Web3 Lawyer Deep Dive: A Comprehensive Guide to Stablecoin Regulatory Frameworks in the EU, UAE, and Singapore

TechFlow Selected TechFlow Selected

Web3 Lawyer Deep Dive: A Comprehensive Guide to Stablecoin Regulatory Frameworks in the EU, UAE, and Singapore

Outline the regulatory frameworks for stablecoins of the three parties respectively.

Author: Crypto Salad

In previous articles, the Crypto Salad team provided a detailed introduction to the stablecoin regulatory frameworks in the United States and Hong Kong from multiple perspectives. Beyond these two jurisdictions, many other countries and regions around the world have also established relatively comprehensive stablecoin regulatory systems.

In this article, the Crypto Salad team selects three of the most representative and internationally influential jurisdictions—namely, the European Union (EU), the United Arab Emirates (UAE), and Singapore—and applies the same analytical framework and logical structure, combined with the team’s practical experience in blockchain projects, to outline the respective stablecoin regulatory frameworks in these three jurisdictions.

This analysis of stablecoin regulation will proceed from the following angles: regulatory timeline, governing documents, supervisory authorities, and core components of the regulatory framework. The specific structure is as follows:

Table of Contents

(I) European Union

1. Regulatory Timeline and Governing Documents

2. Supervisory Authorities

3. Core Components of the Regulatory Framework

a. Definition of Stablecoins

b. Issuer准入 Thresholds

c. Value Stability Mechanism and Reserve Asset Maintenance

d. Compliance Requirements in Circulation

e. Special Regulations for Significant ARTs

(II) United Arab Emirates

1. Regulatory Timeline and Governing Documents

2. Supervisory Authorities

3. Core Components of the Regulatory Framework

a. Definition of Stablecoins

b. Issuer准入 Thresholds

c. Value Stability Mechanism and Reserve Asset Maintenance

d. Compliance Requirements in Circulation

(III) Singapore

1. Regulatory Timeline and Governing Documents

2. Supervisory Authorities

3. Core Components of the Regulatory Framework

a. Definition of Stablecoins

b. Issuer准入 Thresholds

c. Value Stability Mechanism and Reserve Asset Maintenance

d. Compliance Requirements in Circulation

(The above diagram illustrates a comparison of stablecoin regulatory frameworks across the EU, UAE, and Singapore, for reference only.)

I. European Union

1. Regulatory Timeline and Governing Documents

The European Union officially released its core regulatory document, the Markets in Crypto-Assets Regulation (hereinafter “MiCA”), in June 2023. MiCA aims to establish a unified regulatory framework for crypto-assets, addressing issues of fragmented regulation among member states.

The rules under MiCA concerning stablecoin issuance came into full effect on June 30, 2024. All entities subject to these provisions are now required to fully comply.

2. Supervisory Authorities

The European Banking Authority (EBA) and the European Securities and Markets Authority (ESMA) are responsible for developing the regulatory framework and overseeing issuers of significant stablecoins and related service providers.

The national competent authority in the member state where the stablecoin issuer is located also holds partial supervisory powers over the issuer.

3. Regulatory Framework and Key Provisions

a. Definition of Stablecoins

MiCA Article 18 divides stablecoins into two categories:

I. Electronic Money Tokens (EMT)

An EMT refers to a crypto-asset whose value is stabilized solely by reference to one official currency. MiCA explicitly states that the function of an EMT is very similar to that of electronic money as defined in Directive 2009/110/EC. Like electronic money, an EMT essentially serves as an electronic substitute for traditional fiat currency and can be used in everyday payment scenarios.

II. Asset-Referenced Tokens (ART)

An ART refers to a crypto-asset whose value is stabilized by reference to a combination of values including one or more official currencies.

The distinction between EMTs and ARTs goes beyond merely the number and type of referenced currencies. MiCA Article 19 elaborates on their differences:

Under Directive 2009/110/EC, holders of EMTs always have a contractual claim against the issuer and possess the right to redeem their tokens at face value at any time. This means the redemption capability of EMTs is absolutely guaranteed by legal claims.

In contrast, ARTs do not automatically confer such creditor rights upon holders and may therefore fall outside the scope of Directive 2009/110/EC. Some ARTs do not grant holders claims equal to the face value of the referenced currency or impose restrictions on redemption periods. If an ART holder lacks a corresponding claim against the issuer, or if the claim does not match the face value of the referenced currency, confidence in the stability of the token may be undermined.

