Who will replace Ethereum's dominance in the RWA market?

TechFlow Selected TechFlow Selected

Who will replace Ethereum's dominance in the RWA market?

Exploring Ethereum's structural challenges in the RWA market and the rise of new tokenization platforms.

Authors: Chi Anh, Ryan Yoon, Tiger Research

Translation: AididiaoJP, Foresight News

Executive Summary

-

Ethereum currently leads the RWA market due to first-mover advantage, institutional precedents, deep on-chain liquidity, and decentralized architecture.

-

L1 blockchains with faster transaction speeds and lower costs, as well as RWA-dedicated chains designed for compliance, are addressing Ethereum’s limitations in cost and performance. These emerging platforms position themselves as next-generation RWA infrastructure by offering superior technical scalability or built-in compliance features.

-

The next phase of RWA growth will depend on three key factors: on-chain regulatory compatibility, a service ecosystem built around real-world assets, and sufficient on-chain liquidity.

Where is the RWA market developing?

Real-World Asset tokenization (RWA) has become one of the mainstream trends in the blockchain industry. Global consulting firms such as Boston Consulting Group (BCG) have released extensive market forecasts, and Tiger Research finds growing momentum in emerging markets like Indonesia.

So what exactly are RWAs? They refer to converting tangible assets—such as real estate, bonds, and commodities—into digital tokens. The tokenization process inherently relies on blockchain infrastructure. Currently, Ethereum holds the leading position among infrastructures supporting such tokenization.

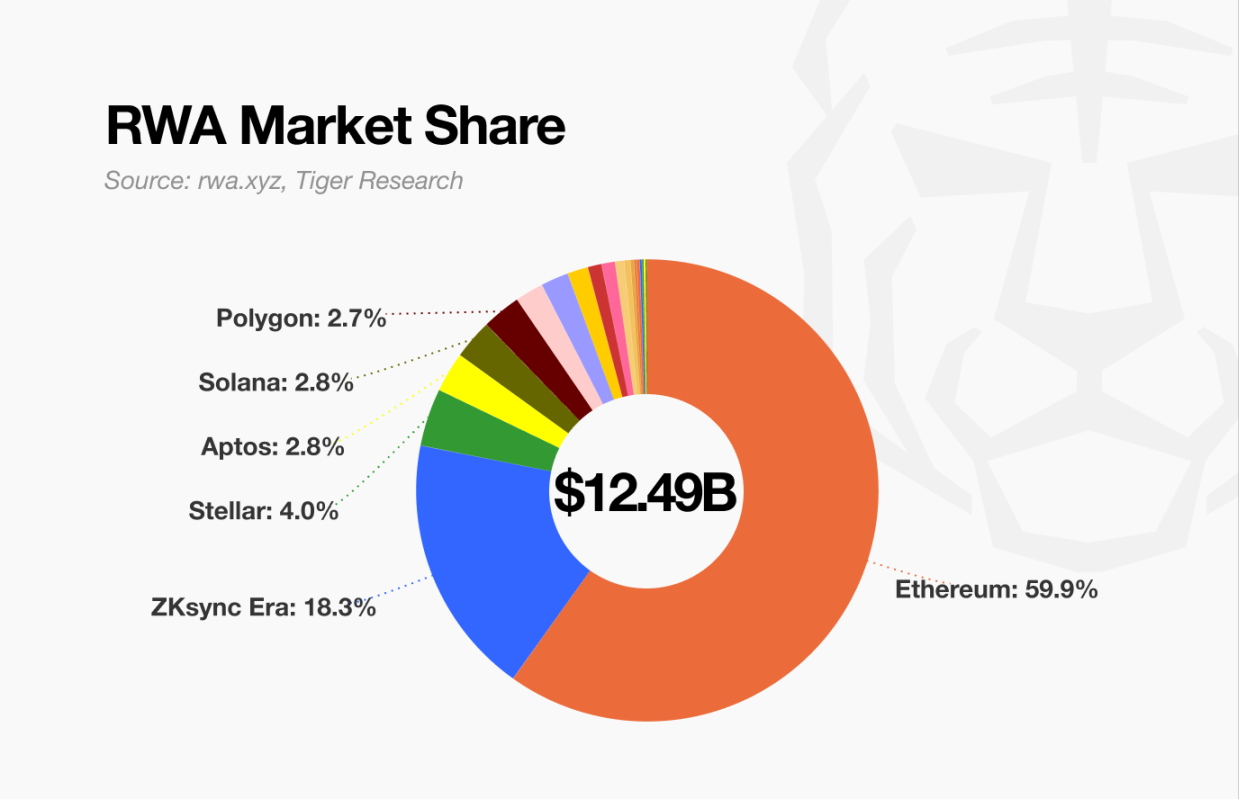

Source: rwa.xyz, Tiger Research

Despite increasing competition, Ethereum maintains dominance in the RWA market. While several RWA-focused blockchains have emerged and platforms like Solana—already established in DeFi—are expanding into RWA, Ethereum still accounts for over 50% of market activity, underscoring its strong market position.

