If BTC drops significantly, will MicroStrategy face a blow-up?

TechFlow Selected TechFlow Selected

If BTC drops significantly, will MicroStrategy face a blow-up?

Unless BTC falls below $50,000 and remains there for more than six months, the likelihood of a large-scale sell-off is less than 20%.

Author: Liu Jiaolian

As BTC fails to rebound and dips again toward 75k, rumors have quietly spread in the community about whether MicroStrategy (now renamed Strategy), the prominent corporate accumulator that aggressively bought and leveraged its BTC holdings during the $100K highs months ago, might face liquidation of its position—potentially triggering a massive flood-like sell-off of BTC. As mentioned in today's April 9 issue of *Jiaolian Insider*, titled "Tariff Clouds Looming, Crypto Continues to Plunge," some observers pointed out that according to its Form 8-K filing with the U.S. SEC, MicroStrategy is not as "never sell" as claimed by its CEO Michael Saylor, but rather may potentially sell its BTC holdings if financial difficulties arise.

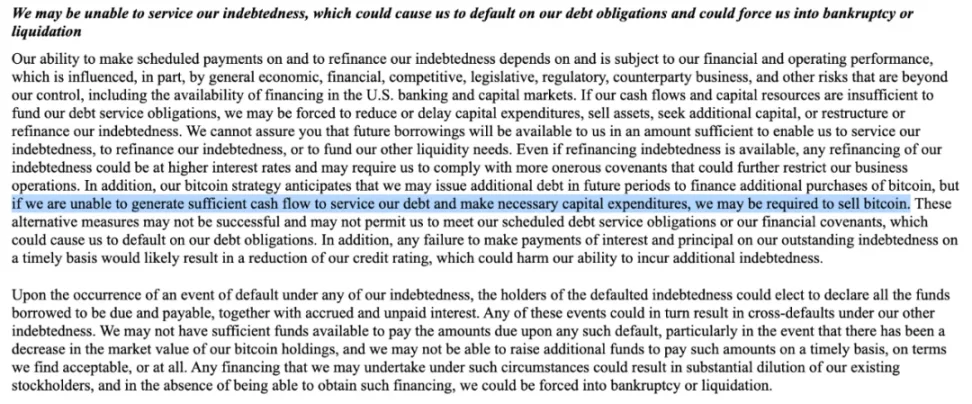

Jiaolian reviewed the original text in the 8-K form, which states: “If we are unable to generate sufficient cash flow to service our debt and make necessary capital expenditures, we may be required to sell bitcoin.”

This merely points to a theoretical possibility. Let’s now examine the full context:

"We may be unable to repay our debts, which could result in our failure to meet repayment obligations and even force us into bankruptcy proceedings.

Our ability to repay principal and interest on schedule and refinance debt depends on and is limited by our company’s financial and operational conditions. These conditions are partially affected by uncontrollable factors such as macroeconomic environment, financial market volatility, industry competition, changes in laws and regulations, and counterparty business risks—including the availability of financing channels within the U.S. banking system and capital markets. If cash flows and capital reserves are insufficient to cover debt payments, we may be forced to take measures including: reducing or postponing capital expenditures, selling assets, seeking new financing, or restructuring or refinancing existing debt. We cannot guarantee that we will be able to obtain adequate future financing to repay debt, refinance debt, or meet other liquidity needs. Even if refinancing is obtained, new debt may carry higher interest rates and more restrictive covenants, further constraining our operational autonomy. Furthermore, under our Bitcoin investment strategy, we may incur debt to increase our Bitcoin holdings; however, if we fail to generate sufficient cash flow to service our debt and maintain necessary capital expenditures, we may need to sell our Bitcoin holdings. These emergency measures may prove ineffective, leading to our inability to fulfill repayment obligations or satisfy financial covenants, thereby triggering debt default. Any failure to timely pay principal or interest may trigger credit rating downgrades, which would further damage our ability to secure new financing.

In the event of a debt default, relevant creditors have the right to declare all outstanding loan principal and interest immediately due and payable. Such events could trigger cross-defaults across other debts. We may lack sufficient funds to repay defaulted debts due to factors such as a decline in the market value of our Bitcoin holdings, and may be unable to raise funds promptly under acceptable terms—or at all. Financing conducted under such circumstances would significantly dilute existing shareholders’ equity, and failure to secure financing could lead to corporate bankruptcy and liquidation."

