Dephi Digital Stablecoin Research: Financial Tech Giants Enter, Revenue-Sharing Models Evolve, Future Potential Underestimated

TechFlow Selected TechFlow Selected

Dephi Digital Stablecoin Research: Financial Tech Giants Enter, Revenue-Sharing Models Evolve, Future Potential Underestimated

Although it's still uncertain whether 2025 will become a turning point year for stablecoins, one thing is certain: we've never been closer to that moment.

Author: Robbie Petersen

Translation: TechFlow

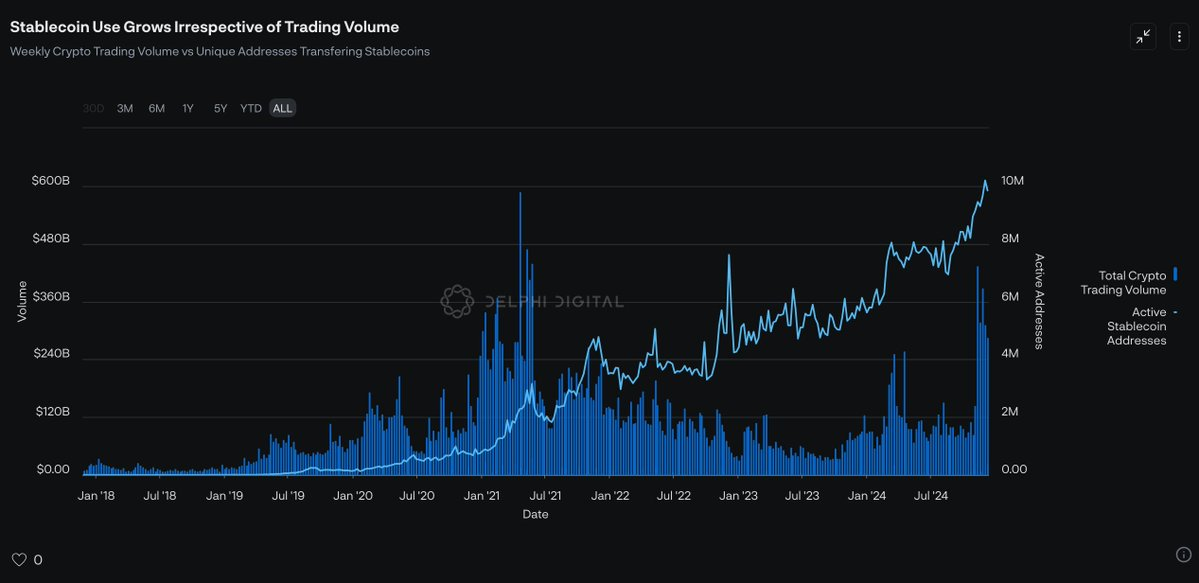

While the total supply of stablecoins continues to rise steadily, this seemingly positive growth masks a more significant underlying trend. Although trading volume on crypto exchanges has yet to recover to historical highs, the number of monthly active addresses using stablecoins for transactions keeps increasing. This divergence suggests a fundamental shift in the role of stablecoins—they are no longer merely lubricants for speculation within the crypto market but are gradually fulfilling their core promise: becoming the foundation of a new digital financial system.

Data source: Artemis, The Tie

(From Delphi's "DeFi Outlook 2025" report)

Perhaps even more significant is that the driving force behind widespread stablecoin adoption may no longer come from emerging startups but from established companies with strong market reach. In the past three months alone, four leading fintech firms have announced formal entries into the stablecoin space: Robinhood and Revolut are developing their own stablecoins; Stripe acquired Bridge to enable faster, lower-cost global payments; and Visa, despite knowing it could cut into its own profits, has begun helping banks issue stablecoins.

These moves mark a major shift in stablecoin adoption: their popularity is no longer driven by ideology or technological idealism, but by clear commercial value. Stablecoins offer tangible benefits to fintech companies—lower operating costs, higher margins, and new revenue streams. As such, they are increasingly aligning with capitalism’s core driver: the pursuit of profit.

As industry-leading fintech firms use stablecoins to boost profitability or capture more of the payment stack, competitors will be forced to follow suit to remain competitive. As I noted in the “Stablecoin Manifesto”, from a game-theoretic perspective, adopting stablecoins will no longer be optional—it will become essential for any fintech company seeking to maintain its market position.