This report examines the key factors behind Ethereum's current leadership in the RWA market and explores critical elements that may shape the next stage of growth and competition.

Why does Ethereum remain ahead?

2.1 First-Mover Advantage and Institutional Trust

The reasons Ethereum became the default platform for institutional tokenization are clear. It was the first to establish key tokenization smart contract standards and actively prepare for the RWA market.

Backed by a highly active developer community, Ethereum established foundational tokenization standards such as ERC-1400 and ERC-3643 well before competing platforms emerged. This early foundation provided institutions with the necessary technological and regulatory groundwork to experiment with RWA projects.

Many institutions prioritize evaluating Ethereum before considering alternatives. Key initiatives by major financial players have cemented Ethereum’s role as essential RWA infrastructure:

JPMorgan’s Quorum and JPM Coin (2016–2017): To support enterprise use cases, JPMorgan developed Quorum, a permissioned fork of Ethereum, while JPM Coin facilitates interbank transfers. This demonstrated that even in private form, Ethereum’s architecture can meet regulatory requirements for data protection and compliance.

Société Générale bond issuance (2019): Société Générale FORGE issued €100 million in covered bonds on Ethereum’s public mainnet. This showed regulated securities could be issued and settled on public blockchains while minimizing intermediary involvement.

European Investment Bank digital bond (2021): The European Investment Bank, in collaboration with Goldman Sachs, Santander, and Société Générale, issued a €100 million digital bond on Ethereum. The bond was settled using a central bank digital currency (CBDC) issued by the Banque de France, highlighting Ethereum’s potential in fully integrated capital markets.

These successful pilot cases strengthened Ethereum’s credibility. For institutions, trust stems from proven use cases and endorsements from other regulated participants. Ethereum continues to attract interest, forming a self-reinforcing cycle of adoption.

Source: Securitize

For example, in 2018, Securitize announced it would build tools on Ethereum to manage the full lifecycle of digital securities. This laid the foundation for BlackRock’s eventual launch of BUIDL—the largest tokenized fund currently issued on Ethereum.

2.2 Blockchain with Sustained Inflows of Traditional Capital

Another key reason for Ethereum’s continued dominance in the RWA market is its ability to convert on-chain liquidity into actual purchasing power.

Tokenizing real-world assets is not just a technical process. A functioning market requires capital willing to actively invest in and trade these assets. Here, Ethereum stands out as the only platform with deep and deployable on-chain liquidity.

