Re-examining Ethena: After an 80% Drop and a Rebound, Is ENA Still in the Undervalued Sweet Spot?

TechFlow Selected TechFlow Selected

Re-examining Ethena: After an 80% Drop and a Rebound, Is ENA Still in the Undervalued Sweet Spot?

Thus, a game of Fast Card began.

Author: Alex Xu

Introduction

Ethena is one of the few breakout DeFi projects in this market cycle. After its token launch, its circulating market cap briefly exceeded $2 billion (with a fully diluted valuation surpassing $23 billion). However, since April of this year, its token price has sharply declined, with Ethena's circulating market cap retracting over 80% from its peak and the token price falling as much as 87% at its lowest point.

Since September, Ethena has accelerated its pace of collaboration with various projects, expanding the use cases for its stablecoin USDE. The stablecoin’s supply has also begun to rebound from its lows. From a low of around $400 million in September, Ethena’s circulating market cap has now recovered to approximately $1 billion.

In my article published in early July titled “Altcoins Keep Falling — Time to Refocus on DeFi?,” I mentioned Ethena, expressing the following view at the time:

“...Ethena’s business model (a publicly accessible fund focused on perpetual futures arbitrage) still faces clear limitations. The expansion of its stablecoin (which reached $3.6 billion at the time) relied heavily on secondary market users being willing to buy its token ENA at premium prices, subsidizing high yields for USDE. This somewhat Ponzi-like design can easily spiral into negative feedback loops affecting both operations and token price when market sentiment sours. The key turning point for Ethena will come when USDE becomes a stablecoin widely held by 'organic holders'—at which point its business model would have successfully transitioned from an arbitrage-focused fund to a true stablecoin operator.”

Since then, the price of ENA has fallen another 60%. Even though it has recently rebounded nearly 100% from its lows, it still trades over 30% below its level at that time.

I am re-evaluating Ethena at this moment, focusing primarily on three questions:

-

Current business performance: Ethena’s core metrics today, including scale, revenue, total costs, and actual profitability

-

Future outlook: Promising narratives and potential growth trajectories for Ethena

-

Valuation: Is the current price of ENA in an undervalued sweet spot?

This article reflects my interim thoughts as of publication and may change in the future. My views are highly subjective and may contain factual, data, or logical errors. I welcome criticism and further discussion from peers and readers, but this article does not constitute any investment advice.

Below is the main body of the analysis.

1. Business Performance: Ethena’s Current Core Operations

1.1 Ethena’s Business Model

Ethena positions itself as a synthetic U.S. dollar project with “native yield,” placing it in the same category as MakerDAO (now SKY), Frax, crvUSD (Curve’s stablecoin), and GHO (Aave’s stablecoin)—that is, stablecoins.

In my view, the business models of most stablecoin projects in crypto today are fundamentally similar:

-

Raise capital, issue debt (stablecoins), and expand the project’s balance sheet

-

Deploy the raised capital into financial operations to generate returns

When the returns generated from these operations exceed the total cost of raising capital and running the project, the project becomes profitable.

Take the centralized stablecoin project Tether (issuer of USDT): Tether collects USD from users, issues USDT tokens in return, and invests the collected funds into interest-bearing assets such as Treasury bonds and commercial paper. Given USDT’s broad utility and its perceived 1:1 parity with the U.S. dollar, users are willing to provide USD to Tether without compensation. In fact, redeeming USDT back into USD often incurs a fee.

As a latecomer in the stablecoin space, Ethena clearly lags behind established players like USDT and DAI in terms of network effects and brand credibility. This manifests in higher funding costs—users only provide their assets to Ethena in exchange for USDE if they expect high returns. To attract capital, Ethena offers incentives in the form of its native token ENA and yield from financial income generated by its operational funds.