Stablecoin 2.0: Revenue-Sharing Stablecoins

Intuitively, the most obvious beneficiaries in the stablecoin ecosystem are the issuers. This is due to the “winner-takes-all” nature of the stablecoin market, which stems from the network effects of money. Currently, these network effects manifest in three key ways:

-

Liquidity: USDT and USDC are the most liquid stablecoins in the crypto market. Using newer forks of USDT may result in higher slippage during trades.

-

Payment utility: In many emerging economies, USDT has become a common means of payment. As a digital medium of exchange, its network effect is extremely powerful.

-

Pricing dominance: Nearly all major trading pairs—on both centralized and decentralized exchanges—are priced in USDT or USDC.

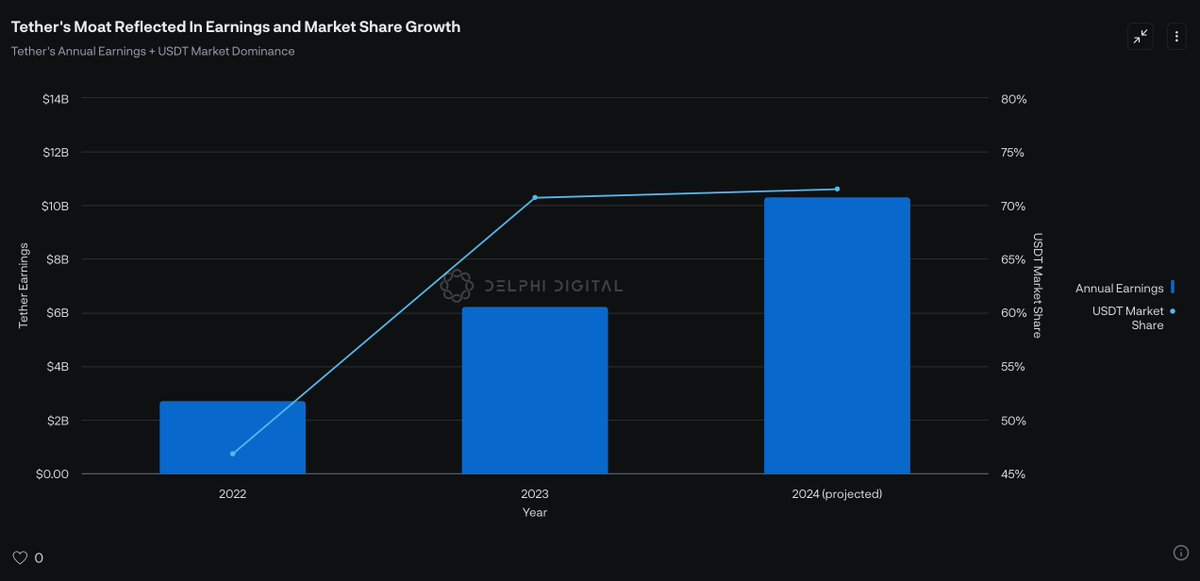

In short, the more users USDT has, the more new users it attracts. This self-reinforcing network effect has allowed Tether to continuously expand its market share while boosting profitability.

Although Tether’s network effects are difficult to disrupt at scale in the short term, an emerging model—revenue-sharing stablecoins—is beginning to gain traction. This model is particularly well-suited for the new stablecoin ecosystem driven by fintech companies. To understand its potential, we must first examine the basic structure of the stablecoin economy.

