Fed Decision Preview: How U.S. Interest Rates Impact the Stablecoin Industry?

TechFlow Selected TechFlow Selected

Fed Decision Preview: How U.S. Interest Rates Impact the Stablecoin Industry?

This article focuses on fiat-collateralized dollar stablecoins, adopting a global perspective to explore in depth how the Federal Reserve's interest rate cycle and other potential risks could reshape the industry landscape.

Author: 0xYYcn Yiran, Bitfox Research

The stablecoin market continues to grow rapidly in size and significance, driven by the rising popularity of cryptocurrencies and expanding mainstream use cases. By mid-2025, its total market capitalization had surpassed $250 billion, an increase of over 22% from the beginning of the year. According to Morgan Stanley, these dollar-pegged tokens now see daily trading volumes exceeding $100 billion and drove a staggering $27.6 trillion in on-chain transaction volume in 2024 alone. Nasdaq data indicates this transaction scale has already exceeded the combined totals of Visa and Mastercard. Yet beneath this apparent prosperity lies a series of hidden vulnerabilities—most critically, the business models of issuers and the stability of their tokens are tightly bound to fluctuations in U.S. interest rates. As the Federal Open Market Committee (FOMC) approaches its next policy decision, this report focuses on fiat-collateralized dollar stablecoins (such as USDT and USDC), adopting a global perspective to explore how Federal Reserve interest rate cycles and other potential risks may reshape the industry landscape.

Stablecoin 101: Growth Amid Hype and Regulation

Definition of Stablecoins:

Stablecoins are crypto assets designed to maintain a constant value, with each token typically pegged 1:1 to the U.S. dollar. This price stability is achieved through two primary mechanisms: full backing by reserve assets (such as cash and short-term securities) or algorithmic supply controls. Fiat-collateralized stablecoins like Tether (USDT) and Circle (USDC) issue each unit of their token fully backed by cash and short-term securities. This collateralization mechanism is central to their price stability. According to the Atlantic Council, approximately 99% of circulating stablecoins today are denominated in U.S. dollars.

Industry Significance and Current State:

In 2025, stablecoins are breaking out of the crypto niche and accelerating integration into mainstream finance and commerce. Payment giant Visa launched a platform enabling banks to issue stablecoins; Stripe integrated stablecoin payment functionality; Amazon and Walmart are reportedly exploring issuing their own stablecoins. At the same time, global regulatory frameworks are taking shape. In June 2025, the U.S. Senate passed the landmark "GENIUS Act" (Generative, Secure, and Transparent Payments Act), establishing the first federal-level stablecoin regulation. Key requirements include maintaining a stable 1:1 reserve ratio using high-quality liquid assets (cash or short-term Treasury bills maturing within three months) and clearly defining holder rights and protections. Across the Atlantic, Europe’s Markets in Crypto-Assets (MiCA) framework imposes stricter rules, empowering authorities to restrict non-euro stablecoins if they threaten monetary stability in the eurozone. On the market front, stablecoins show strong growth momentum: as of June 2025, their total circulating value exceeded $255 billion. Citigroup forecasts the market could surge to $1.6 trillion by 2030—a roughly sevenfold increase. This trajectory underscores that stablecoins are becoming mainstream, but rapid growth also brings new risks and friction.