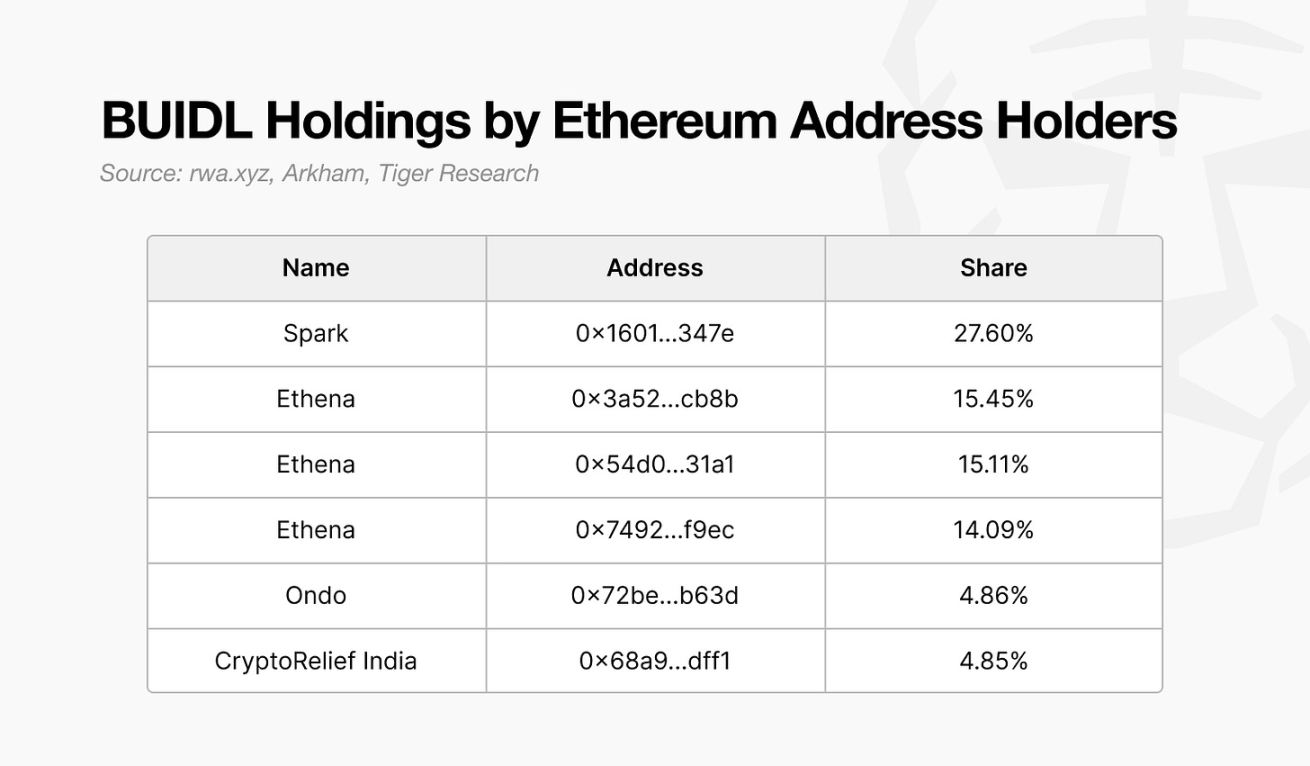

Source: rwa.xyz, Arkham, Tiger Research

This is evident in platforms like Ondo, Spark, and Ethena, all holding significant amounts of the tokenized BUIDL fund on Ethereum. These platforms have attracted hundreds of millions in funding by offering products backed by tokenized U.S. Treasuries, stablecoin-based lending, and synthetic yield-bearing dollar instruments.

-

Ondo Finance has accumulated over $600 million in TVL through its Treasury-backed products USDY and OUSG.

-

Spark Protocol leveraged MakerDAO’s DAI liquidity to purchase over $2.4 billion in U.S. Treasuries.

-

Ethena built a bankless yield infrastructure on Ethereum using its synthetic stablecoin USDe and sUSDe, attracting institutional demand and DeFi liquidity.

These examples show Ethereum is more than just an asset tokenization platform. It provides a robust liquidity base that supports investment and asset management for large institutions and financial firms. In contrast, many emerging RWA platforms struggle to ensure sustained capital inflows or maintain active secondary market trading after initial token issuance.

The reason for this gap is clear. Ethereum has integrated stablecoins, DeFi protocols, and compliant infrastructure, creating a comprehensive financial environment where issuance, trading, and settlement can all occur on-chain.

Thus, Ethereum remains the most efficient environment for turning tokenized assets into real purchasing activity—an enduring structural advantage.

2.3 Building Trust Through Decentralization

Decentralization plays a crucial role in establishing trust. Tokenizing real-world assets involves transferring ownership and transaction records of high-value assets onto the blockchain. During this process, institutions prioritize system reliability and transparency—areas where Ethereum’s decentralized architecture excels.

Ethereum is a public chain supported by thousands of independently operated nodes worldwide. The network is open to all, with changes governed by participant consensus rather than centralized control. This eliminates single points of failure, resists hacking and censorship, and ensures uninterrupted uptime.

In the RWA market, this structure creates tangible value. Transaction records are stored on an immutable ledger, reducing fraud risks. Smart contracts enable trustless transactions without intermediaries. Users can access services, sign agreements, and participate in financial activities without centralized approval.

Features such as transparency, security, and accessibility make Ethereum an ideal choice for institutions exploring asset tokenization. Its decentralized system aligns with core requirements for operating in high-risk financial environments.

Emerging Challengers Reshaping the Landscape

Ethereum made tokenized finance feasible—but it also revealed structural limitations that hinder broader institutional adoption. These include limited transaction throughput, latency issues, and unpredictable fee structures.

