From BitUSD to USDT: The Ten-Year Evolution of Stablecoins from Payment Tools to Financial Infrastructure

TechFlow Selected TechFlow Selected

From BitUSD to USDT: The Ten-Year Evolution of Stablecoins from Payment Tools to Financial Infrastructure

As stablecoins continue to bridge traditional finance and cryptocurrency, their future will depend on finding a balance between innovation and effective regulation.

Author: insights4.vc

Translation: TechFlow

It has been ten years since the first stablecoin, BitUSD, was launched, marking a significant evolution in the decentralized finance (DeFi) ecosystem. Today, stablecoins have become an indispensable financial tool in this space, with a total supply exceeding $156 billion. BitUSD was introduced on July 21, 2014, on the BitShares blockchain by cryptocurrency pioneers Dan Larimer and Charles Hoskinson, aiming to maintain a stable 1:1 value peg to the U.S. dollar. However, BitUSD’s de-pegging event in 2018 revealed the complexities of early stablecoin models.

In contrast, modern stablecoins such as Tether (USDT) and USD Coin (USDC) rely on substantial fiat reserves and robust mechanisms to achieve notable stability. Today’s stablecoins play a vital role in the cryptocurrency and DeFi ecosystems, providing liquidity for exchanges, supporting collateralized lending, and enabling market participants to remain invested in digital assets without frequently converting back to fiat currencies.

Types of Stablecoins

Stablecoins can be categorized based on their methods for maintaining price stability:

-

Fiat-collateralized stablecoins: These stablecoins are backed by fiat currency reserves (such as the U.S. dollar), held by centralized custodians. Examples include Tether (USDT) and USD Coin (USDC). Issuers hold fiat reserves equivalent to the issued stablecoins, ensuring each coin can be redeemed at a 1:1 ratio. This mechanism not only stabilizes value but also enhances user trust.

-

Crypto-collateralized stablecoins: These stablecoins are backed by other cryptocurrencies, such as MakerDAO's DAI. Users must lock up a certain amount of crypto assets (e.g., Ethereum) as collateral. Due to the high volatility of cryptocurrencies, these stablecoins typically use over-collateralization and automated liquidation mechanisms to maintain their peg.

-

Algorithmic stablecoins: These stablecoins rely on algorithms to adjust supply according to market demand, without requiring physical collateral. For example, FRAX combines algorithmic mechanisms with partial collateralization, while TerraUSD (UST) previously used a seigniorage model before its collapse. Their stability heavily depends on market confidence and the robustness of their algorithms.

