A Comprehensive Overview of the U.S. Treasury's Report on Cryptocurrency Assets and the Treasury Market

TechFlow Selected TechFlow Selected

A Comprehensive Overview of the U.S. Treasury's Report on Cryptocurrency Assets and the Treasury Market

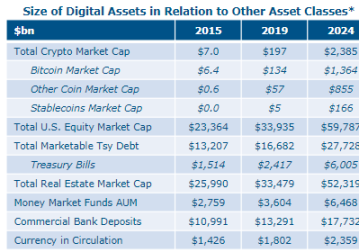

Despite a small base, crypto assets have experienced rapid growth.

Compiled by: Pzai, Foresight News

Trends in Cryptocurrency Asset Growth and Usage

Despite a small base, cryptocurrency assets have experienced rapid growth. This growth stems from both native cryptocurrencies such as Bitcoin and Ethereum, as well as stablecoins.

Chart of Total Cryptocurrency Market Capitalization

To date, household and institutional adoption of cryptocurrencies has been limited to holding digital assets for investment purposes. Compared to other financial and physical assets, the market value of crypto assets remains low. So far, their growth does not appear to have eroded demand for government bonds. Use cases for digital assets continue to evolve, but interest largely follows two main tracks: Bitcoin’s primary role seems to be value storage within the DeFi ecosystem—often called “digital gold.” Speculative interest has played a prominent role in driving cryptocurrency growth. The digital asset market is striving to leverage blockchain and distributed ledger technology (DLT) to develop new applications and improve traditional financial market clearing and settlement infrastructure.

