Crypto payment channel: a superconductor for payments

TechFlow Selected TechFlow Selected

Crypto payment channel: a superconductor for payments

Crypto rails are the superconductors of payments, enabling faster settlement times, lower fees, and seamless cross-border operations.

Author: Dmitriy Berenzon

Translation: Will A Wang

As we step into 2025, blockchain has gradually built a financial payment ecosystem parallel to the traditional financial system. Cryptographic payment rails now carry a stablecoin volume of $200 billion and a stablecoin transaction value of $5.62 trillion in 2024—Visa-adjusted figures more applicable to actual payments—and are nearly equivalent to Mastercard's annual transaction volume. According to ARK Invest's methodology report, stablecoins achieved an annualized transaction volume of $15.6 trillion in 2024, approximately 119% and 200% of Visa and Mastercard’s volumes respectively.

Regardless, the widespread adoption of crypto payments is now an undeniable reality, exemplified notably by Stripe’s $1.1 billion acquisition of Bridge, a stablecoin service provider. As Stripe CEO Patrick Collison stated, crypto payment rails are superconductors for payments. They form the foundation of a parallel financial system that enables faster settlement, lower fees, and seamless cross-border operations. This idea took a decade to mature, but today we see hundreds of companies working to make it real. Over the next decade, we will witness crypto rails becoming central to financial innovation and driving global economic growth.

Previously, we introduced the Web3 crypto payment system built on blockchain infrastructure through multiple Web3 payment articles:

-

Web3 Payment In-Depth Report: Industry Giants’ Full-Scale Offensive, Poised to Reshape the Crypto Market Landscape, which explains how Web3 payments are constructed and outlines major players' strategies in 2023;

-

Web3 Payment In-Depth Report: From E-Cash to Tokenized Money and the Future of PayFi, a systematic overview of how Web3 payments evolved from e-cash to tokenized money/digital dollars and future trends. Also refer to Circle’s 2025 USDC Economic Report: The Digital Dollar on the Internet of Value.

-

Web3 Payment In-Depth Report: How Stablecoins Will Unfold in 2025, offering insights from the perspective of stablecoins.

The following articles will examine global regional adoption patterns of crypto payments, as differing logics—financial efficiency upgrades in the Northern Hemisphere versus inflation-resistant value storage in the Southern Hemisphere—have created a situation where “you’re in one world while I’m in another.” Moreover, since both payments and money now exist on-chain, integrating crypto payments with DeFi to maximize utility represents a key future trend—what we call PayFi or DeFi 2.0? Feel free to engage, stay tuned.

There remain many challenges to address, as listed by Kevin:

-

transaction market: $16 trillion

-

trade finance: $89 trillion

-

remittance $4 trillion prefund

-

international wire fees average nearly 7%

-

3-5 business days for settlement

-

1.4 billion people unbanked

This translation of Dmitriy Berenzon’s article Cryptorails: Superconductors for Payments offers a comprehensive view from the lens of traditional payments, illustrating how blockchain-based crypto payment rails can enhance conventional systems, presenting multiple real-world use cases and future projections—well worth deep reading.

In 2009, when Satoshi Nakamoto launched Bitcoin, he envisioned using cryptographic networks for payments so that money could flow freely across the internet like information. While this direction was correct, the technology, economic models, and ecosystems at the time were not suitable for commercializing this use case.

Fast forward to 2025, we observe the convergence of several critical innovations and developments making this vision inevitable: stablecoins have been widely adopted by consumers and enterprises; market makers and OTC desks now comfortably hold stablecoins on their balance sheets; DeFi applications have built robust on-chain financial infrastructure; abundant fiat on/off-ramps exist globally; blockspace has become faster and cheaper; embedded wallets simplify user experience; and clearer regulatory frameworks reduce uncertainty.

Today, we have the opportunity to build a new generation of payment companies leveraging the power of "crypto rails" to achieve better unit economics than traditional financial systems constrained by multiple rent-seeking intermediaries and outdated infrastructure. These crypto rails are forming the backbone of a parallel financial system that operates 24/7 in real-time and is inherently global.

In this article, Dmitriy Berenzon will:

-

explain key components of the traditional financial system;

-

outline current primary use cases of crypto rails;

-

discuss ongoing barriers and challenges to adoption;

-

share predictions on the market outlook five years ahead.

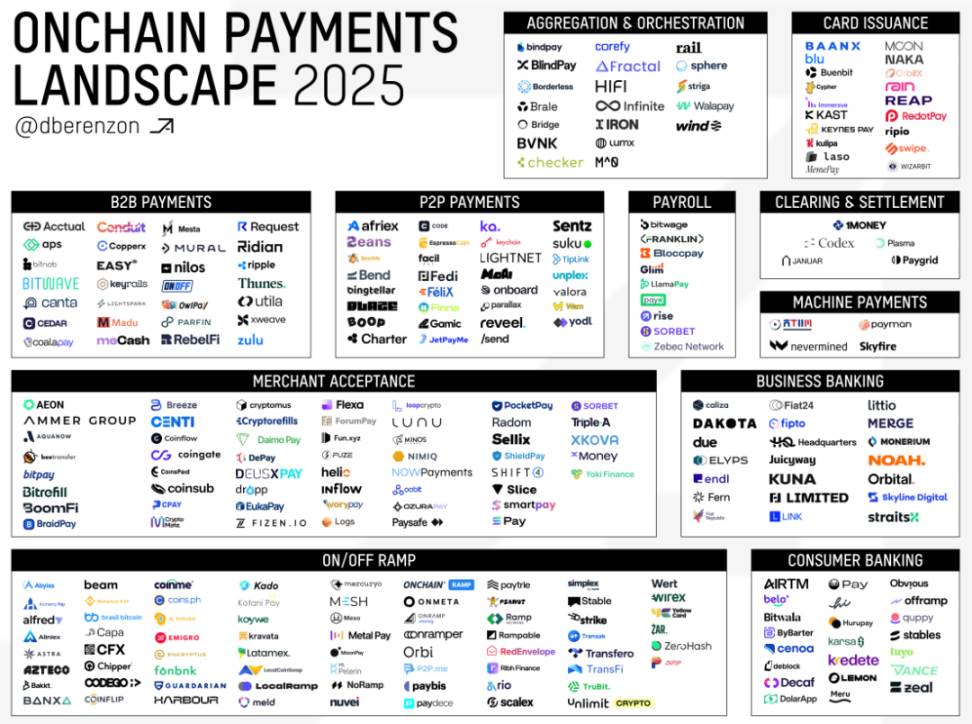

To further emphasize the scope, note that the number of companies operating here is far greater than you might imagine—approximately 280 as of writing:

I. Existing Payment Rails

To understand the significance of crypto rails, one must first grasp key concepts of existing payment channels and their complex market structures and system architectures. If already familiar, feel free to skip this section.

