Artemis Research: Why Can ETH Become the Reserve Asset of the On-Chain Economy?

TechFlow Selected TechFlow Selected

Artemis Research: Why Can ETH Become the Reserve Asset of the On-Chain Economy?

From inflationary assets to scarce reserves, Ethereum is reshaping the foundation of digital finance.

Author: Kevin Li

Translation: TechFlow

Recently, interest in Ethereum has surged again, particularly following the emergence of ETH reserve holdings. Our fundamental analyst explores a valuation framework for ETH and constructs a compelling long-term bull case. As always, we welcome your engagement and exchange of ideas—but remember to do your own research (DYOR).

Let’s dive into ETH with our fundamentals analyst Kevin Li.

Key Takeaways

-

Ethereum (ETH) is transitioning from a misunderstood asset into a scarce, programmable reserve asset that secures and powers a rapidly institutionalizing on-chain ecosystem.

-

ETH's adaptive monetary policy projects declining inflation—peaking at approximately 1.52% even if 100% of ETH is staked, and falling to around 0.89% by year 100 (2125). This is far below the 6.36% average annual growth rate of U.S. M2 money supply (1998–2024), and comparable even to gold’s supply growth.

-

Institutional adoption is accelerating, with firms like JPMorgan and BlackRock building on Ethereum, driving sustained demand for ETH to secure and settle on-chain value.

-

The annual correlation between on-chain asset growth and native ETH staking exceeds 88%, highlighting strong economic alignment.

-

The U.S. Securities and Exchange Commission (SEC) issued a policy statement on staking on May 29, 2025, reducing regulatory uncertainty. Ethereum ETF filings now include staking provisions, boosting returns and enhancing institutional alignment.

-

ETH’s deep composability makes it a productive asset—usable for staking/re-staking, as DeFi collateral (e.g., Aave, Maker), AMM liquidity (e.g., Uniswap), and as native gas token on Layer 2s.

-

While Solana gained attention through memecoin activity, Ethereum’s superior decentralization and security position it to dominate high-value asset issuance—a larger, more durable market.

-

The rise of corporate ETH reserve strategies, starting with Sharplink Gaming ($SBET) in May 2025, has led public companies to hold over 730,000 ETH. This new demand trend mirrors the 2020 Bitcoin reserve wave and has contributed to ETH outperforming BTC recently.

Not long ago, Bitcoin was widely seen as a compliant store of value—the idea of it as “digital gold” once seemed fanciful to many. Today, Ethereum (ETH) faces a similar identity crisis. ETH is often misunderstood, has underperformed in annual returns, missed key meme cycles, and experienced slowing retail adoption across much of the crypto ecosystem.

A common critique is that ETH lacks a clear value accrual mechanism. Critics argue that the rise of Layer 2 solutions erodes base-layer fees, weakening ETH’s status as a monetary asset. When viewed solely through transaction fees, protocol revenues, or “real economic value,” ETH starts to resemble a cloud computing stock—more akin to Amazon than a sovereign digital currency.

In my view, this represents a category error. Evaluating ETH purely through cash flows or protocol fees conflates fundamentally different asset classes. Instead, it’s better understood through a commodity-like framework similar to Bitcoin. More precisely, ETH constitutes a unique asset class: a scarce yet productive, programmable reserve asset whose value accumulates through its role in securing, settling, and powering an increasingly institutionalized, composable on-chain economy.

Fiat Debasement: Why the World Needs Alternatives

To fully grasp ETH’s evolving monetary role, it must be viewed within the broader economic context—especially in an era of fiat debasement and monetary expansion. Driven by persistent government stimulus and spending, inflation rates are often understated. While official CPI data shows inflation hovering around 2% annually, this metric may be adjusted and could mask the true decline in purchasing power.

