Web3 Payment In-Depth Report: 2025, Stablecoins in Africa

TechFlow Selected TechFlow Selected

Web3 Payment In-Depth Report: 2025, Stablecoins in Africa

Everyone sees a different facet, but all point to the same future.

Author: Will Awang

Preface

The World Is Flat

Our world has transformed from isolated local economies into a tightly interconnected global system through the internet’s worldwide connectivity, leading Thomas L. Friedman to declare "the world is flat." While the internet has made information flow free and global, the infrastructure supporting financial flows still largely relies on pre-internet frameworks, making the transfer of funds/value still difficult and expensive.

Although some regional financial innovations have accelerated capital movement, Africa's financial rails have not kept pace. Traditional finance has failed to provide stability, accessibility, and efficiency, exposing people to inflation and financial uncertainty, limiting their control over savings, and making it hard to access global markets. But just as the region leapfrogged the desktop era and moved directly into mobile, Africa is now poised to leapfrog outdated banking infrastructure and actively embrace stablecoins.

We can no longer limit our view to stablecoin use cases in native crypto markets; we must adopt a new perspective on real-world applications of stablecoins outside crypto-native contexts. Stablecoins have become a key part of the crypto narrative in sub-Saharan Africa, serving as a popular hedge against long-term inflation and currency depreciation.

"Stablecoins on blockchain networks are an answer. Stablecoins represent our first real chance to transform money the way email transformed communication: making it open, instant, and borderless. This is a WhatsApp moment for money/value—a global network built on blockchain and stablecoins that benefits everyone."

—— Chris Dixon

I. Africa’s Quiet Stablecoin Revolution

Africa leads the world in mobile money penetration and adoption, demonstrating strong demand for alternative financial solutions. The emergence of stablecoins is therefore natural, offering seamless access to financial services with just a smartphone. Stablecoins can build on this foundation to expand financial inclusion and enable more efficient borderless transactions.

According to Chainalysis data, Africa is the fastest-growing region in cryptocurrency adoption, with year-on-year growth of 45% from 2022–2023 to 2023–2024, outpacing emerging markets like Latin America at 42.5%. This rapid growth highlights the immense potential for stablecoin adoption, especially in Africa where bank penetration remains among the lowest globally.

"Stablecoins are already a reality in cross-border payments across Africa... the rest of the world is just catching up."

—— Zekarias Amsalu, Co-Founder of Africa Fintech Summit

One of the main drivers behind stablecoin adoption in Africa is the foreign exchange (FX) crisis faced by many countries. About 70% of African nations face FX shortages, making it difficult for businesses to access U.S. dollars needed for operations. In countries like Nigeria, where the local currency, the Naira (NGN), has sharply depreciated, stablecoins offer a much-needed alternative. "Banks don’t have dollars, the government doesn’t have dollars, and even if they did, they wouldn’t give them to you."

—— Chris Maurice, CEO & Co-founder of Yellow Card

Over the past three years, stablecoins have become an indispensable part of Africa’s financial system, providing a reliable means of value storage, cross-border remittances, and trade without relying on highly volatile and unstable local currencies. Dollar-backed stablecoins like USDT and USDC are filling gaps in traditional finance, enabling people in dollar-scarce economies to access stable value storage.

From remittances and retail savings to B2B trade and cross-border payments, stablecoins are addressing critical issues in Africa—Dollar Access, Instant Settlement, and FX Inefficiencies—problems particularly acute in markets underserved by traditional payment channels.

Africa is one of the most dynamic growth markets globally, with the fastest population growth, youngest median age, and nine of the twenty fastest-growing economies. With 400 million mobile payment users, digital finance is already widespread. Stablecoins represent the next leap forward—turning smartphones into globally connected dollar accounts. Looking ahead, in ten years, more Africans will likely conduct daily transactions using crypto wallets and stablecoins rather than traditional bank accounts.

"You don’t need to educate users—life forces them to use it."

—— Sky, Co-founder of ROZO

II. Projects Driving Future Stablecoin Adoption

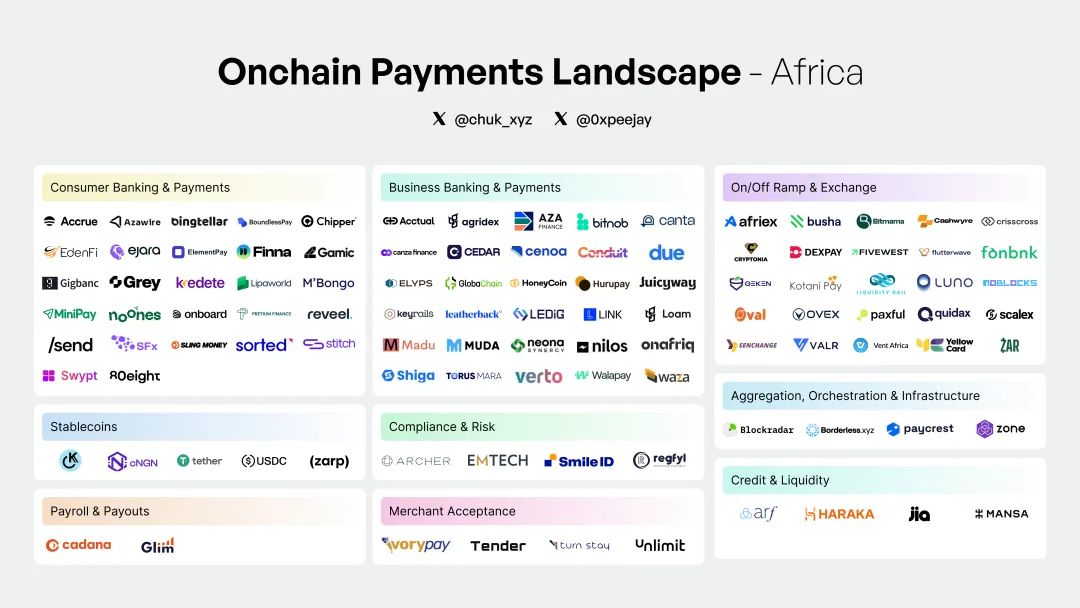

Chuk from Paxos created an ecosystem map covering payment channels, use cases, and companies to illustrate the depth of this transformation. While many market maps depict the global stablecoin ecosystem, few focus on Africa’s role in shaping its financial future. Hence, we present this map to highlight the builders and use cases redefining Africa’s financial infrastructure.