1.2 Ethena’s Core Business Data

1.2.1 USDE Issuance Scale and Distribution

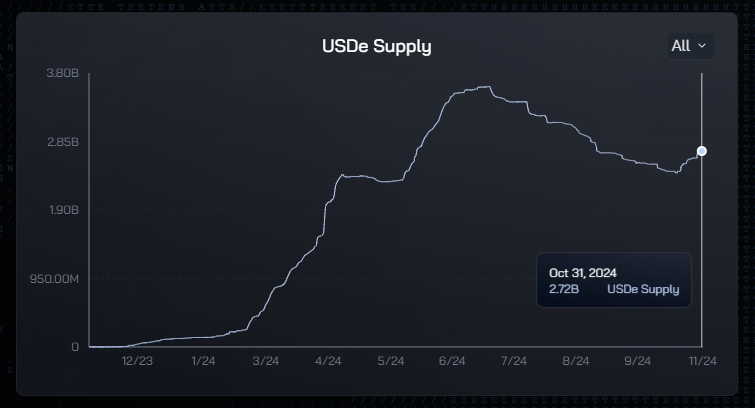

Data source: https://app.ethena.fi/dashboards/solvency

After hitting a new high of $3.61 billion in early July 2024, USDE issuance steadily declined until bottoming out at $2.41 billion in mid-October. It has since started to recover and stood at approximately $2.72 billion as of October 31.

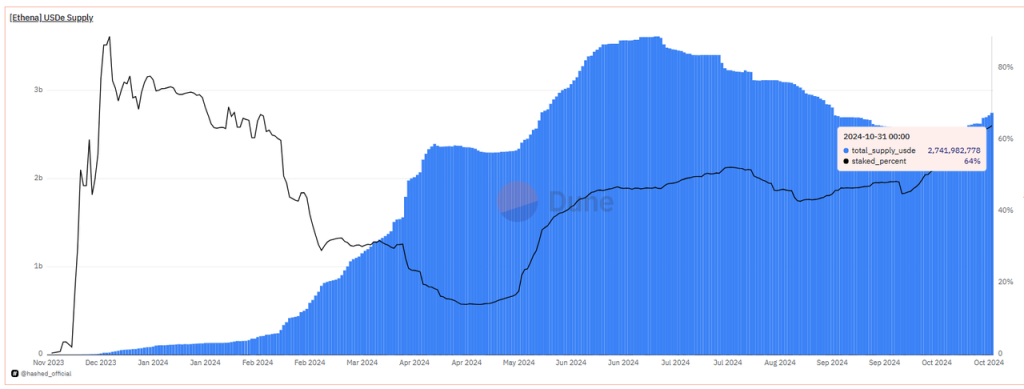

Of the $2.72 billion in circulation, 64% of USDE is currently staked, offering an APY of 13% (per official website data).

Data source: https://dune.com/queries/3456058/5807898

This indicates that most users hold USDE primarily for yield generation. The 13% APY represents the “risk-free” return in USDE terms and also reflects Ethena’s current cost of capital.

By comparison, the yield on short-term U.S. Treasury bills was 4.25% (as of October 24), while USDT deposits on Aave offered 3.9%, and USDC offered 4.64%.

It is evident that Ethena continues to maintain relatively high funding costs to grow its capital base.

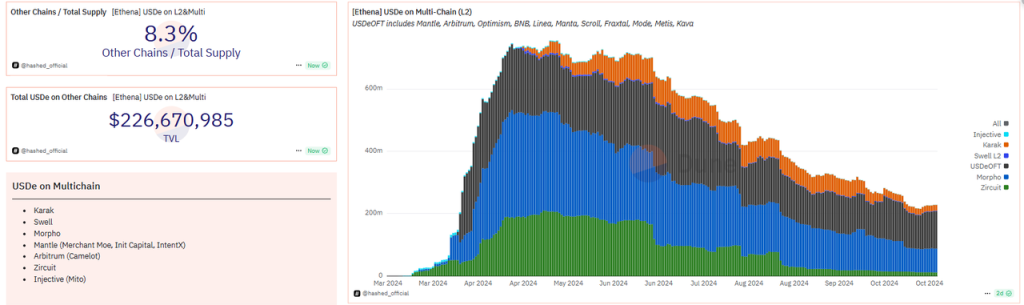

USDE is issued not only on Ethereum but also across multiple L2s and L1s. As of now, USDE issued on other chains amounts to $226 million, representing about 8.3% of the total supply.