All subsequent regulatory analysis in this article will separately address both ARTs and EMTs.

Regarding algorithmic stablecoins, MiCA does not include them within its stablecoin regulatory framework. Since algorithmic stablecoins lack clearly defined reserves linked to real-world assets, they do not fall under either EMT or ART as defined by MiCA.

From a regulatory standpoint, this effectively means algorithmic stablecoins are prohibited under MiCA—a position closely aligned with policy directions in the U.S. and Hong Kong. This reflects a shared global regulatory caution toward algorithmic stablecoins lacking backing by tangible assets.

Regulatory Analysis of ARTs under MiCA

b. Issuer准入 Thresholds

According to MiCA Article 16, ART issuers fall into two types:

-

The first type consists of legal persons or enterprises established in the EU and authorized by the competent authority of a member state pursuant to MiCA Article 21. To apply for authorization, applicants must submit information and documents including the issuer's address, Legal Entity Identifier (LEI), articles of association, business model, and legal opinions.

-

The second type includes credit institutions compliant with MiCA Article 17. Such institutions must provide relevant documentation—including operational plans, legal opinions, and token governance arrangements—to the competent authority within 90 days.

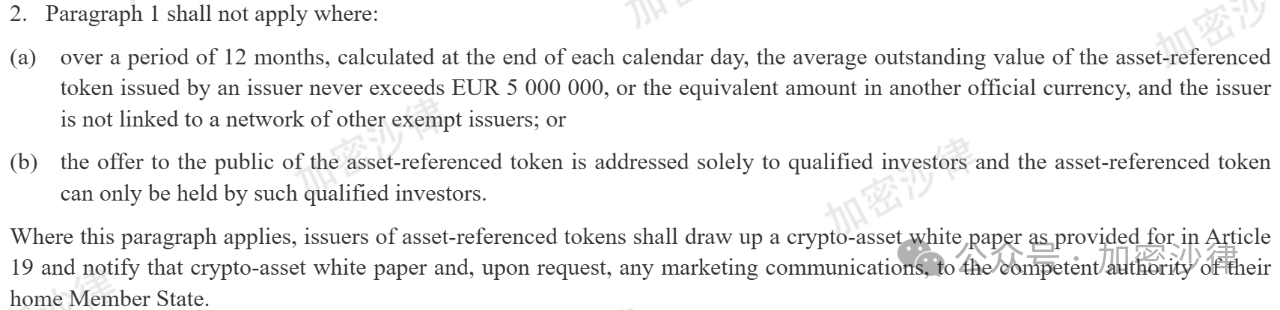

However, MiCA also provides exemptions from issuer qualification requirements. An issuer qualifies for exemption if it meets either of the following conditions:

I. The average circulating value of its issued ART has never exceeded €5,000,000 (or equivalent in other official currencies) over any 12-month period;

II. The ART is issued exclusively to qualified investors and circulates only among them.

Although MiCA exempts these two categories of ART issuers from formal qualification requirements, it does not imply absence of oversight. In practice, such issuers are still required to draft a white paper in accordance with MiCA Article 19 and notify the competent authority of their home member state for registration purposes.

(Above: Original text of MiCA Article 16.2)

In addition, ARTs with an average circulating value exceeding €100,000,000 are subject to stricter supervision. Their issuers bear additional reporting obligations and must report the following information quarterly to the competent authority:

The number of holders, the total value of issued ARTs and size of reserve assets, daily average transaction count, and average transaction amount during the quarter.

Finally, MiCA specifies minimum own funds requirements for all ART issuers. An ART issuer must always maintain own funds that are equal to or greater than the highest of the following three thresholds:

I. €350,000;

II. 2% of the average amount of reserve assets as specified in Article 36;

III. One-quarter of the fixed management expenses incurred in the previous year.

In summary, MiCA adopts a flexible "tiered supervision" approach toward ART issuers.

Issuers whose ARTs have an average circulating value below €5,000,000 or are issued solely to qualified investors may be exempt from authorization requirements but must still prepare a white paper and notify the competent authority.

Issuers with ARTs averaging between €5,000,000 and €100,000,000 in circulation must meet full MiCA qualification requirements, complete the authorization process, and submit required documentation.

