditionally high-growth sectors.

India Focus

UK–India Trade Deal: A Major Non-U.S. Pivot

-

The UK and India reached a landmark trade agreement, cutting tariffs on over 90% of British exports to India.

-

The UK expects exports to India to grow 60% by 2040, benefiting from access to India’s rapidly expanding market.

Automotive sector big winner

-

India slashed auto import tariffs from 100% to 10%, a dramatic shift that could reshape the market.

-

But quotas limit total imports, constraining short-term commercial gains for UK automakers.

India gains more

While headlines emphasize UK export growth, India benefits more from its own tariff reductions:

-

Lower consumer prices

-

Increased domestic competition

-

Enhanced global competitiveness of Indian firms

These structural advantages could boost India’s long-term export capacity and productivity.

50% of Indian Exports to UK Now Duty-Free

About 50% of Indian exports previously facing 4%–16% tariffs will now enter the UK tax-free, aiding Indian textile, pharmaceutical, and food exporters.

Strategic Trade Restructuring

-

The deal reflects a global trend: as U.S. tariffs disrupt existing trade patterns, nations are diversifying partnerships.

-

India is actively pursuing trade liberalization with the EU, ASEAN, and even the U.S., positioning itself as a key player in the post-globalization reset.

Summary

The defining traits of the hyper-speculative capitalism era are liquidity-driven dynamics, fiscal dominance, and market detachment from traditional economic logic. Bitcoin’s frenzy, trade realignment, and labor market shifts are all symptoms of this new reality. Investors and policymakers must adapt—navigating challenges posed by liquidity swings and policy uncertainty.

A defining feature of today’s global economy is liquidity-driven market behavior. Traditional economic theory holds that asset prices should reflect intrinsic value or discounted future cash flows. Yet in the age of hyper-speculative capitalism, liquidity—i.e., the abundance of available funds—has become the primary driver of market prices.

Take Bitcoin: its price movements are highly correlated with global M2 money supply growth. When central banks inject massive liquidity via quantitative easing or other means, these funds often flow into high-risk, high-return assets like cryptocurrencies. This trend was especially evident in 2025, as Bitcoin continued rising despite the Fed maintaining high interest rates—underscoring that markets now prioritize liquidity over traditional economic indicators.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News