Data source: https://dune.com/hashed_official/ethena

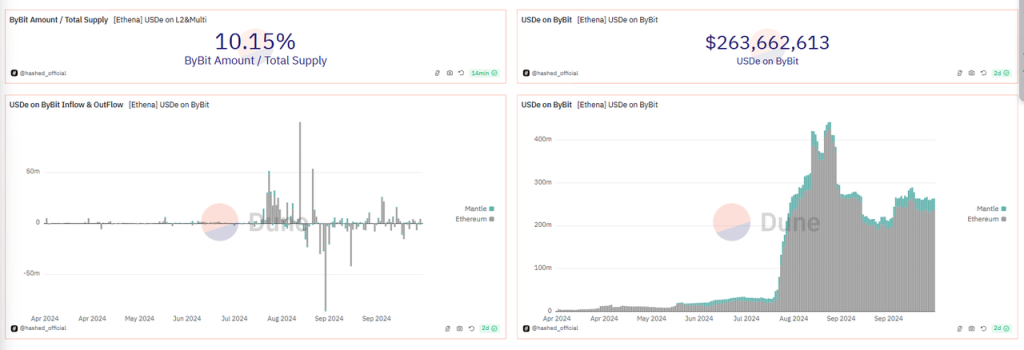

Additionally, Bybit, as both an investor and key partner of Ethena, supports USDE as collateral for derivatives trading and previously offered up to 20% yield on USDE deposits (reduced to a maximum of 10% in September). Bybit is thus one of the largest custodians of USDE, currently holding $263 million (peaking above $400 million).

Data source: https://dune.com/hashed_official/ethena

1.2.2 Protocol Revenue and Underlying Asset Composition

Ethena currently generates protocol revenue from three sources:

-

Staking rewards from ETH held in its underlying assets;

-

Funding rate and basis income from hedging and arbitraging derivatives positions;

-

Yield from stablecoin holdings: interest or incentive subsidies from depositing stablecoins, such as earning Coinbase’s loyalty program rewards (~4.5% APY) by holding USDC on Coinbase, or depositing into Spark’s sUSDS (formerly sDAI).