Issuers with ARTs exceeding €100,000,000 in average circulation must satisfy standard qualification criteria and fulfill additional reporting duties.

All ART issuers, regardless of circulation scale or target investor group, must maintain sufficient own funds at all times.

(Diagram illustrating issuer qualification requirements for different types of ARTs)

c. Value Stability Mechanism and Reserve Asset Maintenance

First, MiCA Article 36 mandates that ART issuers must always hold reserve assets that meet two core conditions:

I. Capable of covering risks associated with the assets pegged to the ART;

II. Sufficient to address liquidity risks arising from holders’ perpetual redemption rights.

In other words, reserve assets must mitigate both endogenous risks stemming from the reserves themselves and external run risks triggered by redemptions from token holders.

However, MiCA does not prescribe specific standards regarding the amount or composition of reserve assets. Instead, it delegates this task to the European Banking Authority (EBA), which is responsible for drafting technical standards to further clarify reserve and liquidity requirements.

(Above: Excerpt from MiCA Article 36)

Second, ART issuers must ensure complete segregation between reserve assets and their own corporate assets, and entrust reserve assets to third parties for independent custody.

Third, ART issuers may invest part of their reserve assets, provided the investments meet the following conditions:

I. Instruments must be highly liquid financial instruments with minimal market, credit, and concentration risk;

II. Investments must be readily convertible into cash with minimal adverse price impact upon exit.

In short, reserve assets can only be invested in extremely low-risk, highly liquid compliant financial instruments to minimize exposure.

d. Circulation Compliance

First, MiCA Article 39 clearly states that ART holders have the unconditional right to request redemption from the issuer. ARTs must be redeemed at the market value of the reference asset upon holder request. Furthermore, issuers must establish clear policies outlining the terms and underlying mechanisms for exercising redemption rights.

Second, MiCA imposes limits on the maximum circulation volume of ARTs. If an ART exceeds 1 million transactions per quarter or an average daily transaction value exceeding €200,000,000, the issuer must immediately cease further issuance and submit a plan to the competent authority within 40 working days to bring transaction volumes and values below these thresholds.

This establishes a hard ceiling on ART circulation under MiCA. Regardless of demand, no ART may exceed this cap. This rule aims to prevent excessive circulation that could trigger internal liquidity risks.

e. Special Rules for Significant ARTs

A Significant Asset-Referenced Token (Significant ART) is an ART meeting specific criteria, defined by seven indicators.

The first three relate directly to the ART’s circulation volume and market size:

I. Number of ART holders exceeds 10 million;

II. Market capitalization or reserve asset size exceeds €5 billion;

III. Daily average number of transactions and daily average transaction value exceed 2.5 million transactions and €500 million, respectively.

The remaining four indicators concern characteristics of the ART issuer:

IV. The issuer is designated under Regulation (EU) 2022/1925 of the European Parliament and Council as a gatekeeper providing core platform services;

V. The issuer’s activities have international significance, particularly in payments and remittances using ARTs;

VI. The degree of interconnectedness between the issuer and the broader financial system;

VII. The issuer also issues other ARTs, EMTs, or provides at least one crypto-asset service.

When an ART meets any three of these seven criteria, the European Banking Authority (EBA) shall classify it as a Significant ART. Within 20 working days of notification, supervisory responsibility shifts from the national competent authority to the EBA, which assumes ongoing oversight.

The rationale behind distinguishing Significant ARTs lies in MiCA Article 45, which imposes additional obligations on their issuers, including but not limited to:

I. Adoption and implementation of compensation policies conducive to effective risk management;

II. Assessment and monitoring of token liquidity needs to meet redemption demands. To this end, issuers must establish, maintain, and implement liquidity management policies and procedures;

III. Regular liquidity stress testing of the token. The EBA may dynamically adjust liquidity requirements based on stress test results.

Brief Analysis of EMT Regulations under MiCA

Compared to ARTs, the准入 requirements for EMT (Electronic Money Token) issuers are stricter. Only certified Electronic Money Institutions (EMIs) or credit institutions may legally issue EMTs under MiCA. Additionally, EMT issuers must prepare a crypto-asset white paper and notify the competent authority thereof.

Beyond these points, the regulatory requirements for EMT issuers regarding reserve asset maintenance and management largely mirror those applicable to ART issuers, with substantial overlap. Therefore, a separate detailed analysis is omitted here.