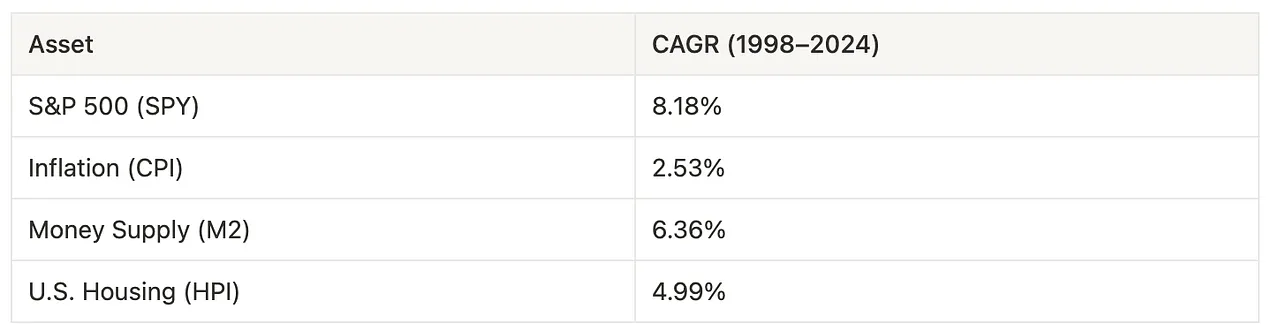

From 1998 to 2024, CPI inflation averaged 2.53% per year. In contrast, the U.S. M2 money supply grew at an average annual rate of 6.36%, outpacing both inflation and housing prices, and approaching the S&P 500’s 8.18% return. This suggests that nominal stock market growth may stem more from monetary expansion than productivity gains.

Figure 1: Returns of S&P 500, CPI, M2 Supply, and Housing Price Index (HPI)

Source: Federal Reserve Economic Data

Rapid money supply growth reflects governments’ increasing reliance on monetary stimulus and fiscal spending to manage economic instability. Recent legislation, such as Trump’s “Big Beautiful Bill” (BBB), introduced aggressive new spending measures widely expected to fuel inflation. Meanwhile, Elon Musk’s championed Department of Government Efficiency (DOGE) appears to have fallen short of expectations. These developments are fostering growing consensus that the current monetary system is inadequate, creating urgent demand for a more reliable store of value or form of money.

What Constitutes a Store of Value—and Where ETH Fits

A reliable store of value typically meets four criteria:

-

Durability—it must withstand the test of time without degradation.

-

Purchasing Power Preservation—it should maintain buying power across market cycles.

-

Liquidity—it must be easily tradable in active markets.

-

Adoption and Trust—it must enjoy broad trust or adoption.

Today, ETH excels in durability and liquidity. Its durability stems from Ethereum’s decentralized and secure network. Its liquidity is also high: ETH is the second most traded crypto asset, with deep markets on both centralized and decentralized exchanges.

However, when assessed purely through a traditional “store of value” lens, ETH’s ability to preserve value, along with its adoption and trust, remains contested. It is precisely here that the concept of a “scarce, programmable reserve asset” becomes more fitting, emphasizing ETH’s active mechanisms for value preservation and trust-building.

ETH’s Monetary Policy: Scarce Yet Adaptive

One of the most debated aspects of ETH’s role as a store of value is its monetary policy—specifically how it manages supply and inflation. Critics frequently point to Ethereum’s lack of a fixed supply cap. However, this criticism overlooks the architectural sophistication of Ethereum’s adaptive issuance model.

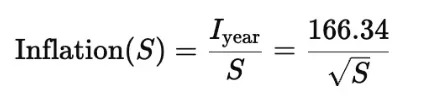

ETH issuance is dynamically tied to the amount of staked ETH. While issuance increases with higher staking participation, the relationship is sublinear: inflation rises slower than total staking growth. This is because issuance scales inversely with the square root of staked ETH, naturally moderating inflation.