(Mobile Money to Global Money: Africa’s Stablecoin Revolution, Chuk @ Paxos)

In our investment activities across African markets over the past three years, we’ve seen increasing numbers of companies building around stablecoins, each playing a crucial role in driving adoption and innovation. Below are some of the most notable players, along with key growth and funding metrics highlighting the sector’s rapid expansion.

-

Yellow Card: One of Africa’s leading crypto asset exchanges, operating in 20 countries across the continent. It is Africa’s largest and first licensed stablecoin on/off-ramp. Yellow Card enables seamless fiat-to-crypto and crypto-to-fiat conversions. In 2024, the platform doubled its annual transaction volume from $1.5 billion in 2023 to $3 billion.

-

Conduit: Provides stablecoin payment services for importers and exporters in Africa and Latin America. Its annualized TPV is projected to surge from $5 billion in 2023 to $10 billion in 2024.

-

Juicyway: A Lagos-based startup leveraging stablecoins for cross-border payments. Since 2021, Juicyway has processed a total of $1.3 billion in payments.

-

Bridge: Founded in 2022 and acquired by Stripe two years later for $1.1 billion. Bridge strengthened global stablecoin payment infrastructure, serving most African payment companies and facilitating stablecoin payments across Europe, the U.S., and Asia.

-

Jia: A blockchain-based fintech company providing loans to SMEs in emerging markets. In 2024, Jia disbursed over $10 million in cumulative loans, up from $2 million the previous year, with an internal rate of return (IRR) of 24% and a default rate of 0.14%.

-

Onboard: A global P2P trading protocol allowing anyone, anywhere, to access on-chain finance. Nestcoin raised $1.9 million in its latest round to scale its product.

-

KotaniPay: Offers stablecoin settlement solutions for businesses and individuals. KotaniPay is developing an API product connecting blockchains with local payment channels. In 2023, it secured $2 million in seed funding.

-

Accrue: Building a dollar stablecoin agent network to expand cross-border payment infrastructure. Raised $1.58 million in seed funding to scale operations.

-

Convexity: Developed Nigeria’s first regulated stablecoin, cNGN. The company has collaborated with the Central Bank of Nigeria since 2021 and received an interim license from the Nigerian Securities and Exchange Commission (SEC) in 2024.

-

Honeycoin: A platform for cross-border remittances, bill payments, airtime purchases, and online spending. GTV surged from $40 million last quarter to $500 million in Q4 2024.

-

Paycrest: A decentralized liquidity protocol enabling instant, low-cost payments backed by stablecoins. They also developed Zap, a DApp for seamless crypto-fiat payments, which won the Base 2024 Global Onchain Summer Buildathon. Zap is now production-ready as Noblocks—the first interface enabling instant decentralized payments between any bank or mobile wallet, powered by a distributed network of liquidity nodes.

-

Haraka: A stablecoin-powered microcredit protocol targeting underserved entrepreneurs in emerging markets. Haraka uses a reputation-based credit scoring system and has shown early commercial validation through partnerships with Grameen Foundation and Mercy Corps.

Many of these companies have experienced significant growth over the past two years and are at the forefront of stablecoin innovation in Africa.

For the global fintech community, the question isn't whether stablecoins will go mainstream—it's what we can learn from where they already are: Africa.

III. Stablecoins Are Solving Africa’s Everyday Problems

"In Africa, it's not about choosing between stablecoins and other financial tools. It's stablecoins—or nothing." — Samora Kariuki, Frontier Fintech

Across Africa, stablecoins are solving real problems. From asset preservation to trade facilitation, adoption is driven by necessity, not speculation. Below are the most critical use cases based on actual needs, along with the companies building solutions to support them.

3.1 Daily Tools: Savings, Spending, and Credit

In many African countries, high inflation, currency depreciation, and limited access to banking make financial security extremely difficult. Stablecoins offer a more reliable path—as dollar-denominated tools for saving, transacting, and accessing credit.

A. Asset Preservation

In regions where dollar banking is inaccessible, inflation is high, and legacy payment networks are costly or unreliable, stablecoins are increasingly favored. Africa exemplifies these conditions, making stablecoins a vital tool for protecting savings and maintaining purchasing power, especially in economies with rapidly depreciating local currencies.

Currency depreciation is one of Africa’s biggest financial challenges. Take the Kenyan Shilling: while Kenya’s GDP tripled between 2008 and 2024, its exchange rate against the dollar has depreciated by 50% since 2021. The contradiction is clear: economic growth is rising, but confidence in the local currency isn’t. Similarly, over the past 18 months, inflation and naira depreciation have been key drivers of stablecoin adoption in Nigeria. The naira hit an all-time low in February 2024 and has struggled since, further highlighting demand for stable alternatives.

(Stablecoins: Leapfrogging Africa’s Financial System, Ayush Ghiya and Uchenna Edeoga)

As local currencies continue to lose value, stablecoins are becoming the preferred hedge, offering a more reliable way to store and transfer wealth. Unlike cash or gold, stablecoins are fully digital and widely accessible, requiring no reliance on banks, payment networks, or central banks. They not only hedge against currency volatility but also offer higher yields than traditional savings accounts—an attractive option for Africans seeking to preserve and grow wealth. While traditional banks offer low interest rates, stablecoin savings platforms leverage decentralized finance (DeFi) and crypto lending models to generate higher returns for users.