1.1 Card Networks

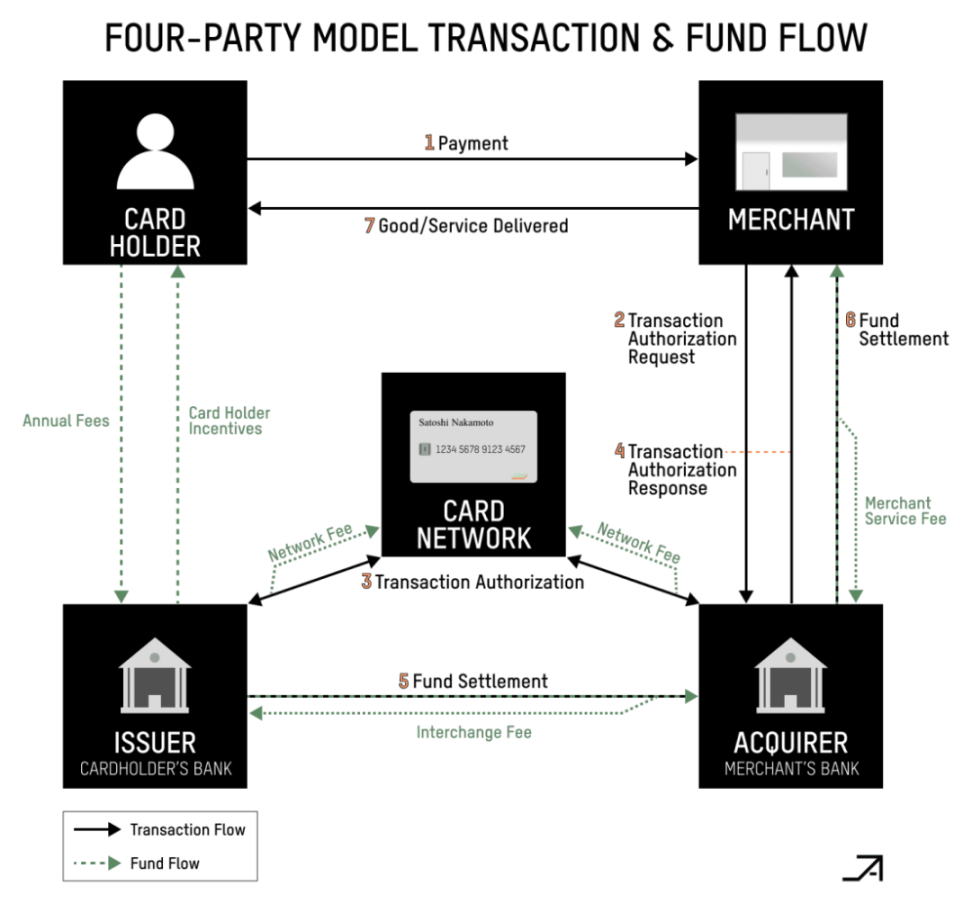

Although card network topologies are complex, the main participants in credit card transactions haven’t changed much over the past 70 years. Fundamentally, a credit card transaction involves four key parties:

-

Merchant

-

Cardholder

-

Issuing Bank

-

Acquiring Bank

The first two are straightforward, but the latter two deserve explanation.

An issuing bank (or issuer) provides customers with credit or debit cards and authorizes transactions. When a transaction request is made, the issuing bank decides whether to approve it by checking the cardholder’s account balance, available credit, and other factors. Credit cards essentially lend funds from the issuer, whereas debit cards transfer directly from your account.

If a merchant wants to accept credit card payments, they need an acquirer (which could be a bank, payment processor, gateway, or independent sales organization)—an authorized member of the card network. The term “acquirer” comes from its role in collecting payments on behalf of merchants and ensuring these funds reach the merchant’s account.

The card network itself provides the channel and rules for credit card payments. It connects acquirers with issuing banks, offers clearing functions, sets participation rules, and determines transaction fees. ISO 8583 remains the primary international standard defining how credit card payment information (e.g., authorization, settlement, refunds) is structured and exchanged among network participants. Within the network, issuers and acquirers act like distributors—issuers focus on getting more cards into users’ hands, while acquirers aim to get as many card terminals and payment gateways into merchants’ hands as possible to enable credit card acceptance.

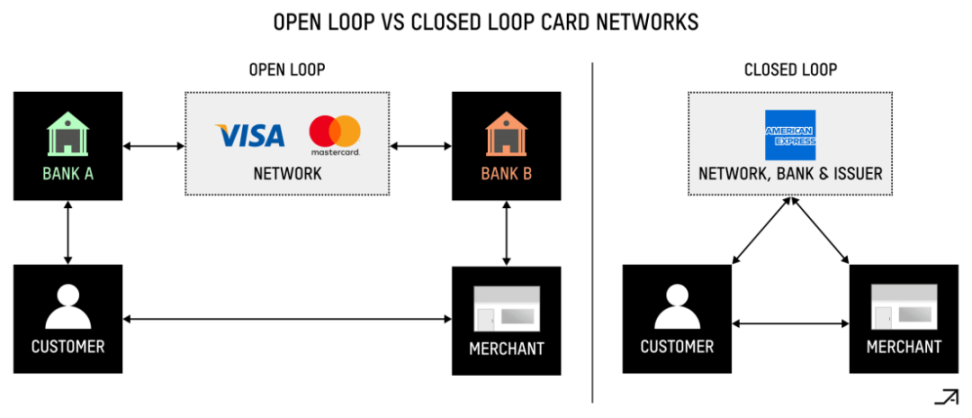

Additionally, there are two types of card networks: “open-loop” and “closed-loop.” Open-loop networks like Visa and Mastercard involve multiple parties: issuing banks, acquiring banks, and the card network itself. The card network facilitates communication and transaction routing but functions more like a marketplace, relying on financial institutions to issue cards and manage customer accounts. Only banks are allowed to issue cards on open-loop networks. Each debit or credit card has a Bank Identification Number (BIN), issued by Visa to banks, while non-bank entities like PayFacs require a “BIN sponsor” to issue cards or process transactions.