Figure 2: Rough Formula for Inflation from Staking ETH

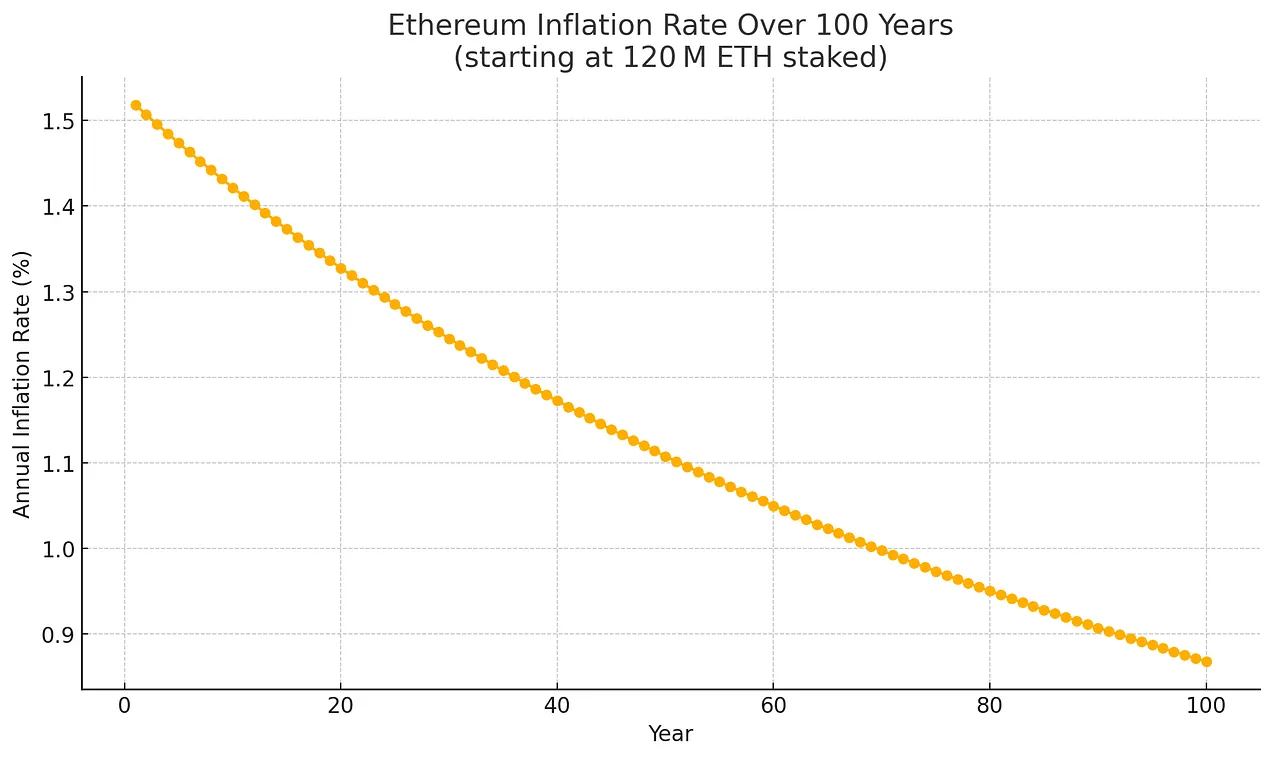

This mechanism introduces a soft inflation cap—ensuring inflation declines over time even as staking participation grows. In the worst-case simulated scenario (100% of ETH staked), annual inflation peaks at about 1.52%.

Figure 3: Illustrative Projection of Maximum ETH Issuance Assuming 100% Staking, Starting with 120 Million ETH Over 100 Years

Crucially, even this worst-case issuance rate declines as total ETH supply grows, following an exponential decay curve. Assuming 100% staking and no ETH burning, projected inflation trends are:

Year 1 (2025): ~1.52%

Year 20 (2045): ~1.33%

Year 50 (2075): ~1.13%

Year 100 (2125): ~0.89%

Figure 4: Illustrative Projection of Maximum ETH Issuance Assuming 100% Staking, Showing Decline as Total Supply Increases

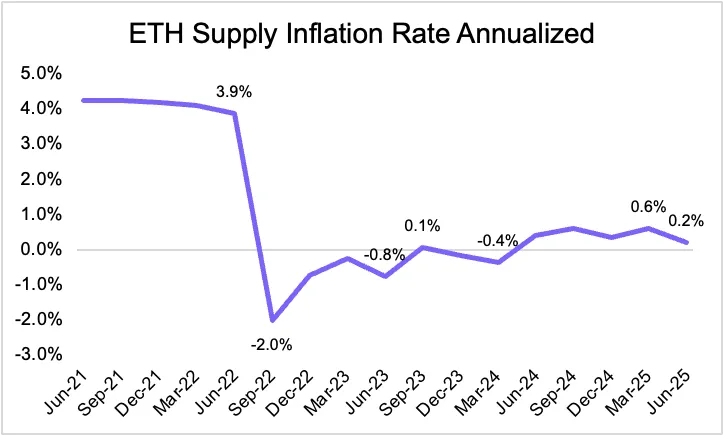

Even under these conservative assumptions, Ethereum’s declining inflation curve reflects inherent monetary discipline—enhancing its credibility as a long-term store of value. The picture improves further when considering Ethereum’s burn mechanism via EIP-1559, where a portion of transaction fees is permanently removed from circulation. Net inflation can thus fall well below gross issuance, sometimes turning deflationary. In practice, since Ethereum’s transition from proof-of-work to proof-of-stake, net inflation has consistently remained below gross issuance and has periodically turned negative.