II. United Arab Emirates

1. Regulatory Timeline

In June 2024, the Central Bank of the UAE issued the Payment Token Services Regulation, clarifying the definition and regulatory framework for “payment tokens” (i.e., stablecoins).

2. Governing Documents

The primary regulatory document is the aforementioned Payment Token Services Regulation.

3. Supervisory Authorities

The UAE is a federal state composed of seven autonomous emirates, including well-known ones such as Dubai and Abu Dhabi. Consequently, its stablecoin regulatory framework features a dual-track system: federal-level and emirate-level coexistence.

The Central Bank of the UAE issued the Payment Token Services Regulation and directly oversees stablecoin issuance at the federal level. However, its jurisdiction excludes two financial free zones: DIFC (Dubai International Financial Centre) and ADGM (Abu Dhabi Global Market).

These two zones operate under independent legal systems and have their own regulatory bodies, thus falling outside direct oversight by the Central Bank of the UAE.

This dual-track regulatory system ensures uniform federal-level supervision to safeguard the sound development of the stablecoin industry, while allowing financial free zones space for institutional innovation and experimentation. Compared to the chaotic and overlapping regulatory landscape in the U.S.—where SEC, CFTC, and the Federal Reserve frequently assert conflicting jurisdictions—the UAE’s dual-track model appears significantly clearer and more efficient.

4. Core Elements of the Regulatory Framework

a. Definition of Stablecoins

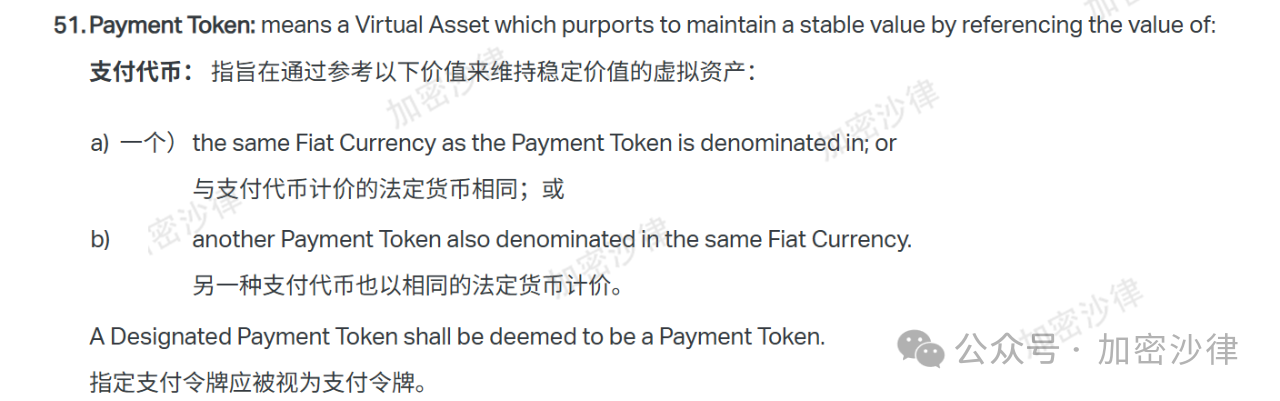

The Payment Token Services Regulation (hereinafter “the Regulation”) avoids using the term “stablecoin” and instead uses “payment token.” For consistency, we refer to it as “stablecoin” throughout this article.

Article 1 of the Regulation defines a stablecoin as:

“A virtual asset intended to maintain a stable value by referencing the value of a fiat currency or another stablecoin denominated in the same currency.”

(Above: Article 1.51 of the Payment Token Services Regulation)

Thus, compared to the EU’s MiCA or Hong Kong’s Stablecoin Ordinance, the UAE’s definition is broader.

Additionally, Article 4 of the Regulation specifies tokens excluded from its scope:

1. Token-type exemptions: Tokens used solely for reward programs or loyalty points circulating within a closed ecosystem (e.g., supermarket membership points) are not regulated.

2. Usage-based exemptions: Stablecoins with less than 500,000 AED in reserves and fewer than 100 holders are also exempt.

Compared to the EU’s layered regulatory model, the UAE’s approach is simpler and more concise.