Currently, dollar-backed stablecoins are the top choice for users in emerging markets. Across much of Africa, USDT (on Tron) has become the de facto digital dollar. Most users acquire stablecoins through centralized custodial apps like Binance, prioritizing speed and liquidity over Western concerns about reserves or transparency.

For users facing FX rationing and 30% inflation, functionality matters most. Stablecoins help users preserve assets in remote areas and save in stable currencies. World Bank data shows that as of 2021, only 49% of Africans had bank accounts, yet 400 million use mobile payments—stablecoins can meet user needs where banks cannot reach.

Platforms like Fonbnk enable instant recharge to USDT conversion even on basic phones, while Accrue provides a local community agent network for cash-in and cash-out of stablecoins. Nigeria’s crypto platform Busha Earn allows users to save stablecoins at yields up to 7.5% annually—far exceeding most Nigerian bank rates. Sub-Saharan Africa leads the world in DeFi application usage, likely due to growing demand for accessible financial services. This suggests stablecoins are not just an alternative—they’re essential for financial stability in regions where traditional systems fail.

This makes stablecoin savings highly attractive—not just for higher interest, but because users earn yield on top of the value gained from hedging currency depreciation. Together, these factors make stablecoins powerful tools for wealth preservation and growth.

"By converting everyday prepaid payments—mobile data, bank transfers, and mobile money—into USDT, Fonbnk acts as a stablecoin settlement layer, offering 400 million unbanked and underbanked Africans a hedge against currency depreciation and opening new paths to savings and credit beyond traditional banking." — Chris Duffus, Founder & CEO, Fonbnk

B. Expanding Credit Access

Africa faces a $330 billion credit gap for MSMEs, with lack of banking services leading to underdeveloped credit ecosystems. Millions of individuals and small businesses are excluded from traditional banking. In these markets, small enterprises are often overlooked by traditional institutions due to high collateral requirements, lengthy documentation, and lack of credit history. Without access to affordable upfront capital, many MSMEs turn to informal lenders. Lack of affordable credit limits their ability to sustain operations and contribute to economic growth.

In Web3, stablecoin-based lending protocols have shown great potential in addressing this issue over the past three years. However, most such solutions still require excessive collateral—around 150% in crypto assets—effectively excluding MSMEs in emerging markets. While low-collateral lending protocols like Goldfinch have emerged, they primarily serve as alternative debt providers for fintech lenders, not direct financing for physical small businesses.

Recently, two companies—Jia (offering factoring, supply chain financing, and other loans via DeFi) and Haraka (using an innovative social credit system)—are actively disrupting this space and capturing Africa’s market opportunity. These firms provide blockchain-based loans to small businesses, empowering responsible borrowers with ownership, enabling wealth creation and driving local economic development.

Bringing real-world economic activity on-chain benefits both investors and borrowers. Investors gain democratized access to real yields, while borrowers access blockchain liquidity and treat ownership as a way to create long-term wealth for themselves and their communities. Blockchain also reduces the high transaction costs common in private credit markets (often passed to borrowers) and allows borrowers to build on-chain credit histories, establishing reputations over time.

These tools give users greater control over their finances and unlock previously inaccessible financial options.

3.2 Cross-Border Flows: Trade, Treasury, and Remittances

As Stripe CEO Patrick Collison said, stablecoins are “room-temperature superconductors for financial services.” They allow businesses to pursue opportunities previously hindered by the cost and friction of existing payment channels or traditional gatekeepers. This is especially evident in cross-border payments, where legacy systems are slow, expensive, and rely on multiple intermediaries. High fees and long delays complicate transactions—particularly in Africa, where average remittance costs are around 8%, and financial infrastructure is often limited or absent.

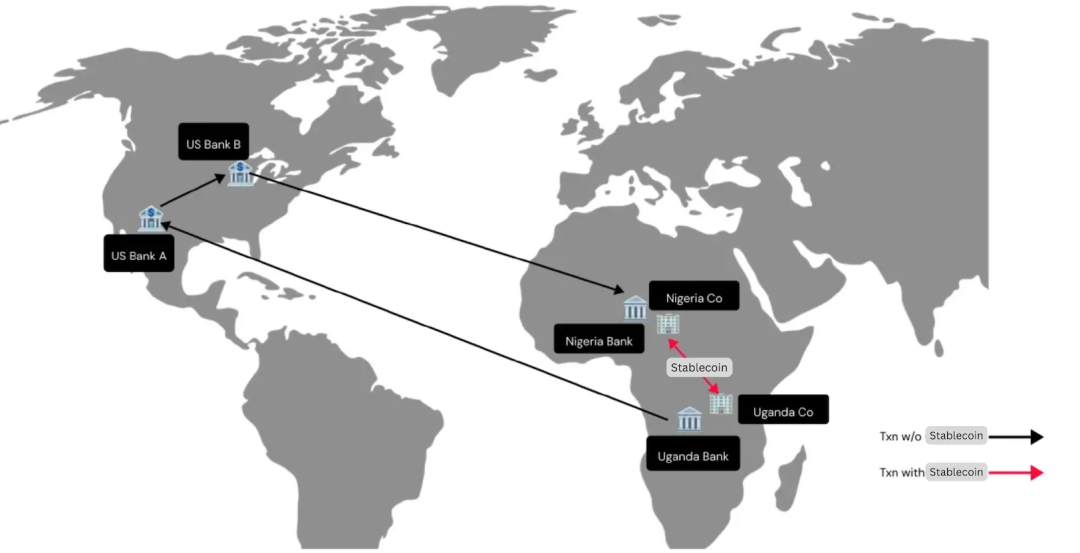

Cross-border payments are foundational to Africa’s daily economy—from importing goods and sending remittances to repatriating profits and paying freelancers. Yet, the payment channels supporting these flows remain fragile: delays of 3–5 days, fees of 5–10%, and constraints from FX rationing. Stablecoins change this by offering a solution—enabling real-time, low-cost transfers without large capital reserves or bank intermediaries.

