Augusta of the Crypto World: Why RWA Tokens Choose the "Elite Model"?

TechFlow Selected TechFlow Selected

Augusta of the Crypto World: Why RWA Tokens Choose the "Elite Model"?

The history of financial exclusion is often a story about maintaining privilege through exclusion.

Author: Prathik Desai

Translation: Block unicorn

In the 20th century, Augusta National Golf Club was widely criticized for its overt elitism. As the host of The Masters Tournament, the club has only 300 members, with an extremely strict membership process—prospective members cannot even apply directly. Membership must be obtained through invitation. Alternatively, someone must nominate you, after which you wait patiently.

Critics called it the ultimate "men's club," which was indeed true before 2012. Worse still, for decades the club banned African Americans from becoming members. Sports journalists questioned why golf’s most prestigious event was held at a venue that excluded 99.9% of humanity. Public perception was terrible: a small group of wealthy white men controlled access to an experience millions longed for.

The club prides itself on having some notable members, including four-time Masters champion Arnold Palmer, business magnates Warren Buffett and Bill Gates, and Dwight D. Eisenhower, the 34th President of the United States.

Clearly, this is not the most democratic way to run a club.

But why should Augusta National Golf Club strive to democratize access to a world-class golf course? Open access rarely builds premium brands. The club pursues excellence. With only 300 members and virtually no outside players, the course remains pristine year-round. Every detail is managed with extreme precision.

For example, it can afford the rigorous maintenance required to sustain the Augusta National brand legend—think hand-trimming fairways with scissors, coloring pine needles, and moving entire forests to achieve perfect television angles. Fewer stakeholders mean higher precision. When access is controlled, quality reaches perfection.

The same logic explains one of the most misunderstood trends in today’s crypto space: why real-world asset (RWA) tokens—the digital representations of everything from government bonds to real estate—are overwhelmingly held by a few wallets.

But here, exclusivity isn’t based on gender or race.