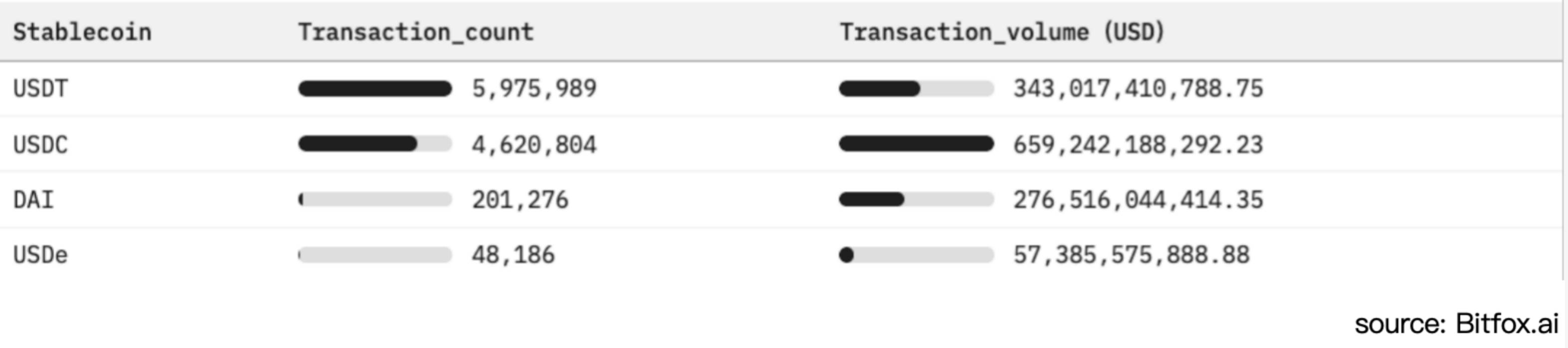

Figure 1: Ethereum Stablecoin Adoption Comparison and Market Activity Analysis (Past 30 Days)

Fiat-Supported Stablecoins and Interest Rate Sensitivity Model

Unlike traditional bank deposits that generate interest for customers, stablecoin holders typically earn no yield. Under the GENIUS Act, fiat-collateralized dollar stablecoin user balances are explicitly set at zero interest (0%). This regulatory setup allows issuers to retain all investment income generated from reserve funds. In the current high-interest-rate environment, this mechanism has turned companies like Tether and Circle—the issuer of USD Coin—into highly profitable entities. However, this model also exposes them to extreme vulnerability during interest rate downturns.

Reserve Investment Structure:

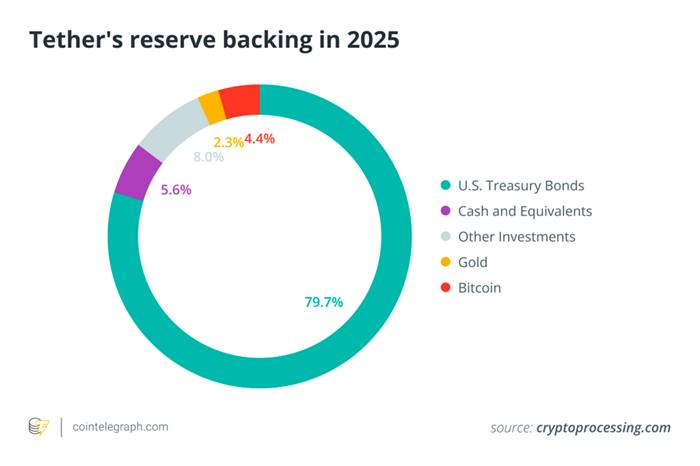

To ensure liquidity and maintain their dollar peg, major issuers allocate the bulk of their reserves into short-term U.S. Treasury bills and other short-dated financial instruments. As of early 2025, Tether held between $113 billion and $120 billion in U.S. government debt—approximately 80% of its total reserves—ranking it among the top 20 global holders of U.S. Treasuries. The chart below details Tether’s reserve composition, clearly showing heavy concentration in Treasuries and cash equivalents, while non-traditional assets such as other securities, gold, and Bitcoin represent only a small fraction of the portfolio.

Figure 2. Tether's Reserve Composition in 2025 (Dominantly U.S. Treasury Bills), Reflecting High Dependence of Fiat-Supported Stablecoins on Interest-Bearing Government Assets

High-quality reserve assets not only support the peg and bolster user confidence but also generate substantial interest income—the lifeline of the current stablecoin business model. Between 2022 and 2023, the Federal Reserve’s aggressive rate hikes pushed yields on Treasury bills and bank deposits to multi-year highs, significantly boosting returns on stablecoin reserves. For example, Circle’s disclosed financials show that of its $1.68 billion in total revenue in 2024, $1.67 billion (99%) came from interest earnings on reserve assets. Meanwhile, according to Techxplore, Tether reportedly earned $13 billion in profit in 2024—rivaling or surpassing profits of Wall Street powerhouses like Goldman Sachs. This level of profitability—achieved with a team of around 100 employees at Tether—highlights the powerful boost high interest rates provide to stablecoin issuers. In essence, stablecoin issuers operate a high-return "carry trade," deploying user funds into Treasury assets yielding over 5%, and capturing the entire spread due to users accepting a 0% rate. This creates significant exposure to interest rate volatility.