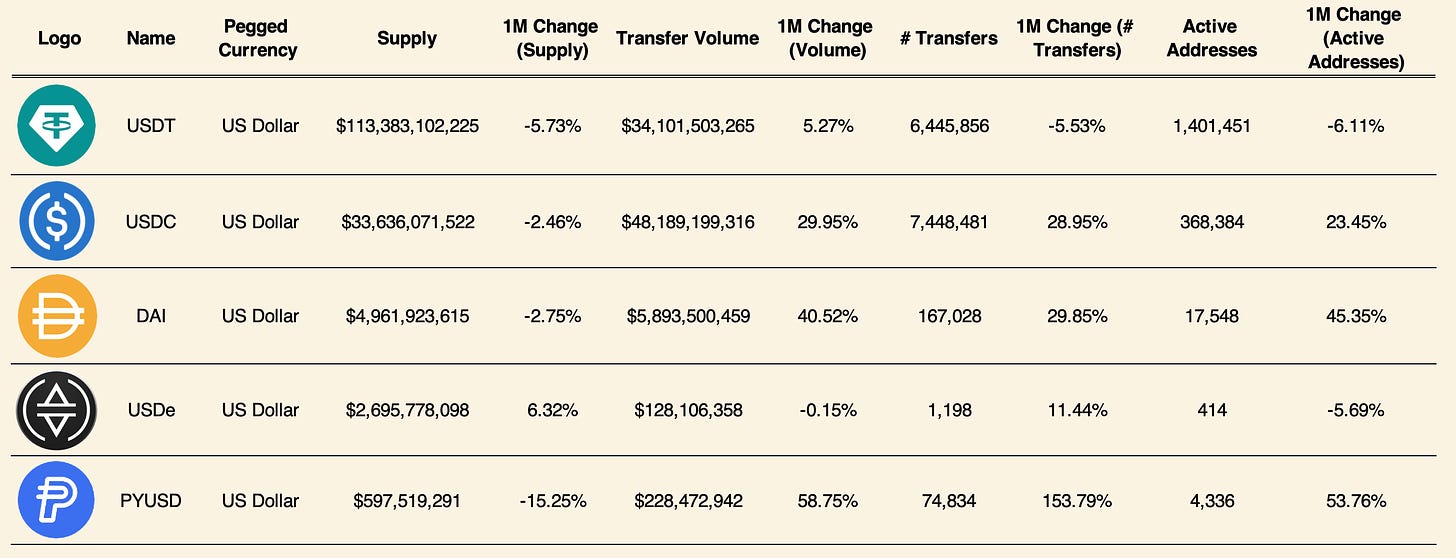

Top five stablecoins by supply (Total supply: $155.1B, Source: Artemis)

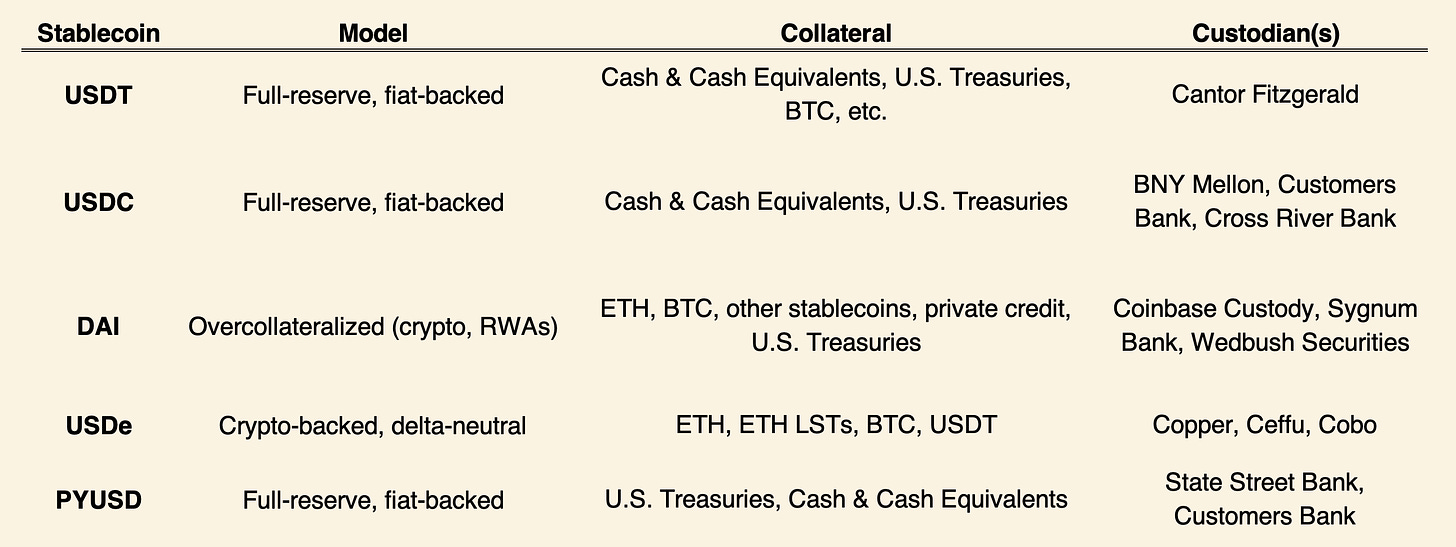

Stablecoin models: Collateral and custody analysis

Tether (USDT)

-

Collateral & Custody: Tether is backed by fiat reserves including cash, cash equivalents, and U.S. Treasuries, with custody managed by Cantor Fitzgerald. As of October 26, Tether reported holding $100 billion in U.S. Treasuries, over 82,000 bitcoins (worth approximately $5.5 billion), and 48 tons of high-grade gold.

-

Supply & Usage Trends: USDT has a supply of $113.4 billion, down 5.73% over the past month. Although transaction volume increased by 5.27%, active addresses declined by 6.11%, indicating reduced user activity.

