Behind the Listing of U.S. Stocks on Blockchain: Hype in Narrative, Silence in Market—Can Old Wine in a New Bottle Become the Engine for a Second Bull Market Curve?

TechFlow Selected TechFlow Selected

Behind the Listing of U.S. Stocks on Blockchain: Hype in Narrative, Silence in Market—Can Old Wine in a New Bottle Become the Engine for a Second Bull Market Curve?

Amid持续 market downturn, can stock tokenization—a "new bottle for old wine"—emerge as a new narrative to build a market bottom?

Author: Frank, PANews

Tokenized U.S. stocks have recently become a hot topic in an otherwise sluggish market.

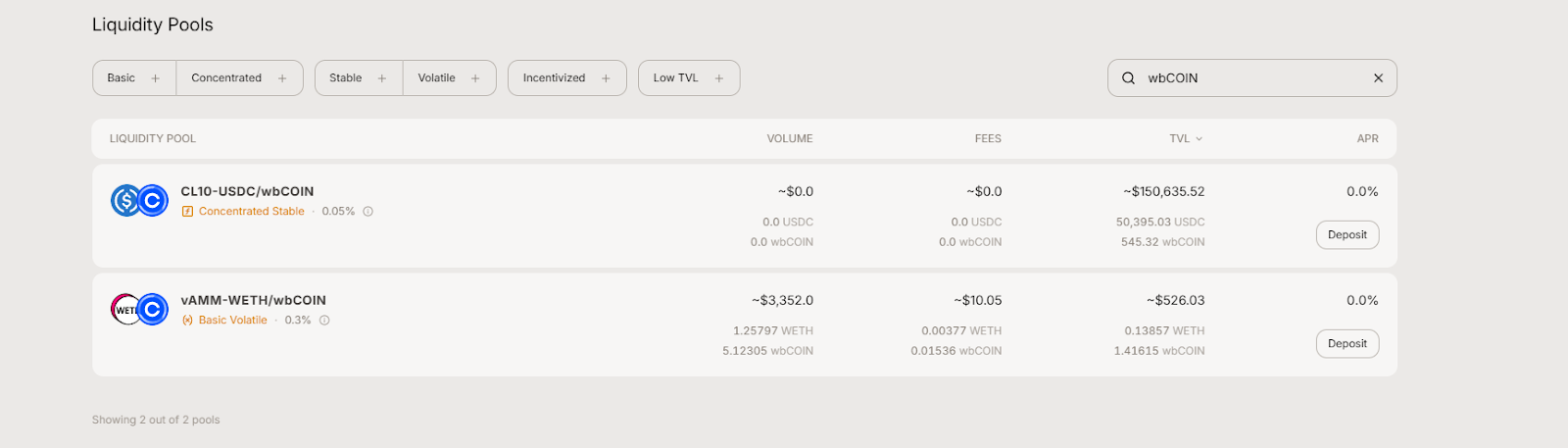

On March 8, Swiss-based tokenization issuer Backed launched the Coinbase stock token wbCOIN on Base, allowing users to trade it with USDC via CoWSwap. The company claims the token is 1:1 pegged to the value of $COIN shares and grants legal claim rights. Although Backed emphasized that it has no official affiliation with Coinbase, the move sparked community debate: Is tokenization of U.S. equities entering a new growth cycle? Amid prolonged market downturns, can this “old wine in a new bottle” become a fresh narrative for building a market bottom?

Narrative First, Value Later: The Hot-Cold Contrast of Tokenized U.S. Stocks

With the pro-crypto Trump administration taking office, the legal dispute between the SEC and Coinbase came to an end. In early 2025, Jesse Pollak, head of the Base protocol, stated on X that Coinbase was considering bringing tokenized $COIN shares to the Base network for U.S. users. However, Coinbase still needs time to launch such a service compliantly.

Backed moved swiftly, getting ahead of the curve. According to official information, Backed was founded in 2021 and initially received investment support from institutions like Gnosis and Semantic. Headquartered and operating globally, its products are issued under the EU regulatory framework, comply with MiFID II requirements, and have passed EU prospectus approval.

However, wbCOIN isn’t Backed’s first tokenized stock product. As early as July 2024, Backed partnered with INX to launch tokenized trading of NVIDIA shares. It has also released tokenized versions of S&P 500 and Tesla stocks. At the time of their launches, however, market attention wasn’t focused on security tokenization. Today’s market, desperate for credible narratives to rebuild confidence, is more receptive.

Still, the lukewarm response to wbCOIN isn't solely due to its inaccessibility to U.S. markets or general market weakness. The trading activity following wbCOIN’s launch clearly lags behind the buzz. As of March 11, wbCOIN’s TVL stood at approximately $4.42 million.

Data from Aerodrome shows its trading volume was merely $3,352—lower than that of a newly launched meme coin.

This lackluster performance isn’t just because wbCOIN is new. Another earlier-launched product, BNVDA, recorded only $113 in trading volume, similarly ignored by the market.

Despite strong conceptual appeal, the current tokenized U.S. stock market remains in its infancy, with limited scale and activity. Perhaps a Coinbase-backed tokenized product could generate greater trading interest.

Tokenized U.S. Stocks: Old Concept, New Era – Compliance Is Key

In reality, putting U.S. stocks on blockchain isn’t a new idea. Before this latest wave, both crypto firms and traditional financial institutions had explored it—mostly ending in failure.