Figure 5: Annualized ETH Supply Inflation Rate

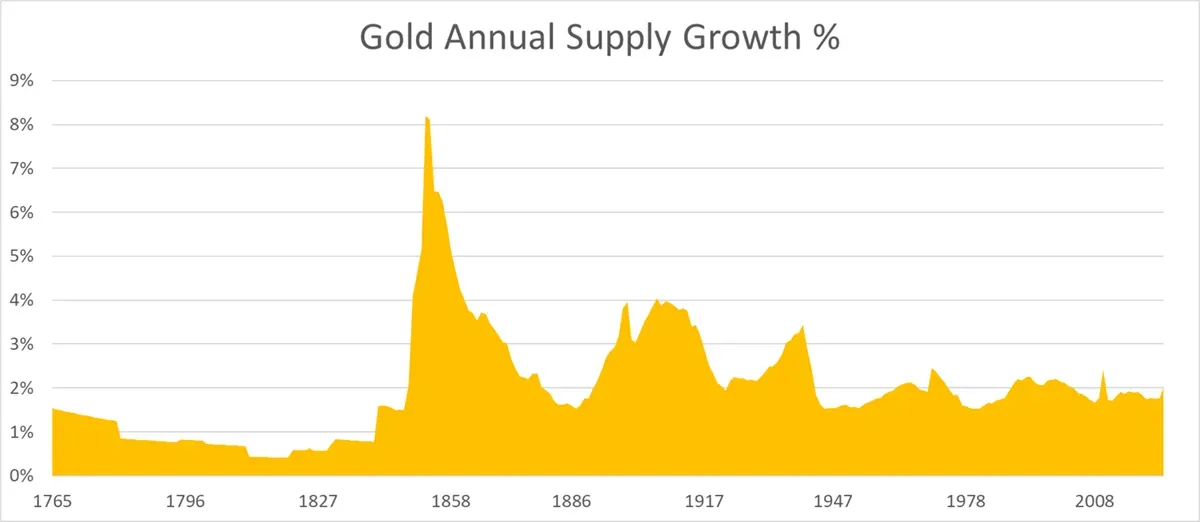

Compared to fiat currencies like the U.S. dollar—whose M2 money supply grows over 6% annually—Ethereum’s structural constraints (and potential deflation) enhance its appeal as a reserve asset. Notably, Ethereum’s maximum supply growth rate now rivals—and slightly undercuts—gold’s, further cementing its status as a sound monetary asset.

Figure 6: Annual Gold Supply Growth Rate

Source: ByteTree, World Gold Council, Bloomberg, Our World in Data

Institutional Adoption and Trust

While Ethereum’s monetary design effectively addresses supply dynamics, its real-world utility as a settlement layer is now the primary driver of adoption and institutional trust. Major financial institutions are building directly on Ethereum: Robinhood is developing a tokenized stock platform, JPMorgan is launching its deposit token (JPMD) on Ethereum’s Layer 2 (Base), and BlackRock is tokenizing a money market fund on Ethereum via BUIDL.

This on-chain shift is driven by a powerful value proposition that solves legacy inefficiencies and unlocks new opportunities:

-

Efficiency and Cost Reduction: Traditional finance relies on intermediaries, manual processes, and slow settlements. Blockchains streamline these via automation and smart contracts, lowering costs, reducing errors, and cutting processing times from days to seconds.

-

Liquidity and Fractional Ownership: Tokenization enables fractional ownership of illiquid assets like real estate or art, expanding investor access and unlocking trapped capital.

-

Transparency and Compliance: Blockchain’s immutable ledger ensures verifiable audit trails, simplifying compliance and reducing fraud through real-time visibility into transactions and ownership.

-

Innovation and Market Access: Composable on-chain assets enable new products—like automated lending or synthetic assets—creating new revenue streams and extending finance beyond traditional boundaries.

ETH Staking as Security and Economic Alignment

The on-chain migration of traditional financial assets highlights two major drivers of ETH demand. First, the growth of real-world assets (RWA) and stablecoins increases on-chain activity, raising demand for ETH as a gas token. More importantly, as Tom Lee observed, institutions may need to buy and stake ETH to secure the infrastructure they depend on, aligning their interests with Ethereum’s long-term security. In this context, stablecoins represent Ethereum’s “ChatGPT moment”—a breakthrough use case demonstrating the platform’s transformative potential and broad utility.

As more value settles on-chain, alignment between Ethereum’s security and its economic value becomes increasingly critical. Ethereum’s finality mechanism, Casper FFG, ensures blocks are finalized only when a supermajority (two-thirds or more) of staked ETH agrees. While an attacker controlling at least one-third of staked ETH cannot finalize malicious blocks, they can disrupt consensus and halt finality entirely. In such cases, Ethereum can still propose and process blocks, but without finality, transactions may be reversed or re-ordered—posing serious settlement risks for institutional use cases.

Even when operating on Layer 2s that rely on Ethereum for final settlement, institutional participants depend on the base layer’s security. Layer 2s do not diminish ETH; instead, they enhance its value by increasing demand for base-layer security and gas. They submit proofs, pay base fees, and typically use ETH as their native gas token. As rollups scale execution, Ethereum accumulates value through its foundational role in providing secure settlement.

