GENIUS Act and Stablecoins: A New Investment Frontier Under Regulation

TechFlow Selected TechFlow Selected

GENIUS Act and Stablecoins: A New Investment Frontier Under Regulation

In the near future, USDT and/or USDC are expected to top the list of U.S. Treasury holders.

Author: James Lavish

Translation: Baihua Blockchain

There is now a growing chorus claiming that "stablecoins are the future of crypto assets."

This includes voices from U.S. Treasury officials, and even possibly central bankers.

But what exactly are stablecoins? Why are they so important? And what problems do they solve for investors and the U.S. Treasury?

Explaining Stablecoins in Plain Terms

In simple terms, a stablecoin is a digital asset (cryptocurrency) designed to maintain price stability.

How is this achieved?

By pegging its price to a reference asset—such as fiat currency, commodities like gold, or even a basket of assets.

The goal of stablecoin issuers is to combine the transactional advantages of cryptocurrency—fast settlement, programmability, global accessibility—with the "price stability" of fiat money.

Before we go further, let’s look at the main types of stablecoins available today:

-

Fiat-collateralized stablecoins: Aim to maintain a 1:1 peg with a national currency such as the U.S. dollar; common examples include USDT (Tether) and USDC (USD Coin).

-

Commodity-backed stablecoins: Pegged to physical assets such as gold (e.g., PAXG, backed by physical gold reserves).

-

Crypto-collateralized stablecoins: Backed by volatile cryptocurrencies as collateral, using over-collateralization to manage price fluctuations.

-

Algorithmic stablecoins: Maintain their peg through supply-and-demand algorithms rather than actual physical reserves. (For example, TerraUSD (UST), which collapsed in 2022, was a classic failure case of an algorithmic stablecoin.)

Today, we’ll focus on dollar-pegged stablecoins and the actions taken around them by the U.S. Treasury and federal regulators.

Dollar-pegged stablecoins primarily serve as digital cash on crypto exchanges and within the broader crypto ecosystem. They play a critical role in trading, lending, decentralized finance (DeFi) applications, and cross-border payments.

Stablecoins like USDT and USDC are used by traders to move funds between exchanges or hold value during periods of market uncertainty.

Unlike traditional banks—which face constraints from operating hours, liquidity limits, and regulatory challenges—dollar stablecoins offer real-time settlement, global accessibility, and integration with smart contracts.

This makes them nearly indispensable in the 24/7 crypto markets.

But how reliable are they?

This leads us to audits—used to verify the underlying assets backing stablecoins.

Circle publicly discloses attestation reports confirming that each USDC token is backed 1:1 by liquid U.S. dollar assets, including cash and short-term U.S. Treasuries. USDC undergoes monthly audits by Grant Thornton LLP, setting a gold standard for transparency in the stablecoin space.

Tether (USDT), however, has faced criticism for lack of transparency and past inconsistencies. Although it now issues quarterly attestations and promises full audits, its reserves include less liquid assets such as commercial paper. In 2021, Tether was fined $41 million by the U.S. Commodity Futures Trading Commission (CFTC) for misrepresenting its reserve holdings. Despite this, USDT remains the most traded stablecoin globally—though with slightly higher reputational risk.

So what happens when investors grow concerned about a stablecoin’s underlying assets and stability?

The stablecoin can “de-peg,” meaning it deviates from its intended parity with the pegged currency.

For example, when Silicon Valley Bank collapsed, USDC dropped from $1 (its par value with the dollar) to $0.87, as investors worried about Circle’s exposure to the bank.

USDC and the Collapse of Silicon Valley Bank:

-

As of early March 2023, Circle held approximately $40 billion in USDC reserves.

-

About $3.3 billion (roughly 8.25%) was held as cash deposits at Silicon Valley Bank.

-

When SVB failed and was taken over by the U.S. Federal Deposit Insurance Corporation (FDIC), markets feared Circle might not have immediate or full access to these funds.

-

This panic caused USDC to temporarily de-peg, falling to $0.87 on some exchanges, until the U.S. government stepped in to guarantee deposits, after which the peg returned to $1.

For holders, this meant that if you owned $100,000 worth of USDC, its value briefly fell to $87,000 before recovering once government assurances restored confidence.