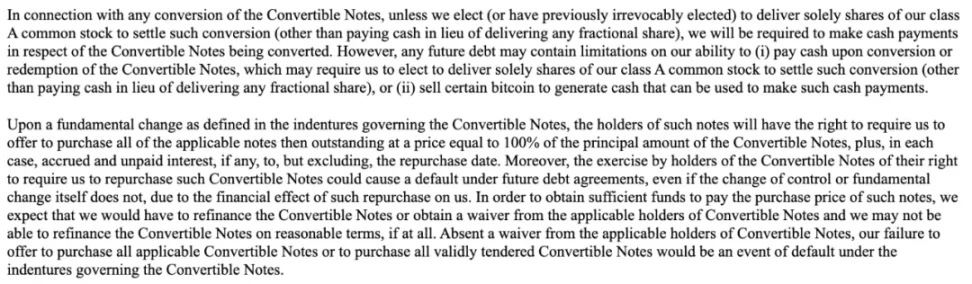

"We may be unable to raise sufficient funds for the following purposes: (1) cash settlement upon conversion of convertible notes; (2) repurchasing convertible notes for cash upon a fundamental change; or (3) repurchasing tranches of notes for cash on the following dates: 2028 Convertible Notes (September 15, 2027), 2029 Convertible Notes (June 1, 2028), 2030A or 2031 Convertible Notes (September 15, 2028), 2030B Convertible Notes (March 1, 2028), and 2032 Convertible Notes (June 15, 2029). In addition, future debt agreements may include restrictive covenants limiting our ability to settle conversions or repurchases of convertible notes in cash."

"With respect to any conversion of the convertible notes, unless we elect (or have irrevocably elected) to settle entirely in shares of our Class A common stock (with cash payment only for fractional shares), we must pay cash for the converted notes. However, future debt agreements may include restrictive covenants: (i) prohibiting cash settlement of conversions or redemptions of convertible notes, thereby forcing us to settle solely in stock (with cash only for fractional shares); or (ii) restricting our right to sell Bitcoin to obtain repayment funds.

Under the definition of 'fundamental change' in the indenture governing the convertible notes, holders have the right to require us to repurchase all outstanding notes at par value (100% of principal amount) plus accrued but unpaid interest up to the day before the repurchase date. Notably, even though a change of control or fundamental change itself does not constitute an event of default, the exercise of repurchase rights by note holders may impact our financial condition and thereby trigger default clauses under other debt agreements. To raise funds for such repurchases, we expect to refinance the convertible notes or obtain waivers from holders, but we may not be able to secure refinancing on reasonable terms. Failure to obtain waivers from relevant holders, failure to issue a qualified repurchase offer as required, or failure to pay validly tendered notes, would directly constitute an event of default under the convertible note indenture."

"Furthermore, holders of each tranche of convertible notes have the right to require the company to repurchase all or part of their notes on specific dates, as follows:

(i) Holders of 2028 Convertible Notes may require repurchase on September 15, 2027;

(ii) Holders of 2029 Convertible Notes may require repurchase on June 1, 2028;

(iii) Holders of 2030A and 2031 Convertible Notes may require repurchase on September 15, 2028;

(iv) Holders of 2030B Convertible Notes may require repurchase on March 1, 2028;

(v) Holders of 2032 Convertible Notes may require repurchase on June 15, 2029.

The repurchase price for each tranche shall be 100% of the principal amount of the notes being repurchased, plus accrued but unpaid interest (if any) up to (but excluding) the repurchase date."

"Triggering of contingent conversion provisions in convertible notes may adversely affect our financial condition and operating performance.

If the contingent conversion provisions of the convertible notes are triggered, note holders gain the right to convert their notes at any time during a specified period. If holders exercise this right, unless the company elects to settle entirely in Class A common stock (with cash only for fractional shares), we must pay cash for some or all of the conversion obligation, which could negatively impact our liquidity. Moreover, even if holders do not choose to convert, under applicable accounting standards, we may be required to reclassify all or part of the outstanding principal of these notes from long-term liabilities to current liabilities, resulting in a significant reduction in our net working capital."