USDC

-

Collateral & Custody: USDC is fully backed by fiat reserves and managed by BNY Mellon, Customers Bank, and Cross River Bank.

-

Supply & Usage Trends: USDC has a supply of $33.6 billion, down 2.46%. However, transaction volume surged by 29.95%, and active addresses increased by 23.45%, reflecting strong transactional demand.

DAI

-

Collateral & Custody: This over-collateralized stablecoin uses ETH, BTC, private credit, and U.S. Treasuries as collateral, with custody provided by Coinbase Custody, Sygnum Bank, and Wedbush Securities.

-

Supply & Usage Trends: DAI has a supply of $5 billion, down 2.75%. Yet, transaction volume rose by 40.52%, and active addresses increased by 45.35%, reflecting rising adoption and transaction activity.

USDe

-

Collateral & Custody: USDe is a synthetic stablecoin that achieves delta neutrality using ETH, ETH LSTs, BTC, and USDT, with custody handled by Copper, Ceffu, and Cobo.

-

Supply & Usage Trends: USDe has a supply of $2.7 billion. While transaction volume slightly declined, active addresses saw a modest increase, showing stable usage patterns.

PYUSD (PayPal USD)

-

Collateral & Custody: Issued by PayPal, PYUSD is fully backed by fiat assets such as U.S. Treasuries, cash, and equivalents, with custody by State Street Bank and Trust Company and Customers Bank.

-

Supply & Usage Trends: PYUSD is the smallest among major stablecoins, with a supply of $598 million. Transaction volume increased by 58.75%, and active addresses grew by 153.79%, indicating significant user interest and expanding usage.

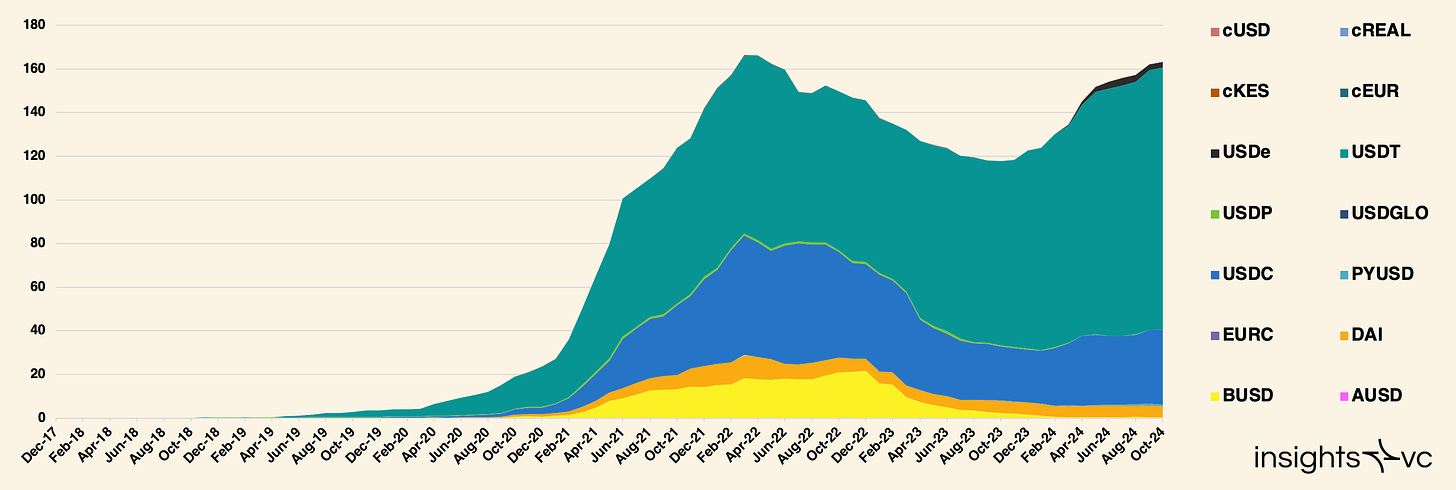

Stablecoins – Supply (Source: Artemis)