It should be noted that the Regulation governs not only issuers but also activities such as conversion, custody, and transfer of stablecoins. The following discussion focuses primarily on issuer-related regulations.

b. Issuer准入 Thresholds

To obtain a license, a stablecoin issuer must meet the following requirements:

Legal Form Requirement:

The applicant must be a corporate entity registered in the UAE and licensed or registered by the Central Bank of the UAE.

Initial Capital Requirements;

Necessary Documents and Information.

c. Value Stability Mechanism and Reserve Asset Maintenance

First, stablecoin issuers must establish robust systems to protect and manage reserve assets, ensuring that:

-

Reserve assets are used solely for their intended purpose;

-

Reserve assets are protected from operational and other related risks;

-

Reserve assets are safeguarded at all times from claims by the issuer’s other creditors.

Second, issuers must hold reserve assets in cash form within independent custodial accounts dedicated exclusively to holding such reserves, ensuring independence and security.

Third, the Regulation sets explicit requirements for reserve asset maintenance:

The value of reserve assets must be at least equal to the total fiat currency face value of all outstanding stablecoins—ensuring full backing. This aligns with standards in the EU and Hong Kong.

Issuers must accurately record and verify inflows and outflows of reserve assets and regularly reconcile system records with actual holdings to ensure consistency between book and actual values.

Issuers must engage external auditors to conduct monthly audits, ensuring auditor independence—no direct affiliation with the issuer. The audit team must confirm that reserve asset value equals or exceeds the fiat-denominated value of circulating stablecoins. This indicates relatively high audit transparency expectations. Notably, Tether, the issuer of the largest stablecoin USDT, currently conducts only quarterly audits and does not yet meet this monthly audit standard.

Issuers must implement strong internal controls and procedures to protect reserve assets from misappropriation, fraud, or theft.

d. Circulation Compliance Requirements

The Regulation addresses compliance in circulation from several key aspects:

[Stablecoins as Pure Payment Instruments – Interest-Bearing Stablecoins Not Recognized]

First, the Regulation stipulates that stablecoins must not pay interest or any time-based benefits to users. Thus, stablecoins are permitted only as pure payment tools, without investment or yield-generating features. Consequently, interest-bearing stablecoins (e.g., USDY issued by Ondo) are not recognized under this framework. This aligns with mainstream regulatory positions globally.

[Unrestricted Redemption Rights]

Second, stablecoin holders may redeem tokens for the corresponding fiat currency at any time without restriction. Issuers must clearly disclose redemption terms and fees in customer agreements and must not charge unreasonable fees beyond legitimate costs.

[Anti-Money Laundering and Counter-Terrorist Financing Requirements]

Stablecoin issuers, as obligated entities, must comply with UAE’s applicable anti-money laundering (AML) and counter-terrorist financing (CFT) laws and regulations and establish comprehensive and effective internal AML strategies and controls.

Typically, AML/CFT obligations for stablecoin issuers follow existing national frameworks. For example, Hong Kong-based issuers must adhere to Hong Kong’s AML Ordinance. This effectively integrates stablecoin issuers into the broader national AML supervisory regime.

[Payment and Personal Data Protection]

Stablecoin issuers must establish policies to protect user personal data collected during operations. However, issuers may disclose such data under certain circumstances to the following entities:

-

Central Bank of the UAE;

-

Other regulatory bodies approved by the Central Bank;

-

Courts;

-

Or other government agencies with authorized access.

III. Singapore

1. Regulatory Timeline

In December 2019, Singapore enacted the Payment Services Act (PSA), defining payment service providers,准入 thresholds, licensing requirements, and related regulations.

In December 2022, the Monetary Authority of Singapore (MAS) issued a public consultation paper on the proposed Stablecoin Regulatory Framework. Less than a year later, MAS formally released the Stablecoin Regulatory Framework on August 15, 2023. This framework applies to single-currency stablecoins (SCS) issued in Singapore and pegged to the Singapore dollar or G10 currencies.

2. Governing Documents

-

Payment Services Act (PSA)

-

Stablecoin Regulatory Framework

The Stablecoin Regulatory Framework supplements the PSA and further clarifies compliance obligations for stablecoin issuers.

3. Supervisory Authority

The Monetary Authority of Singapore (MAS) is responsible for oversight, including issuing licenses and enforcing compliance for stablecoin issuers.

