The U.S. has finally welcomed perpetual contracts.

TechFlow Selected TechFlow Selected

The U.S. has finally welcomed perpetual contracts.

The U.S. has finally welcomed perpetual contracts—but cannot access the same product traded elsewhere in the world.

By Vaidik Mandloi

Translated by Block Unicorn

Last year, perpetual contract (perp) trading volume exceeded $90 trillion. For context, that surpasses the combined GDP of the world’s top ten countries. Today, perpetual futures account for roughly three-quarters of all cryptocurrency derivatives trading—and their growth has outpaced nearly every other financial product in history.

Yet, until last Friday, no U.S. institution could legally trade these contracts. On May 29, the U.S. Commodity Futures Trading Commission (CFTC) approved Kalshi to list the first-ever regulated Bitcoin perpetual futures contract in U.S. history. On the same day, the CFTC also authorized Coinbase to route its customers to global perpetual contract and options trading via the Deribit platform.

Following the announcement, Hyperliquid’s token HYPE surged 30%. For reference, Hyperliquid is currently the largest on-chain perpetual exchange—but it does not serve U.S. users. Michael Selig, Chairman of the CFTC, published a commentary in CoinDesk calling perpetuals “a foundational tool for risk management and price discovery in global crypto asset markets.” If you’ve been active in crypto for some time, witnessing this unfold in real time truly feels surreal. Let me explain why this matters so much.

How Did Perpetuals Accumulate $90 Trillion?

It all began in 1993, when Nobel Prize-winning economist Robert Shiller published a paper proposing a futures contract with no expiration date. His idea was that homeowners could hedge against falling home prices without selling their homes.

The concept was intriguing—but had no practical application at the time, because the entire derivatives market operated on expiration-based settlement. Clearinghouses and margin models were built around fixed settlement dates—for example, agricultural contracts settled monthly, bond futures had coupon payment dates. There simply wasn’t supporting infrastructure, so the idea remained confined to academic journals for decades.

Then, in May 2016, three founders from Hong Kong decided to give it a try. Arthur Hayes, Ben Delo, and Sam Reed launched BitMEX, adapting Shiller’s original idea with key modifications. They built a Bitcoin-based, non-expiring futures contract and added a mechanism to keep its price anchored to the underlying market—enabling leverage of up to 100x. Within just 18 months, BitMEX became the largest cryptocurrency derivatives exchange.

So what exactly are perpetual contracts—and how do they work?

In a standard futures contract, you bet on the price of an underlying asset at a specific future date. For instance, a Bitcoin futures contract expiring in June 2026 settles at the spot price in June. To maintain your position beyond that date, you must roll into the next contract. The problem is that each rollover incurs fees—and creates gaps in your exposure.

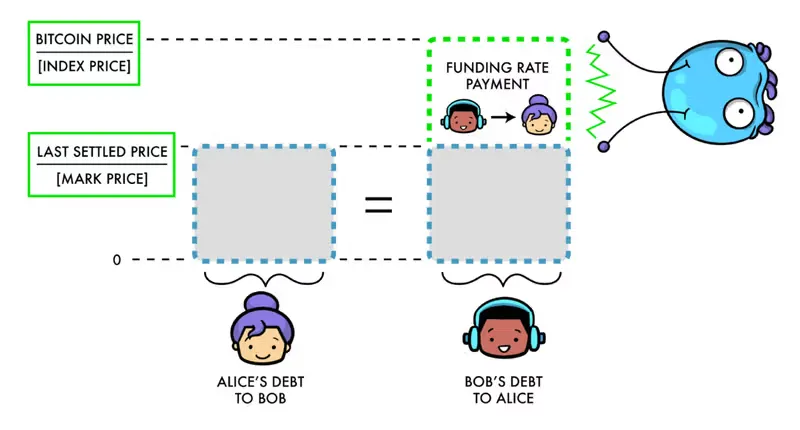

Perpetual contracts eliminate expiration entirely. You open a position—and it remains open until you close it. Your position can last five minutes—or five months. Crucially, standard futures naturally converge to the spot price at expiry. Perpetuals don’t—so another mechanism is needed to anchor their price. That mechanism is the funding rate.

One reason perpetual exchanges are so popular is that, unlike traditional exchanges—which spread liquidity across quarterly contracts (March, June, September, December)—perpetual exchanges concentrate all trading on a single platform, with one unified order book. This makes them among the most efficient trading venues—and in financial markets, efficiency compounds: more traders mean tighter spreads, which attract even more traders.

Offshore derivatives volume grew from $28 trillion in 2023 to over $90 trillion in 2025. On-chain derivatives volume on decentralized exchanges grew even faster—up 346% in 2025 alone, reaching $6.7 trillion. And on any given day, derivatives volume is roughly 10–15 times spot volume. That means price discovery has shifted from spot to derivatives markets. When Bitcoin swings 5% on a Tuesday afternoon, that move almost always originates in derivatives trading. A cascade of leveraged liquidations triggers buying or selling—and the spot market follows.

The “tail wagging the dog” phenomenon is underway—and the part of the market that truly determines price—the core of crypto markets—has historically excluded U.S. institutions entirely.

What Does This Mean for the U.S.?