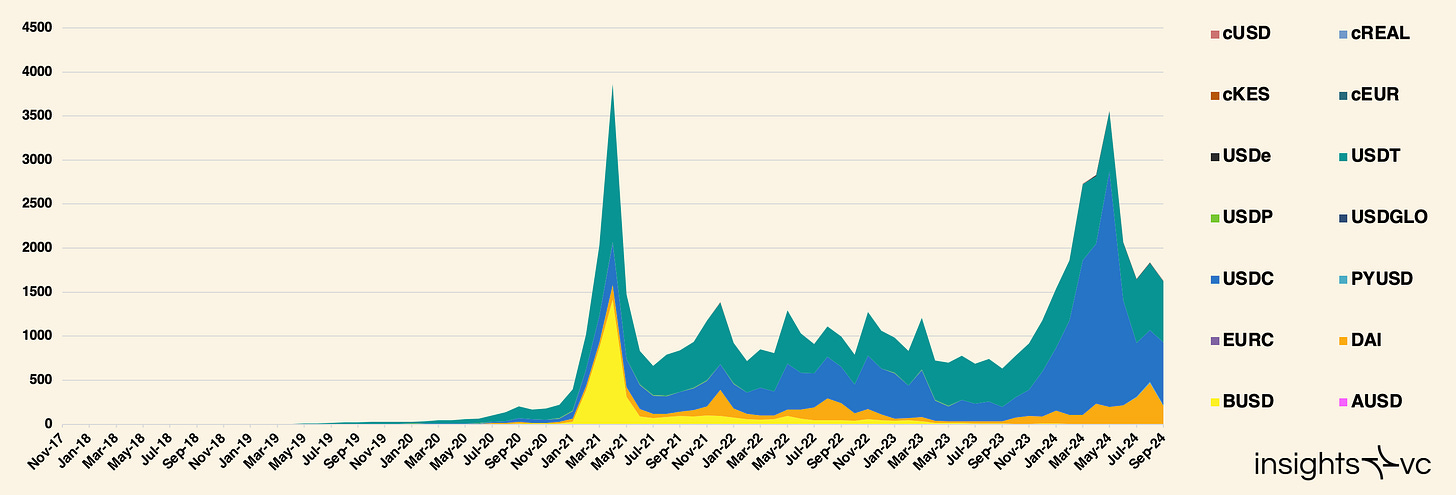

The data in the chart illustrates growth and fluctuations in stablecoin usage and transaction volumes over time. Starting in early 2018, both stablecoin supply and transaction volume rose significantly, peaking around mid-2021—likely driven by growing interest in decentralized finance (DeFi) and the broader crypto market. After 2021, while supply remained elevated, transaction volumes showed cyclical spikes, especially in early 2024, possibly indicating renewed market activity or volatility during that period.

Stablecoins – Transaction Volume (Source: Artemis)

USDT and USDC dominate the stablecoin market, forming the bulk of supply and trading volume. Other stablecoins such as DAI, BUSD, and emerging players like PYUSD, while smaller in share, are growing steadily, reflecting a trend toward market diversification.