4. Core Components of the Regulatory Framework

a. Definition of Stablecoins

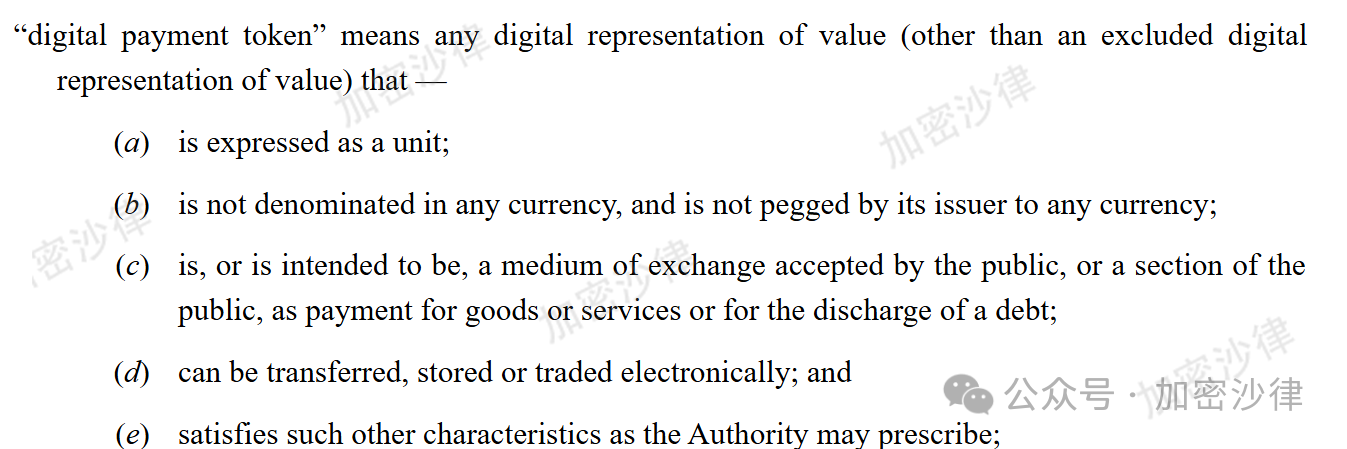

Article 2 of the Payment Services Act defines a payment token as:

(1) Represented in units;

(2) Not denominated in any currency, nor pegged to any currency by the issuer;

(3) Is or is intended to be accepted by the public or a segment of the public as a medium of exchange for payment of goods or services or discharge of debt;

(4) Can be transferred, stored, or traded electronically.

(Above: Original definition of digital payment tokens under Article 2 of the PSA)

For consistency and readability, the term “stablecoin” will replace “payment token” henceforth.

The subsequently released Stablecoin Regulatory Framework adopts a narrower definition, regulating only single-currency stablecoins (SCS) issued in Singapore and pegged to the Singapore dollar or G10 currencies.

b. Issuer准入 Thresholds

To obtain a license from MAS, a stablecoin issuer must meet the following three conditions:

-

Base Capital Requirement: The issuer’s capital must be no less than 50% of annual operating expenses or SGD 1 million, whichever is higher.

-

Business Restriction Requirement: The issuer must not engage in trading, asset management, staking, lending, or other businesses, nor directly hold equity stakes in other legal entities.

-

Solvency Requirement: Liquid assets must cover normal withdrawal demands or exceed 50% of annual operating expenses.

c. Value Stability Mechanism and Reserve Asset Maintenance

MAS has established the following rules regarding reserve asset management:

First, reserve assets must consist exclusively of assets with extremely low risk and high liquidity: cash, cash equivalents, and bonds with residual maturities of no more than three months.

Furthermore, issuers of these assets must be sovereign governments, central banks, or international institutions rated AA- or higher.

This demonstrates MAS’s strict and detailed constraints on reserve asset composition—particularly evident when compared to the UAE, which does not specify such granular limitations.

Second, issuers must establish a fund and open segregated accounts to strictly separate proprietary funds from reserve assets.

Third, the daily market value of reserve assets must exceed the outstanding supply of stablecoins, ensuring full backing at all times.

d. Circulation Compliance Requirements

Stablecoin issuers have a statutory obligation to redeem tokens. Holders may freely redeem stablecoins, and issuers must complete redemptions at par value within five business days.

The views expressed herein are those of the author alone and do not constitute legal advice or opinion on any specific matter.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News