In the long run, many institutions may move beyond passive staking via custodians and begin running their own validators. While third-party staking solutions offer convenience, operating validators gives institutions greater control, enhanced security, and direct participation in consensus. This is especially valuable for stablecoin and RWA issuers, enabling them to capture MEV, ensure reliable transaction inclusion, and leverage private execution—features crucial for operational reliability and transaction integrity.

Critically, broader institutional participation in validator operations helps address one of Ethereum’s current challenges: concentration of staked equity among a few large operators, such as liquid staking protocols and centralized exchanges. By diversifying the validator set, institutional involvement enhances Ethereum’s decentralization, strengthens its resilience, and boosts the network’s credibility as a global settlement layer.

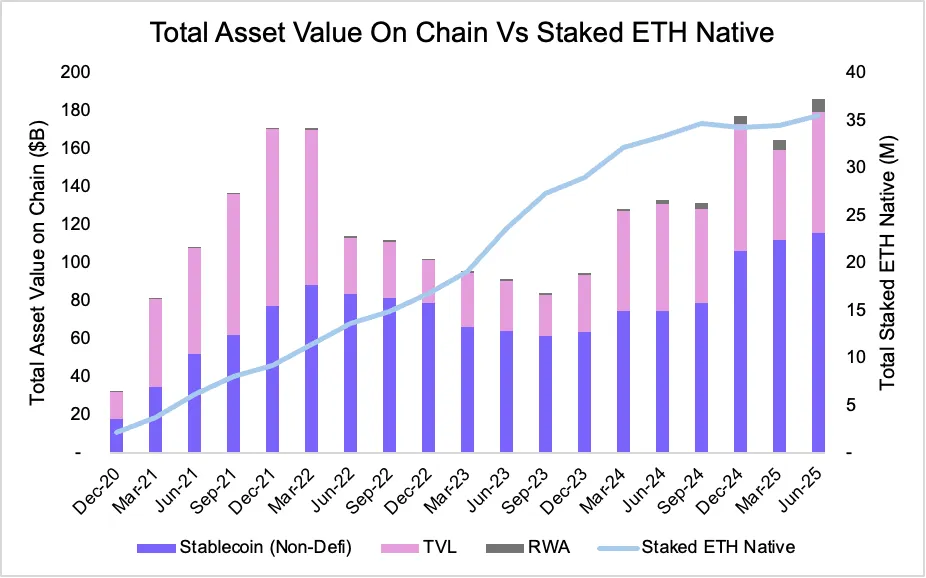

A notable trend from 2020 to 2025 reinforces this alignment of incentives: the growth of on-chain assets closely tracks the growth of staked ETH. As of June 2025, stablecoin supply on Ethereum reached a record $116.06 billion, while tokenized RWAs climbed to $6.89 billion. Meanwhile, staked ETH grew to 35.53 million ETH—a significant increase underscoring how network participants balance security with on-chain value.