In contrast, closed-loop networks like American Express are self-contained, with a single company handling all aspects of the transaction process—they typically issue their own cards, act as their own bank, and provide their own merchant acquiring services. Generally, closed-loop systems offer more control and better profit margins but suffer from limited merchant acceptance. Conversely, open-loop systems offer broader adoption but involve shared control and revenue among participants.

Source: Arvy

The economics of payments are highly complex, involving multiple layers of fees within the network. Interchange Fees are portions of the payment fee collected by issuing banks for providing access to their customers. Although acquirers technically pay interchange fees directly, the cost is usually passed on to merchants. Card networks typically set interchange fees, which often constitute the majority of total payment costs. These fees vary significantly across regions and transaction types. For example, in the U.S., consumer credit card fees range from ~1.2% to ~3%, while in the EU they are capped at 0.3%. Additionally, Scheme Fees are determined by card networks to compensate for connecting acquirers and issuers and acting as a “channel” to ensure accurate transaction and fund flows. There are also Settlement Fees paid to acquirers, usually a percentage of the settled amount or transaction volume.

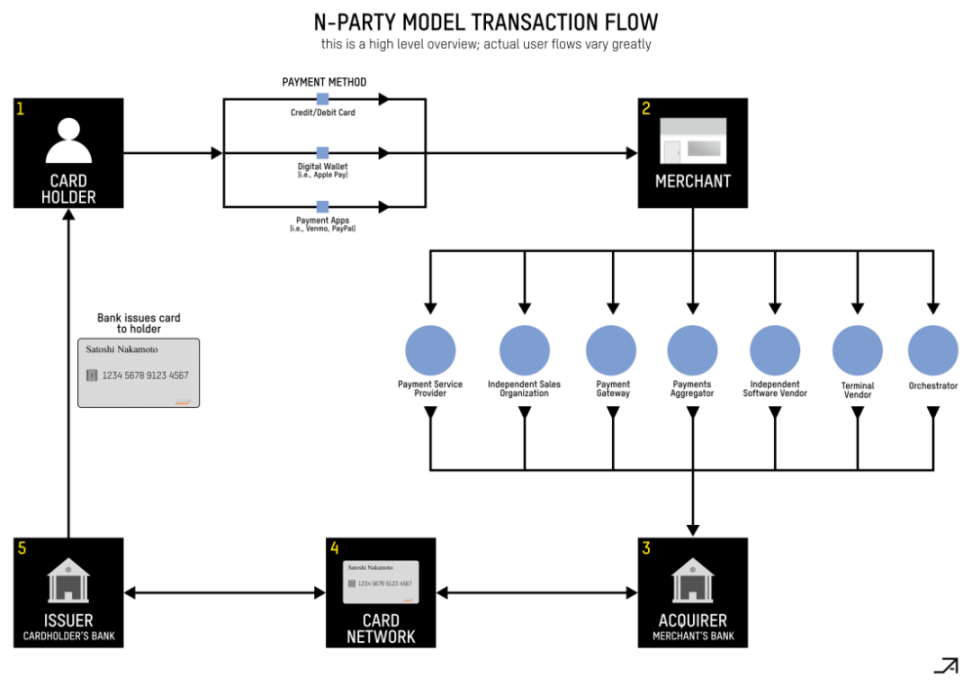

While these represent the most important participants in the value chain, the actual market structure in practice is far more complex:

Source: 22nd

Within the above chain, several additional key participants exist:

-

Payment Gateway: Encrypts and transmits payment information, connects payment processors and acquirers for authorization, and relays transaction approval or denial to businesses in real time.

-

Payment Processor: Acts on behalf of the acquirer to handle payments. It forwards transaction details from the gateway to the acquirer, which then communicates via the card network with the issuing bank for authorization. The processor receives the authorization response and sends it back to the gateway to complete the transaction. It also handles settlement—the process of funds actually entering the merchant’s bank account. Typically, a business sends a batch of authorized transactions to the processor, which submits them to the acquirer to initiate fund transfers from the issuing bank to the merchant’s account.

-

Payment Facilitator (PayFac) or Payment Service Provider (PSP): Pioneered around 2010 by PayPal and Square, these function as mini-payment processors between merchants and acquirers. By bundling many smaller merchants into their systems, they act as aggregators achieving economies of scale, simplifying operations by managing fund flows, processing transactions, and ensuring payments. PayFacs hold direct merchant IDs from card networks and take responsibility for onboarding, compliance (e.g., anti-money laundering laws), and underwriting on behalf of partnering merchants.

-

Orchestration Platform: A middleware layer that simplifies and optimizes a merchant’s payment processes. It connects via a single API to multiple processors, gateways, and acquirers, improving success rates, reducing costs, and enhancing performance by routing payments based on location, fees, etc.

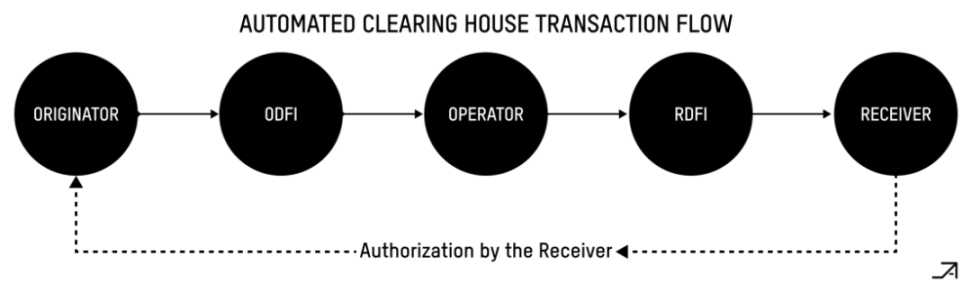

1.2 Automated Clearing House

The Automated Clearing House (ACH) is one of the largest payment networks in the U.S., actually owned by the banks that use it. Established in the 1970s, it gained popularity when the U.S. government began using it to distribute Social Security benefits, encouraging banks nationwide to join. Today, it is widely used for payroll, bill payments, and B2B transactions.

ACH transactions fall into two main types: credits and debits. When users receive salaries or pay bills online using bank accounts, they are using the ACH network. The process involves several participants: the individual or company initiating the payment (originator), their bank (ODFI), the recipient’s bank (RDFI), and the operator that manages all these transactions. In the ACH process, the originator submits the transaction to the ODFI, which sends it to the ACH operator, who then routes it to the RDFI. At the end of each day, the operator calculates net settlement totals for its member banks (the Federal Reserve manages actual settlements).