The once-prominent FTX exchange offered tokenized trading of stocks like Tesla and GameStop between 2020 and 2022. However, FTX's collapse in 2022 abruptly ended the service. Rumors later emerged questioning whether FTX actually held sufficient underlying shares, further eroding trust in exchange-issued tokenized stocks.

In 2021, Binance also experimented with tokenized stocks for Tesla, Coinbase, and Apple, allowing users to buy fractional shares. But tightening global regulations quickly followed—financial regulators in the UK and Germany warned these products might violate securities laws. Within weeks, Binance delisted all stock tokens.

Another exchange, Bittrex Global, which featured tokenized stock trading, shut down its platform and entered bankruptcy proceedings after facing regulatory pressure and an SEC lawsuit.

These cases show that regulatory hurdles were the primary reason for past failures in offering tokenized U.S. stocks. Now, renewed interest in stock tokenization stems from several factors:

1. With the Trump administration prioritizing and supporting crypto, tensions between regulators and the crypto industry have eased.

2. The market is in a downturn and needs narratives backed by real-world value.

3. Technological and compliance frameworks have matured. Compared to earlier unregulated expansion, today’s crypto market emphasizes compliance design and technical safeguards. For example, Backed obtains EU-approved prospectuses before issuing any token, clearly defining token holders’ rights to the underlying stock. On the technical side, oracle systems and public chain performance have improved significantly.

One-Thousandth of a Percent vs. Trillion-Dollar Dreams: The Reality Check for Tokenized Stocks

Despite impressive growth rates, the actual size of the tokenized stock market remains far below institutional forecasts. Fundamentally, whether tokenized U.S. stocks or other securities, they fall under the category of RWA (Real World Assets). Given that both cryptocurrencies and U.S. equities are high-volatility, high-liquidity assets, the massive trading volume, capital scale, and strong fundamentals of U.S. stocks make them highly attractive to the crypto world.

The industry holds extremely optimistic expectations for the future of stock tokenization. Some authoritative institutions project the tokenized asset market could reach tens of trillions of dollars by 2030: Boston Consulting Group (BCG) estimates global tokenized assets could hit $16 trillion by 2030. Security Token Market even predicts $30 trillion in assets will be tokenized by then, driven primarily by stocks, real estate, bonds, and gold.

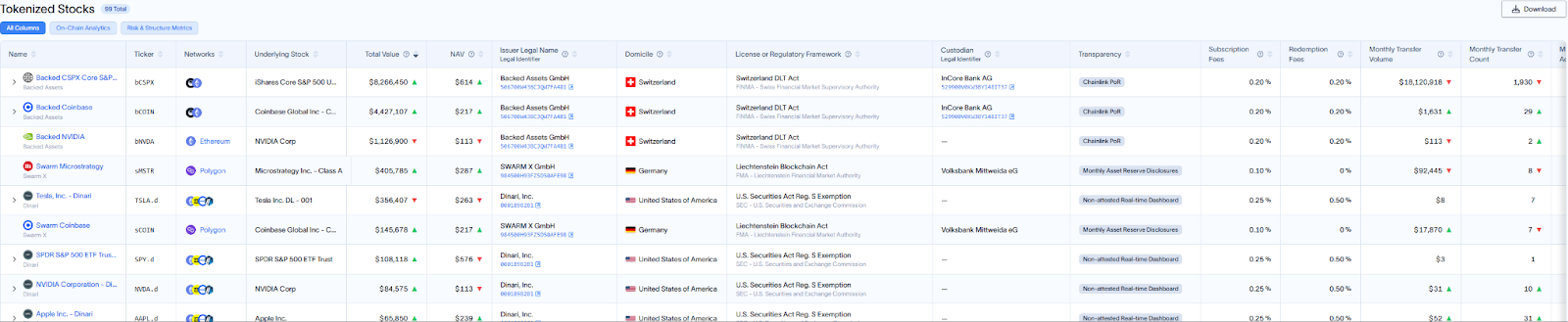

As of March 11, the total value of globally tokenized RWA assets stands at around $17.8 billion, with stock-related assets valued at approximately $15.43 million—less than 0.1% of the total—and monthly trading volume only $18 million. Clearly, within the RWA space, stock tokenization remains an immature market.

Yet in terms of growth rate and risk resilience, tokenized stocks show promise. In July 2024, the total on-chain value of tokenized stocks was about $50 million; within six months, it tripled. This growth significantly outpaces that of most alt assets during the same period.

Recently, the crypto market experienced a sharp correction, with Bitcoin falling below $80,000 and total market cap retreating to levels seen in the first half of 2024—a nearly 30% drop over three months. Yet tokenized stocks performed much better, remaining near historical highs. This suggests that overall market volatility in equities is less influenced by individual assets compared to crypto, and differing volatility patterns across asset classes contribute to greater stability. This offers tokenized stocks a new form of value anchoring.

For today’s investors, tokenized U.S. stocks are neither a bear-market savior nor a fleeting trend. They resemble a seed needing time to sprout—whether it grows into a towering tree depends on the triad of regulation, technology, and market sentiment. The answer may lie in the SEC’s next policy move, Coinbase’s upcoming compliance steps, or the flow of retail and institutional capital in the next bull run. One thing is certain: this experiment is far from over.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News