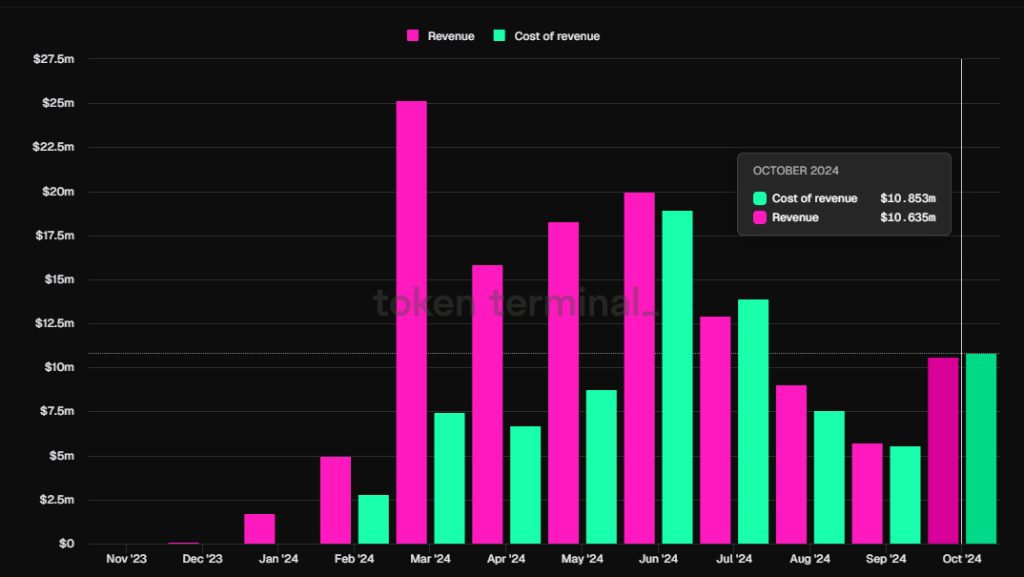

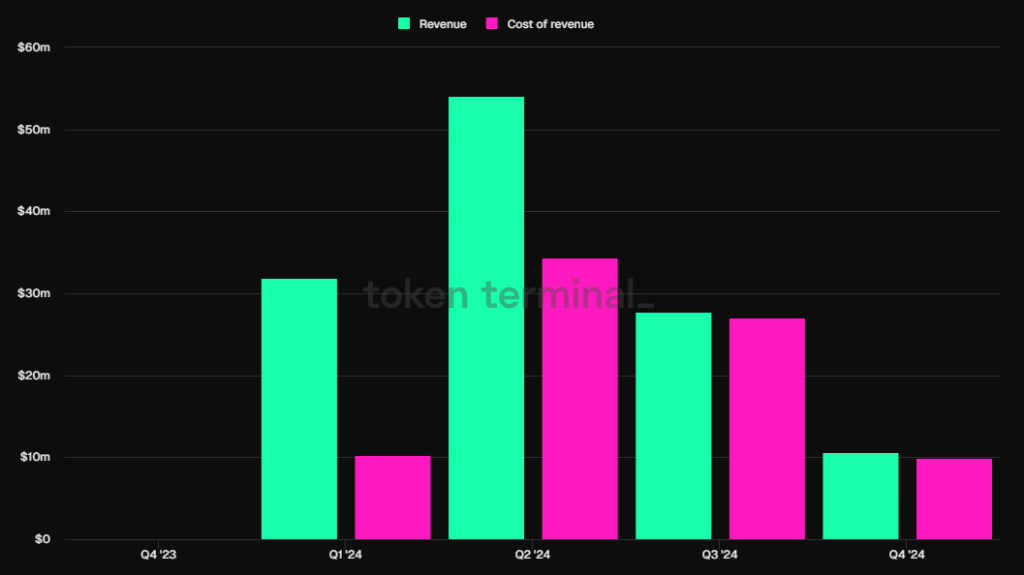

According to Token Terminal data, verified by Ethena’s official team, the protocol’s revenue has recovered from last month’s low. October’s protocol revenue reached $10.63 million, an 84.5% increase month-over-month.

Data source: Token Terminal – Ethena protocol revenue and revenue allocated to USDE (cost of revenue)

A portion of this revenue is distributed to USDE stakers, while the remainder goes into the protocol’s Reserve Fund, used to cover negative funding rate periods and risk events.

The official documentation states that “the amount of protocol revenue allocated to the reserve fund must be determined through governance.” However, I could not find any specific proposal regarding reserve allocation ratios on the official forum. Changes in allocation ratios were only initially announced via the official blog. In practice, Ethena has adjusted its revenue distribution multiple times post-launch. While community input was considered early on, final decisions remained under centralized control without formal governance processes.

As shown in the Token Terminal chart above, the split between revenue allocated to USDE stakers (red bars, i.e., cost of revenue) and the reserve fund has been highly volatile.

In the early stages, when protocol revenue was high, most of it went to the reserve fund—on March 11, for example, 86.7% of weekly revenue was allocated to reserves. Starting in April, as ENA’s price began to fall rapidly, token-based incentives proved insufficient to sustain demand for USDE. To stabilize USDE’s scale, Ethena shifted revenue distribution toward stakers, allocating most income to them. Only in the past two weeks has weekly protocol revenue clearly exceeded payouts to USDE stakers (excluding ENA token incentives).

Underlying asset composition, data source: https://app.ethena.fi/dashboards/transparency

Currently, 52% of Ethena’s underlying assets are BTC arbitrage positions, 21% ETH arbitrage positions, 11% ETH staking arbitrage positions, and the remaining 16% are stablecoins. Thus, BTC-focused arbitrage remains Ethena’s primary revenue driver. ETH staking, once emphasized, now contributes minimally due to its smaller asset share.

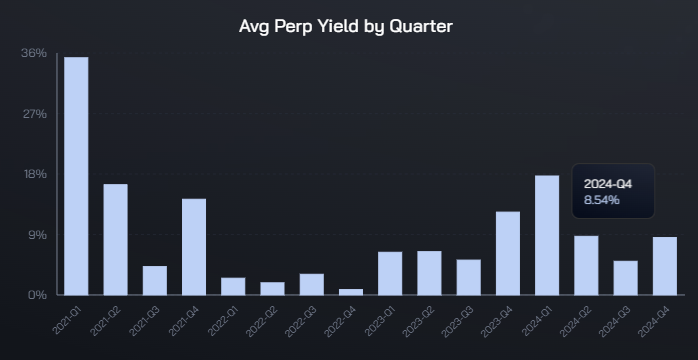

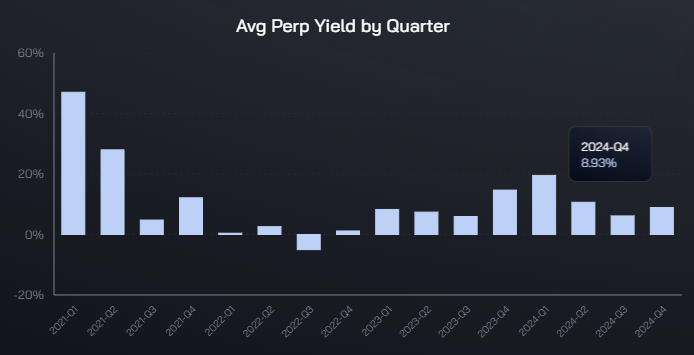

Average quarterly yield from BTC and ETH perpetual contract arbitrage, data source: https://app.ethena.fi/dashboards/hedging

BTC perpetual arbitrage average yield has recovered from Q3’s lows to levels seen in Q2, with the current quarter’s average annualized yield exceeding 8%. Even during the weakest period in Q3, BTC arbitrage averaged over 5% annualized yield.