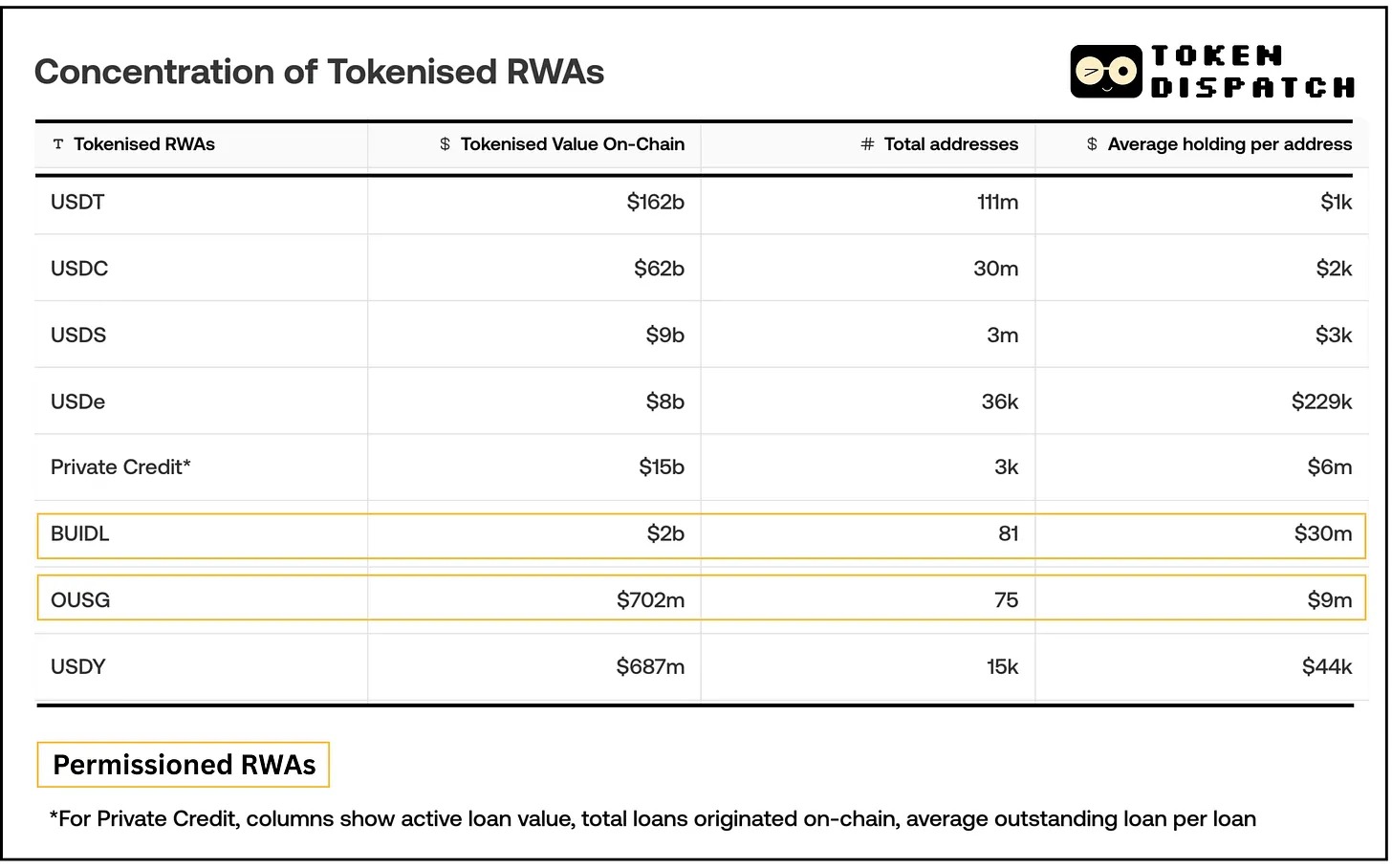

BlackRock’s tokenized money market fund BUIDL (BlackRock USD Institutional Digital Liquidity Fund) represents around $2.4 billion in assets, yet as of July 31, 2025, had only 81 holders.

Likewise, Ondo Finance’s U.S. Treasury bond fund OUSG (Ondo Short-Term U.S. Government Bond Fund) shows only 75 on-chain holders. In contrast, major stablecoins like USDT/USDC are held across millions of addresses (approximately 175 million stablecoin holders across networks).

At first glance, these digitized dollar assets resemble everything blockchain was supposed to fix: centralization, gatekeeping, exclusivity. Since you can copy-paste wallet addresses, why can’t you buy these yield-generating tokens just like any other crypto asset?

The answer lies in the same operational logic that allows Augusta National Golf Club to maintain its exclusive control. These tokens are designed to be centralized.

Regulated Reality

The history of financial exclusivity is often a story about preserving privilege through exclusion. But in these cases, exclusivity serves a different purpose: maintaining system compliance, efficiency, and sustainability.

Most RWA tokens represent securities or funds that cannot be freely offered to the public without registration. Instead, issuers use private or limited offerings regulated by the U.S. Securities and Exchange Commission (SEC), such as Regulation D in the U.S. or Reg S offshore, restricting tokens to qualified or compliant investors.

BUIDL (BlackRock), offered via Securitize, is available only to Qualified Purchasers in the U.S. (a subset of accredited investors with a minimum investment of approximately $5 million).

Likewise, Ondo’s OUSG (tokenized Treasury bond fund) requires investors to be both accredited investors and qualified purchasers.

These are not arbitrary barriers. They are SEC-mandated requirements under Regulation D 506(c), determining who can legally own certain types of financial instruments.

The contrast becomes clearer when we examine tokens designed for different regulatory frameworks. Ondo’s USDY is targeted exclusively at non-U.S. investors (sold overseas under Reg S). By circumventing U.S. restrictions, it achieves broader distribution, allowing non-Americans who complete KYC to purchase USDY. USDY has 15,000 holders—not many, but far more than OUSG’s 75.

The same company, the same tokenized asset—just a different regulatory framework. The result is a 200-fold difference in distribution.

This is where the comparison between Augusta National Golf Club and RWAs becomes precise. To meet these goals, RWA token platforms embed compliance into the token code or surrounding infrastructure. Unlike freely tradable ERC-20 tokens, these tokens often have transfer restrictions built into the smart contract layer.

Most security tokens use a whitelist/blacklist model (via standards such as ERC-1404 or ERC-3643), where only pre-approved wallet addresses can receive or send tokens. If an address is not on the issuer’s whitelist, the token’s smart contract blocks any transfer to that address.

It’s like a guest list enforced by code. You can’t just show up at the door with a wallet address and demand entry. Someone must verify your identity, check your accredited investor status, and add you to the approved list. Only then will the smart contract allow you to receive the token.

Backed Finance offers two forms of its token—an unrestricted version and a wrapped “compliant” token. The wrapped token “only allows whitelisted addresses to interact with the token,” and Backed automatically adds users to the whitelist once they pass KYC.

The Efficiency Argument

From the outside, this system appears exclusive. From the inside, it appears efficient. Why? From the issuer’s perspective, given their business models and constraints, a centralized holder base is often a rational—even intentional—choice.