Scale of Crypto Assets Relative to Other Asset Classes

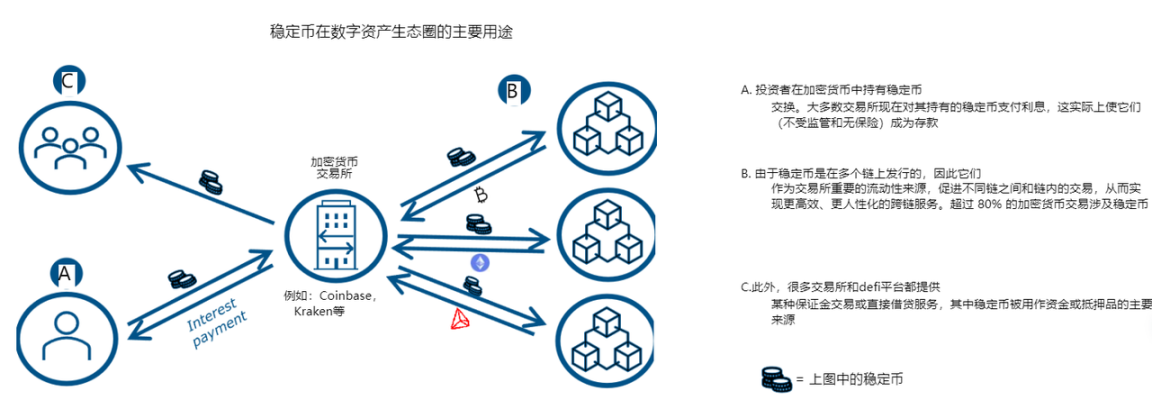

Stablecoins

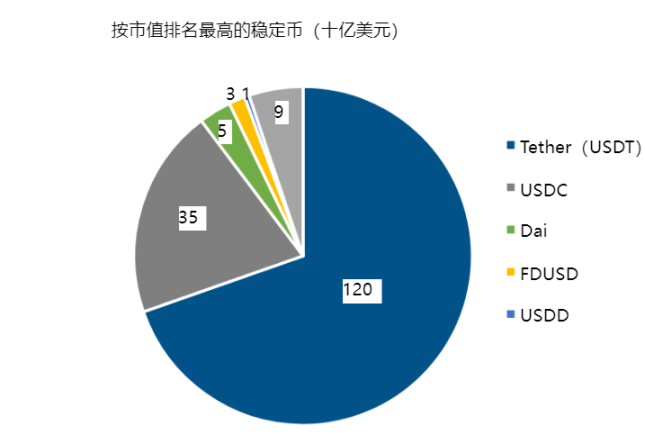

Stablecoins are cryptocurrencies designed to maintain stable value, typically by pegging the coin's value to an underlying pool of collateral. In recent years, as the crypto market matures, stablecoin usage has grown rapidly—driven by increasing demand for crypto assets with stable, cash-like characteristics—and they have become attractive collateral within DeFi networks. While there are various types of stablecoins, fiat-backed stablecoins have seen the most significant growth. Over 80% of all cryptocurrency trading volume now involves stablecoins.

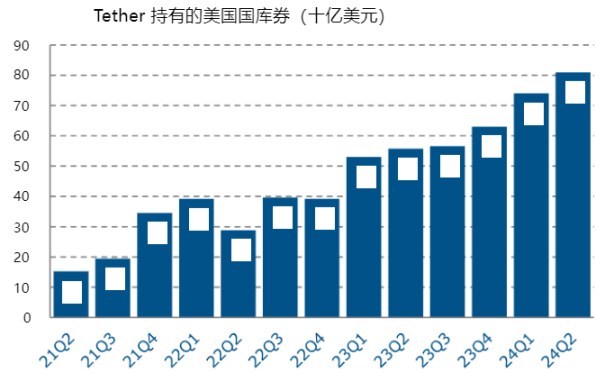

The most popular stablecoins in today’s market are fiat-backed, with a large portion of this collateral held in the form of U.S. Treasury securities and repo transactions backed by Treasuries. We estimate that approximately $120 billion in stablecoin reserves are directly invested in Treasury securities. In the short term, we expect continued growth in the stablecoin market and the broader digital asset sector. However, medium-term regulatory and policy decisions will determine the fate of these forms of "private money." History shows that privately issued monies failing to meet national quality assurance standards can lead to financial instability and are therefore highly undesirable.

Demand Analysis

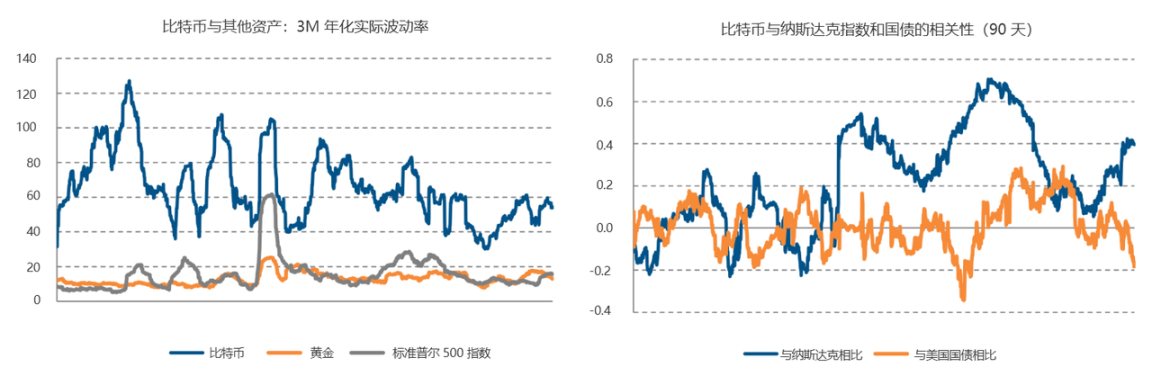

In recent years, prices of native crypto assets like Bitcoin have risen sharply, yet volatility remains high. Since 2017, Bitcoin has undergone four major price corrections. To date, the digital asset market has had limited access to traditional safe-haven or hedging instruments such as government bonds. Institutional support for Bitcoin (e.g., BlackRock ETF, MicroStrategy) has increased, while crypto assets continue to behave like “high-volatility” assets. As the market cap of digital assets grows, structural demand for Treasuries may rise, serving both as a hedge and as an on-chain safe-haven asset.