ETH perpetual arbitrage yields have followed a similar trend, now also exceeding 8% annualized.

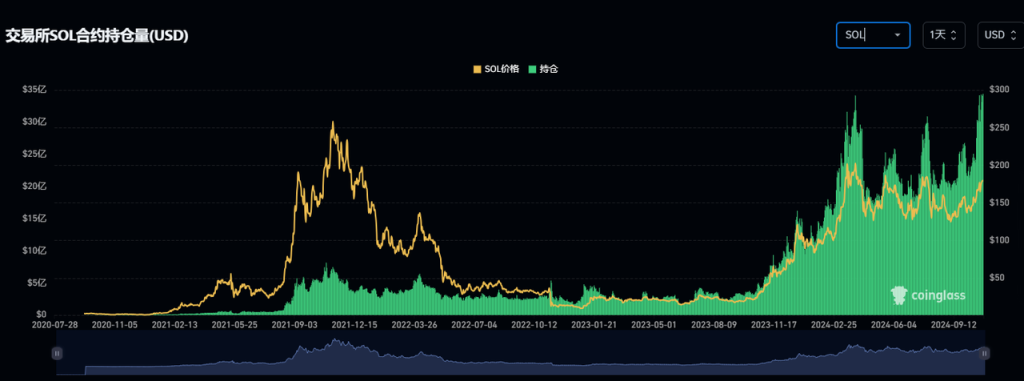

Now consider Solana’s (SOL) futures market size. Despite SOL’s price rise this year driving open interest to $3.4 billion, it remains far below ETH’s $14 billion and BTC’s $43 billion (excluding CME data).

SOL open interest trend, data source: Coinglass

SOL’s funding rates, based on Binance and Bybit (largest exchanges), are currently around 11% annualized—similar to BTC and ETH.

Current annualized funding rates for major cryptocurrencies

Data source: https://www.coinglass.com/zh/FundingRate

Thus, even if SOL is added as a new arbitrage asset, its current scale and yield offer no significant advantage over BTC and ETH, meaning limited incremental revenue in the short term.

1.2.3 Ethena’s Protocol Expenses and Profitability

Ethena’s protocol expenses fall into two categories:

-

Financial expenses: paid in USDE to USDE stakers, funded by protocol revenue (from derivatives arbitrage, ETH staking, and stablecoin yield).

-

Marketing expenses: paid in ENA tokens to users participating in various growth campaigns. Participants earn points (named differently across phases—e.g., Shards, later Sats) and exchange them for ENA rewards after each campaign season.

Financial expenses are straightforward—USDE stakers have clear yield expectations, clearly displayed on Ethena’s homepage:

Current USDE staking APY: 13%, source: https://ethena.fi/

More complex are the continuous marketing campaigns launched since Ethena’s inception, featuring varying rules, behavior-specific point incentives, weight mechanisms, and cross-platform activity calculations.

Let’s briefly review Ethena’s series of growth campaigns since launch:

1. Ethena Shard Campaign: Epoch 1–2 (Season 1)

-

Duration: Feb 19 – Apr 1, 2024 (less than 1.5 months)

-

Main incentivized actions: Providing USDE liquidity on Curve.

-

Secondary incentives: Minting USDE, holding sUSDE, depositing USDE/sUSDE into Pendle, holding USDE on partner L2s.

-

Scale growth: USDE supply grew from under $300M to $1.3B.

Total ENA distributed (marketing spend): 750 million (5% of total supply). The top 2,000 wallets could claim 50% immediately, with the rest linearly vested over six months. Smaller wallets had no lock-up. According to @sankin’s Dune dashboard, nearly 500 million ENA were claimed by June. Before June, ENA traded between ~$0.67 and $1.50, averaging ~$1. After early June, ENA dropped rapidly from $1 to ~$0.20, averaging ~$0.60 during the vesting period. The remaining 250 million ENA were mostly claimed during this phase.

