Foresight Ventures PayFi Report (Part 1): Industry Panorama Analysis

TechFlow Selected TechFlow Selected

Foresight Ventures PayFi Report (Part 1): Industry Panorama Analysis

Explore the reasons behind the rise of PayFi, provide an overview of the current state of its industry, list key cases, and uncover its potential application scenarios.

Author: Kedar@Foresight Ventures, Alice@Foresight Ventures

Contributor: Max Hamilton @Foresight Ventures

PayFi: The Transformative Force in Financial Transactions

In today's world, cross-border payments often take days, and businesses must bear transaction fees amounting to billions of dollars annually. PayFi emerges as an innovative solution that combines the advantages of decentralized finance (DeFi) with the immediacy of modern payment systems, promising to reshape the future of transactions.

As the global financial landscape continues to evolve, PayFi stands at the intersection of blockchain technology and payment systems, aiming to merge DeFi’s efficiency with the instantaneity and convenience of modern payment solutions to transform how transactions are conducted. This article will explore the reasons behind PayFi’s emergence, outline the current state of its industry, present key case studies, and uncover its potential applications.

1. The Emergence and Advantages of PayFi

(1) Bridging the Gap Between DeFi and Payments

Traditional financial systems have long suffered from inefficient settlement processes—slow processing times, high transaction costs, and limited accessibility—all of which were starkly exposed during the 2008 financial crisis. While DeFi has introduced innovative financial services through decentralized platforms, it lacks real-time transaction processing capabilities for everyday use.

PayFi leverages blockchain technology to enable real-time transaction settlement. Based on the Time Value of Money (TVM) theory—which holds that money available now is worth more than the same amount in the future due to its earning potential—PayFi maximizes financial efficiency by enabling immediate, secure, and low-cost transactions.

(2) Unique Advantages of PayFi

-

Real-Time Settlement: Transactions are completed instantly, eliminating delays inherent in traditional banking systems.

-

Security and Reliability: The immutable ledger feature of blockchain ensures transparent and secure transactions, providing users with strong safeguards.

-

Cost Reduction: By removing intermediaries, transaction fees are significantly reduced, saving users money.

-

Global Accessibility: Its decentralized platform reaches markets underserved by traditional financial services, including the unbanked, promoting financial inclusion.

-

Innovative Products: Enables novel financial service models such as "buy now, pay never," and provides creators with advanced monetization methods.

