SEC decides to save itself by fencing off a patch overrun with wild grass

TechFlow Selected TechFlow Selected

SEC decides to save itself by fencing off a patch overrun with wild grass

SEC embraces RWA and DeFi.

Author: Zuoye

The Great Depression of 1929 led to the creation of the Securities Exchange Act of 1934 and the SEC (U.S. Securities and Exchange Commission), but—fortunately or unfortunately, depending on whether you're an e/acc accelerationist or a pro-regulation free-market advocate—the SEC has never since stopped financial innovation or crises.

In 1998, LTCM (Long-Term Capital Management) collapsed quantitatively over Russian bonds, nearly reenacting the 1929 crisis, yet this did not prevent the ATS (Alternative Trading Systems) rule from taking effect in 1999, allowing quant trading, hedging, and arbitrage to fully embrace information technology.

After the 2008 financial crisis, dark pool trading came under regulatory scrutiny, yet dark pools still exist. In 2025, after Gary Gensler's departure, the SEC resolved to embrace the future trend—everything will be on-chain, everything will be compliant.

-

On-chain: RWA is just the beginning. Future trading, asset allocation, and yield generation will all revolve around blockchain, just as we embraced computers;

-

Compliance: Airdrops, staking, IXO, and rewards will form a U.S.-style Super App (Reg Super-App), with all DeFi being re-Americanized.

The SEC’s Existential Crisis

The Great Depression created the SEC; cryptocurrency ends it.

SEC regulatory shift timeline: Gary Gensler departs → Crypto Task Force → Project Crypto

There are clear signs. The evolution of SEC regulatory actions can be divided into two phases: January, when Gary was forced out, and April onward, when current Chair Atkins took office, launching a new crypto policy marked by the formation of the Crypto Task Force, culminating in Project Crypto by the end of July—an all-out "surrender" to crypto.

To understand why Project Crypto emerged, one must examine the SEC’s regulatory dynamics between April and July. During this period, numerous moves were made: on one hand, lawsuits involving Ripple and Kraken needed to be settled gracefully; on the other, companies like Coinbase and Grayscale grew increasingly assertive, actively demanding that the SEC ease regulations.

The Ripple case especially became a landmark shift from "enforcement-first regulation" to "regulation-as-service." Kraken’s subsequent restart of its IPO process proved that the crypto concept had been fully accepted by U.S. regulators, while Robinhood began boldly advancing tokenized stocks.

The approval of physical BTC/ETH ETF staking and redemption was the most significant breakthrough, but many other tokens and forms remain subject to case-by-case review—for instance, Trump’s own Trump Group ETF is also waiting in line.

Daring to obstruct America’s crypto destiny? This is no ordinary SEC—it must strike hard!

Caption: SEC's 2025 Crypto Regulatory Paradigm Shift, Image Source: @zuoyeweb3

Trump thus chose an unconventional path, boosting the CFTC and pushing legislative initiatives like the Genius Act. The CFTC is already expanding its authority, and the White House crypto report effectively accepts existing DeFi in full.

The SEC has already transferred stablecoin regulation to banking regulators, and more digital asset oversight is shifting to the CFTC. Where the SEC goes from here has become an urgent real-world question.

The more powerful Clarity Act has yet to become law formally. If the SEC doesn’t act proactively, it risks being completely overtaken by the CFTC—especially as stablecoin issuance now directly touches the core of securities law. Before the Clarity Act becomes law, the SEC must use administrative practice to preemptively define its regulatory domain and establish de facto control.

But under the current framework, the SEC can do little. Topics such as approving more staking-based ETFs (e.g., SOL), arbitrary-token ETFs, tokenized stocks/securities, and crypto company listings and DATCO treasury approvals are met with SEC stalling tactics—repeated delays and suspensions.

By July 17, rumors had already surfaced about plans to merge the SEC with the CFTC. Right after the SEC launched Project Crypto, the CFTC followed closely with its Crypto Sprint initiative—details don’t matter.

The era of SEC and CFTC division will end in the crypto age. To maximize its institutional interests, the SEC’s only viable choice is to embrace the new era and abandon all dogmas of the old world.

"On-Chaining" the Real World

DeFi fully compliant; the offshore arbitrage era ends.

As previously noted, neither the Genius Act nor the Clarity Act includes specific DeFi regulation—the former focuses only on stablecoins, the latter is too broad. Now, the SEC’s Project Crypto provides detailed administrative rules, covering all aspects of DeFi through people, capital, and regulations.

No need to go overseas—bring people back to the U.S.

In short: anything offshore exchanges or foreign foundations could do can now be done domestically in the United States.

Whether stablecoins, IXOs, or tokenization (stocks, bonds), even if different agencies have jurisdiction, the SEC won’t casually sue for illegal securities offerings—as long as communication is maintained.

Second, the sentencing of the Tornado Cash founder is beyond SEC authority, but the SEC can ensure developer safety, making the U.S. the preferred location for builders and encouraging healthy, orderly competition.

DeFi with rules—bring capital back to the U.S.

In short: no more offshore shell games, no excessive obsession with decentralization levels.

All aspects of DeFi—including token issuance, on-chain activities (staking, lending, trading, investing), and reward distribution—will be compliant. Self-custody trading will be elevated to a “U.S. liberal value,” and various crypto staking ETFs will be fully liberalized.