A rough estimate: value of 750M ENA ≈ (500M × $1) + (250M × $0.60) = ~$650 million.

In less than two months, USDE grew by ~$1 billion in supply, at a marketing cost of $650 million—excluding financial expenses paid to stakers.

Still, as ENA’s initial airdrop, this heavy spending was exceptional.

2. Ethena Sats Campaign: Season 2

-

Duration: Apr 2 – Sep 2, 2024 (5 months)

-

Main incentives: Locking ENA, providing USDE liquidity, using USDE as loan collateral, depositing into Pendle, restaking protocols, and Bybit.

-

Secondary incentives: Locking USDE on Ethena’s platform, holding/using USDE on partner L2s, using sUSDE as collateral.

-

Scale growth: USDE grew from $1.3B to $2.8B.

ENA distributed: Again 5% of total supply (750 million ENA), with top 2,000 wallets facing 50% immediate release and 6-month vesting for the rest. At the current ENA price of $0.35, 750 million ENA is worth ~$262.5 million.

3. Ethena Sats Campaign: Season 3

-

Duration: Sep 2, 2024 – Mar 23, 2025 (under 7 months)

-

Main incentives: Locking ENA, holding USDE in designated partner protocols (DEXs and lending platforms), depositing USDE into Pendle.

-

Scale growth: Despite Season 3, USDE growth has stalled. Current supply is ~$2.7B, slightly down from ~$2.8B at the start.

-

ENA expenditure: Given the longer duration and likely continued decline in reward value, Season 3 is expected to maintain a 5% total allocation (750 million ENA).

We can now roughly calculate Ethena’s total protocol expenses since launch (as of Oct 31):

-

Financial expenses (paid in stablecoins to USDE stakers): $81.65 million

-

Marketing expenses (paid in ENA): $650M + $262.5M = $912.5 million (excluding potential post-September expenses)

Ethena’s quarterly protocol revenue vs. financial expenses, source: Token Terminal

-

Total protocol revenue during the same period: $124 million

Contrary to the popular perception that “Ethena is highly profitable,” after deducting financial and marketing expenses, Ethena has incurred a net loss of approximately $868 million by the end of October. This figure excludes additional ENA emissions from September onward, so the actual loss may be even higher.

An $868 million net loss is the price tag for scaling USDE to $2.7 billion in market value within a year.

In truth, like many DeFi projects in the previous cycle, Ethena follows a model of boosting key metrics and protocol revenue through token subsidies. However, Ethena employs a unique points-based system that delays token distribution and incorporates multiple partners as participation channels, making it difficult for users to assess the true financial return of their participation—effectively increasing user stickiness.

2. Future Outlook: Promising Narratives and Development Potential

Over the past two months, ENA has rebounded nearly 100% from its lows—even after the unlock of Season 2 rewards in early October. These two months have also been packed with news and positive developments for Ethena, including:

-

Oct 28: Derive (formerly Lyra), a derivatives and options platform, added sUSDE as collateral

-

Oct 25: Wintermute added USDE as OTC trading collateral

-

Oct 17: Ethena proposed integrating its liquidity and hedging engine into Hyperliquid

-

Oct 14: Community proposal to add SOL to USDE’s underlying assets

-

Sep 30: Launch of Ethereal, the first project on Ethena Network, promising 15% token airdrop to ENA holders. Ethena Network announced more ecosystem app launches in the coming weeks

-

Sep 26: Announcement of USTB—a “new stablecoin co-launched with BlackRock”—in reality, USTB is a stablecoin backed by BUILD, BlackRock’s on-chain Treasury token, with minimal direct involvement from BlackRock

-

Sep 4: Collaboration with Etherfi and Eigenlayer to launch eUSD—the first AVS collateral asset denominated in stablecoins. Depositing USDE into Etherfi mints eUSD, which launched on Sep 25

In short, USDE and sUSDE use cases have expanded significantly over the past two months. However, demand stimulation has been limited—for example, eUSD, the AVS collateral asset launched with Etherfi and Eigenlayer, currently has only a few million dollars in scale.

In reality, the real catalyst behind ENA’s recent price surge was a bullish article published on October 12 by well-known trader and crypto KOL Eugene @0xENAS: “Ethena: The Trillion Dollar Crypto Opportunity.”