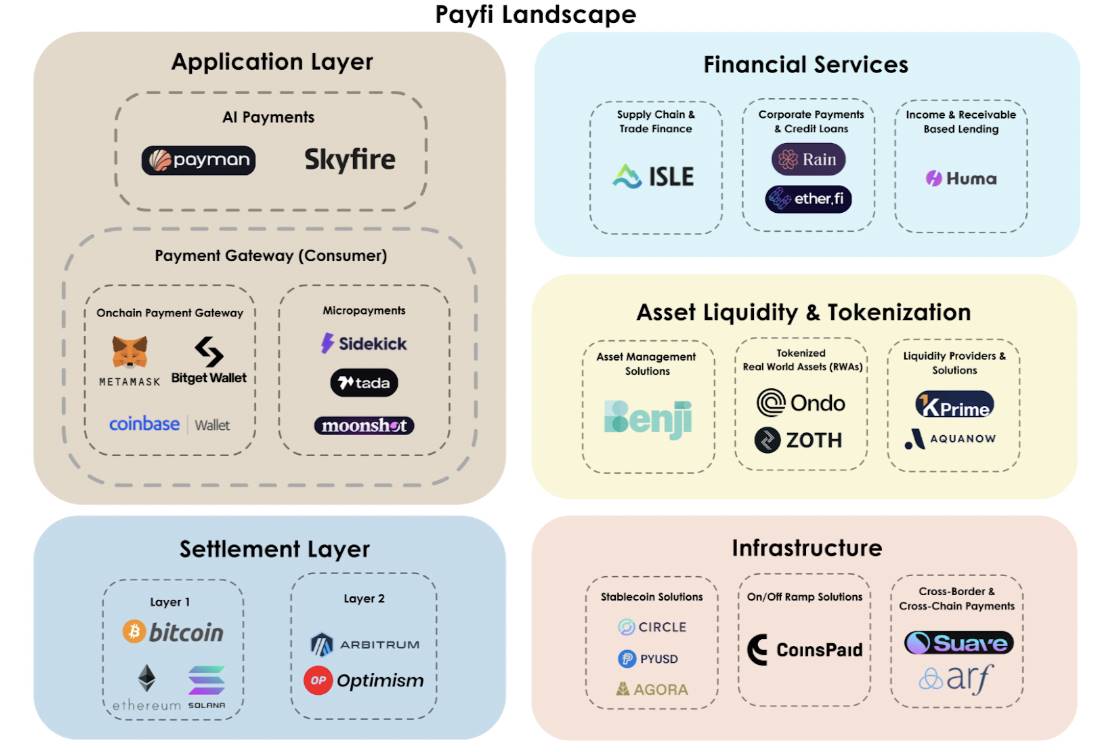

2. Industry Landscape and Segment Insights in PayFi

The PayFi ecosystem is rapidly expanding, with innovation emerging across sectors to address financial challenges. Below is an analysis of key segments and examples of pioneering companies within each area.

(1) Cross-Chain and Cross-Border Payments

Chronic Issues in Traditional Cross-Border Payments

-

Slow Speeds and High Latency: Traditional payment channels are inefficient, often requiring several days for settlement. Complex processes across time zones and banking hours further exacerbate delays.

-

Inefficient Capital Use and Pre-Funded Account Constraints: Requirements to pre-fund nostro accounts force financial institutions to hold foreign currency reserves, creating a $4 trillion global liquidity gap. Idle funds generate no returns, representing a hidden cost passed on to end users, resulting in higher fees.

-

High Transaction Costs: Multiple intermediary fees—including pre-funding charges and currency conversion fees—make the average cost of global remittances as high as 6.35% (World Bank data).

Industry Innovation Cases

-

Arf: Builds a regulated global settlement banking platform offering financial institutions on-chain liquidity solutions. Leveraging stablecoins like USDC, Arf enables fast and low-cost cross-border settlements. It uses blockchain to provide real-time liquidity on demand, reducing reliance on nostro accounts. Arf also offers instant credit lines in USDC, allowing institutions to temporarily borrow funds during transactions and repay after settlement. By abandoning pre-funded account models, Arf’s short-term USDC-based liquidity solutions significantly reduce capital requirements and settlement times, cutting operational costs for global traders. Emphasizing transparency, Arf creates fully traceable lending records—loan, repayment, and receivable data can be easily audited on-chain. Committed to strict compliance, Arf is a member of the VQF Association of Financial Services Standards and adheres to international AML and financial regulations, setting an industry benchmark. To date, it has processed over $1.6 billion in on-chain transactions with zero defaults.

-

suave.money: Develops a cross-chain payment solution enabling businesses to accept crypto payments from any blockchain network. Companies can seamlessly integrate various token payments and flexibly choose which tokens to receive, enhancing payment flexibility across blockchain ecosystems. suave.money simplifies cross-chain transactions—enterprises need not manage multiple wallets or rewrite dApps—allowing them to attract user bases from different blockchain networks and expand customer reach. By facilitating payments from over ten blockchain networks, it enhances liquidity access and supports the growth of DeFi and Web3 projects. Simplifying cross-chain operations reduces enterprise complexity, enabling broader customer engagement without investing in specialized infrastructure. Through innovation, suave.money helps businesses unlock trillions in cross-chain capital potential, securing a significant position in the fast-evolving DeFi and crypto payments space, delivering unparalleled flexibility and convenience to users.

(2) Income and Receivables-Based Lending

-

Challenges of Traditional Lending Models: Conventional lending relies heavily on collateral, excluding borrowers who lack substantial assets or credit history, limiting financial inclusivity and fairness.

-

Rise of Innovative Solutions: Platforms like Huma Finance allow users to borrow against future income or receivables, using blockchain to make lending transparent and efficient.

-

Positive Impact: This model greatly improves financial inclusion by providing new funding avenues for underserved markets overlooked by traditional institutions, fostering balanced economic development and social equity.