(Stablecoins: Leapfrogging Africa’s Financial System, Ayush Ghiya and Uchenna Edeoga)

Consider the scenario above: a Ugandan user wants to send funds to someone in Nigeria. Using SWIFT, due to lack of direct banking links, the transfer may route through an intermediary bank in the U.S. But with a stablecoin payment network, the user can convert local currency to stablecoins, send them directly to the Nigerian recipient, who then converts them into Naira and accesses funds locally.

This process eliminates inefficiencies of SWIFT and net-settlement models, as transfers occur directly via exchanges or blockchain wallets connected to currency on/off-ramp service providers. These providers integrate with local payment systems, enabling seamless conversion between stablecoins and local currencies.

Recently, Stripe acquired Bridge—a stablecoin API provider—for $1.1 billion, just two years after its 2022 founding—to enhance its global stablecoin payment network. Africa is Bridge’s primary market, providing stablecoin payment services for most African payment companies operating in Europe, the U.S., and Asia. This underscores growing market demand for stablecoin infrastructure and the rapid expansion of key players in the space.

While Bridge laid the groundwork for stablecoin orchestration and issuance, much work remains in this sub-sector. Cross-border payments remain a massive opportunity, but several key challenges persist.

A. Trade and B2B Payments

China is Africa’s largest trading partner, with African imports from China reaching $176 billion in 2023, resulting in a $66.6 billion trade deficit. This creates sustained demand for dollar payments, which stablecoins fulfill efficiently and with high liquidity. Due to deep liquidity and broad exchange support, USDT (on Tron) has become the preferred channel for many commercial payments.

"Stablecoins are the new backbone of cross-border payments in Africa. Businesses using Conduit can settle payments nearly instantly, reduce working capital needs, maintain liquidity, and avoid currency fluctuations." — Eric Wainaina, General Manager, Africa at Conduit

"Stablecoins have completely changed the game for importers who couldn’t access dollars through banks—now their businesses are thriving." — Suleiman Murunga, Director, MUDA

Intra-African trade payments: Intra-African trade accounts for only 15% of the continent’s total imports and exports, far below North America’s 54%, Asia’s 60%, and the EU’s 70%. A major cause is the lack of direct currency exchange infrastructure—most transactions require converting local currencies into USD, GBP, or EUR before switching to another African currency. This inefficiency adds $5 billion in unnecessary costs annually to intra-African trade. Solving this is crucial for smooth trade across the continent.

Profit repatriation: Large multinational companies selling goods and services in Africa can use stablecoins to bring funds back home. With stablecoin infrastructure, settlements take under 30 minutes, versus 2–3 days with traditional methods.

B. Remittances and Global Payments

Just as stablecoins facilitate outbound payments, they also bring money into Africa—covering remittances, salaries, and freelancer income.

Remittances are one of the most common cross-border payment needs, yet traditional remittance methods are costly. In 2023, global remittance flows reached $883 billion, with fees disproportionately affecting low-income users. Today, sending $200 from the U.S. to Nigeria via stablecoins costs less than $0.01, compared to $7.60 via traditional methods. Massively reducing these costs remains a priority.

"Sub-Saharan Africa remains the most expensive region globally for remittances, with average costs hitting 8.37% in 2024. Yet, many overseas Africans don’t know they can now send money home faster and cheaper using stablecoins." — Xino Zee, Lead at Send Africa

Payments: For gig economy freelancers, cross-border micropayments remain costly and inefficient. In places like Kenya, some even 'rent' PayPal accounts because setting up their own is too difficult—highlighting how access barriers compound already high international micropayment costs. Stablecoins can streamline payments, greatly benefiting these workers. Additionally, multinational companies can use stablecoins to manage cash flow efficiently and pay employees, customers, or suppliers globally without friction.

Global aid: Currently, only about 40 cents of every dollar donated to global aid organizations reaches beneficiaries, with the rest going to multiple intermediaries. A more efficient, low-cost system is clearly needed to deliver aid transparently and seamlessly.

A new wave of companies is rebuilding Africa’s cross-border payment infrastructure around stablecoins. Exchanges like Yellow Card, Busha, VALR, and Luno provide liquidity for local fiat on/off-ramps. Conduit, Honeycoin, Shiga Digital, and Juicyway support commercial trade, collections, and payments, while Sling and Send drive consumer P2P payments.

These builders have quietly moved billions of dollars collectively. Many don’t sell “stablecoins” directly but sell cheaper remittances, working capital efficiency, and currency stability.

IV. Opportunities for African Builders

"In Africa, you kick a tree and three stablecoin fintech startups fall out... the strongest teams we back now have single-channel or industry-specific liquidity—with stablecoins hidden behind the scenes." — Brenton Naicker, Principal & Head of Growth (Africa) at CV VC

4.1 Four Levers for Value Creation

The first wave of stablecoin growth focused on infrastructure: on/off-ramps, channel liquidity, and basic wallet functions. This layer is rapidly becoming crowded. The next phase is differentiation—who owns the users, who defines standards, and who captures profits in real-world use cases. Below are four levers shaping value creation across Africa:

A. Distribution: Winning Users

Control over user interface and customer relationships determines where transaction volume flows. The strongest companies don’t lead with stablecoin infrastructure but solve payment, lending, or treasury problems, hiding stablecoins behind the scenes.

B. Liquidity: Controlling Both Ends of the Channel

Local FX liquidity is uneven and hard to replicate. Teams that manage liquidity at origin and destination points can offer better pricing, internal netting, and lower fees. Liquidity compounds, creating a defensive moat.