Figure 7: Total On-Chain ETH Value vs. Value of Native Staked ETH

Source: Artemis

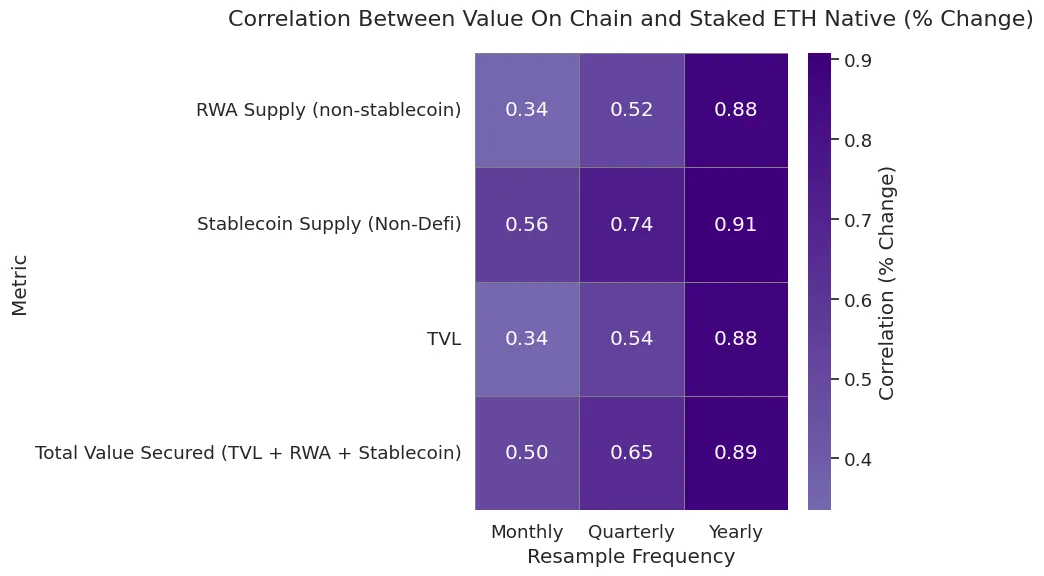

Quantitatively, the annual correlation between on-chain asset growth and native ETH staking has consistently exceeded 88% across major asset categories. Stablecoin supply, in particular, shows a strong link to staked ETH growth. While quarterly correlations fluctuate due to short-term volatility, the overall trend remains intact—as assets flow on-chain, the incentive to stake ETH strengthens.

Figure 8: Monthly, Quarterly, and Annual Native Correlations Between Staked ETH and On-Chain Value

Source: Artemis

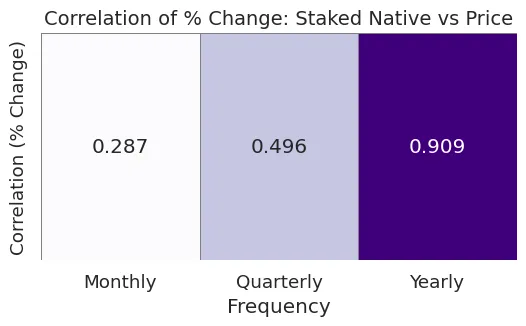

Moreover, rising staking levels influence ETH’s price dynamics. As more ETH is staked and removed from circulation, supply tightens—especially during periods of high on-chain demand. Our analysis shows an annual correlation of 90.9% between staked ETH and ETH price, and 49.6% quarterly—supporting the view that staking not only secures the network but also exerts favorable supply-demand pressure on ETH itself over time.

Figure 9: Native Correlation Between Staked ETH and Price

Source: Artemis

A recent policy clarification from the U.S. Securities and Exchange Commission (SEC) has eased regulatory uncertainty around Ethereum staking. On May 29, 2025, the SEC’s Division of Corporation Finance stated that certain protocol staking activities—limited to non-entrepreneurial roles such as self-staking, delegation, or custody under specific conditions—do not constitute securities offerings. While more complex arrangements remain subject to case-by-case analysis, this clarification encourages more active institutional participation. Following the announcement, Ethereum ETF filings began including staking clauses, allowing funds to earn rewards while contributing to network security. This not only improves returns but further solidifies institutional acceptance and trust in Ethereum’s long-term viability.

Composability and ETH as a Productive Asset

Another defining feature that sets ETH apart from pure stores of value like gold and Bitcoin is its composability—which inherently drives demand for ETH. Gold and BTC are non-productive assets, whereas ETH has native programmability. It plays an active role in the Ethereum ecosystem, supporting decentralized finance (DeFi), stablecoins, and Layer 2 networks.

Composability refers to the ability of protocols and assets to interoperate seamlessly. On Ethereum, this makes ETH not just a monetary asset, but a foundational building block for on-chain applications. As more protocols build around ETH, demand for it grows—not only as gas, but also as collateral, liquidity, and staking capital.

Today, ETH is used in several key ways:

-

Staking and Re-staking—ETH secures Ethereum itself and can be re-staked via EigenLayer to provide security for oracles, rollups, and middleware.

-

Collateral in Lending and Stablecoins—ETH backs major lending protocols like Aave and Maker and serves as the foundation for overcollateralized stablecoins.

-

Liquidity in AMMs—ETH pairs dominate decentralized exchanges like Uniswap and Curve, enabling efficient swaps across the ecosystem.

-

Cross-Chain Gas—ETH is the native gas token on most Layer 2s, including Optimism, Arbitrum, Base, zkSync, and Scroll.

-

Interoperability—ETH can be bridged, wrapped, and used on non-EVM chains like Solana and Cosmos (via Axelar), making it one of the most transferable on-chain assets.

This deep, integrated utility makes ETH a scarce yet highly efficient reserve asset. As ETH becomes embedded in the ecosystem, switching costs rise and network effects strengthen. In a sense, ETH may be more like gold than BTC. Much of gold’s value comes from industrial and jewelry applications, not just investment—whereas BTC lacks such functional utility.