Source: The U.S. Payment System: A Guide for Payment Professionals

One of the most important aspects of ACH is how it manages risk. When a company initiates an ACH payment, its bank (ODFI) is responsible for ensuring everything is legitimate. This is especially crucial for debits—imagine someone unauthorized using your bank account details. To prevent this, regulations allow disputes up to 60 days after receiving a statement, and companies like PayPal have developed clever verification methods such as micro test deposits to confirm account ownership.

The ACH system has struggled to meet modern demands. In 2015, it introduced “Same-Day ACH” for faster processing. Nonetheless, it still relies on batch processing rather than real-time transfers and has limitations. For instance, you cannot send more than $25,000 in a single transaction, and it isn't suitable for international payments.

1.3 Wire Transfers

Wire transfers are central to high-value payment processing, with the two main U.S. systems being Fedwire and CHIPS. These systems handle time-sensitive, guaranteed payments requiring immediate settlement, such as securities trades, major commercial deals, and real estate purchases. Once executed, wire transfers are typically irrevocable and cannot be canceled or reversed without the recipient’s consent. Unlike conventional payment networks that batch-process transactions, modern wire systems use Real-Time Gross Settlement (RTGS), meaning each transaction settles individually as it occurs. This is crucial because the system handles hundreds of billions daily, and intraday bank failures using traditional net settlement would pose excessive risk.

Fedwire is an RTGS system allowing participating financial institutions to send and receive same-day funds. When a business initiates a wire, its bank verifies the request, deducts funds from the account, and sends a message to Fedwire. The Federal Reserve then immediately debits the sending bank’s account and credits the receiving bank’s account, after which the receiving bank credits the final recipient’s account. The system operates from 9 PM the previous day to 7 PM Eastern Time, closing on weekends and federal holidays.

CHIPS, owned by large U.S. banks through The Clearing House, is a smaller private-sector alternative serving only a few major banks.

Unlike Fedwire’s RTGS approach, CHIPS uses a netting settlement system, allowing offsetting of multiple payments between counterparties. For example, if Alice wants to send Bob $10 million and Bob wants to send Alice $2 million, CHIPS combines these into a single $8 million payment from Bob to Alice. While this means CHIPS payments take longer than real-time transactions, most settle intra-day.

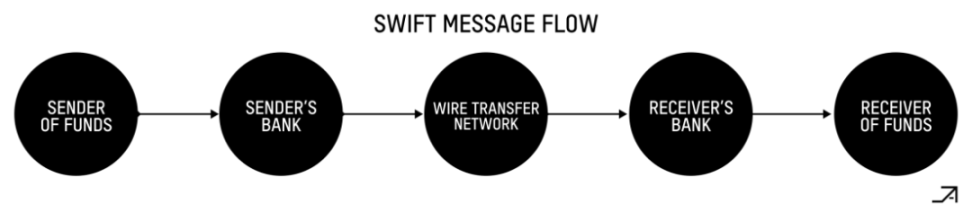

SWIFT complements these systems but is not a payment system itself—it’s a global messaging network for financial institutions. It’s a member-owned cooperative whose shareholders represent over 11,000 member organizations. SWIFT enables banks and securities firms worldwide to exchange secure, structured messages, many of which initiate payment transactions across various networks. According to Statrys, SWIFT transfers take about 18 hours to complete.

In a typical flow, the sender instructs their bank to wire funds to the recipient. Below is a simplified scenario where both banks belong to the same wire network.

Source: The U.S. Payment System: A Guide for Payment Professionals

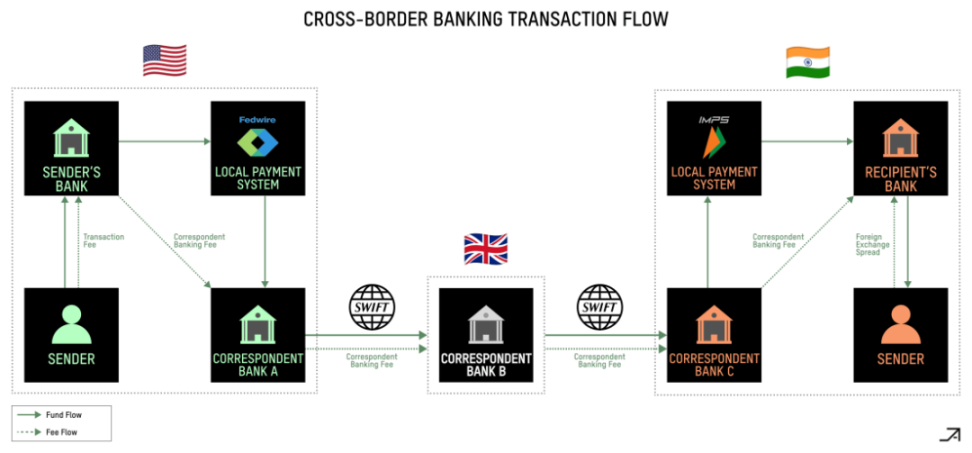

In more complex cases, particularly cross-border payments, transactions require execution through a correspondent banking relationship, typically coordinated via SWIFT.

Source: Matt Brown

II. Real-World Use Cases

Now that we have a foundational understanding of traditional payment rails, we can focus on the advantages of crypto payment rails.

Crypto payment rails are most effective in situations where traditional dollar access is limited but demand for dollars is strong. Consider places where individuals need dollars to preserve wealth or as a banking alternative but lack easy access to traditional USD bank accounts—typically countries with economic instability, high inflation, capital controls, or underdeveloped banking systems, such as Argentina, Venezuela, Nigeria, Turkey, and Ukraine. Moreover, one could argue that compared to most other currencies, the dollar is a superior store of value, and consumers and businesses often prefer it because it can easily serve as a medium of exchange or be converted into local fiat at point-of-sale.

The advantages of crypto payment rails are also most evident in globalized payment scenarios, as blockchain networks are borderless, leveraging existing internet connectivity to provide global coverage. According to the World Bank, there are currently 92 RTGS systems in operation globally, each typically owned by its respective central bank. While ideal for domestic payments within those countries, the problem is they cannot “talk to each other.” Crypto payment rails can act as glue between these disparate systems and extend functionality to countries lacking them.

Crypto payments are also particularly suited for payments with urgency or high time preference. This includes cross-border supplier payments and foreign aid disbursements. This is especially helpful in scenarios where correspondent banking networks are particularly inefficient. For example, despite geographic proximity, sending remittances from Mexico to the U.S. is actually harder than from Hong Kong to the U.S. Even in developed corridors like U.S. to Europe, payments often require four or more intermediary banks.