Finally, end offshore regulatory arbitrage. Return to the U.S. for investment, development, and entrepreneurship—ensure crypto happens in America.

RWA regulated—on U.S. chains.

In short: on-chaining officially becomes the main theme.

Compared to DeFi, RWA has separate guidelines, categorized into stocks, bonds, equity, and physical assets. Windows are open for tokenized stocks and private market tokenization (Pre-IPO).

This will be a deeper transformation than computerization—from paper certificates to electronic trading, then to full on-chaining. Any asset that can be financialized will be tokenized, eliminating information asymmetry between the few and the many. Of course, this may take many years.

In the end, DeFi will become a new financial form, not just a supplement to TradFi, and ETH will become the new carrier of U.S. financial hegemony.

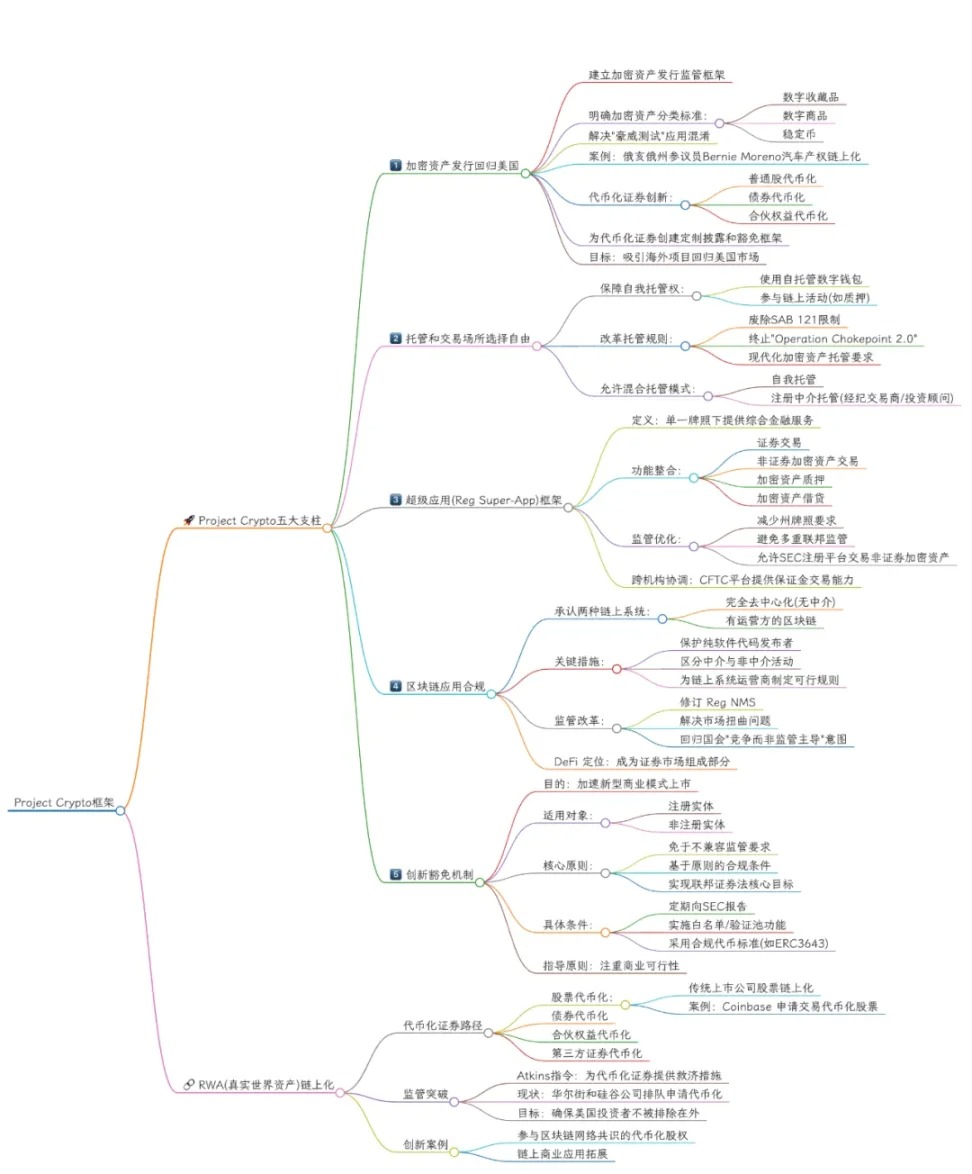

Caption: SEC Project Crypto Framework, Image Source: @zuoyeweb3

The title of this section borrows from the slogan of Rialo, an RWA L1 developed by Subzero Labs. This time, RWA will no longer be synthetic assets or virtual custodial issuance, but will directly enable any asset to go on-chain—for example, Figma, upon its recent listing, retained the option to issue tokenized stock.

Stocks will be tokenized stocks; assets will be tokenized assets.

Conclusion

A catalyst for financial bubbles, or an inevitable path to asset innovation?

From today onward, Project Crypto can be seen as DeFi’s “Securities Act moment.” But how much of its principles will actually be implemented—and how much will be accepted by Trump and Capitol Hill—remains up to fate.

Still, the CFTC and SEC will ultimately merge completely, because future digital commodities and digital securities will become indistinguishable.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News