With nearly 400 retweets, over 1,800 likes, and more than 700,000 views, the post drove ENA’s price from $0.27 to $0.41 within four days—an increase of over 50%.

Besides reviewing Ethena’s product features, Eugene highlighted three main arguments. In my view, only the first holds merit; the other two are deeply flawed:

1. Falling global risk-free rates due to U.S. rate cuts make USDE’s APY more attractive, drawing in more capital

2. The newly launched USTB, “co-developed with BlackRock,” is an “absolute gamechanger” that will boost USDE adoption, as USDE can switch to USTB during periods of negative perpetual funding rates to earn risk-free Treasury yields

Critique: USTB uses BUILD as collateral—it doesn’t mean USTB is jointly developed by BlackRock and Ethena. Just because DAI holds large amounts of USDC doesn’t make it a joint product of Circle and MakerDAO. In reality, during negative funding rate periods, Ethena could simply close positions and allocate to BUILD or sDAI directly, or deposit USDC on Coinbase to earn ~4.5% yield—no need to issue a separate USTB. USTB appears to be little more than a publicity stunt leveraging BlackRock’s name. Calling such a marginal product an “absolute gamechanger” raises questions about the author’s understanding or motives.

3. Future ENA emission rates will decrease, significantly reducing selling pressure

Critique: Season 2 still allocates 5% of total ENA supply (750 million tokens) to be released over the next six months—hardly a reduction from the prior season. Moreover, in March 2025, Ethena will face massive unlocks from the team and investors, suggesting poor inflation outlook for ENA over the next six months.

Nevertheless, Ethena still has several promising developments ahead over the next few months to a year:

-

Anticipation of Trump’s potential return and Republican victory (results imminent) could warm crypto markets, boosting BTC and ETH perpetual arbitrage yields and volumes, thereby increasing Ethena’s protocol revenue

-

More projects emerging within the Ethena ecosystem beyond Ethereal, increasing airdrop opportunities for ENA holders

-

Launch of Ethena’s own blockchain could bring attention and nominal staking use cases for ENA—though I expect this will happen only after more ecosystem projects are established

However, the most critical factor for Ethena remains broader acceptance of USDE as collateral and trading pair on top-tier CEXs.

Bybit has already formed a deep partnership with Ethena.

Coinbase operates its own USDC and, as a U.S.-based company sensitive to regulation, is extremely unlikely to support USDE as collateral or trading pair.

Among Binance and OKX, OKX has participated in two Ethena funding rounds, aligning its financial interests to some degree. There is a possibility—though not high—that OKX adds USDE as a trading pair or futures collateral, despite associated operational and reputational risks. Binance, having participated in only one funding round, has even less incentive to list USDE, especially given its own supported stablecoin projects.

Eugene cited the expectation that USDE would become margin collateral across major exchanges as a reason to be bullish on Ethena. However, I remain skeptical.

3. Valuation: Is ENA Currently Undervalued?

We analyze ENA’s current valuation from qualitative and quantitative perspectives.

3.1 Qualitative Analysis

Events likely to positively impact ENA’s price in the coming months include:

-

Improved arbitrage yields driven by a recovering crypto market, leading to better protocol revenue outlook, higher ENA prices, and expanded USDE scale

-

Inclusion of SOL in underlying assets, attracting attention from SOL ecosystem investors and developers

-

More projects like Ethereal launching on Ethena Network, creating additional airdrop incentives for ENA holders

-

Prior to the next major ENA unlock, the team has strong incentives to pump the price—to fuel a positive feedback loop and secure higher exit prices for themselves

Moreover, over the past half-year, Ethena’s team has demonstrated exceptional business development capabilities—arguably the best among stablecoin projects in forging external partnerships, surpassing even market leader MakerDAO in aggressiveness and efficiency.

Factors currently weighing on ENA’s value and suppressing its price include:

-

ENA lacks tangible revenue distributions, relying instead on speculative staking use cases (e.g., securing multi-chain safety as AVS assets) and self-referential mechanics (“mining your own coin”)

-

Ethena’s actual profitability is weak. Massive subsidies to capture market share have led to severe net losses, borne entirely by ENA holders