On the other hand, crypto payment rails are less attractive for domestic transactions in developed countries, especially where credit card penetration is high or real-time payment systems already exist. For example, intra-European payments proceed smoothly via SEPA, and euro stability eliminates the need for dollar-denominated alternatives.

2.1 Merchant Acceptance

Merchant acceptance can be divided into two distinct use cases: front-end integration and back-end integration. In the front-end approach, merchants directly accept cryptocurrency as payment from customers. While one of the oldest use cases, historically it hasn’t seen significant transaction volume because few people held crypto, even fewer wanted to spend it, and options for holders were limited. Today’s market differs, as increasing numbers of people hold crypto assets (including stablecoins), and more merchants accept them as a payment option to reach new customer segments and ultimately sell more goods and services.

Geographically, most transaction volume comes from businesses selling to consumers in early crypto-adopting countries/regions, typically emerging markets like China, Vietnam, and India. From the merchant side, most demand originates from online gambling and retail stock brokerage firms targeting emerging markets, Web2 and Web3 markets (such as watch retailers and content creators), and real-money gaming (like fantasy sports and lotteries).

The “front-end” merchant acceptance process typically looks like this:

-

PSP usually creates a wallet for the merchant after KYC/KYB;

-

User sends cryptocurrency to the PSP;

-

PSP converts the cryptocurrency into fiat via liquidity providers or stablecoin issuers and sends funds to the merchant’s local bank account, possibly using other licensed partners.

The main challenge hindering continued adoption of this use case is psychological—cryptocurrency seems unreal to many. Two user personas must be addressed: one completely indifferent to value, treating it all as magical internet money; the other pragmatic, wanting funds deposited directly into their bank.

Moreover, consumer adoption of crypto payments is more difficult in the U.S., where credit card rewards effectively pay consumers 1–5% cashback on purchases. Attempts have been made to convince merchants to promote crypto payments directly to consumers as a credit card alternative, but so far, none have succeeded. While lower interchange fees benefit merchants, this isn’t a concern for consumers. Merchant Customer Exchange launched in 2012 and failed by 2016 precisely because they couldn’t kickstart consumer-side adoption. In other words, it’s hard for merchants to directly incentivize users to switch from credit card to crypto asset payments, as payments are already “free” to consumers—so the value proposition must first be solved at the consumer level.

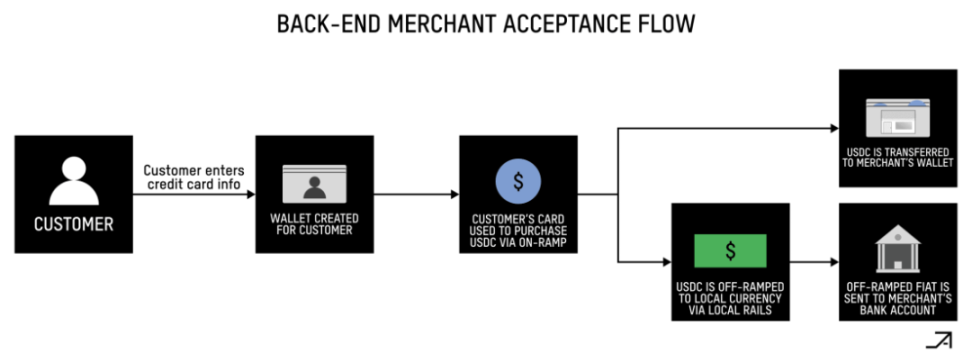

In the back-end approach, crypto payments can provide merchants with faster settlement times and improved access to funds. Settlement via Visa and Mastercard may take 2–3 days, American Express 5 days, and international settlements even longer—for example, about 30 days in Brazil. In certain use cases, such as marketplaces like Uber, merchants may need to pre-fund their bank accounts to make payouts before settlement.

In contrast, one can effectively enter the crypto payment rail via the user’s credit card, transfer funds on-chain, and ultimately deposit funds directly into the merchant’s bank account in local currency. Beyond improving working capital due to reduced capital lock-up during payment processing, merchants can further enhance treasury management by freely and instantly swapping between digital dollars and yield-bearing assets like tokenized U.S. Treasuries.

More specifically, the “back-end” merchant acceptance process might look like this:

-

User enters credit card details to complete transaction;

-

PSP creates a wallet for the customer and funds it via entry points accepting traditional payment methods;

-

Credit card transaction purchases USDC, which is then sent from the customer’s wallet to the merchant’s wallet;

-

PSP optionally transfers funds to merchant’s bank account via local rail T+0 (same day);

-

PSP typically receives funds from the acquirer on T+1 or T+2 (within 1–2 days).

2.2 Debit Cards

The ability to link debit cards directly to non-custodial smart contract wallets builds an unexpectedly powerful bridge between blockspace and the real world, driving organic adoption across different user personas. In emerging markets, these cards are becoming primary consumption tools, increasingly replacing traditional banking. Interestingly, even in countries with stable currencies, consumers are using these cards to accumulate USD savings progressively while avoiding FX fees at point of purchase. High-net-worth individuals are also increasingly using crypto-linked debit cards as efficient tools to spend USDC globally.

Debit cards have two advantages over credit cards: they face fewer regulatory restrictions (e.g., MCC 6051 is outright rejected in capital-controlled Pakistan and Bangladesh), and they carry lower fraud risk because refunding settled crypto transactions poses serious liability issues for credit cards.

In the long run, cards tied to crypto wallets for mobile payments could actually be the best way to combat fraud, as smartphones offer biometric authentication: scan your face, spend, and top up your wallet from your bank account.

2.3 Remittance

Remittances refer to funds sent by individuals who migrated abroad for work back to their home countries. According to the World Bank, remittance flows totaled approximately $656 billion in 2023, equivalent to Belgium’s GDP.

Traditional remittance systems are costly, leaving recipients with less money. On average, cross-border remittance fees are 6.4% of the amount sent, though these vary widely—from 2.2% sending from Malaysia to India (and even lower for high-volume corridors like U.S. to India) to 47.6% from Turkey to Bulgaria. Banks tend to charge the highest fees, around 12%, while money transfer operators like MoneyGram average 5.5%.

Source: World Bank

Crypto payments can offer a faster, cheaper way to send money overseas. The number of such companies largely depends on the overall size of the remittance market, with the highest-volume corridors being U.S. to Latin America (especially Mexico, Argentina, and Brazil), U.S. to India, and U.S. to the Philippines. A key driver is non-custodial embedded wallets offering Web2-level user experience.