Tokenization

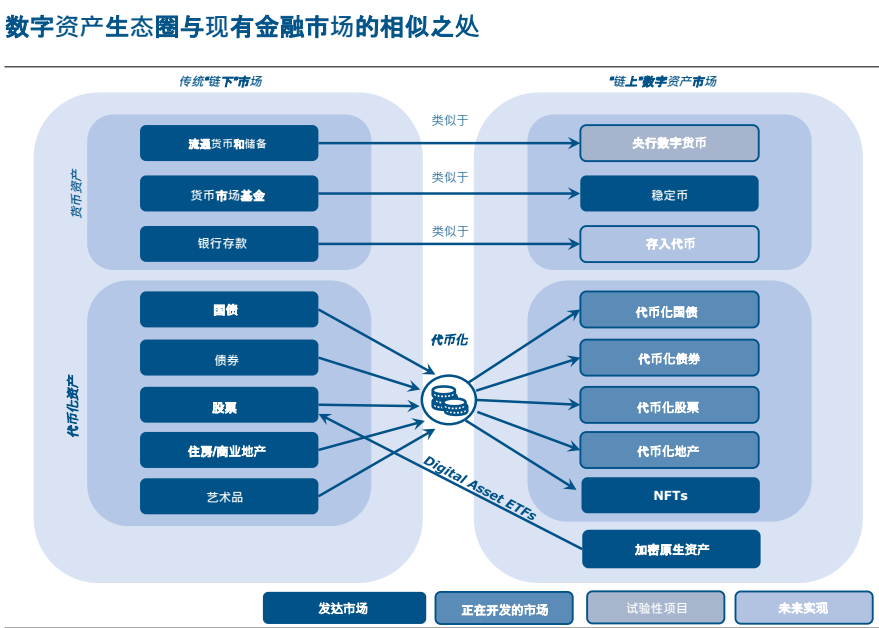

Similarities Between Digital Asset Ecosystems and Traditional Financial Markets

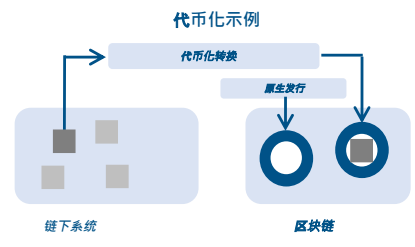

Tokenization refers to the process of digitally representing rights in token form on programmable platforms such as distributed ledgers/blockchains. It holds the potential to bring the benefits of programmable, interoperable ledgers into a wider range of traditional financial assets. Key features and advantages of tokenization include:

-

Core Service Layer: Tokenized assets integrate the “core layer” containing asset and ownership information with the “service layer” governing transfer and settlement rules.

-

Smart Contracts: Tokenization enables automation, allowing transactions to execute automatically via smart contracts when predefined conditions are met, facilitating the transfer of assets and claims.

-

Atomic Settlement: Tokenization simplifies settlement by ensuring all parts of a transaction settle simultaneously across all counterparties, reducing settlement failure risk and enhancing reliability.

-

Composability: Different tokenized assets can be combined to create more complex and innovative financial products, offering highly customizable solutions for asset management and transfer.

-

Fractional Ownership: Tokenized assets can be divided into smaller, more accessible units.

The benefits of tokenization extend far beyond native crypto assets like Bitcoin and the public, permissionless blockchain technologies on which they rely.

Some markets (e.g., international payments or repos) stand to gain direct and substantial benefits from tokenization, while others may see only incremental gains. However, realizing this potential requires either a unified ledger or at least a set of highly interoperable, seamlessly integrated ledgers. These ledgers must also be developed under the support of central banks and the trust foundation they provide.