-

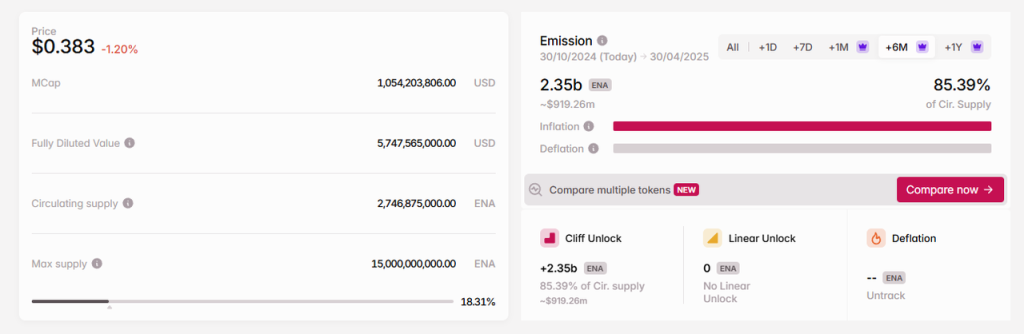

ENA faces significant inflationary pressure over the next six months—from ongoing campaign emissions and, more critically, the upcoming unlock of team and investor tokens in late March 2025. According to tokenomist.ai, ENA faces 85.4% inflation relative to current circulating supply over the next six months.

Data source: https://tokenomist.ai/

3.2 Quantitative Comparison

Ethena’s business model is fundamentally similar to other stablecoin projects. Its innovation lies in how it deploys raised capital—specifically, using it for perpetual futures arbitrage to generate returns.

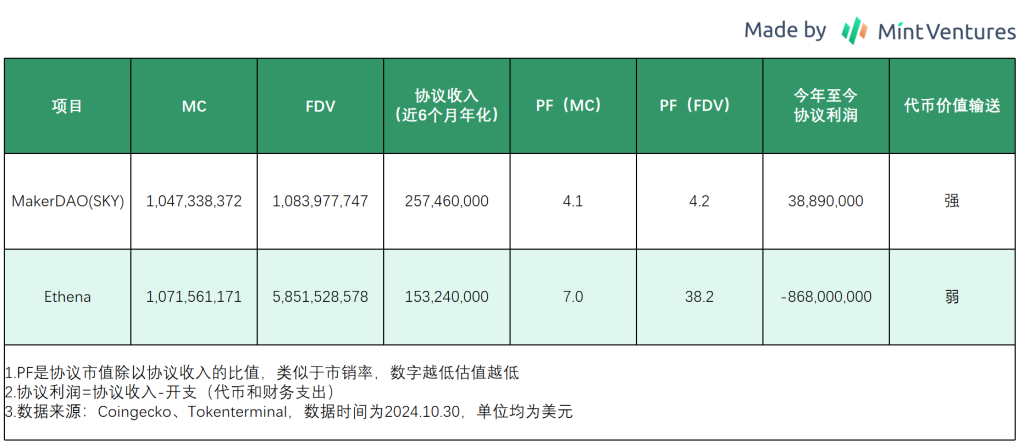

Therefore, we compare ENA against MakerDAO (now SKY), the largest stablecoin project by market cap, as a valuation benchmark.

Compared to the established protocol MakerDAO, ENA currently offers no valuation advantage in terms of protocol revenue or profitability.

Conclusion

While many regard Ethena as a representative innovative project of this cycle, its core business model is no different from other stablecoin projects: raise capital, conduct financial operations, and aggressively promote adoption of its debt instrument (the stablecoin) to minimize funding costs.

At this stage, Ethena—still in the early phase of stablecoin adoption—remains in a state of massive losses, contrary to claims by many KOLs that it is “highly profitable.” Its valuation is not undervalued compared to leading stablecoin projects like MakerDAO.

However, as a new entrant, Ethena has demonstrated exceptional business development agility, outperforming peers in partnership expansion. Like many DeFi projects in the previous cycle, rapid scale growth and increasing adoption can boost investor optimism, pushing up token prices. Higher token prices enable higher APYs, further expanding USDE’s scale—a self-reinforcing upward spiral.

Yet, such projects eventually reach a tipping point where the market realizes growth was fueled by token subsidies, and token price appreciation rests solely on sentiment rather than intrinsic value.

At that point, a race to exit begins.

In the end, only a few projects survive such downward spirals. Last cycle’s stablecoin star Luna (issuer of UST) is buried, Frax has shrunk dramatically, and Fei has ceased operations.

As a product with strong Lindy effect (the longer it exists, the stronger it becomes), Ethena and its USDE still require more time to prove the stability of its architecture and its ability to survive once subsidies are reduced.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News