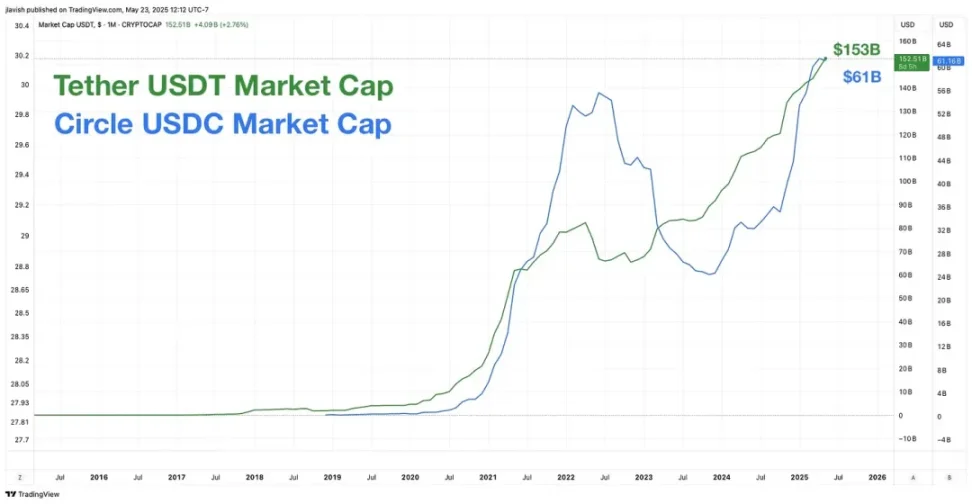

Since then, the stablecoin market has continued to thrive, with both importance and scale growing steadily. The combined market capitalization of USDT and USDC now stands at $214 billion.

This growth has not gone unnoticed. With this expansion, the U.S. Treasury now views dollar-pegged stablecoins as a strategic extension of dollar influence.

In short, the Treasury needs stablecoins.

Why the U.S. Treasury Needs Stablecoins

Simply put, stablecoins promote global use of the dollar, thereby driving demand for U.S. Treasury securities.

Dollar-pegged stablecoins like USDC and USDT act as digital versions of the dollar—accessible anywhere in the world with just a smartphone and internet connection.

This extends the dollar’s reach into regions without robust banking systems.

In effect, stablecoins function as on-chain, permissionless dollars, enabling users worldwide to store value, conduct cross-border transactions, and hedge against local currency risks.

This broad-based demand reinforces the dollar’s status as the world’s primary reserve currency.

Jeremy Allaire, CEO of Circle, once said: "USDC does the job of the dollar overseas better than many banks."

This is beneficial—it helps spread dollar usage globally, even reaching unbanked populations in remote areas.

But how does this help the U.S. Treasury?

The answer is simple.

To maintain a 1:1 peg, stablecoins must be backed by high-quality, liquid assets. For most major issuers, this means holding one specific type of security above all others.

Yes—U.S. Treasuries.

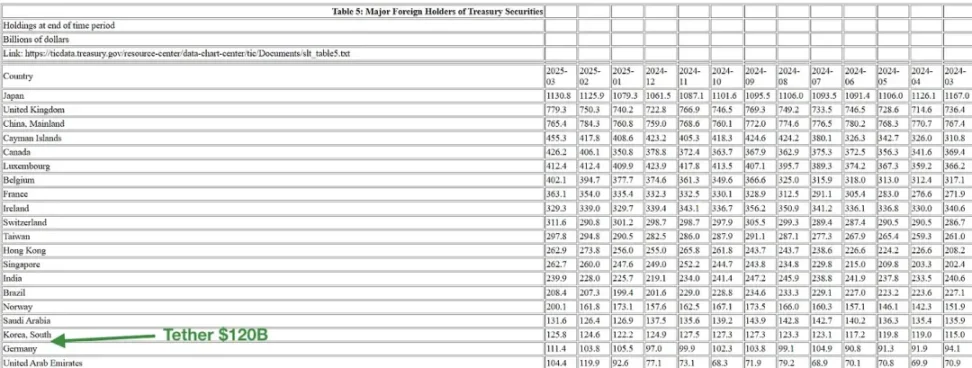

According to a May 1 press release from Tether: "Tether... reached a record high in total U.S. Treasury exposure, approaching $120 billion, including indirect exposure via money market funds and reverse repurchase agreements."

This places Tether among the top holders of U.S. Treasuries:

In fact, Tether holds more Treasuries than Germany or the United Arab Emirates. How did it grow so large so quickly?

Last year, Tether was one of the top ten buyers of U.S. Treasuries, adding $33.1 billion in holdings and ranking as the seventh-largest net buyer—behind only the UK and ahead of Canada.

Don’t forget USDC. Though smaller in market cap, USDC reports that over 75% of its reserves are invested in U.S. government debt with maturities of three months or less (i.e., Treasury bills), with the remainder held as cash in major banks.