A crypto-based remittance process might look like this:

-

Sender enters via bank account, debit card, credit card, or directly to a chain address via PSP; if no wallet exists, one is created;

-

PSP converts USDT/USDC into recipient’s local currency, either directly or via market makers or OTC partners;

-

PSP pays fiat into recipient’s bank account, either directly from their pooled bank account or via local payment gateways; alternatively, PSP may first generate a non-custodial wallet for the recipient to claim funds and let them choose to keep it on-chain;

-

In many cases, the recipient must complete KYC before receiving funds.

Nonetheless, go-to-market paths for crypto remittance ventures remain challenging. One issue is that you usually need to incentivize people to leave existing remittance operators, which can be expensive. Another is that transfers on most Web2 payment apps are already free, so native transfers alone aren’t enough to overcome the network effects of existing apps. Finally, while the on-chain transfer component works well, you still need to interact with traditional banking institutions at the “last mile,” so users may still face the same—or worse—issues due to on/off-ramp costs and friction. Specifically, payment gateways that convert to local fiat and deliver via custom methods like mobile phones or kiosks will capture the largest profit margins.

2.4 B2B Payments

Cross-border (XB) B2B payments are one of the most promising applications for crypto payments due to inefficiencies in traditional systems. Payments via correspondent banking can take weeks to settle—sometimes even longer. One founder reported taking 2.5 months to send a supplier payment from Africa to Asia. Another example: cross-border payments from Ghana to Nigeria (two neighboring countries) can take weeks with fees as high as 10%.

Furthermore, cross-border settlement is slow and expensive for PSPs. Companies like Stripe may need up to a week to pay international merchants and must lock up funds to cover fraud and refund risks. Shortening conversion cycles would unlock significant working capital.

XB B2B payments have made notable progress on crypto rails primarily because businesses care more about fees than consumers. Saving 0.5–1% per transaction may not sound substantial, but with large volumes—especially for thin-margin businesses—it becomes significant. Speed also matters. Settling payments in hours instead of days or weeks has a major impact on corporate working capital. Additionally, unlike consumers who expect seamless out-of-the-box experiences, businesses tolerate worse UX and greater complexity.

Moreover, the cross-border payments market is massive—estimates vary, but according to McKinsey, the cross-border payments market generated about $240 billion in revenue in 2022, with transaction volume around $150 trillion. That said, building sustainable businesses remains difficult. While the “stablecoin sandwich”—converting local currency to stablecoin and back—is certainly faster, it’s also expensive, as bidirectional on/off-ramping erodes margins, often resulting in unsustainable unit economics. Some companies attempt to solve this by building internal market-making divisions, but this is highly balance-sheet intensive and hard to scale. Additionally, customer acquisition is relatively slow, with concerns around regulation and risk, often requiring extensive education.

That said, as stablecoin legislation opens doors for more enterprises to hold and operate digital dollars, FX costs could drop rapidly over the next two years. With more on/off-ramp and token issuers securing direct banking relationships, they’ll be able to efficiently offer internet-scale wholesale exchange rates.

2.4.1 XB Supplier Payments

For B2B payments, most cross-border transactions involve importers paying suppliers, typically buyers in the U.S., Latin America, or Europe and suppliers in Africa or Asia. Local payment channels in these countries are underdeveloped, making it hard to find local banking partners. Crypto payments can also alleviate country-specific pain points. For example, in Brazil, you can’t use traditional channels to pay millions of dollars, making international payments difficult for businesses. Some well-known companies, like SpaceX, are already using crypto payments for this use case.

2.4.2 XB Receivables

Businesses with global customers often struggle to collect funds timely and efficiently. They usually partner with multiple PSPs to collect locally but need fast collection methods, which can take days or even weeks depending on the country. Crypto payments are faster than SWIFT transfers, compressing timelines to T+0.

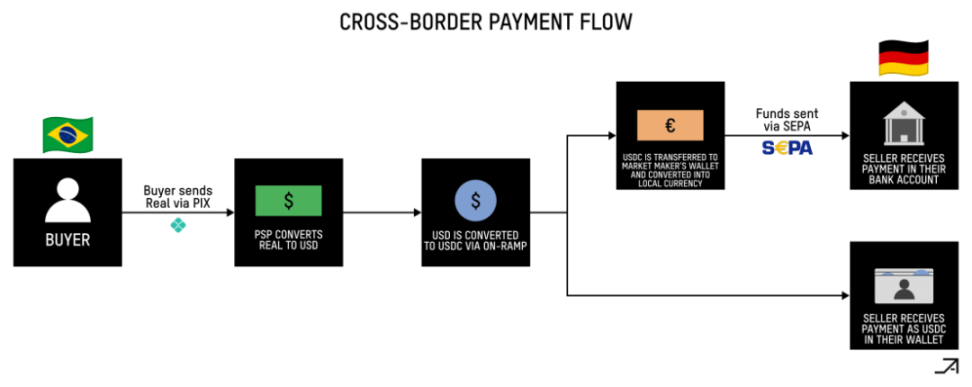

Here’s an example of a Brazilian company purchasing goods from a German company:

-

Buyer sends Reais to PSP via PIX;

-

PSP converts Reais to USD, then to USDC;

-

PSP sends USDC to seller’s wallet;

-

If seller wants local fiat, PSP sends USDC to a market maker or trading desk to convert to local currency;

-

If seller has license/bank account, PSP wires funds via local payment channels; otherwise, uses local partners.

2.4.3 Treasury Operations

Companies can also use crypto payment rails to improve treasury operations and accelerate global expansion. They can hold USD balances and use local on/off-ramp channels to reduce FX risk and enter new markets faster—even when local banks are unwilling to support them. They can also use crypto rails as an internal mechanism to restructure and repatriate funds across operating countries.

2.4.4 Foreign Aid Disbursement

Another common B2B use case we see is time-sensitive payments, where these crypto rails enable faster delivery to recipients. An example is foreign aid disbursement—allowing NGOs to use crypto rails to send money to local export agents who can separately pay eligible individuals. This is particularly effective in economies with very weak financial systems and/or governments. For example, in South Sudan, where the central bank has collapsed, local payments can take over a month. But with just a phone and internet connection, there’s a way to bring digital currency into the country, allowing individuals to exchange it for fiat and vice versa.