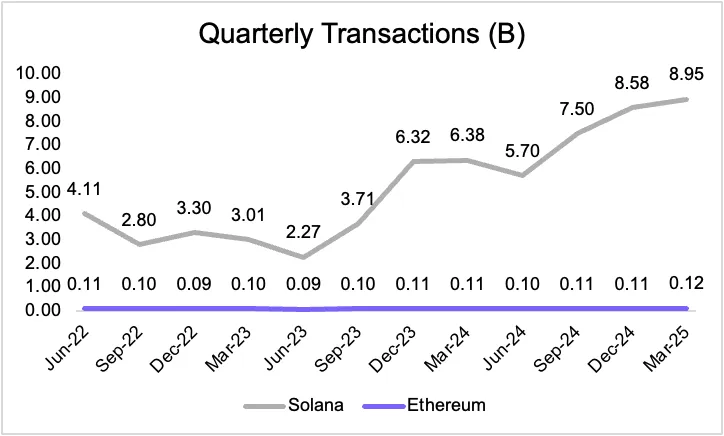

Ethereum vs. Solana: The Layer-1 Divide

In this cycle, Solana appears to be the biggest winner in the Layer 1 space. It has effectively captured the memecoin ecosystem, creating a vibrant network for new token launches and development. While this momentum is real, Solana remains less decentralized than Ethereum due to its limited number of validators and high hardware requirements.

That said, demand for Layer 1 blockspace may become stratified. In such a layered future, both Solana and Ethereum could thrive. Different assets require different trade-offs between speed, efficiency, and security. However, in the long run, Ethereum—with its stronger decentralization and security guarantees—is likely to capture a larger share of asset value, while Solana may dominate in transaction frequency.

Figure 10: SOL vs. ETH Quarterly Transaction Volume

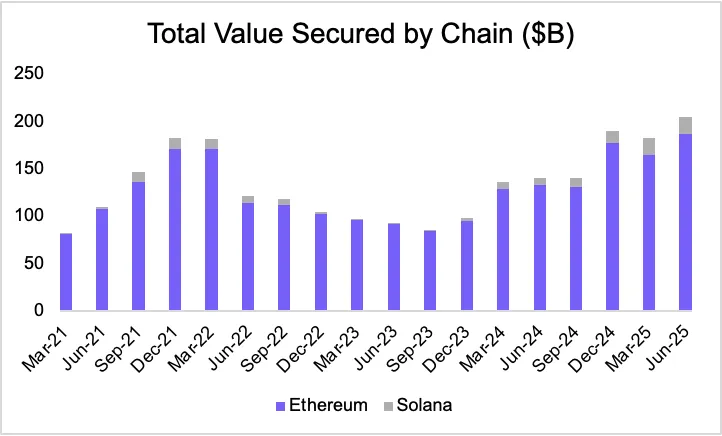

Yet in financial markets, the market size for assets prioritizing robust security far exceeds that for assets focused solely on execution speed. This dynamic favors Ethereum: as more high-value assets go on-chain, Ethereum’s role as the foundational settlement layer becomes increasingly valuable.

Figure 11: Total Value Secured On-Chain ($ billions)

Source: Artemis

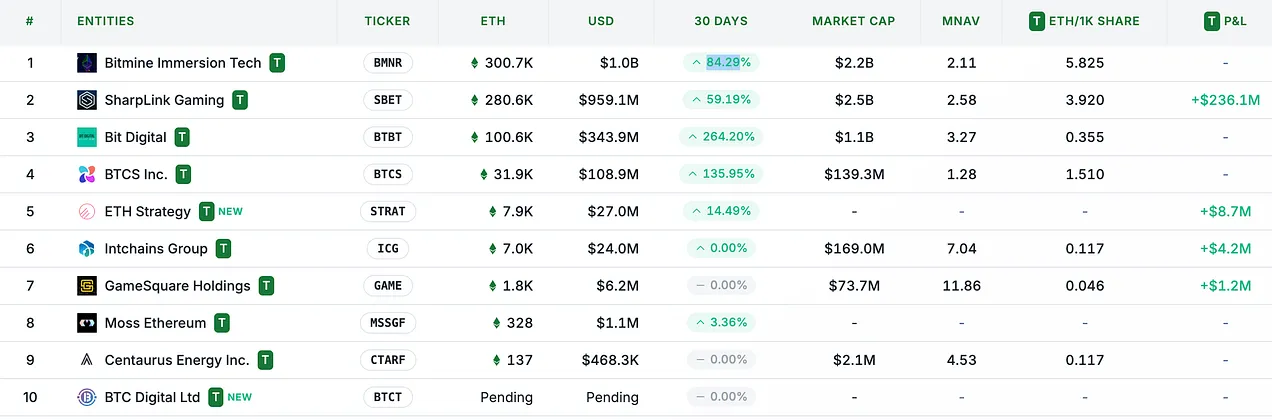

Reserve Momentum: ETH’s MicroStrategy Moment

While on-chain assets and institutional demand are long-term structural drivers for ETH, corporate treasury strategies—akin to MicroStrategy’s (MSTR) use of Bitcoin—could become a sustained catalyst for ETH’s value. A key inflection point came in late May when Sharplink Gaming ($SBET) announced its Ethereum treasury strategy, led by Ethereum co-founder Joseph Lubin.