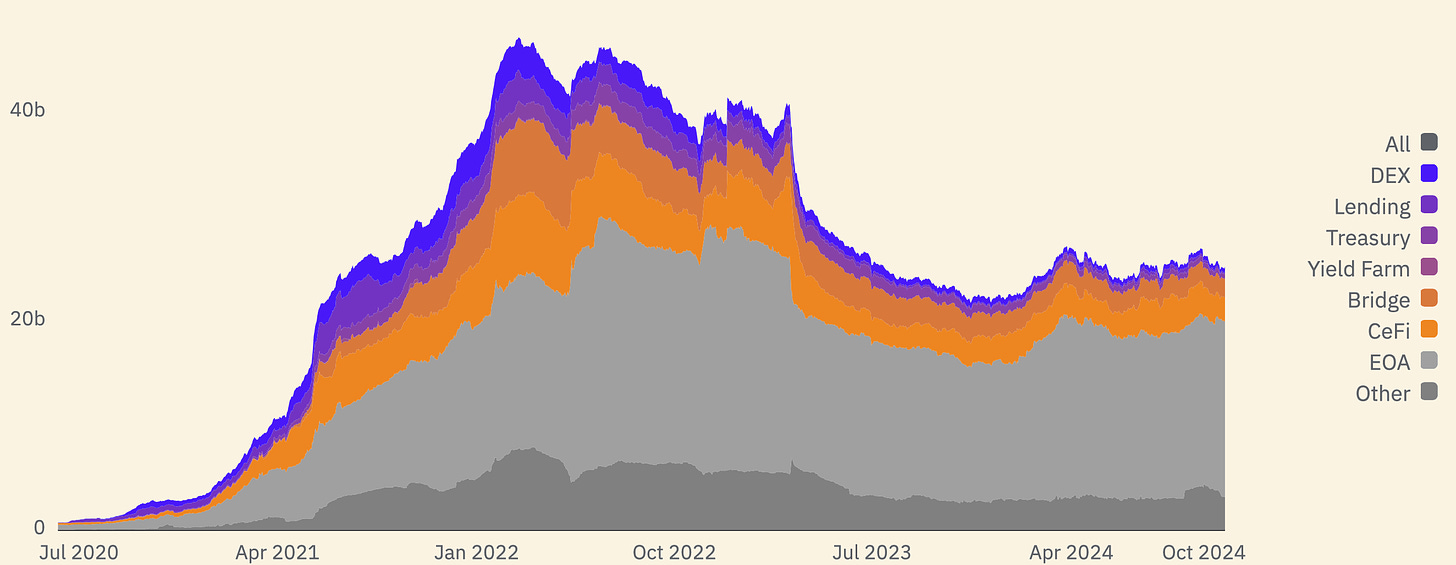

Distribution of USDC and USDT

There are significant differences in how USDC and USDT are distributed across decentralized finance (DeFi) and centralized finance (CeFi) platforms, as well as various wallets. For USDC, the largest holdings are in externally owned accounts (EOAs), totaling $16.8 billion, followed by CeFi with $2.3 billion and bridged assets at $1.8 billion. Treasury accounts hold $438 million, decentralized exchanges (DEXs) $388 million, and lending protocols $195 million. Yield farming usage is minimal at just $3 million, with miscellaneous holdings totaling $3.2 billion.

USDC Distribution

In contrast, USDT distribution is more concentrated, with $81.5 billion held in externally owned accounts (EOAs) and $26.3 billion in centralized finance (CeFi). Bridged assets account for $5.1 billion, DEXs hold $473 million, and lending protocols $439 million. Treasury accounts hold only $54 million, yield farming just $1 million, and other holdings total $2.5 billion.

USDT Distribution

As of October 2024, Ethereum, Tron, Arbitrum, Coinbase’s Base, and Solana are the primary blockchains for stablecoin settlements. While Ethereum leads in overall settlement value, its higher network fees result in fewer monthly sending addresses compared to lower-cost networks like Tron and Binance Smart Chain. Since sending addresses are harder to manipulate than raw transaction counts, these metrics reveal a complex landscape where Tron, Polygon, Solana, and Ethereum lead in stablecoin activity.

Stablecoin Transfer Volume Across Networks (in trillions of USD) – 2024 Market Trends

Stripe Acquires Bridge Network

On October 20, 2024, Stripe acquired Bridge Network for $1.1 billion, marking a milestone in the stablecoin and crypto payments market. Dubbed the “Stripe of crypto,” Bridge specializes in enabling businesses to make stablecoin payments without directly handling digital tokens. Major investors including Index Ventures and Haun Ventures supported the company, whose valuation surged 200% from $350 million since August, when top firms like Sequoia participated in funding. Bridge generates estimated annual revenue between $10 million and $15 million. Stripe’s acquisition signals its commitment to stablecoin infrastructure, with CEO Patrick Collison likening it to a “room-temperature superconductor in financial services.”