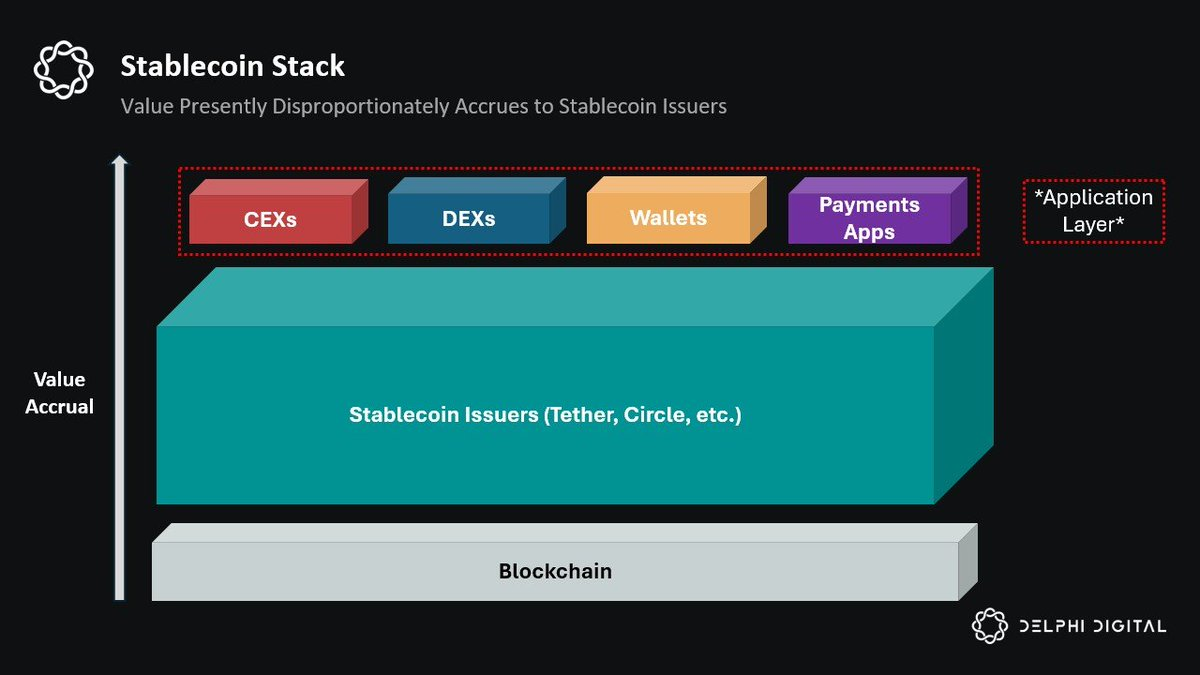

Currently, the stablecoin ecosystem consists of two main roles: (1) stablecoin issuers (e.g., Tether and Circle) and (2) stablecoin distributors (e.g., various applications).

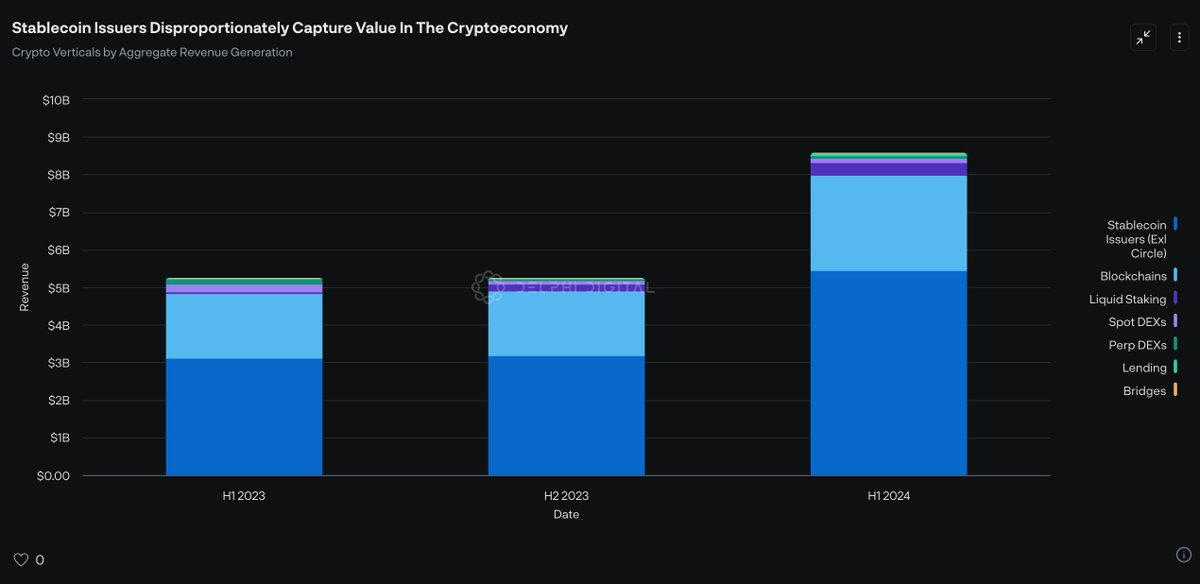

Today, stablecoin issuers generate over $10 billion in annual revenue—more than the combined revenue of all blockchains. Yet this arrangement reveals a critical structural flaw: the actual value of stablecoins is driven by distributors. In other words, without distribution channels like exchanges, DeFi apps, payment platforms, and wallets, USDT would have no utility and thus could not capture any value. Yet these distributors currently receive no economic benefit from this activity.

To address this imbalance, revenue-sharing stablecoins have emerged. This model fundamentally reshapes the existing stablecoin economy by redistributing a portion of the issuer’s revenue to applications that provide liquidity and distribution. In simple terms, revenue-sharing stablecoins allow apps to monetize their distribution power.