The U.S. has finally embraced perpetuals—but not the same product traded elsewhere in the world. Even Coinbase itself must route funds through its Bermuda subsidiary to Dubai-based Deribit, because liquidity accumulated offshore over years of regulatory hostility—and cannot be rebuilt overnight.

U.S. traders face a leverage cap of roughly 10x, with full segregation protections from the CFTC; offshore traders use 50x–100x leverage. With 100x leverage, $1 controls $100 of risk exposure. A 10% price move yields a 10x return. In contrast, options deliver far lower returns for the same move—because the upfront premium already prices in expected volatility, and time decay steadily erodes value. A typical one-month Bitcoin call option delivers only ~3x return on the same 10% move. Leverage is the differentiator—and U.S. leverage remains comparatively modest.

That’s why Hyperliquid’s stock surged on the day the CFTC legalized previously illegal trading. Many assumed volume would shift from Hyperliquid to Kalshi and Coinbase—and that regulated, institutionally backed platforms would cannibalize Hyperliquid’s market share.

Hyperliquid generated $907 million in revenue last year—with zero U.S. users. Think about who trades on these platforms: someone shorting a memecoin 50x at 3 a.m. won’t open a Kalshi account to short Bitcoin 10x. Institutional investors requiring regulation and fund segregation never used Hyperliquid to begin with. These are products for entirely different audiences. The CFTC’s action effectively validated the product category Hyperliquid dominates—affirming its own intrinsic value.

Although regulatory constraints currently limit U.S. exchanges to Bitcoin-only trading, Hyperliquid has long transcended crypto. Through HIP-3, anyone can launch trading for any asset—and many are live. During February’s peak activity, silver trading hit $4 billion daily—and oil briefly surpassed Bitcoin in April.

Jeffrey Sprecher, CEO of Intercontinental Exchange (ICE)—parent company of the New York Stock Exchange—said at a Bernstein conference two days before the CFTC approved Hyperliquid’s exchange: “What we’re talking about now is Hyperliquid—if you haven’t heard of it yet, it’s bigger than Nasdaq, okay?” ICE is now in dialogue with Hyperliquid to understand its business model—and asking regulators why traditional exchanges can’t offer identical products. The learning direction has flipped: Wall Street is studying a two-year-old, zero-VC-backed decentralized exchange, because the trading infrastructure it built is exactly what the world’s largest exchanges now want to replicate.

Perpetuals Will Eat Everything

I believe this matters more than anything else—because perpetuals are no longer confined to crypto.

They began as a Bitcoin trading tool, then expanded to all altcoins. Today, they cover commodities like gold, silver, oil, and natural gas. Next came stocks—Nvidia, Tesla—and pre-IPO companies like SpaceX and OpenAI. Now, through the HIP-4 platform, they’ve entered prediction markets.

In just two years, perpetuals evolved from a crypto-native hack into a financial instrument that references any global asset—trades 24/7—and has no expiry or central clearing counterparty. Traditional derivatives made sense in an era of physical exchanges, paper-based settlement, and overnight market closures.

But today’s global digital infrastructure enables round-the-clock trading—and time-based markets risk gaps. For example, an oil trader wanting to position ahead of a weekend geopolitical event has no recourse on any regulated exchange—but such trades are already live on Hyperliquid. The CFTC acknowledges this too. Its staff advisory on 24/7 trading explicitly states: “Given digital infrastructure and global reach, crypto-asset-based derivatives may be well-suited for 24/7 trading.”

The real competition now lies in whether U.S.-regulated platforms can adapt quickly enough to matter. For instance, centralized exchange futures average ~4 basis points in fees—while Hyperliquid charges just 2 bps. The gap is even wider in spot: 15 bps vs. 5 bps. Since switching platforms takes minutes, traders will simply choose the cheaper venue.

Compass Point analysts issued a “sell” rating on Coinbase the week the CFTC approved its derivatives listing plan—citing competitive pressure in derivatives markets eroding pricing power and squeezing margins. Coinbase’s perpetual revenue in Q1 2026 stood at $50 million, while retail trading revenue fell to its lowest level since Q3 2024. Though perp revenue is growing, it’s cannibalizing higher-margin spot trading.

This compression effect manifests across many domains. If you can take leveraged directional exposure to any asset—anytime—without expiry, traditional derivatives become trivial. Why roll quarterly futures if perpetuals provide continuous exposure? True, funding rates can exceed rollover costs during crowded markets—sometimes adding 2% every eight hours. Exchanges have every incentive to preserve quarterly contracts, since rollovers generate two extra trades and two rounds of fees. But most retail traders hold positions for hours or days—making no-expiry contracts clearly simpler.

Why buy short-dated options if perpetuals offer similar directional leverage? Yes, options cap downside risk to the premium paid. But look at actual volumes: In 2025, average daily volume in S&P 500 0-day options hit 2.3 million contracts—most purely directional bets. For that purpose, perpetuals are simpler.

I’m not claiming perpetuals will fully replace options or traditional futures—options provide defined risk and convexity benefits that perpetuals cannot replicate. But for the vast majority of purely directional, leveraged trading activity, perpetuals are objectively superior—and more economical. Ultimately, the product has proven successful: $90 trillion in annual volume speaks for itself.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News