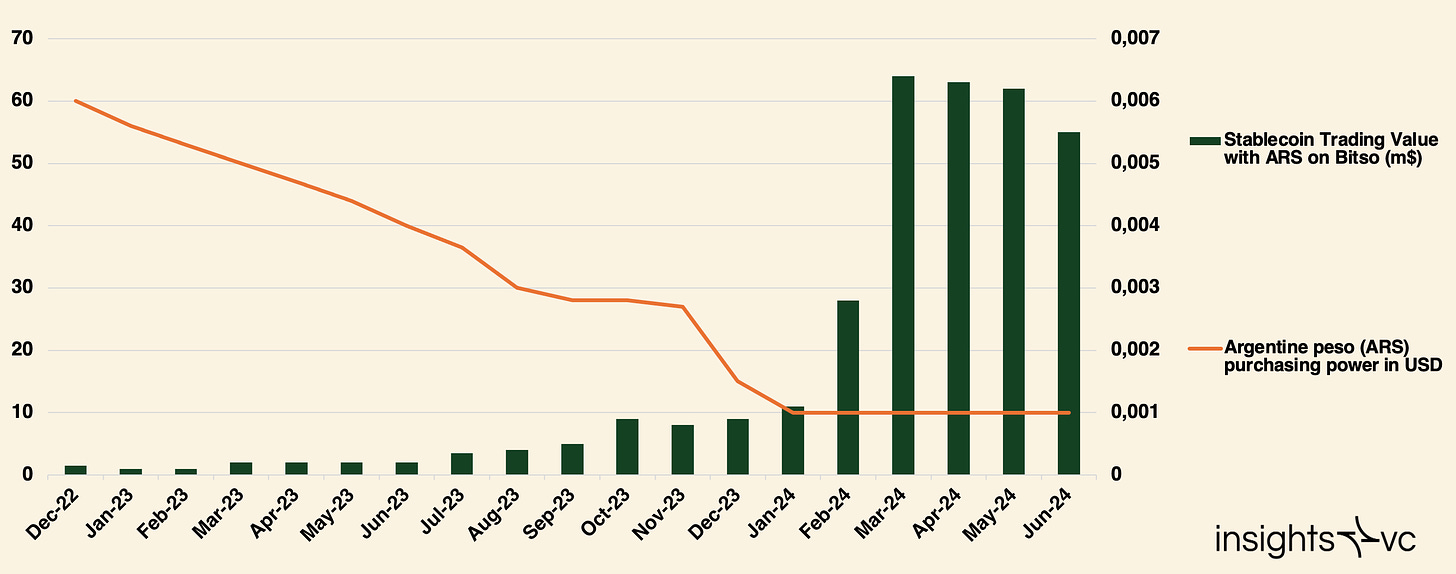

Emerging Markets and Currency Stability

In emerging markets facing severe currency depreciation, stablecoins serve as tools to hedge against local currency instability. Residents in countries like Argentina, Turkey, and Venezuela increasingly adopt stablecoins to combat local currency devaluation. For instance, stablecoin transaction volume in Argentina far exceeds the global average at 61.8%, driven by inflation and demand for dollar alternatives.

Stablecoin transaction volume on Bitso (in millions of USD) vs. purchasing power of Argentine peso (ARS) in USD

Retail transaction volume share by asset type in selected countries vs. global average (July 2023 – June 2024)

Cross-border Transactions and Remittances

Stablecoins are transforming cross-border payments, particularly in Africa and Latin America. In sub-Saharan Africa, stablecoins are crucial for businesses facing foreign exchange shortages and high remittance costs. In Nigeria, for example, using stablecoins reduces remittance fees by approximately 60% compared to traditional methods. Similarly, in Latin America, stablecoins enable faster and lower-cost cross-border transactions, prompting Circle to recently expand operations in Brazil to meet this demand.

Regulatory Developments and Challenges

Regulatory environments vary significantly across regions, impacting stablecoin growth. The EU’s Markets in Crypto-Assets Regulation (MiCA), effective since June 2024, provides a comprehensive regulatory framework for stablecoin projects in Europe, creating favorable conditions for development. Conversely, regulatory uncertainty in the U.S. has led some stablecoin activities to shift to non-U.S. markets. Issuers like Circle emphasize that clear regulation is essential to maintaining U.S. competitiveness in the stablecoin space.