Tokenized U.S. Treasuries

Tokenization of U.S. Treasuries is a relatively new trend, with most projects still not scaled. Notable ongoing public and private initiatives include:

-

Tokenized Treasury Funds: Allow investors to access Treasuries in “tokenized” form on blockchains. They function in many ways similarly to Treasury ETFs or government money market funds (MMFs).

-

Tokenized Treasury Repo Projects: Enable instant, 24/7 settlement and trading of tokenized Treasuries, potentially paving the way for more timely intraday repo transactions.

-

Ongoing Pilot Programs by DTCC and Other Institutions: Several private and public market participants are piloting tokenization to streamline payment and securities settlement.

Key potential benefits of tokenizing U.S. Treasuries include:

-

Improved Clearing and Settlement: Enables simplified “atomic settlement,” where all components of a Treasury-related transaction settle simultaneously among all parties, reducing settlement failure risk.

-

Enhanced Collateral Management: Smart contracts embedded directly into tokenized Treasuries enable more efficient collateral management, including pre-programmed transfers upon meeting preset conditions.

-

Greater Transparency and Accountability: Immutable ledgers enhance transparency in Treasury market operations, reduce opacity, and offer regulators, issuers, and investors real-time insights into trading activity.

-

Composability and Innovation: The ability to bundle different tokenized assets could lead to novel, highly customizable financial products and services based on U.S. Treasuries, such as derivatives and structured products.

-

Increased Inclusivity and Demand: Tokenization can make Treasuries more accessible to a broader investor base, including retail investors and those in emerging markets.

-

Enhanced Liquidity: Tokenization may unlock new investment and trading strategies through seamless integration and programmable logic, with tokenized Treasuries tradable 24/7 on blockchain networks.

Despite these potential benefits, design choices around tokenized U.S. Treasuries entail certain risks and challenges requiring careful consideration:

-

Technological Risk: Developing tokenization infrastructure in a cost-effective manner is difficult. Until sufficient scale (“incumbent advantage”) is achieved, it is unlikely to match the efficiency of traditional markets (“incumbency advantage”). It remains unclear whether DLT platforms offer compelling technical advantages over traditional systems, and transition costs may be high given the relatively small size of current digital markets.

-

Cybersecurity Threats: Certain DLT solutions—public, permissionless blockchains—are vulnerable to hacking and other cyberattacks, posing risks to the security of tokenized Treasuries.

-

Operational Risk:

-

Counterparty Risk: Investors may face counterparty risk—the possibility that issuers or custodians of tokenized securities default.

-

Custody Risk: Secure custody of tokenized Treasuries requires robust solutions, which may involve challenges similar to those associated with digital asset custody.

-

Privacy Concerns: Some participants view increased transparency on public blockchains as a disadvantage.

-

Regulatory and Legal Uncertainty:

-

Evolving Regulations: Legal requirements and compliance obligations regarding tokenized assets remain unclear.

-

Jurisdictional Challenges: Varying regulatory frameworks across jurisdictions may complicate cross-border transactions and create complex legal issues.

If the tokenized market expands significantly, it could introduce financial stability and market risks:

-

Contagion risk

-

Complexity and interconnectedness

-

Disintermediation of banks/payments

-

Basis risk

-

24/7 trading: May make markets more susceptible to manipulation and higher volatility

Financial Stability Risks from Significant Expansion of Future Tokenized Markets

-

Contagion and Interlinkage Risks:

-

Tokenization creates a bridge; as tokenized assets grow in scale, volatility in “on-chain” assets may spill over into broader financial markets.

-

During periods of stress, seamless ledgers could become a negative factor, enabling deleveraging and fire sales to spread rapidly across all assets.

-

Liquidity and Maturity Mismatch Risks:

-

Mismatches in liquidity and maturity between non-native tokens and underlying assets could trigger potential deleveraging and price volatility—similar to ETFs, MMFs, and Treasury futures.

