Why is the economy still booming despite tight monetary policy?

TechFlow Selected TechFlow Selected

Why is the economy still booming despite tight monetary policy?

Maybe it's because we've been focusing on the wrong metrics.

Author: Alp Simsek, Professor of Finance at Yale School of Management

Translation: Tia, Techub News

Editor's Note:

In the current global economic environment, the Federal Reserve's monetary policy is receiving unprecedented attention. Although policy rates have risen to historical highs, the U.S. economy remains strong—a phenomenon that seems to defy expectations from traditional economic theory. The persistently hot labor market and steady economic growth raise an important question: why hasn't tight monetary policy effectively curbed overheating as it has in the past? Recent research suggests this is not a paradox, but rather a limitation of conventional analytical frameworks. By re-examining how financial conditions affect the economy, we can gain deeper insight into the actual transmission mechanism of monetary policy.

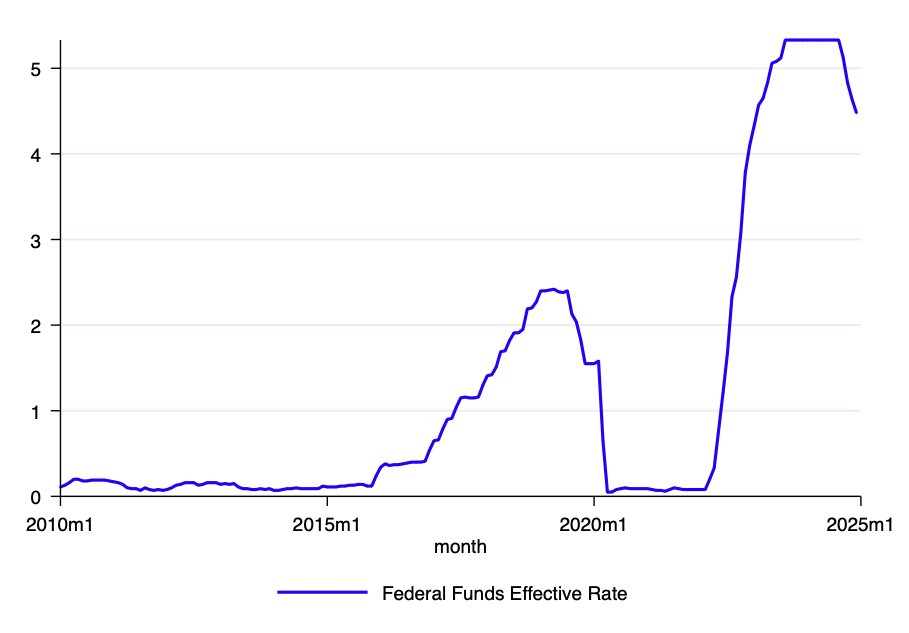

The Fed has raised interest rates to historic levels, yet the economy continues to expand—strong employment reports are proof of that. Why is this happening?

According to our latest paper, it may be because we’re watching the wrong indicators.

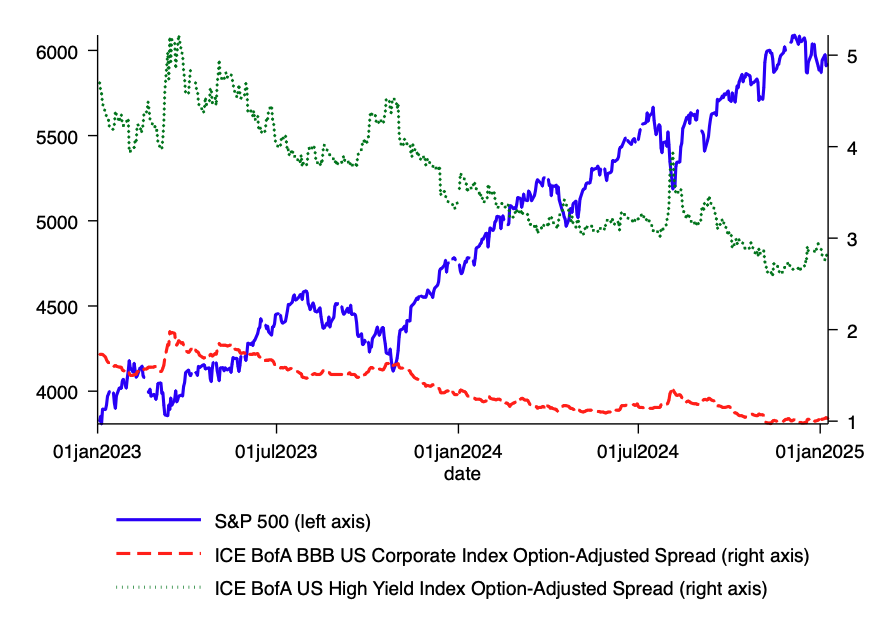

Although policy rates are high, financial conditions are actually quite accommodative. Rising stock markets and tightening credit spreads have effectively offset much of the Fed’s tightening efforts.