To address these challenges, Layer 2 rollup solutions such as Arbitrum, Optimism, and Polygon zkEVM have emerged. Major upgrades including Merge (2022), Dencun (2024), and the recently launched Pectra (2025) have enhanced Ethereum’s scalability. However, the network still falls short of traditional financial infrastructure. For instance, Visa processes over 65,000 transactions per second—far beyond Ethereum’s current capacity. For institutions requiring high-frequency trading or real-time settlement, these performance gaps remain a critical constraint.

Latency and finality also pose challenges. Block production averages 12 seconds, and with additional confirmations needed for secure settlement, finality often takes up to three minutes. During network congestion, delays can increase further, complicating time-sensitive financial operations.

More importantly, gas fee volatility is a concern. Transaction fees can exceed $50 during peak times and frequently surpass $20 even under normal conditions. This fee uncertainty complicates business planning and may undermine the competitiveness of Ethereum-based services.

Securitize exemplifies this shift. After encountering Ethereum’s limitations, the company expanded to other platforms such as Solana and Polygon, while also developing its own blockchain, Converage. Although Ethereum played a vital role in early institutional experiments, it now faces mounting pressure to meet the demands of a more mature, performance-sensitive market.

3.1 High-Throughput, Cost-Efficient General-Purpose Blockchains Are Emerging

As Ethereum’s limitations become more apparent, institutions are increasingly exploring alternative general-purpose blockchains. These platforms aim to overcome Ethereum’s key performance bottlenecks—particularly in transaction speed, fee stability, and finality time.