-

Smart contract-driven automatic margin liquidations could cause liquidity stress, especially under tight settlement timelines.

-

Increased Leverage:

-

Tokenization can directly increase leverage in the financial system. For example, the underlying assets of tokens could be re-pledged, or the tokens themselves could be structured as derivatives.

-

Tokenization could generate tradable securities from illiquid or physical assets that can then serve as collateral.

-

Increased Complexity and Opacity:

-

Greater composability from tokenization, along with new non-traditional assets entering the digital finance ecosystem, could significantly increase the complexity and opacity of the financial system.

-

Poorly coded smart contracts could rapidly trigger unintended financial transactions with unforeseen consequences.

-

Banking Disintermediation:

-

Tokenized short-term Treasuries may prove to be an attractive alternative to bank deposits, potentially disrupting the banking system and negatively impacting core banking operations.

-

Stablecoin Run Risk:

-

Even with better collateral backing, stablecoins are unlikely to meet the necessary NQA principles required to support widespread tokenization.

-

Runs on stablecoins have occurred frequently in recent years, and the collapse of major stablecoins like Tether could trigger broad selloffs in short-term Treasuries.

Designing DLT/Blockchain for Tokenized U.S. Treasuries: Framework Elements

Establishing a trusted, industry-wide accepted framework is essential for scaling digital assets and DLT, as fraud, scams, and theft have grown alongside the digital asset market, undermining confidence in the underlying technology.

To date, most major crypto projects have been built on public, permissionless blockchains—a feature often cited as one of blockchain’s key attractions.

We believe this architecture is unsuitable for broader adoption of tokenized U.S. Treasuries:

-

Technology Choice: Public, permissionless blockchains use complex consensus mechanisms (e.g., Proof-of-Work, Proof-of-Stake), making them inefficient at processing large volumes of transactions.

-

Operational Fragility: These blockchains rely on decentralized nodes without centralized authority, creating vulnerabilities.

-

Governance Vulnerabilities: Public blockchains lack clear governance structures, increasing the risk of system failures or exploitation by attackers.

-

Security Risks: The decentralized nature and lack of oversight in public blockchains heighten exposure to exploits and attacks, as evidenced by historical breaches in Bitcoin and Ethereum.

-

Money Laundering and Compliance Issues: Public, permissionless blockchains allow anonymity, potentially facilitating illegal activities such as money laundering and sanctions evasion.

Tokenization of the Treasury market may require developing a blockchain managed by a single or multiple trusted private or public institutions.

Regulatory Elements

In recent years, global regulatory efforts around digital assets and cryptocurrencies have intensified, yet remain highly fragmented and full of gaps.

United States: Regulation remains fragmented, with authority split among multiple agencies including the SEC, CFTC, and FinCEN.

Executive Order on Ensuring Responsible Development of Digital Assets (2022): Signed in 2022, this order outlined a government-wide strategy for addressing opportunities and risks in digital assets. It called for the development of a regulatory framework for digital assets—culminating in the House passing the FIT21 Act (Financial Innovation and Technology for the 21st Century Act) in 2024, marking the most significant and comprehensive effort to regulate digital assets, stablecoins, and cryptocurrencies.

European Union: The Markets in Crypto-Assets Regulation (MiCA) will take effect in 2024. MiCA is the EU’s first comprehensive regulatory framework for cryptocurrencies and digital assets. It establishes rules for issuing crypto assets, stablecoins, and utility tokens, and regulates service providers such as exchanges and custodians. It focuses on consumer protection, stablecoin oversight, anti-money laundering measures, and transparency around environmental impact. Licensed entities under MiCA can operate across the EU using a “passporting” model, enabling them to offer services in all member states under a unified framework.