C. Regulation: Shaping Rules Before They’re Set

In competitive markets like Nigeria and Kenya, flawless execution is critical. But in less-developed markets like Malawi or Cape Verde, first-movers face less competition and can collaborate with regulators to define the rules. Early trust-builders may secure long-term policy alignment.

"Dollar liquidity across much of Africa is already on-chain via stablecoins. Policymakers should prioritize large-scale on-chain deployment of local currencies to accelerate economic sovereignty and trade." — Wale Ayeni, Managing Partner of Helios Digital Ventures

D. Verticalization: Tailoring for Specific Workflows

Every sector—agriculture (e.g., Agridex), logistics, education, or global aid—has unique workflows, user expectations, compliance needs, and payment rhythms. Specialized builders speak the jargon, integrate with existing tools, and solve problems generalists can’t. Once trusted, they can layer on additional financial services like credit, treasury, or insurance. Focus brings stickiness and profitability.

4.2 Africa’s Major Crypto Economies

(State of Crypto Report 2024: New data on swing states, stablecoins, AI, builder energy, and more)

A. Nigeria—The Epicenter of African Crypto Activity

Driven by a booming fintech industry and severe economic challenges, Nigeria—the most populous country in Africa—leads in stablecoin adoption. In recent years, Nigeria’s economy has faced multiple shocks: low oil prices (a key driver of exports), compounded by the pandemic and supply chain disruptions, leading to prolonged financial uncertainty. Nigeria suffers from some of the highest inflation rates in Africa, even exceeding Francophone regions. As the Naira continues to depreciate, stablecoins have become essential tools for Nigerians seeking wealth preservation and global transactions.

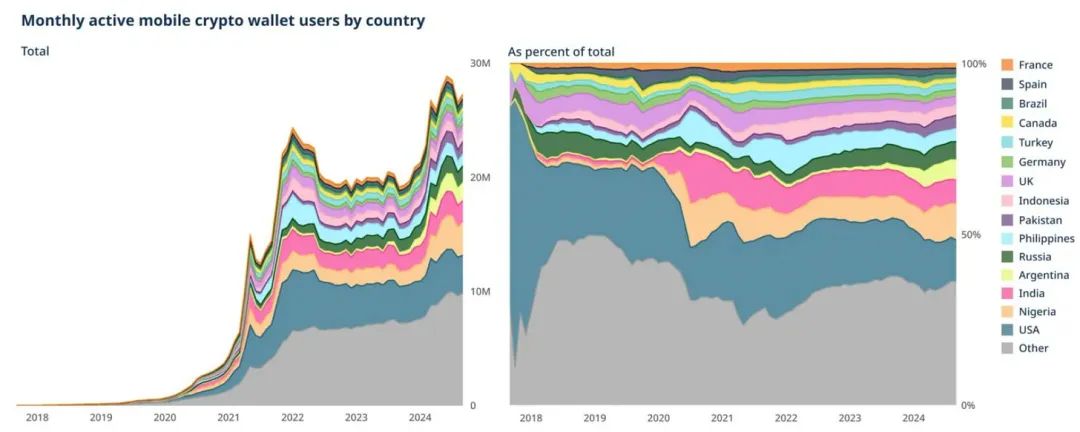

In Chainalysis’ Global Crypto Adoption Index, Nigeria ranks second overall. Between July 2023 and June 2024, the country received approximately $59 billion worth of cryptocurrency. Nigeria is also a leading market for mobile crypto wallet adoption, second only to the U.S. The country is actively pursuing regulatory clarity, including through incubation programs, and stablecoin usage in everyday transactions—such as bill payments and retail purchases—is growing significantly.

(Sub-Saharan Africa: Nigeria Takes #2 Spot in Global Adoption, South Africa Grows Crypto-TradFi Nexus, Chainalysis)

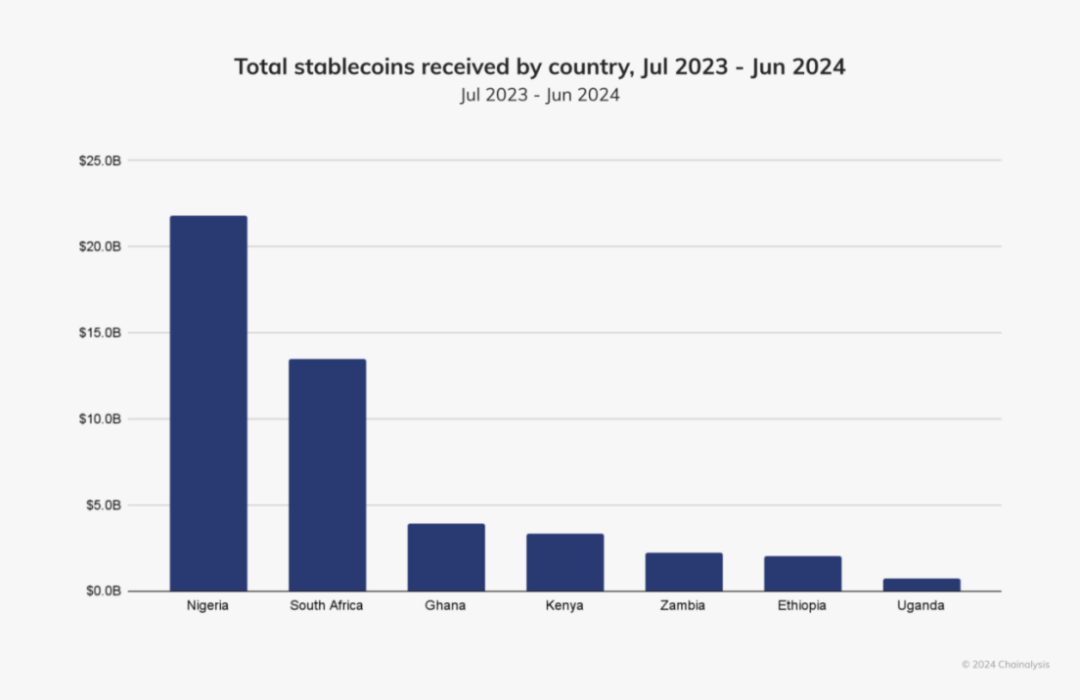

Alongside Ethiopia, Ghana, and South Africa, stablecoins are a core component of Nigeria’s crypto economy, accounting for about 40% of all stablecoin inflows in the region—the highest in sub-Saharan Africa. Nigerian users report high transaction frequency and a deep understanding of stablecoins as financial tools, not just asset classes.