-

Huma Finance Case Study: Builds a decentralized lending protocol offering borrowing based on future income and receivables for individuals and businesses. Its on-chain platform connects borrowers with global investors, pioneering income-backed lending as an alternative to traditional over-collateralized DeFi models. In collaboration with Circle, Request Network, and Superfluid, Huma launched the world’s first on-chain factoring market on Ethereum and Polygon, enabling users to pledge tokenized invoices or payment streams as collateral—expanding both the scope and form of acceptable collateral. Leveraging blockchain efficiency, the factoring process takes less than one minute on-chain, delivering a seamless user experience. Huma’s technical architecture consists of several key components: the Decentralized Income Portfolio layer transforms diverse income sources—such as invoices, payrolls, and staking rewards—into tokenizable assets, forming a rich foundation for lending; the Evaluation Agent Framework conducts precise risk assessments for various loan requests, ensuring reliable and stable on-chain credit quality; and a suite of smart contracts enables diverse lending use cases—from invoice factoring to general credit lines—through configurable logic, meeting personalized user needs. Focusing on SMEs and the unbanked, Huma provides critical liquidity support, helping these groups overcome traditional financial barriers to access previously inaccessible capital, driving their economic development and social integration, and contributing positively to building a fairer, more inclusive financial ecosystem.

(3) Tokenization of Real-World Assets

-

Challenges in Traditional Asset Trading: Trading real-world assets like real estate is cumbersome, costly due to intermediaries, and slow, burdening buyers and sellers alike.

-

Innovative Breakthrough via Tokenization: Tokenizing real estate and other real-world assets allows ownership to be divided into fractional shares via smart contracts, enabling partial ownership trading while dramatically accelerating transaction speed and process efficiency, injecting new vitality into asset markets.

-

Significant Benefits: This model lowers investment entry barriers, enabling broader participation in real-world asset investing, while greatly enhancing asset liquidity, accelerating buy-sell cycles, and improving overall market efficiency and resource allocation.

-

Ondo Finance Success Story: Launches tokenized U.S. Treasuries and other yield-generating products on blockchain platforms, opening new investment avenues. Investors gain easy, DeFi-based access to short-term U.S. Treasuries and fixed-income assets, effectively bridging traditional finance and DeFi. Ondo’s innovative offerings provide investors with stable, high-yield, liquid, and secure investment options, breaking down barriers between traditional finance and DeFi. This allows more investors to share in the benefits of traditionally closed capital markets, enriching portfolio diversification and boosting overall market efficiency. As of September 2024, Ondo Finance achieved remarkable success in tokenized U.S. Treasury products, surpassing $600 million in total value locked (TVL). USDY (yield-bearing stablecoin) reached $384 million in TVL, while OUSG (tokenized U.S. Treasury) hit $221 million—clear evidence of strong market recognition and acceptance, affirming Ondo’s leadership and influence in real-world asset tokenization.

-

Zoth’s Innovation: Operates a dedicated marketplace for tokenized trade finance assets, offering investors convenient access to dollar-denominated fixed-income products. By tokenizing traditional financial assets such as trade receivables and corporate bonds, Zoth bridges traditional finance and DeFi, creating high-return, low-risk investment opportunities for investors while providing businesses with new financing and capital management tools. Zoth plays a vital role in the market—not only offering premium investment options for wealth preservation and growth but also supporting business development. By unlocking working capital more efficiently through tokenized trade assets, enterprises can optimize capital structures, enhance competitiveness, and strengthen risk resilience. Additionally, this promotes optimal global capital allocation, directing financial resources more rationally toward enterprises and projects in need, further refining the on-chain trade finance ecosystem and making positive contributions to overall financial stability and growth.

(4) Enterprise Payment and Credit Solutions

Consumer Demand vs. Traditional Credit Limitations: Today’s consumers demand greater payment flexibility, expecting convenient and diverse options without the burden of debt. However, traditional credit models often fail to meet these needs, causing inconvenience and financial strain.

PayFi’s Innovative Model: To address this, PayFi introduces unique payment models such as “buy now, pay never,” cleverly using interest earned from DeFi lending platforms to offset purchase costs. This offers consumers a completely new, flexible, and debt-free payment solution, significantly enhancing purchasing power and shopping experience.