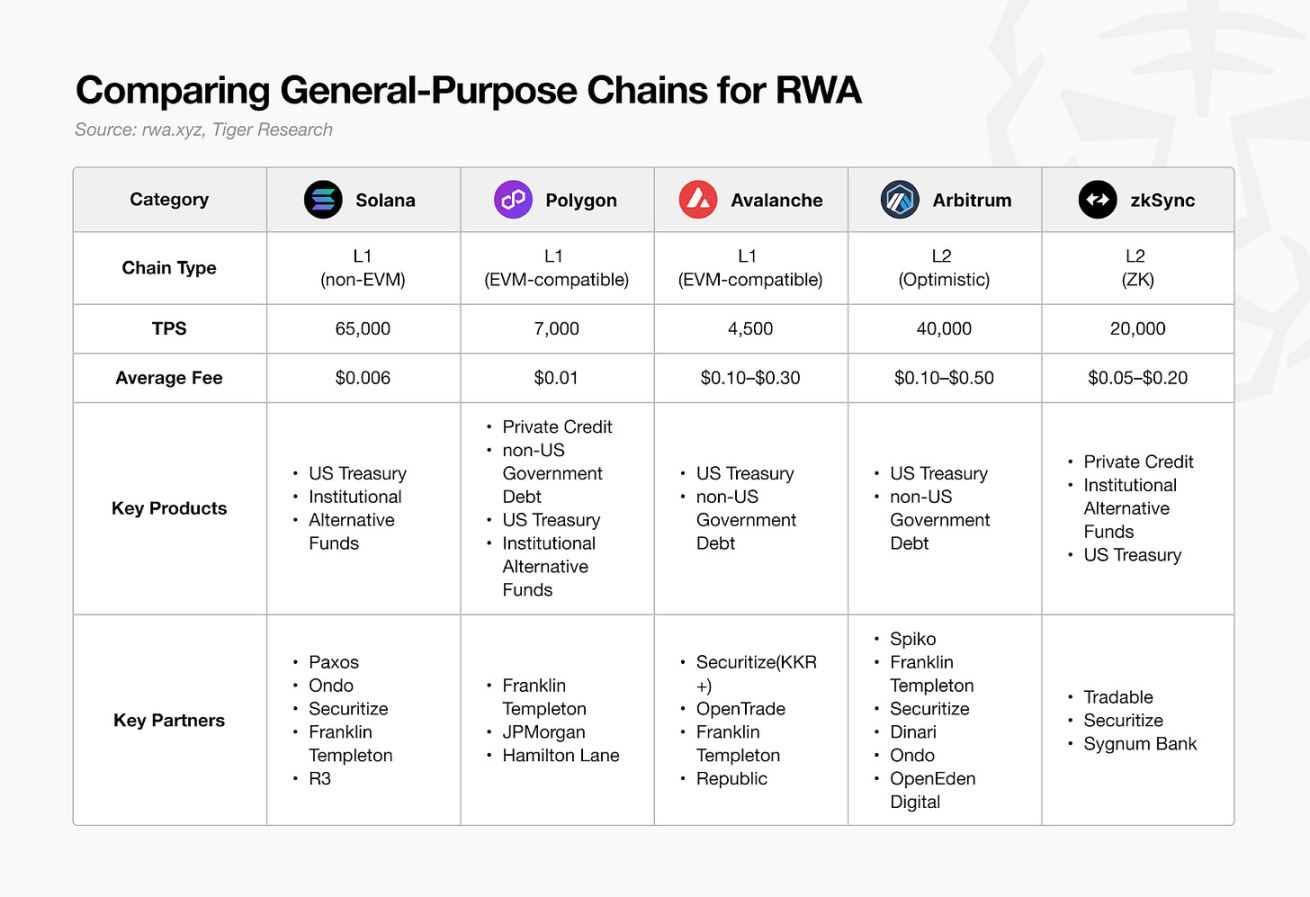

Source: rwa.xyz, Tiger Research

Despite ongoing institutional engagement, the actual scale of tokenized assets (excluding stablecoins) on these platforms remains far below Ethereum. In many cases, tokenized assets launched on general-purpose chains are part of multi-chain deployment strategies led by Ethereum.

Nonetheless, there are signs of meaningful progress. In private credit, new tokenization initiatives are emerging. For example, on zkSync, the Tradable platform has gained traction, capturing over 18% of activity in the sector—second only to Ethereum.

At this stage, general-purpose blockchains are only beginning to gain footing. Platforms like Solana, whose DeFi ecosystems have grown rapidly, now face a strategic challenge: how to translate that momentum into sustainable positioning within the RWA space. Superior technical performance alone is insufficient. Solana must meet institutional expectations regarding trust and compliance.

Ultimately, success in the RWA market will depend less on raw throughput and more on the ability to deliver tangible value. Differentiated ecosystems built around each chain’s unique strengths will determine their long-term positioning in this emerging field.