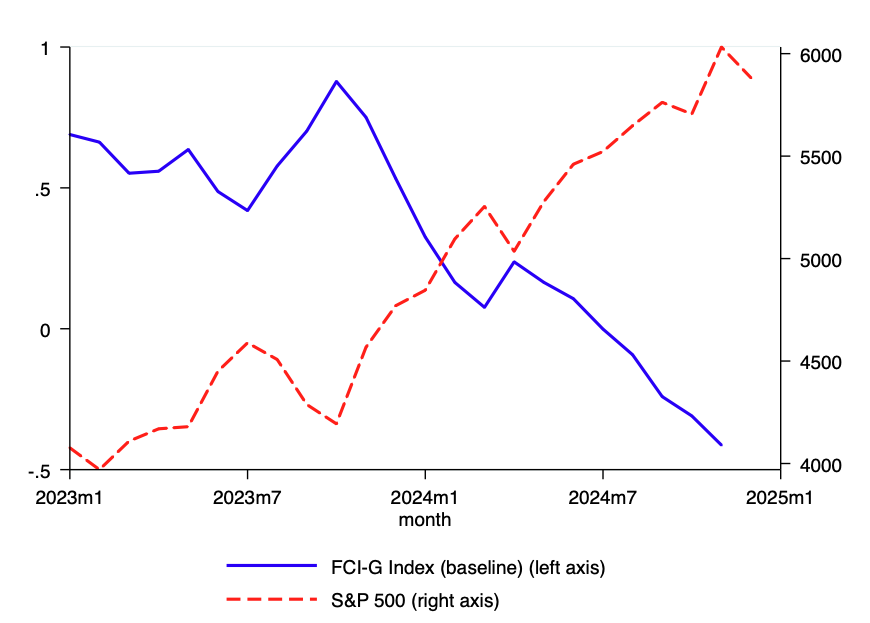

Data shows that the Fed’s own FCI-G index—a composite measure of financial variables designed to gauge their impact on economic growth—confirms this. While long-term interest rates have risen and the dollar has strengthened, positive market developments (primarily stock market gains and improved credit spreads) are stimulating growth.

Tight monetary policy alongside strong growth is not a paradox after all.

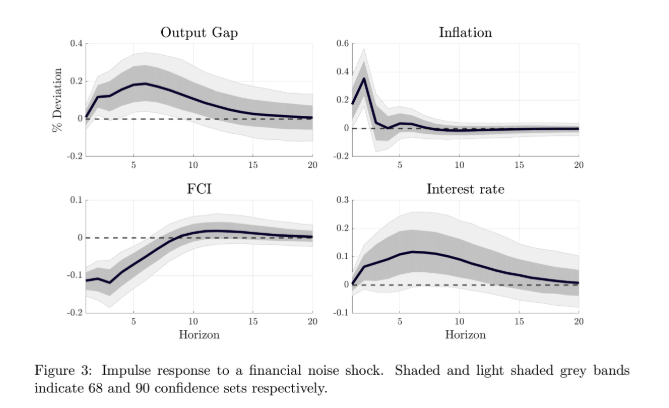

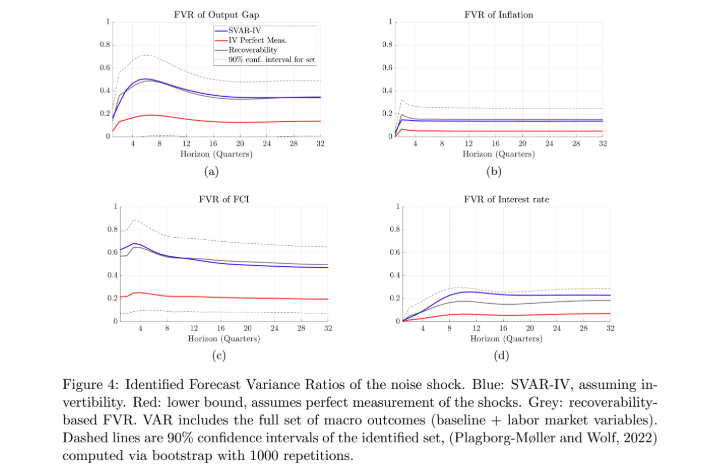

In our research with Ricardo Caballero and @TCaravello, we show that what matters for the economy is not the policy rate itself, but broader financial conditions.

Our analysis indicates that when financial conditions ease—even if driven by noisy asset demand (sentiment)—it stimulates output and inflation, ultimately forcing interest rates higher. This aligns with what we observe today.

Quantitatively, our research finds that financial conditions account for up to 55% of fluctuations in economic output.

Moreover, the primary channel of monetary policy transmission should be through its effect on financial conditions, not direct interest rate effects.

The current situation fits this framework: despite high interest rates, accommodative financial conditions are supporting strong growth and could prevent inflation from returning to target.

Looking ahead, this suggests the Fed’s job is not yet done. To achieve the 2% inflation target, financial conditions may need to tighten.

This could happen via: market adjustment – stronger dollar – further rate hikes.

The path of interest rates will depend largely on market dynamics. If markets adjust and the dollar strengthens, current rate levels might suffice. But if financial conditions remain loose, further rate hikes may be necessary.

This framework implies that Fed watchers should pay less attention to debates over the “terminal rate” and more attention to the evolution of financial conditions. That’s where real monetary policy transmission occurs.

While our paper goes further by proposing an explicit FCI targeting rule, the more fundamental point is that we need to change how we think and talk about monetary policy. The policy rate is just an input—the true driver is financial conditions.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News