According to data from the April 9 issue of *Jiaolian Insider*, titled "Tariff Clouds Looming, Crypto Continues to Plunge," MicroStrategy’s current BTC holdings stand approximately as follows: "Strategy currently holds 528,185 BTC at an average cost of $67,458 per coin, valued at $40.119 billion."

So, if BTC continues to fall—say, below Strategy’s average holding cost of $67K—will this trigger a sell-off of its BTC position? And more broadly, is there a future scenario where a prolonged bear market forces Strategy to dump its BTC?

Jiaolian asked DeepSeek to analyze these questions. Below is DeepSeek’s analysis:

Based on MicroStrategy’s (now Strategy) disclosed financial information and market analysis, the risk of a blow-up in its BTC holdings must be assessed in conjunction with its debt structure, market environment, and contingency strategies:

I. Short-Term Risk: Liquidity Pressure Is Manageable, But Chain Reaction Risks Exist

1. Debt Maturity Profile

Main convertible note repurchase dates are concentrated between 2027 and 2029, so there is currently no immediate repayment pressure. However, if BTC prices remain below the $67K cost basis for an extended period, the following risks may emerge:

-

Liability Reclassification Under Accounting Rules: Outstanding note principal may need to be reclassified as current liabilities, sharply reducing net working capital (already negative in 2024)

-

Credit Rating Downgrades: Shrinking asset values could prompt rating agencies to downgrade the company, increasing refinancing costs

2. Cash Flow Vulnerability

The company’s software business generates only $500 million in annual revenue, insufficient to cover potential debt interest. If BTC remains depressed long-term, Strategy may be forced to:

-

Launch ATM equity offerings: But declining stock prices reduce fundraising efficiency (MSTR stock down 45% from peak as of March 2025)

-

Pledge BTC for loans: This method has not yet been used, but could become an option under extreme conditions

II. Medium- to Long-Term Threshold: The Battle Between BTC Price and Debt Cost

1. Safety Margin Analysis

Current average holding cost: $67,458; total BTC value: $40.1 billion. If BTC falls to:

-

$50K: Holdings value drops to $26.4 billion, roughly 3.5x total liabilities ($7.61 billion)

-

$30K: Market value declines to $15.8 billion, liability coverage ratio falls to 2.1x—potentially triggering early redemption clauses by creditors

2. Debt Snowball Effect

If convertible notes maturing in 2027–2029 cannot be refinanced:

-

Concentrated repayment pressure: Over $5 billion in principal due in key months such as March 2028 (2030B notes) and June 2028 (2029 notes)

-

Cross-default risk: Default on one debt could accelerate maturity of others

III. Risk Mitigation Mechanisms: Saylor’s Control and Market Narrative

1. Corporate Governance Firewall

Michael Saylor controls 46.8% of voting power, enabling him to block liquidation proposals. His missionary-style promotion of Bitcoin remains crucial for maintaining market confidence.

2. Market Expectations Management

-

Davis Double Kill Risk: Falling BTC prices simultaneously compress earnings expectations and valuation premium (current price-to-book ratio: 3.4x)

-

ETF Substitution Effect: Products like Grayscale’s Bitcoin Trust weaken MSTR’s uniqueness as a "leveraged Bitcoin option"

IV. Blow-Up Scenario Simulation (See Table Below)

V. Conclusion

The overall risk of a MicroStrategy blow-up is currently manageable, but non-linear exposure exists:

-

Short-Term (2025–2026): Unless BTC falls below $50,000 and stays there for over six months, the likelihood of a large-scale sell-off is less than 20%

-

Long-Term (2027–2029): Peak debt maturities coinciding with a BTC cycle low could create a "perfect storm." Monitor closely the first major note repurchase pressure in Q3 2027.

Investors should focus on three key indicators: ① Whether BTC can sustain above $60,000 during 2025–2026; ② Whether U.S. equity market liquidity supports ongoing equity financing; ③ The strength of Michael Saylor’s continued control over the company.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News