The combined demand from these issuers now rivals that of some mid-sized sovereign nations.

In a world of rising deficits and increasing Treasury issuance, this demand is a welcome "lifeline" for Washington.

This new non-sovereign demand for Treasuries is reshaping traditional debt markets:

Stablecoin reserves act as yield-seeking balance sheets, favoring safe assets like short-term Treasuries.

Unlike traditional banks, these issuers are not subject to Basel capital requirements or deposit insurance rules that constrain balance sheet size.

For instance, Tether reported over $13 billion in net profit in 2024—mostly from interest on its Treasury portfolio—with only about 100 employees.

While this demand is crucial for a U.S. Treasury selling massive amounts of debt, it also brings concentration risk and raises questions about transparency, redemption processes, and systemic risk.

We saw this during the USDC and Silicon Valley Bank episode. Although the peg recovered quickly after federal intervention, the event showed how confidence can evaporate rapidly.

A redemption run on USDT or USDC could force the rapid liquidation of tens of billions in Treasuries—rippling through global repo markets and short-term funding instruments.

Thus, regulators—from the Treasury to the Financial Stability Oversight Council—are viewing stablecoins not just as technological and financial innovations, but as emerging systemically important institutions.

By anchoring themselves to U.S. Treasuries, stablecoins have become both buyers and amplifiers of dollar dominance. In the process, they’ve… well, tied up the full weight of U.S. fiscal and regulatory power.

This brings us to the GENIUS Act.

The GENIUS Act: Washington Joins the Conversation

Recognizing that stablecoins are no longer fringe crypto concepts but major players in global liquidity and debt markets, policymakers have stepped in with what they call “responsible innovation.”

This is the GENIUS Act.

Its full name is the Guiding and Ensuring National Innovation for US Stablecoins Act, introduced by Senator Bill Hagerty (R-TN) and Senator Kirsten Gillibrand (D-NY)—a bipartisan legislative proposal.

Key provisions of the bill include:

-

Federal Licensing: Issuers with more than $10 billion in circulation must obtain federal licenses and be subject to oversight.

-

Full Reserves: Stablecoins must be backed 1:1 by high-quality liquid assets such as U.S. Treasuries and cash.

-

Mandatory Audits: Issuers must undergo regular independent audits and disclose reserve data publicly (Tether, take note).

-

Two-Tier Regulation: Smaller issuers with less than $10 billion in circulation can operate under state-level regulation, keeping the ecosystem open for startups.

-

CBDC Alternative: The bill explicitly supports private-sector dollar stablecoins as an alternative to a central bank digital currency (CBDC).

What is the current legislative status of the GENIUS Act?

The GENIUS Act passed the U.S. Senate last week (May 19) by a bipartisan vote of 66 to 32. But of course, not everyone supports it.

Senator Elizabeth Warren has emerged as one of its strongest and harshest critics, warning that the GENIUS Act may lack sufficient consumer protections and could excessively benefit private crypto interests.

Warren has long argued that if the U.S. is to issue a digital dollar, it should be issued and controlled by the public sector—possibly as a central bank digital currency (CBDC)—to better ensure consumer protection, financial stability, and minimal environmental impact.

However, a CBDC would give governments and banks absolute surveillance and control over every dollar you own, down to individual transactions.

It could even allow authorities to deny any or all transactions, or freeze and confiscate your entire balance.

Regardless, I believe a CBDC is unlikely to be created or adopted in the U.S. in the near term.

Back to the GENIUS Act.

The bill now moves to the House of Representatives. While it enjoyed strong bipartisan support in the Senate, its path in the House appears more complex.

Some House Republicans have proposed competing versions of stablecoin legislation, with key disagreements over state versus federal regulatory authority, the role of the Federal Reserve, and the division of control between federal and state agencies.

Meanwhile, some House Democrats align with Senator Warren, arguing the bill favors crypto insiders and lacks adequate consumer safeguards against abuse or systemic risk.

Therefore, while the GENIUS Act has significant momentum, it is far from finalized. More debate, negotiation, and likely amendments are expected before it reaches the President’s desk.

Washington is essentially saying: Fine, stablecoins are here to stay—and we desperately need them to support unlimited future U.S. Treasury issuance—but we will ensure they are safe, sound, and properly structured.

Summary

Either way, I believe stablecoins are here to stay, the GENIUS Act will eventually be signed into law, and it will provide structure for stablecoins—further cementing their position on the U.S. Treasury holdings leaderboard.

I expect that in the not-too-distant future, USDT and/or USDC will top that list—as the world’s largest holder of U.S. Treasuries.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News