If scaled widely, this model could become a major—or even primary—source of income for applications. As profit margins tighten across industries, we may enter an era of “Stablecoin Distribution as a Service” (SDaaS), where crypto applications adopt stablecoin distribution as a core business model. This shift makes sense: stablecoin issuers today capture more value than all blockchain protocols and applications combined.

Despite countless attempts to challenge Tether’s dominance in the past, the revenue-sharing stablecoin model stands out for two key reasons:

-

Channel-centric approach: Unlike earlier yield-bearing stablecoins that targeted end users directly, revenue-sharing stablecoins focus on distribution channels—the entities that control user access. For the first time, this aligns the incentives of distributors and issuers.

-

Ecosystem synergy: Previously, if an application wanted to benefit economically from stablecoins, it had to launch its own standalone stablecoin. But this approach was limited—other apps had little incentive to integrate it, and its utility remained confined within the issuing app, unable to compete with USDT’s network effects. In contrast, revenue-sharing stablecoins incentivize multiple apps to integrate simultaneously, leveraging the collective network effect of the entire distribution ecosystem.

Revenue-sharing stablecoins not only inherit the advantages of USDT—such as cross-application composability and strong network effects—but also further incentivize distribution partners by sharing revenue with the application layer.

Currently, there are three leading players in the revenue-sharing stablecoin space:

-

Paxos’ USDG: Launched in November and designed to comply with Singapore’s upcoming stablecoin regulatory framework from the Monetary Authority of Singapore (MAS). Paxos has already partnered with several major platforms to integrate USDG, including Robinhood, Kraken, Anchorage, Bullish, and Galaxy Digital.

-

M^0’s “M”: Built by former core team members of MakerDAO and Circle, M^0 aims to serve as a lean, trust-minimized settlement layer enabling any financial institution to mint and redeem its revenue-sharing stablecoin “M.” Unlike others, “M” can also act as an underlying asset for other stablecoins (e.g., Noble’s USDN). Additionally, M^0 employs a unique custody model composed of a decentralized network of independent validators and a Two Token Governor (TTG) governance system, offering greater transparency and credible neutrality compared to other models. More details in my article [Link pending].

-

Agora’s AUSD: Similar to USDG and “M,” Agora shares revenue with integrated applications and market makers to attract partnerships. Agora has backing from prominent market makers and apps, including Wintermute, Galaxy, Consensys, and Kraken Ventures—aligning key stakeholders’ incentives early on. AUSD’s total supply has already reached $50 million.

Looking ahead to 2025, I expect these stablecoin issuers to further expand their influence. Distributors may begin prioritizing stablecoins that offer higher revenue shares, and market makers may favor holding inventory in revenue-sharing stablecoins, knowing they can earn yields on large holdings.

Although “M” and AUSD currently rank 33rd and 36th by stablecoin supply respectively, and USDG has not yet launched, I predict that by the end of 2025, at least one of them will break into the top ten. Meanwhile, the market share of revenue-sharing stablecoins is expected to grow from the current 0.06% to over 5%—an 83-fold increase. With major fintech players entering the space, these stablecoins are poised for a new wave of adoption.

Slow Buildup, Sudden Breakout

Although stablecoin adoption is often compared to the historical development of Eurodollars, this analogy oversimplifies reality. Stablecoins are not Eurodollars—they are digital; globally accessible without barriers; capable of instant cross-border settlement; usable by AI agents; exhibit strong network effects at scale; and crucially, offer clear economic incentives to existing fintech firms and enterprises by aligning with every company’s core objective: earning more profit.

Therefore, the view that stablecoin adoption will unfold slowly, like Eurodollars, overlooks a key truth. The only similarity between stablecoins and Eurodollars may be their bottom-up emergence, resistant to control by any incumbent giant or government—especially those who perceive the technology as a threat. But unlike Eurodollars, stablecoin adoption won’t take 30 to 60 years. Instead, it will follow a “slow buildup, sudden breakout” trajectory, as network effects rapidly reach a tipping point.

Today, the stablecoin ecosystem is rapidly taking shape. Regulatory frameworks are maturing; fintech firms like Robinhood and Revolut have begun launching their own stablecoins; Stripe appears to be exploring how stablecoins can help it capture more of the payment stack. Most strikingly, even PayPal and Visa—despite knowing stablecoins may erode their profits—are actively building in this space, fearing that if they don’t act, competitors will seize the opportunity first.

While it remains uncertain whether 2025 will be the year stablecoins finally break through, one thing is certain: we’ve never been closer.

Perhaps we’re still underestimating the true potential of stablecoins.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News