A payment flow for this use case might look like this:

-

NGO provides funds to PSP;

-

PSP sends bank transfer to OTC partner;

-

OTC partner converts fiat to USDC and sends it to local partner’s wallet;

-

Local partner acquires USDC via P2P traders.

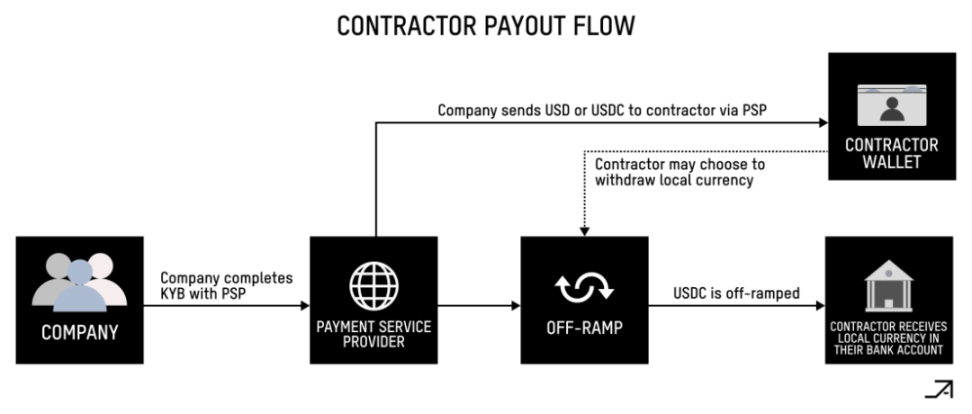

2.5 Payroll

From the consumer side, one of the most promising early adopters is freelancers and contractors, especially in emerging markets. The value proposition for these users is that more money ends up in their pockets rather than going to intermediaries, and that money can be digital dollars. This use case also brings cost efficiencies for the enterprise sending bulk payments, particularly useful for crypto-native companies (like exchanges) that already hold most of their funds in crypto.

A contractor payment flow typically looks like this:

-

Company completes KYB/KYC with PSP;

-

Company sends USD to PSP or sends USDC to wallet addresses linked to contractors;

-

Contractor decides whether to keep it as crypto or withdraw to bank account; PSP typically has master service agreements with one or more OTC partners holding relevant licenses in respective jurisdictions for local payouts.

2.6 On/Off-Ramps

On/off-ramps are a crowded, competitive market. While many early attempts failed to scale, the market has matured over recent years, with many companies operating sustainably and offering global local payment channels. Though on/off-ramps can serve as standalone products (e.g., simply buying crypto assets), they are arguably the most critical part of bundled services (like payments).

Building on/off-ramps typically involves three parts: obtaining necessary licenses (e.g., VASP, MTL, MSB), securing local banking partners or PSPs with access to local payment channels, and connecting to market makers or OTC desks for liquidity.

Initially, exchanges dominated on-ramps, but today, an increasing number of liquidity providers—from small forex and OTC desks to large trading firms like Cumberland and FalconX—are offering on-ramping. These firms can typically handle up to $100 million in daily volume, so they’re unlikely to run out of liquidity for popular assets. Some teams may even prefer them because they can commit to spreads, helping control margins.

Due to licensing, liquidity, and orchestration complexities, non-U.S. on/off-ramp operations are generally far more difficult than U.S. ones. This is especially true in Latin America and Africa, where dozens of currencies and payment methods exist. For example, you can use PDAX in the Philippines as it’s the largest crypto exchange there, but in Kenya, you need multiple local partners like Clixpesa, Fronbank, and Pritium depending on the payment method.

P2P channels rely on networks of “agents”—local individuals, currency providers, and small businesses like supermarkets and pharmacies—who provide fiat and stablecoin liquidity. These agents are especially common in Africa, where many already run mobile money kiosks for services like MPesa. Their primary motivation is economic incentive—they earn via transaction fees and FX spreads. Indeed, for individuals in high-inflation economies like Venezuela and Nigeria, being an agent is more profitable than traditional service jobs like taxi drivers or food delivery. They can work from home via smartphone, typically needing only a bank account and mobile money to start. This system is powerful because it supports dozens of local payment methods without formal licensing or integration, as transfers occur between personal bank accounts.

Notably, P2P channel FX rates are often more competitive. For example, banks in Khartoum, Sudan, typically charge up to 25% FX fees, while local crypto P2P ramps offer 8–9%, effectively market rates rather than forced bank rates. Similarly, P2P channels can offer FX rates about 7% cheaper than banks in Ghana and Venezuela. Usually, spreads are smaller in countries with ample dollar supply. Moreover, the best markets for P2P ramps are those with high inflation, high smartphone penetration, weak property rights, and unclear regulatory guidelines, because financial institutions avoid crypto, creating an environment conducive to self-custody and P2P growth.

A P2P on-ramp payment flow might look like this:

-

User selects or is automatically assigned a counterparty or “agent” who already holds USDT, typically custodied by the P2P platform;

-

User sends fiat to the agent via local payment channel;

-

Agent confirms receipt and sends USDT to the user.

From a market structure perspective, most on/off-ramps are commoditized with low customer loyalty, as users typically choose the cheapest option. To stay competitive, local payment channels may need to expand coverage, optimize for the most popular channels, and find the best local partners. Long-term, we may see consolidation in each country into 2–3 on/off-ramp providers with full licensing, support for all local payment methods, and maximum liquidity. Mid-term, aggregators will be especially useful, as local providers are often faster and cheaper, and combined options usually offer consumers the best prices and completion rates. If they can effectively optimize and route payments across hundreds of partners and routes, they may also suffer least from commoditization. This also applies to orchestration platforms, including compliance, PSP selection, bank partner selection, and value-added services like card issuance.

From the consumer side, the good news is fees may trend toward zero. We’re already seeing this on Coinbase, where instant conversion from USD to USDC costs $0. Long-term, most stablecoin issuers may offer this service to large wallets and fintech companies, further compressing fees.

III. Compliance, Regulation, Licensing

Obtaining regulatory licenses is a painful but necessary step to scaling crypto payment applications. For startups, two paths exist: partnering with already-licensed entities or obtaining licenses independently. Partnering allows startups to bypass the high costs and long timelines of self-licensing, but at the expense of lower margins, as much of the revenue goes to the licensed partner. Alternatively, startups can pre-invest (potentially hundreds of thousands to millions of dollars) to obtain licenses independently. While this path often takes months or even years (one project reported spending 2 years), it enables startups to offer more comprehensive products directly to users.