Nigeria’s crypto activity is primarily driven by small retail and professional-scale transactions, with about 85% of transfers valued below $1 million. With traditional remittance channels being inefficient and costly, many Nigerians rely on stablecoins for cross-border remittances. Sodipo notes: "Cross-border remittances are the primary use case for stablecoins in Nigeria. It’s faster and more affordable."

"Daily activities like bill payments, mobile top-ups, and retail shopping are increasingly powered by cryptocurrency. People are beginning to see crypto’s real-world utility, especially in everyday transactions—different from earlier views of crypto as a quick-rich scheme." — Moyo Sodipo, CEO & Co-founder of Busha, a Nigerian cryptocurrency exchange

Beyond traditional finance, DeFi platforms offer Nigerians new opportunities to earn interest, take loans, and participate in decentralized trading. Sodipo says: "DeFi is a key growth area as users explore ways to maximize returns and access financial services they otherwise couldn’t get."

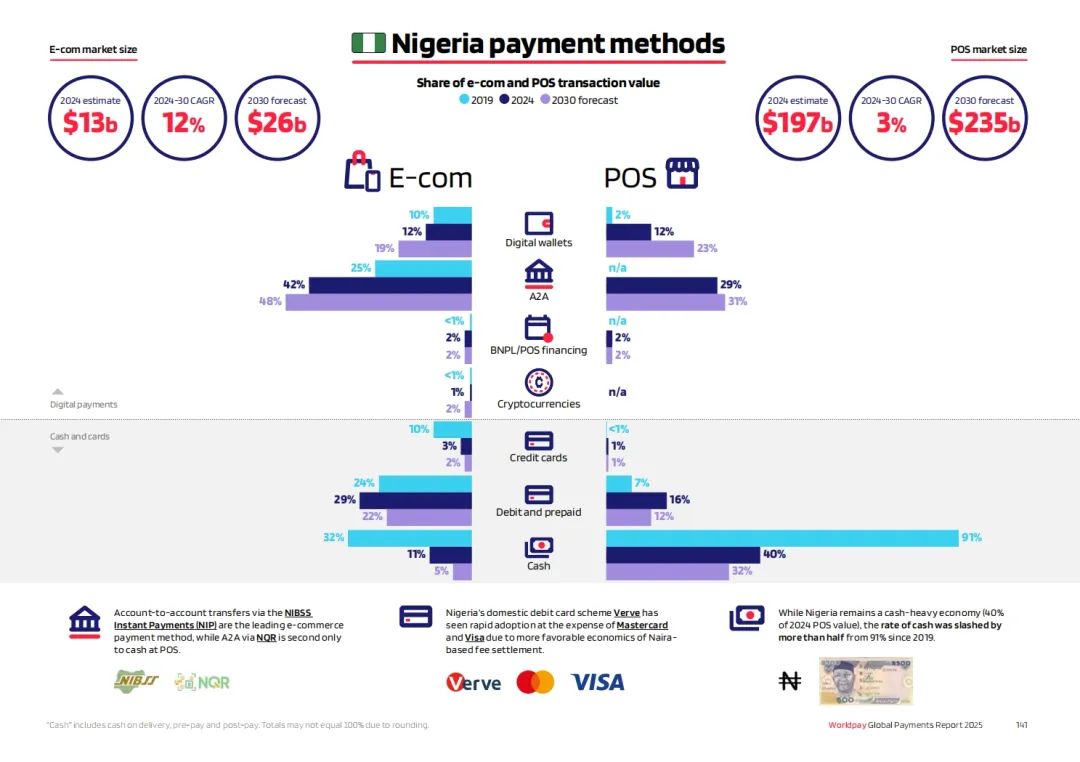

(GPR 2025: the past, present and future of payments, WorldPay)

In the chart above, we see cryptocurrency as a payment method already accounting for 1% of online e-commerce and offline POS transactions in Nigeria, categorized under Digital Payments. Other similar countries in WorldPay’s report include: Argentina, Brazil, India, Nigeria, Philippines, Singapore, Turkey.

Given that inflation, remittances, and financial access are driving stablecoin adoption, it’s expected that usage will be reflected across various scenarios. Nigeria has become the ideal testing ground for stablecoins in Africa. Its role in building stablecoin infrastructure will shape the technology’s trajectory across the continent.

In December 2023, the Central Bank of Nigeria lifted its ban on banks servicing crypto companies, a move critical to crypto adoption. "Since the bank ban was lifted, it has opened up many possibilities for collaboration and smoother transactions," explains Sodipo. Building on this, in June 2024, Nigeria’s Securities and Exchange Commission (SEC) launched the Accelerated Regulatory Incubation Program (ARIP), requiring all Virtual Asset Service Providers (VASPs) to register and undergo evaluation before full approval. "The industry is optimistic about ARIP—it marks a shift away from uncertainty and a positive step toward regulatory clarity," says Sodipo.

These policy moves will enable companies across sectors to consider shifting from traditional payment channels to stablecoin infrastructure. While compliant solutions aren’t perfect, every business adopting stablecoins demonstrates to incumbents that they are reliable, secure, compliant, and superior solutions to traditional payment problems.