Exposure to Interest Rate Fluctuations

Stablecoin issuers’ revenue models are highly sensitive to changes in Federal Reserve rates. For instance, a single 50-basis-point rate cut (0.50%) could slash Tether’s annual interest income by approximately $600 million. As Nasdaq analysts have warned: “Overreliance on interest income will leave issuers like Circle vulnerable during rate-cutting cycles.”

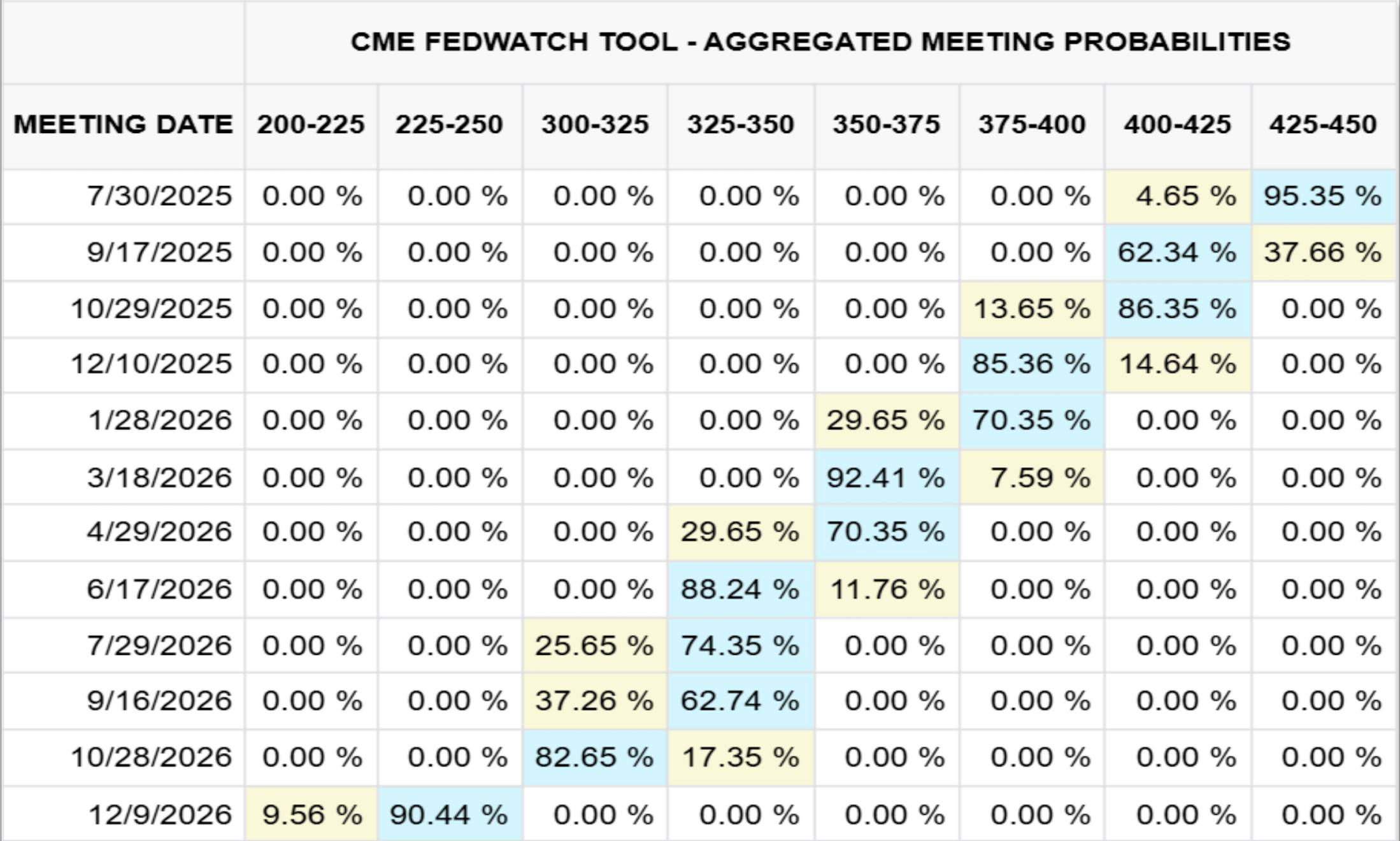

The following Figure 3 shows the federal funds rate curve projected by the CME (Chicago Mercantile Exchange) based on market expectations as of July 23, 2025, forecasting through the end of 2026. Figure 4 uses million-dollar-scale quantitative analysis to illustrate precisely how interest rate changes impact Circle’s reserve income.