Figure 12: ETH Treasury Holdings

Source: strategicethreserve.xyz

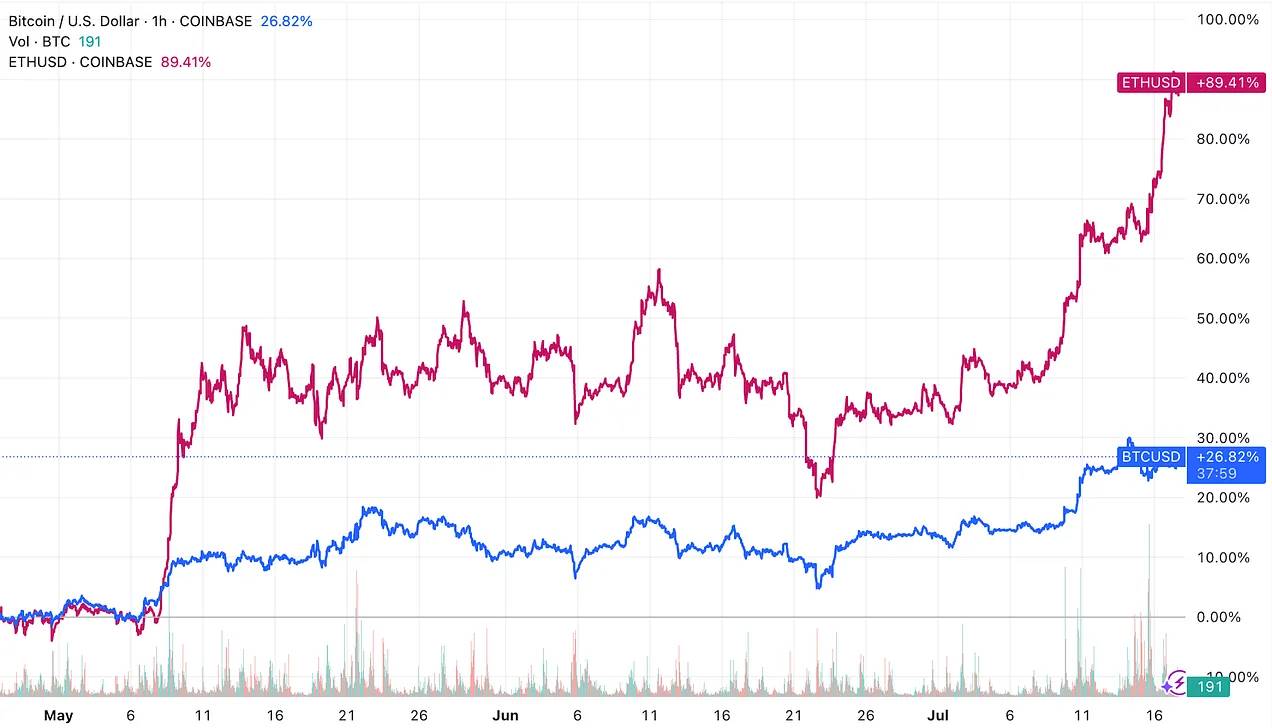

Treasury strategies allow tokens to access traditional finance (TradFi) liquidity while boosting the asset value per share of the issuing company. Since the emergence of Ethereum-based treasury strategies, these firms have accumulated over 730,000 ETH, and ETH has begun to outperform Bitcoin—a rare occurrence in this cycle. We believe this marks the beginning of a broader trend toward Ethereum-centric treasury adoption.

Figure 13: Price Performance of ETH and BTC

Stay tuned for our upcoming research report diving deeper into the evolving landscape of Ethereum treasury adoption!

Conclusion: ETH as the Reserve Asset of the On-Chain Economy

Ethereum’s evolution reflects a broader paradigm shift in how monetary assets are conceptualized in the digital economy. Just as Bitcoin overcame early skepticism to earn recognition as “digital gold,” ETH is forging its own identity—not by mimicking Bitcoin’s narrative, but by evolving into a more versatile and foundational asset. ETH is neither merely a cloud-computing stock nor a utility token for transaction fees or protocol revenues. Rather, it represents a scarce, programmable, and economically essential reserve asset—one that underpins the security, settlement, and functionality of an increasingly institutionalized on-chain financial ecosystem.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News