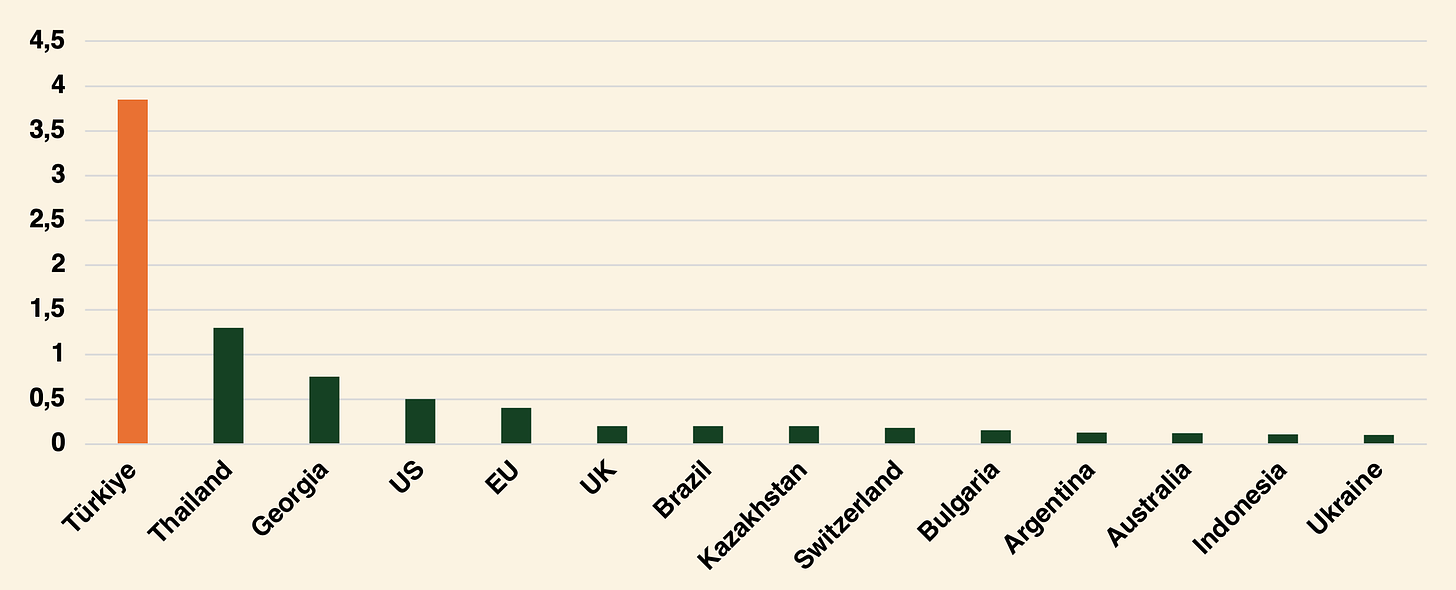

Institutional and Retail Demand

Stablecoin usage is increasing among both retail users and institutions. In Nigeria, stablecoins are widely used for daily transactions and cross-border payments, while in the EU, they are primarily used for B2B transactions such as invoice settlements and remittances. Additionally, in high-inflation countries like Turkey, retail users heavily adopt stablecoins as a hedge against inflation.

Ratio of fiat-to-stablecoin purchase volume to GDP across countries (July 2023 – June 2024)

Global Stablecoin Regulation

Stablecoin regulation varies globally due to considerations around financial stability, investor protection, anti-money laundering compliance, and innovation. Below are approaches taken by key jurisdictions:

European Union

-

MiCA Regulation: Effective from mid-2024, MiCA requires stablecoin issuers to hold sufficient reserves and ensures market integrity and consumer protection.

-

Innovation Initiatives: The EU supports innovation through blockchain regulatory sandboxes and the Distributed Ledger Technology (DLT) Pilot Regime, allowing companies to test within compliant frameworks.

-

Scope Limitations: MiCA currently excludes decentralized finance (DeFi) and non-fungible tokens (NFTs), limiting its applicability in broader crypto sectors.

United States

-

Multi-Agency Oversight: Multiple agencies including the SEC, CFTC, and FinCEN jointly regulate the sector, creating a complex environment.

-

Federal Legislation: Proposed bills such as Lummis-Gillibrand and FIT21 aim to establish a unified legal framework for stablecoin regulation.

-

State-Level Innovation: States like New York and Wyoming lead in legal innovation, with Wyoming recognizing decentralized autonomous organizations (DAOs) as legal entities.

United Kingdom

-

Stablecoins under Existing Framework: Stablecoins fall under existing financial regulations, with the Financial Conduct Authority (FCA) setting standards for anti-money laundering (AML), know-your-customer (KYC), and marketing.