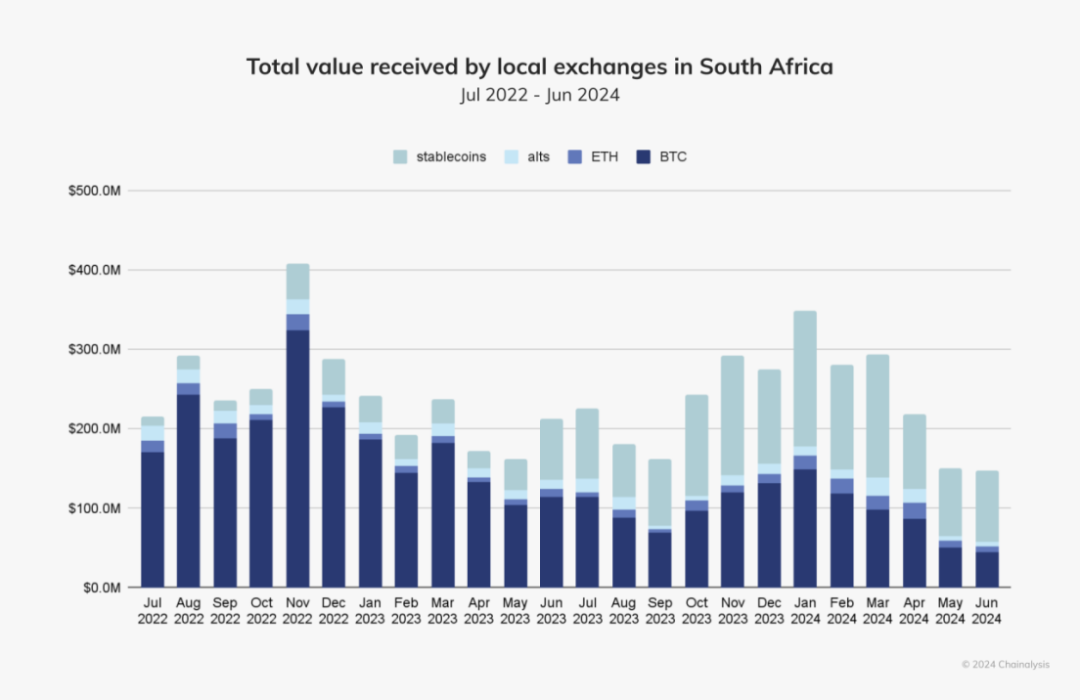

B. South Africa—Market Growth Driven by TradFi Institutional Adoption

As Africa’s largest economy, South Africa has positioned itself as one of the continent’s most advanced Web3 markets, with a mature regulatory framework and strong institutional investor interest. It has become one of Africa’s largest crypto markets, recording $26 billion in trading volume over the past year. Unlike many African countries where crypto adoption is primarily retail-driven, South Africa sees growing institutional participation, with licensed firms and traditional financial institutions entering the space.

Starting in late 2023, stablecoins saw continuous growth on local exchanges in South Africa—growing over 50% month-over-month in October 2023. Stablecoins have replaced Bitcoin as the most popular cryptocurrency in recent months.

(Sub-Saharan Africa: Nigeria Takes #2 Spot in Global Adoption, South Africa Grows Crypto-TradFi Nexus, Chainalysis)

A key driver of crypto growth in South Africa is its clear regulatory stance. The country has classified crypto as a financial product, creating a structured legal environment and providing clarity for businesses and investors. In March 2024, South Africa approved 59 crypto operating licenses, paving the way for broader stablecoin adoption. By setting regulatory guardrails, the government aims to attract investment, protect users from cybercrime, and expand low-cost digital asset trading channels.

The intergovernmental fintech working group is actively refining its approach to stablecoin regulation and plans to formally classify stablecoins as a distinct subset of crypto assets. This aligns with the country’s broader financial modernization and digital payment initiatives, ensuring stablecoins are properly integrated into the financial ecosystem. The 2024 budget review further emphasized the government’s commitment to structural reforms, improved public financial management, and new policies focused on stablecoins and blockchain-based digital payments.

Growing institutional interest has also sparked discussions around bank-issued stablecoins. As traditional institutions explore stablecoin models, South Africa may soon see regulated, bank-backed digital assets, further accelerating mainstream stablecoin adoption. Led by startups like VALR, Luno, and Altify, South Africans are already using stablecoins to diversify investments, make payments, and access financial services more efficiently.

With a developed financial sector, clear regulations, and increasing convergence between crypto and traditional finance, South Africa is emerging as a leader in stablecoin adoption across the continent. As policy frameworks evolve and institutions deepen engagement, South Africa is laying the foundation for stablecoins to play a central role in its evolving digital economy.

C. Kenya—Emerging as East Africa’s Stablecoin Hub

Kenya has long been at the forefront of financial innovation in Africa. From pioneering mobile money to early Web3 adoption, the country consistently bypasses traditional banking in favor of more efficient digital solutions. Today, Kenya is positioning itself as a key player in the stablecoin revolution, leveraging its robust fintech infrastructure, open regulatory environment, and growing demand for alternative financial services.

One of Kenya’s greatest strengths is its deeply rooted mobile money culture. M-Pesa, launched by Safaricom in 2007, has become the backbone of Kenya’s financial system, handling about 60% of the country’s GDP and reaching over 90% of adults. Its success lies in delivering banking without branches, enabling millions of Kenyans to deposit, withdraw, transfer, and even access credit via mobile devices. Stablecoins complement this ecosystem by allowing users to hold value in stable currencies and transact frictionlessly across borders.

Beyond mobile money, Kenya’s regulatory environment has been a key enabler of fintech and Web3 development. Unlike many countries with restrictive stances on digital assets, Kenya’s Capital Markets Authority (CMA) actively promotes innovation through regulatory sandboxes, allowing blockchain-based firms to test and refine their products.