Each additional token holder represents potential compliance risk and added cost, both on-chain and off-chain. Despite these upfront compliance costs, the on-chain rail brings long-term operational efficiencies, especially in automated net asset value (NAV) updates, instant settlement compared to traditional markets’ T+2, and programmability (such as automatic interest distribution).

By implementing tokenization and deploying distributed ledger technology (DLT), asset managers can reduce operating costs by 23%, equivalent to 0.13% of assets under management (AUM), according to global fund network Calastone in its whitepaper.

It predicts tokenization could improve the average fund’s profit and loss statement by $3.1 million to $7.9 million, including $1.4 million to $4.2 million in revenue gains through more competitive total expense ratios (TER).

The entire asset management industry could save a total of $135.3 billion across UCITS, UK, and U.S. (40 Act) funds.

By limiting distribution to known and vetted participants, issuers can more easily ensure every holder meets requirements (accredited investor status, jurisdiction checks, etc.) and reduce the risk of tokens falling into the wrong hands.

The math also makes sense. By targeting a few large investors rather than many small ones, issuers can save on onboarding costs, investor relations, and ongoing compliance monitoring. For a $500 million fund, reaching capacity through five investors each contributing $100 million is more commercially viable than 50,000 investors each investing $10,000. The former is also much simpler to manage. While on-chain transfers settle automatically, the compliance layer involving KYC, accreditation, and whitelisting remains off-chain and scales linearly with the number of investors.

Many RWA token projects explicitly target institutional or corporate investors, not retail. Their value proposition typically revolves around providing crypto-native yield channels for fund managers, fintech platforms, or crypto funds with large cash balances.

When Franklin Templeton launched its tokenized money market fund, they did not intend to replace your bank checking account. They aimed to give CFOs of Fortune 500 companies a way to earn yield on idle corporate cash reserves.

The Stablecoin Exception

Meanwhile, the comparison with stablecoins isn't entirely fair, because stablecoins solve the regulatory challenge differently. USDC and USDT themselves are not securities; they are designed as digital representations of the dollar, not investment contracts. This classification is achieved through careful legal structuring and regulatory engagement, allowing them to circulate freely without investor restrictions.

But even stablecoins require massive infrastructure investment and regulatory clarity to achieve their current scale of distribution. Circle spent years building compliance systems, working with regulators, and establishing banking relationships. The "permissionless" experience users enjoy today is built on a highly permissioned foundation.

RWA tokens face a different challenge: they represent actual securities with real investment returns, and thus fall under securities law. Until there is a clearer regulatory framework for tokenized securities (which the recently passed GENIUS Act begins to address), issuers must operate within existing constraints.

Looking Ahead

The current centralization of RWA tokens is, after all, the closest on-chain representation of how traditional finance operates. Consider traditional private equity funds or bond issuances restricted to qualified institutional buyers—participants are typically limited to a small number of investors.

The difference lies in transparency. In traditional finance, you don’t know how many investors hold a particular fund or bond—this information is private. Only large holders are required to make regulatory disclosures. On-chain, every wallet address is visible, making centralization obvious.

Moreover, exclusivity is not a new trait of on-chain tokenized assets. It has always been this way. The value of RWA tokenization lies in making these funds easier to manage for issuers.

Figure’s Digital Asset Registry Technology (DART) reduced loan due diligence costs from $500 per loan to $15, while shortening settlement time from weeks to days. Goldman Sachs and Jefferies can now purchase loan pools as easily as trading tokens. Meanwhile, tokenized Treasuries like BUIDL suddenly become programmable—you can use these ordinary government bonds as collateral to trade Bitcoin derivatives on Deribit.

In the end, the noble goal of democratizing access can be achieved through regulatory frameworks. Exclusivity is temporary regulatory friction. Programmability is a permanent infrastructure upgrade that makes traditional assets more flexible and tradable.

Returning to Augusta National Golf Club, their controlled membership model makes the golf championship a synonym for perfection. A limited number of members means every detail can be precisely managed. Exclusivity creates the conditions for excellence—and paradoxically, also makes it more cost-effective. Providing the same level of precision and hospitality to a broader, more inclusive audience would multiply the cost exponentially.

A controlled holder base also conveniently ensures compliance, efficiency, and sustainability for fund issuers.

But on-chain barriers are gradually lowering. As regulatory frameworks evolve, wrapped products emerge, and infrastructure matures, more people will gain access to these yields. In some cases, this access may come through intermediaries and products designed for wider distribution (such as Backed Finance’s unrestricted version), rather than direct ownership of the underlying token.

The story is still in its early stages, but understanding why things look the way they do today is key to grasping the transformations ahead.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News