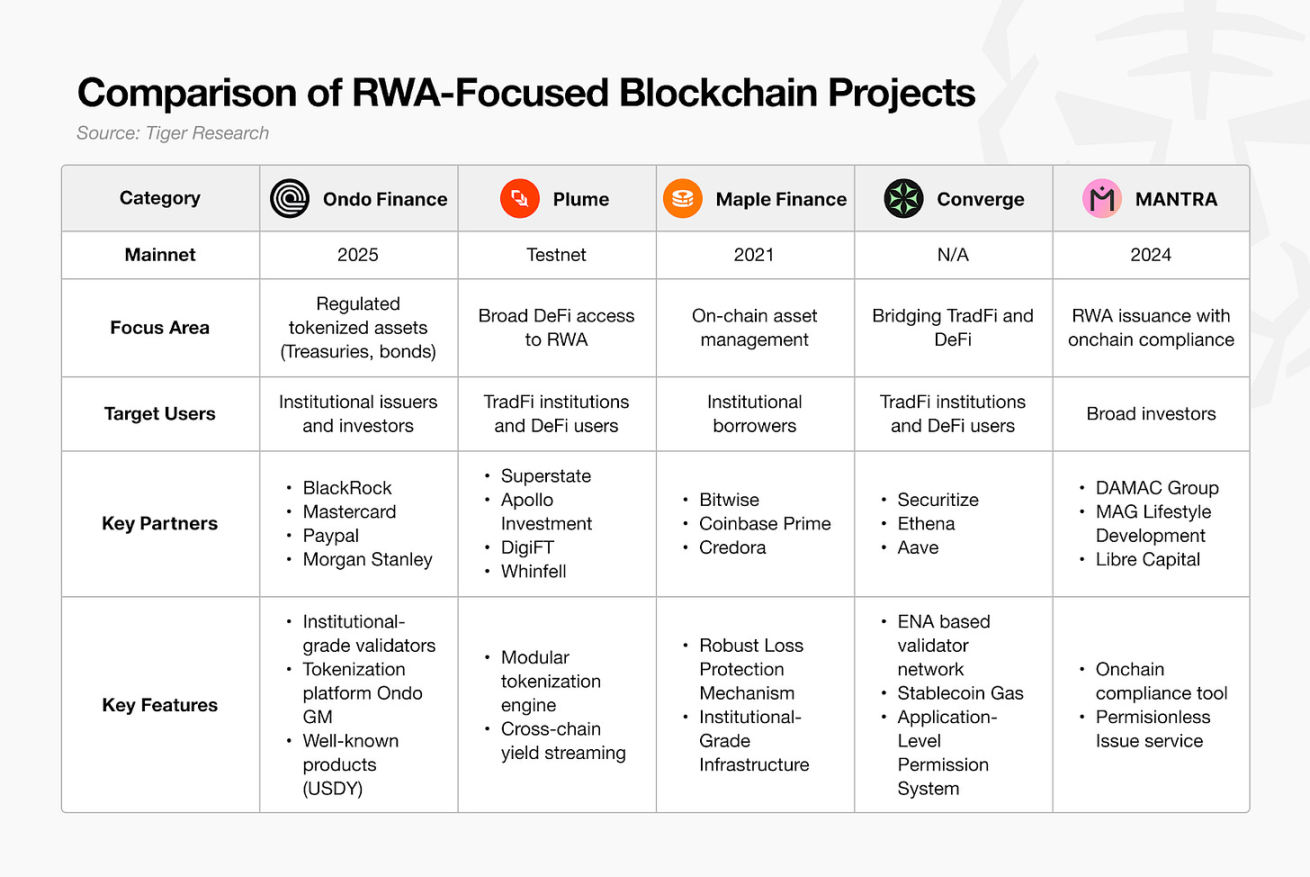

3.2 The Rise of RWA-Dedicated Blockchains

An increasing number of blockchain platforms are moving away from general-purpose designs toward domain-specific focus. This trend is evident in the RWA space, where a new wave of RWA-dedicated chains is emerging—specifically optimized for real-world asset tokenization.

Source: Tiger Research

The rationale behind RWA-dedicated blockchains is straightforward. Tokenizing real-world assets requires direct integration with existing financial regulations—a task where general-purpose blockchain infrastructure often falls short. RWA-dedicated chains aim to fundamentally address specialized technical requirements, particularly in regulatory compliance.

Compliance handling is a key area. KYC and AML procedures are critical to tokenization workflows but are typically processed off-chain. This approach merely wraps traditional financial assets in blockchain format without rethinking the underlying compliance logic.

The shift now is toward fully on-chain compliance. There is growing demand for blockchain networks that not only record ownership but natively enforce regulatory requirements at the protocol level.

Some RWA-focused blockchains are already offering on-chain compliance modules. For example, MANTRA includes decentralized identity (DID) functionality that enables compliance enforcement at the infrastructure layer. Other RWA-dedicated chains are expected to follow similar paths.

Beyond compliance, many platforms target specific asset classes and leverage deep domain expertise. Maple Finance focuses on institutional lending and asset management, Centrifuge on trade finance, and Polymesh on regulated securities. Rather than tokenizing widely held assets like sovereign bonds or stablecoins, these blockchains adopt vertical specialization as a competitive strategy.

Nevertheless, many of these platforms remain in early stages. Some have yet to launch mainnets, and most have limited scale and adoption. If general-purpose chains are only beginning to gain attention in RWA, dedicated chains are still at the starting line.

Who Will Replace Ethereum in the RWA Market?

Ethereum’s dominance in the RWA market is unlikely to persist unchanged. The current tokenized asset market represents less than 2% of its projected size, indicating the industry is still in its infancy. Ethereum’s past advantage largely stemmed from early product-market fit (PMF). As the market matures and scales, the competitive landscape will undergo significant transformation.

Signs of this shift are already visible. Institutions are no longer focusing solely on Ethereum. Both general-purpose blockchains and RWA-dedicated chains are undergoing market validation, and more services are exploring custom chain deployments. Tokenized assets initially issued on Ethereum are now expanding into multi-chain ecosystems, breaking the previous monopoly.

A pivotal turning point will be the realization of on-chain compliance. For blockchain finance to truly innovate, regulatory processes such as KYC and AML must occur directly on-chain. If specialized chains successfully deliver scalable, protocol-level compliance and drive industry-wide adoption, the current market structure could be completely disrupted.

Equally important is actual purchasing power. Tokenized assets only hold investment value when active capital is willing to buy them. Regardless of technology, without effective liquidity, the utility of tokenization is constrained. Therefore, the next generation of RWA platforms must build a robust service ecosystem around tokenized assets and ensure users have ample liquidity to participate.

In short, the next leading RWA platform will likely succeed by achieving three goals simultaneously:

-

Fully integrated on-chain compliance framework

-

Service ecosystem built around tokenized assets

-

Deep and sustainable liquidity ensuring real purchasing power

The RWA market is still in its early stages. Platforms that deliver superior solutions—meeting institutional needs while unlocking new value within the tokenized economy—will replace Ethereum as the dominant force.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News