Demand for stablecoins in Kenya stems from limited formal financial services. Small and medium enterprises (SMEs) face significant credit barriers—Kenyan businesses sought around $1.1 billion in loans in 2021 alone. Stablecoin-powered lending solutions can fill this gap, offering cheaper, faster, and more accessible credit to businesses and individuals.

Kenya has also become a global leader in tokenized private credit. According to RWA.xyz, Kenya ranks first globally in tokenized real-world asset lending, with $73.8 million in loans—outpacing larger economies like India and Brazil. This reflects not only strong demand for alternative financing in Kenya but also its ability to integrate blockchain-based credit models into its financial ecosystem.

With a mature mobile money landscape, progressive regulators, and growing stablecoin adoption, Kenya is rapidly emerging as a key stablecoin hub in East Africa. As more fintech companies build stablecoin-based solutions, Kenya’s role in shaping the region’s financial future will continue to grow.

(Nika, photographed in downtown Nairobi, May 2025)

V. Adoption Barriers to Overcome

While we see strong progress by numerous builders in Africa’s ideal testing ground, stablecoin infrastructure still faces structural challenges. To scale further, builders must tackle difficult obstacles—some technical, others political.

5.1 Policy Risk and Regulatory Uncertainty

While major countries have made regulatory progress, most others remain in gray zones. Stablecoins are neither banned nor fully legalized, slowing enterprise adoption and blocking institutional capital.

As transaction volumes grow, enforcement around capital controls, taxation, anti-money laundering, and reporting may increase. Progress here will come through proactive engagement with regulators. Founders, industry associations, and regional sandboxes can help shape the rules.

"Busha is proud to be the first licensed exchange in this market—we are leading this transformation by providing the liquidity, trust, and infrastructure needed to drive a stablecoin-powered economy. This isn’t the future—it’s already here." — Michael Adeyeri, Co-Founder & CEO of Busha

5.2 Monetary Sovereignty

Governments are increasingly concerned that stablecoin wallets are creating a “shadow dollar economy.” Some countries are exploring local alternatives—like ZARP (Zimbabwe’s Digital Asset Reserve Platform) and cNGN (naira-backed stablecoins)—or piloting central bank digital currencies (CBDCs) to retain monetary control.

"The dominance of dollar stablecoins reflects a crisis of trust… Without bold policy innovation and encouragement of regulated, competitive naira-backed stablecoins like cNGN, African nations risk ceding financial control to offshore stablecoin issuers." — Adedeji Owonibi, Founder & COO of Convexity (cNGN Issuer)

5.3 Liquidity Gaps

Fast cross-border payments require capital to be available at the right time, place, and currency. Providers like Wise and Thunes solve this with pre-funded accounts, but with stablecoins, this responsibility shifts to market makers, OTC desks, and other liquidity providers. As volumes grow, capital remains a constraint in each channel.

PayFi companies like MANSA and Arf are filling this gap. By using stablecoins as a transmission layer, they provide real-time liquidity to fintechs, coordinators, and SMEs.

"Real-time, low-cost liquidity doesn’t just make payments faster—it unlocks entirely new models, like just-in-time supplier financing. For founders who’ve built businesses around settlement risk, this is a game-changer.

The next step is embedding this dollar liquidity directly into the apps and tools emerging market businesses already use, so value can flow as easily as a WhatsApp message." — Mouloukou Sanoh, CEO & Co-Founder, MANSA

5.4 Fraud, Scams, and Consumer Trust

Crypto adoption brings new risks—from phishing scams and fake wallets to poorly secured apps. These vulnerabilities erode user trust, especially among newcomers. Security responsibility falls on consumer-facing apps. Trusted design, risk tools, and education must be core to the product.

"Users are the biggest victims of malicious actors. Users will only keep using and recommending platforms they believe are safe." — Zach Bijesse, CEO & Co-Founder at Archer

5.5 Awareness and Education

Outside crypto-native circles, many merchants and agents still find stablecoins hard to understand. Continued “last-mile” adoption depends on ease of use, training, and demonstrating real value.

"In many rural and even urban communities, awareness of crypto remains low because it seems too technical." — Xino Zee, Lead at Send Africa

These barriers are real—but they are being overcome daily. Successful teams don’t wait for perfect conditions; they build resilience, earn trust, and adapt across channels and communities as regulation evolves.

VI. Stablecoins Are Redefining African Finance

Stablecoins are fundamentally reshaping financial landscapes in emerging markets by offering convenient, efficient, and reliable alternatives to traditional banking. Unlike Western economies where adoption is institutionally driven, Africa hasn’t waited for global consensus on stablecoins—it has started building. Emerging markets like sub-Saharan Africa are experiencing grassroots growth in small-value transfers, remittances, P2P payments, and value storage driven by retail users. At the same time, practical applications are unfolding through fintech companies in remittances, trade, credit, and savings.

Recent years have proven that stablecoins are not just an alternative—they are the inevitable future of money in Africa. They bypass broken financial rails, offer stable value, and enable instant, low-cost transactions, making them essential tools for individuals, businesses, and institutions alike. As more infrastructure is built and regulatory clarity improves, stablecoins will become even more deeply embedded in Africa’s financial system.

This is the prototype of programmable money’s future. This is a region worth learning from, building in, and investing in.

We are producing a documentary series to tell these stories—the human stories of stablecoin use in the last mile—because to fully realize the potential of stablecoins, we need to better understand the conditions driving their adoption and continue advancing it in markets where product-market fit has already been achieved. — Justin Norman, Founder of The Flip

He emphasizes that to understand stablecoin adoption in Africa, we must see the people in the “last mile,” not just the technology.

Africa’s demographics are in place, demand is clear, and as global regulation gradually matures, this momentum will only accelerate. Stablecoins are no longer just a buzzword in crypto markets—they are a system-level transformation decoupling from traditional finance and reconstructing it on-chain.

Different people see different facets, but they all point to the same future—a world that doesn’t need banks, but where everyone can “have banking.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News