Figure 3. Federal Funds Rate Outlook for December 2026 (CME, July 23, 2025)

Figure 4. Sensitivity of Circle’s Reserve Income to Interest Rate Changes

In 2024, Circle’s reserve interest income reached $1.67 billion, accounting for 99% of its total revenue ($1.68 billion). Based on CME data modeling (as of July 23, 2025), if the federal funds rate falls to the 2.25%–2.50% range by December 2026 (a ~90% probability), Circle is expected to lose approximately $882 million in interest income—more than half of its 2024 interest-related earnings. To offset this revenue gap, the company would need to double the circulating supply of its USDC stablecoin by the end of 2026.

Other Core Risks Beyond Interest Rates: Multiple Challenges Facing the Stablecoin System

While interest rate dynamics are central to the stablecoin industry, the ecosystem faces multiple other critical risks and challenges. Amid prevailing optimism, it is essential to systematically identify these risks to provide a clear, comprehensive assessment:

Regulatory and Legal Uncertainty

Stablecoin operations are currently constrained by fragmented regulatory regimes such as the U.S. GENIUS Act and the EU’s MiCA. While these frameworks grant legitimacy to certain issuers, they also impose high compliance costs and sudden market access restrictions. Regulatory actions targeting insufficient reserve transparency, sanctions evasion (e.g., Tether’s involvement in billions of dollars of transactions in sanctioned regions), or consumer harm can swiftly halt redemption functions or ban specific stablecoins from key markets.

Bank Partnerships and Liquidity Concentration Risk

Fiat-collateralized stablecoins rely heavily on a limited number of partner banks for reserve custody and fiat on/off-ramps. A sudden banking crisis (such as the collapse of Silicon Valley Bank, which froze $3.3 billion in USDC reserves) or a large-scale redemption wave can rapidly deplete bank deposits, trigger de-pegging, and—under wholesale redemption pressure that overwhelms a bank’s cash buffer—threaten broader banking system liquidity.

Peg Stability and De-Pegging Risk

Even when fully collateralized, stablecoins can—and have—experienced peg failures amid eroding market confidence. For example, in March 2023, concerns over reserve accessibility caused USDC to plunge to $0.88. Algorithmic stablecoins face even steeper stability curves, with TerraUSD’s (UST) 2022 collapse serving as a stark example.

Transparency and Counterparty Risk

Users depend on attestations—reserve proof reports issued by issuers, typically quarterly—to assess asset authenticity and liquidity. However, the lack of full public audits undermines credibility. Whether held in bank accounts, money market funds, or repo agreements, reserve assets carry counterparty and credit risk, which under stress conditions can materially impair redemption guarantees.

Operational and Technical Security Risks

Centralized stablecoins can freeze or confiscate tokens in response to attacks, introducing single points of governance failure. DeFi versions are vulnerable to smart contract bugs, cross-chain bridge exploits, and custodial hacks. Additionally, user errors, phishing attacks, and the irreversible nature of blockchain transactions pose ongoing security threats to holders.

Macro-Financial Stability Concerns

The concentration of hundreds of billions in stablecoin reserves within the short-term U.S. Treasury market means large-scale redemptions can directly affect Treasury demand and yield volatility. Extreme outflows could trigger fire sales in the bond market. Moreover, the widespread dollarization effect of stablecoins may weaken the transmission of Federal Reserve monetary policy, potentially accelerating the development of a U.S. central bank digital currency (CBDC) or prompting stricter regulatory safeguards.

Conclusion

As the next FOMC meeting approaches, although markets widely expect rates to remain unchanged, upcoming meeting minutes and forward guidance will become focal points. The remarkable growth of fiat-collateralized stablecoins like USDT and USDC masks their deeply entrenched business model dependence on U.S. interest rate movements. Looking ahead, even modest rate cuts (e.g., 25–50 basis points) could erode hundreds of millions—or billions—in interest income, forcing issuers to reassess growth strategies or share some yield with holders to sustain adoption.

Beyond interest rate sensitivity, stablecoins must navigate an evolving regulatory landscape, bank and liquidity concentration risks, challenges to peg integrity, and operational vulnerabilities ranging from smart contract flaws to inadequate reserve transparency. Crucially, as these tokens become systemically important holders of short-term U.S. Treasuries, their redemption behavior could disrupt global bond market pricing and impair the effectiveness of monetary policy transmission.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News