Industry Innovation Cases

-

Rain: Offers a USDC-backed corporate card tailored for Web3 teams (e.g., DAOs and protocol projects) to handle daily business expenses. With this card, Web3 teams can conveniently use on-chain assets like USDC to pay for travel, office supplies, and other operational costs—eliminating the need for complex crypto-to-fiat conversions and streamlining corporate payments. As a core component of Rain’s spending management platform, the card leverages blockchain to seamlessly connect digital assets with traditional payment systems. This innovative approach enables more efficient financial management, reduces intermediary costs and delays, and provides blockchain-native businesses with a smoother, safer payment solution—accelerating Web3 industry growth and adoption.

-

Ether.fi: Its “Ether.fi Cash” product has attracted significant market attention—a Visa-branded credit card with unique features. Users can easily obtain a credit line by pledging their crypto assets (including various Ethereum-based tokens), enabling fiat spending without selling their holdings, offering greater financial flexibility and improved consumer experience. Moreover, the card is deeply integrated with Scroll, an Ethereum Layer 2 network, significantly reducing transaction costs and enhancing cost-effectiveness. It also supports peer-to-peer USDC transfers, enabling easier fund management across use cases while bypassing traditional bank intermediaries to save fees. To boost user engagement and satisfaction, Ether.fi Cash offers attractive cashback rewards, delivering tangible economic benefits and strengthening product competitiveness and retention.

-

Bitget Card: Serves as a crucial bridge between cryptocurrency and traditional payment systems, offering users a convenient and efficient payment solution. Linked to a multi-currency wallet, businesses and individuals can easily hold, convert, and spend major cryptocurrencies such as USDT, BTC, ETH, USDC, and BGB (currently funded primarily in USDT, with plans to add more cryptos). During payments, Bitget Card automatically converts crypto to fiat at real-time exchange rates, enabling smooth transactions at any Visa-accepting merchant worldwide—removing the hassle of manual conversion and exchange rate risks. This truly achieves seamless crypto-fiat integration, offering unmatched convenience. The card significantly impacts enterprise payments: it simplifies workflows by eliminating manual crypto-fiat conversion, enabling real-time fiat spending and improving payment and capital efficiency. Its powerful cross-border capabilities empower companies in international expansion, reducing the burden of managing foreign currency accounts and lowering operational and financial risks. Currently accepted in over 180 countries and regions, Bitget Card strongly supports global business growth. Furthermore, it unlocks rich DeFi use cases—for example, in supplier payments, enterprises can directly pay suppliers in fiat, avoiding complex crypto conversions and improving supply chain payment efficiency; in travel reimbursement, employees can easily cover business expenses like flights and hotels abroad without payment restrictions or fees, facilitating smoother cross-border operations; in employee incentives, companies can issue crypto-based rewards via Bitget Card, allowing staff to convert to fiat or spend directly where crypto is accepted—adding innovation and flexibility to compensation programs and enhancing employer attractiveness and competitiveness.

(5) Supply Chain and Trade Finance

Challenges in Traditional Supply Chain Finance: In conventional supply chain finance, suppliers often face long and complex payment cycles, locking up significant capital and severely constraining operational efficiency, cash flow, and business growth. Statistics show that globally, $2.5 trillion in annual trade finance demand remains unmet due to limitations of traditional financial institutions—an ongoing bottleneck hindering global trade, supply chain collaboration, and economic stability.

PayFi’s Solution: PayFi introduces decentralized platforms to solve invoice financing issues in supply chain finance. Under this model, suppliers leverage blockchain to tokenize outstanding invoices and quickly raise funds on decentralized markets, gaining immediate liquidity and dramatically improving cash flow. Meanwhile, buyers can continue settling according to original schedules, preserving existing payment habits and financial workflows—balancing interests between buyers and suppliers and ensuring efficient supply chain operations.

Industry Innovation Case

-

Isle Finance: A leading on-chain credit market focused on supply chain finance, Isle’s platform precisely matches high-credit buyers with liquidity providers, enabling faster corporate funding. It skillfully applies blockchain technology by rigorously verifying real-world assets (RWAs) and implementing early-payment strategies—particularly benefiting low-credit-rated suppliers—greatly enhancing supply chain liquidity and security. Isle actively promotes reverse factoring, significantly accelerating payment cycles and optimizing cash flow. This blockchain-based innovation allows businesses to offer early-payment discounts, generating stable and attractive returns in supply chain finance, while broadening liquidity sources and fueling sustainable growth.