While established licensing pathways exist in many jurisdictions, achieving global license coverage is extremely challenging, even impossible, as each region has unique money transmission regulations—requiring over 100 licenses for full global coverage. For example, in the U.S. alone, a project needs money transmitter licenses (MTL) in every state, a BitLicense in New York, and registration as a money services business (MSB) with FinCEN. Just obtaining all-state MTLs could cost $500,000 to $2 million and take up to a year. Overseas requirements are equally daunting. Importantly, non-custodial startups that don’t touch fund flows can often bypass immediate licensing requirements and enter markets faster.

IV. Challenges

Adoption of payment methods is often difficult due to the chicken-and-egg problem. Either consumers must widely adopt a payment method, forcing merchants to accept it, or merchants must adopt it, forcing consumer usage. For example, before Uber became popular in 2012, credit cards were niche in Latin America; everyone wanted a card because it enabled Uber use, which was safer and initially cheaper than taxis. This allowed other on-demand apps (like Rappi) to thrive, as people now had smartphones and credit cards. A virtuous cycle emerged: more people wanted credit cards because more cool apps required them.

The same applies to mainstream consumer adoption of crypto payments. We haven’t yet seen a use case where paying with stablecoins is particularly advantageous or absolutely necessary, although debit card and remittance apps are bringing us closer. If a P2P app unlocks a completely new online behavior, it stands a chance—micropayments and creator payments seem like exciting candidates. Broadly speaking, consumer apps won’t gain traction unless they offer step-function improvements over the status quo.

On the on/off-ramp side, several issues persist:

-

High failure rate: If you’ve tried using a credit card to enter, you know the frustration.

-

User experience barriers: While early adopters tolerate the pain of acquiring assets via exchanges, the early majority will likely use specific apps directly. To support this, we need smooth in-app onboarding, ideally via Apple Pay.

-

High fees: Entry fees remain expensive—depending on provider and region, they can still reach 5–10%.

-

Inconsistent quality: Reliability and compliance still vary too much, especially for non-USD currencies.

One under-discussed issue is privacy. While privacy isn’t currently a serious concern for individuals or companies, it will become one once crypto payments become the primary mechanism for commerce. Serious negative consequences will arise when malicious actors begin monitoring payment activities of individuals, companies, and governments via public keys. A short-term solution is “privacy through obscurity”—launching new wallets each time funds need to be sent or received on-chain.

Additionally, establishing banking relationships is often the hardest part, as it presents another chicken-and-egg problem. Banks will accept you if they see transaction volume and profits, but you need banks first to generate that volume. Currently, only 4–6 small U.S. banks support crypto payment companies, and some have hit internal compliance limits. Part of the reason is that crypto payments are still classified as “high-risk activities” akin to cannabis, adult media, and online gambling.

The root cause is that compliance still doesn’t match traditional payment companies. This includes AML/KYC and Travel Rule compliance, OFAC screening, cybersecurity policies, and consumer protection policies. More challenging is embedding compliance directly into crypto payments rather than relying on out-of-band solutions and third-party companies. Lightspark’s Universal Currency Address offers a creative solution by facilitating compliance data exchange among participating institutions.

V. Future Outlook

On the consumer side, we’re now at a stage where certain groups are beginning to accept stablecoins, especially freelancers, contractors, and remote workers. By leveraging card networks to provide consumers with dollar exposure and everyday spending capabilities, we’re also drawing closer to meeting dollar demand in emerging economies. In other words, debit cards and embedded wallets have become the “bridge” bringing crypto to the masses in intuitive forms. On the business side, we’re at the dawn of mainstream adoption. Companies are already using stablecoins at scale, and this number will grow significantly over the next decade.

Considering all this, here are my 20 predictions for the state of this industry in the next 5 years:

-

$200–500 billion in annual payments volume via crypto rails, primarily driven by B2B payments.

-

Over 30 new banks launching natively on crypto payment rails globally.

-

Fintech companies racing to stay relevant, with dozens of crypto-native firms acquired.

-

Some crypto companies (possibly stablecoin issuers) acquiring struggling fintech firms and banks burdened by high CAC and operational costs.

-

About 3 crypto networks (L1 and L2) emerge, scaling with architectures designed for payments. These networks resemble Ripple in spirit but with sound technical stacks, economic models, and go-to-market strategies.

-

80% of online merchants will accept crypto as payment, either through expanded offerings from existing PSPs or via crypto-native payment processors delivering better experiences.

-

Card networks will expand to cover about 240 countries and regions (currently ~210), using stablecoins as last-mile solutions.

-

The majority of remittance volume across 15 global corridors will flow via crypto payment rails.

-

On-chain privacy primitives will eventually be adopted, driven by enterprises and nations using crypto payment rails rather than consumers.

-

10% of all foreign aid disbursements will be sent via crypto payment rails.

-

The on/off-ramp market structure will consolidate, with 2–3 providers capturing most transaction volume and partnerships in each country.

-

The number of P2P ramp liquidity providers will rival that of food delivery drivers in their operating countries. As volume grows, being an agent becomes economically sustainable and continues to offer FX rates at least 5–10% cheaper than banks.

-

>10 million remote workers, freelancers, and contractors will receive compensation via crypto payment rails (directly in stablecoins or local currency).

-

99% of AI agent commerce (including agent-to-agent, agent-to-human, and human-to-agent) will occur on-chain via crypto payment rails.

-

>25 well-known U.S. partner banks will support companies operating on crypto payment rails, eliminating bottlenecks worsened by operational constraints.

-

Financial institutions will experiment with issuing their own stablecoins to facilitate global real-time settlement.

-

Standalone “crypto Venmo” apps will still fail to gain traction due to overly niche user personas, but large messaging platforms like Telegram will integrate crypto payment rails and begin enabling P2P payments and remittances.

-

Loan and credit companies will begin collecting and disbursing via crypto payment rails to improve working capital, thanks to reduced capital locked up during transit.

-

Several non-USD stablecoins will begin large-scale tokenization, giving rise to on-chain FX markets.

-

CBDCs will remain in experimental stages due to bureaucratic hurdles, failing to reach commercial scale.

VI. Conclusion

As Stripe CEO Patrick Collison stated, crypto rails are superconductors for payments. They form the foundation of a parallel financial system that enables faster settlement, lower fees, and seamless cross-border operations. This idea took ten years to mature, but today we see hundreds of companies working to make it real. Over the next decade, we will see crypto rails become central to financial innovation and drive global economic growth.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News