Impacts on the Treasury Market

Assuming current trends in stablecoin collateral choices persist (or are mandated by regulators), continued stablecoin growth will create structural demand for short-term U.S. Treasuries. Although stablecoins currently represent a marginal segment of the Treasury market, over time, runs on the stablecoin market could expose the Treasury market to greater sell-off pressure. Differences in redemption and settlement features may create liquidity and maturity mismatches between tokens and underlying assets, potentially exacerbating financial instability in the Treasury market.

-

Tokenized “derivative” Treasury products could establish a basis market between digital and native assets (similar to futures or total return swaps)—creating additional demand while amplifying volatility during deleveraging episodes.

-

During periods of heightened downside volatility, the growth and institutionalization of the crypto market (e.g., Bitcoin) may generate additional hedging demand and premium demand for tokenized Treasuries. Flight-to-quality demand may be hard to predict. Hedging demand could be structural, depending on how effectively U.S. Treasuries hedge against crypto downside volatility.

-

Tokenization could expand access to Treasuries for domestic and global pools of savings—particularly households and small financial institutions—potentially increasing overall demand for U.S. Treasuries.

-

Tokenization could enhance Treasury market liquidity by reducing operational and settlement frictions.

Conclusion

-

Although the overall digital asset market remains small compared to traditional financial assets like stocks or bonds, interest in digital assets has surged dramatically over the past decade.

-

To date, digital asset growth has generated only negligible incremental demand for short-term U.S. Treasuries, primarily driven by the use and proliferation of stablecoins.

-

Institutional adoption of “high-volatility” assets like Bitcoin and cryptocurrencies may lead to increased hedging demand for short-term Treasuries in the future.

-

The development of DLT and blockchain offers promise for new financial market infrastructure, where a “unified ledger” could enhance operational and economic efficiency.

-

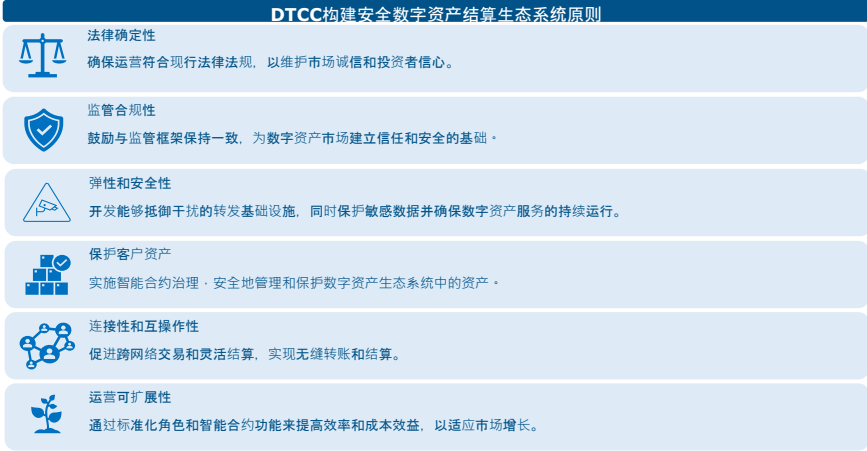

Both private and public sectors are pursuing ongoing projects and pilot programs to apply blockchain technology in traditional financial markets, notably DTCC and the Bank for International Settlements (BIS).

-

Central banks and central bank digital currencies (CBDCs) may play a critical role in future tokenized payment and settlement infrastructures.

-

The legal and regulatory environment must evolve alongside advances in asset tokenization. Operational, legal, and technological risks must be carefully considered when designing technology infrastructure and tokenization approaches.

-

Research initiatives should address the design, characteristics, and concerns related to Treasury tokenization, the introduction of sovereign CBDCs, and associated technological risks.

-

Currently, financial stability risks remain low due to the relatively small size of the tokenized asset market; however, these risks are likely to rise as the tokenized market experiences strong growth.

-

The path forward should involve a cautious approach led by a trusted central entity, supported broadly by private-sector participants.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News