-

Digital Securities Sandbox: This sandbox allows firms to experiment with digital asset solutions in a controlled environment, supporting secure innovation.

Singapore

-

Comprehensive MAS Guidelines: The Monetary Authority of Singapore (MAS) enforces strict AML, consumer protection, and licensing standards for stablecoins.

-

Regulatory Sandbox: Offers a secure testing environment that supports innovation while requiring rigorous KYC, security, and reserve management.

Japan

-

FSA-led Regulation: The Japan Financial Services Agency (FSA) enforces KYC/AML requirements and mandates licenses for stablecoin issuers.

-

Global Standard Leader: Japan allows internationally regulated stablecoins to operate domestically, promoting global interoperability.

-

Payment Services Act Updates: Recent amendments ensure security while adapting to new digital asset trends.

United Arab Emirates (UAE)

-

VARA Licensing Requirements: The UAE’s Virtual Assets Regulatory Authority (VARA) requires businesses engaged in stablecoin-related activities to obtain licenses.

-

Security Focus: Strict KYC and AML frameworks protect consumers and promote responsible development in the stablecoin sector.

Switzerland

-

FINMA Oversight: The Swiss Financial Market Supervisory Authority (FINMA) applies a principles-based approach, enforcing AML and data protection laws.

-

Support for DeFi: Its regulatory framework encourages innovation while ensuring safety and transparency.

Key Regulatory Themes and Requirements

AML and KYC Compliance:

Global AML and KYC compliance requires adherence to FATF standards, mandating stablecoin issuers to verify user identities and monitor transactions. Innovative tools such as zero-knowledge proofs are recommended to enable privacy-preserving KYC.

Regulatory Sandboxes

Regulatory sandboxes provide safe testing environments for digital asset products, balancing innovation with compliance. Key jurisdictions including the UAE, UK, and Japan employ sandbox frameworks and often collaborate internationally to harmonize regulatory practices.

Privacy and Security Protocols

Stablecoin providers must implement robust cybersecurity measures. As data privacy and asset custody regulations gain importance, regions like Hong Kong now require secure storage of assets.

Integration and Exclusion of DeFi

Decentralized Finance (DeFi) largely remains outside the scope of stablecoin regulation, though countries like the UK and Japan are exploring ways to integrate DeFi with traditional finance. The EU’s MiCA currently excludes DeFi from oversight, although future revisions may address this gap.

Outcomes and Unintended Consequences

Positive Outcomes

-

Enhanced consumer protection and market integrity have boosted confidence in stablecoins, fostering market growth in regions with clear regulatory frameworks.

-

Clear regulatory policies in places like Singapore and Switzerland have attracted digital asset firms, driving economic development and positioning these regions as global hubs for digital assets.

Challenges and Unintended Consequences

-

Regulatory Arbitrage: Some companies may relocate to jurisdictions with lighter regulation, posing risks of regulatory arbitrage. Regions like Gibraltar and the UAE face challenges balancing innovation with stringent oversight.

-

Privacy Concerns: MiCA’s transparency requirements may conflict with privacy-focused blockchain technologies, potentially impacting user privacy.

-

Innovation vs. Regulation: Stringent regulatory frameworks may hinder new market entrants; for example, the fragmented regulatory approach in the U.S. has prompted some firms to move operations overseas due to regulatory uncertainty.

Conclusion

Over the past decade, stablecoins have rapidly evolved from the initial concept of BitUSD into a cornerstone of decentralized finance, with a current total supply exceeding $156 billion. Modern stablecoins like Tether (USDT) and USD Coin (USDC) have achieved widespread adoption through ample fiat reserves, with USDT leading in supply at $113.4 billion. Emerging markets are increasingly adopting stablecoins as hedges against currency depreciation—for instance, stablecoin transactions in Argentina account for 61.8% of its retail transaction volume. Global regulatory responses to stablecoins vary: the EU’s MiCA regulation fosters innovation through clear guidelines, while regulatory uncertainty in the U.S. has driven some issuers to other markets. Institutional interest in stablecoins is growing rapidly, exemplified by Stripe’s $1.1 billion acquisition of Bridge Network. As stablecoins continue to bridge traditional finance and cryptocurrency, their future will depend on striking the right balance between innovation and effective regulation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News