(6) Stablecoin Payment Platforms

Example: Agora

-

Business: Developed the U.S. Digital Dollar (AUSD), fully backed by cash, U.S. Treasuries, and overnight repurchase agreements. The platform is committed to leveraging blockchain to enable broader, more accessible global circulation of the U.S. dollar—especially in regions underserved by traditional finance—advancing financial inclusion and opening new pathways for individuals to access a stable, globally recognized currency.

-

Impact: Democratizes access to the U.S. dollar, aligning closely with PayFi’s vision of expanded financial inclusion. By harnessing blockchain, Agora builds a decentralized and accessible financial system, allowing individuals and businesses to benefit from dollar-backed financial tools—achieving notable success in regions like Argentina and Southeast Asia, supporting local economic development and financial stability.

-

Achievements: Successfully launched stablecoin AUSD initially on Ethereum, later expanding to Avalanche. Impressively, minting volume surpassed $20 million within weeks of launch. Today, the platform is steadily advancing its global rollout of digital dollars, expanding internationally while maintaining a strategic focus on financial inclusion and regulatory compliance—building a solid reputation and growing influence in the stablecoin space.

Example: PayPal

-

Business: Officially launched PayPal USD (PYUSD) in August 2024 on Ethereum, then expanded to Solana in May 2024. Designed to integrate the strengths of both blockchains, PYUSD delivers fast, low-cost digital payments. After moving to Solana, its superior speed and low fees significantly enhanced usability across commercial and DeFi applications, offering users a more efficient and convenient payment option.

-

Impact: With its speed and cost-efficiency, PYUSD is poised to become a compelling alternative to traditional payment systems, substantially improving global payment efficiency. It enables seamless transfers across platforms—including PayPal and Venmo—allowing users to easily hold and move stablecoins while fully leveraging blockchain advantages, bringing greater convenience and innovation to digital asset management and payments.

-

Achievements: Following its expansion to Solana, PYUSD adoption surged, with market cap rapidly exceeding $500 million. This milestone highlights its deep integration and wide acceptance across centralized and decentralized platforms, marking a significant achievement in PayPal’s stablecoin journey and laying a solid foundation for future growth in digital payments.

Example: Bridge (Acquired by Stripe)

-

Business: Bridge, a stablecoin payment platform, focuses on simplifying cross-border digital payments. Through user-friendly APIs, it enables effortless integration of stablecoin-based payments, offering low-cost, high-efficiency cross-border transaction solutions. Before acquisition, Bridge achieved notable success in e-commerce integrations, helping merchants worldwide seamlessly adopt and efficiently process stablecoin payments—greatly expanding stablecoin usage in commerce.

-

Impact: Its recent acquisition by U.S. payments giant Stripe marks a key milestone in stablecoin integration into mainstream finance. Leveraging Stripe’s robust infrastructure and vast network, Bridge can expand its reach and capabilities, delivering more seamless and efficient stablecoin payment and settlement services to global enterprises. This aligns perfectly with PayFi’s vision of promoting financial inclusion and frictionless cross-border transactions to accelerate global adoption of digital currencies. By combining Stripe’s scale with Bridge’s stablecoin expertise, this move is expected to drive broader adoption and deeper integration of blockchain-powered payments into mainstream financial channels, injecting fresh momentum into global payment innovation.

-

Achievements: In August 2024, Bridge achieved an annualized payment volume exceeding $5 billion. Throughout its journey, Bridge has built close partnerships with industry leaders such as Coinbase and SpaceX, continuing to serve them with high-quality payment solutions—accumulating rich practical experience and strong market credibility, positioning itself as a key driver in the evolution of the stablecoin payments sector.

Conclusion

In summary, PayFi is not an entirely new concept. The problems it aims to solve already exist in traditional finance, and there have been attempts to address them. However, this does not diminish PayFi’s value—existing solutions remain incomplete. By tackling core inefficiencies in global payment systems and harnessing the transformative power of blockchain, PayFi has the potential to unlock unprecedented liquidity and advance financial inclusion. As more companies innovate in this space, the vision of a fully decentralized financial ecosystem—where payments are instant, secure, and borderless—is becoming increasingly attainable. Now is the time to embrace the PayFi revolution and shape the future of global finance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News