What Does Ethena’s Price Movement Reveal About the Cryptocurrency Market?

TechFlow Selected TechFlow Selected

What Does Ethena’s Price Movement Reveal About the Cryptocurrency Market?

Ethena provides us with an exceptionally unique perspective to gain deep insights into the cryptocurrency derivatives market.

By: Kyle Soska

Translated by: Block Unicorn

The crypto market has remained in a risk-off state for several consecutive months. I’ve been closely analyzing various market data to identify potential signs of an impending shift. In this article, I’ll delve into the market structure of perpetual futures and examine market risk appetite using data from Ethena’s Transparency Dashboard.

In short: Ethena’s deployed capital is at a multi-year low—just 71% of its 2025 low point. This is not a critique of Ethena but rather a reflection of current market conditions. Directional short positions are nearly balanced with directional long positions—a situation that is exceptionally rare and historically unsustainable in crypto markets.

Cryptocurrency markets have long been characterized by extreme asset volatility and heavy use of leverage among traders. In my earlier research, “Understanding Crypto Derivatives: A BitMEX Case Study,” I explored the novel 100x perpetual contracts offered on BitMEX.

Since the BitMEX era, crypto futures have become the most actively traded product in the crypto market—generating 5–20x more volume than spot markets. As a leveraged trading venue for retail investors, perpetual contracts serve as a reliable barometer of risk appetite in crypto markets—and thus warrant close attention.

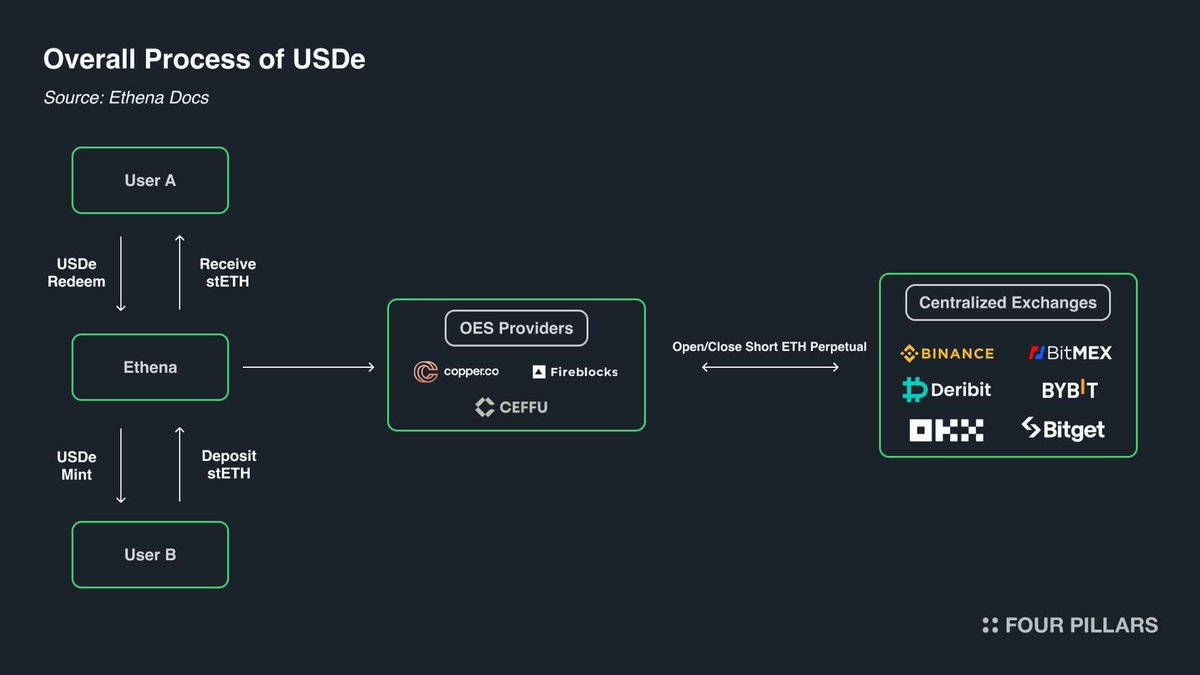

Ethena offers a uniquely insightful window into the crypto derivatives market. As illustrated below, Ethena executes crypto arbitrage trades. The strategy is straightforward: when crypto traders go long, Ethena acts as their counterparty and goes short. Ethena ensures it purchases assets equivalent in quantity to those sold short by traders. In a sense, Ethena provides a form of leverage service. Traders seek exposure to crypto price appreciation but lack sufficient capital; Ethena holds capital but has limited risk tolerance. Thus, traders borrow funds from Ethena via perpetual contracts—at a cost equal to the basis plus the funding rate.

Perpetual contracts are constructed such that each long contract corresponds one-to-one with a short contract. Each unit of open interest represents a cash flow agreement between two counterparties. Exchanges facilitate matching these contracts, ensuring every contract always has well-capitalized long and short holders. The table below shows the four possible outcomes of exchange-facilitated trades.

Perpetual Contract Matching Matrix

Every trade has a buyer and a seller. When both buyer and seller hold the same directional position—i.e., both long or both short—the exchange merely transfers ownership of the contract from one party to the other. Such transfers neither create nor destroy contracts. When the buyer is long and the seller is short, a new contract must be created: the buyer assumes a long position, the seller assumes a short position, and open interest increases by one. Conversely, if the seller is long and the buyer is short, the exchange can directly unwind both parties’ positions and cancel the newly released contract, reducing open interest by one.

So who typically holds these contracts in a normal market? I categorize contract holders into four main groups:

- [Long] Directional Longs

- [Short] Directional Shorts / Hedgers

a. Direct asset shorts / hedging

b. Hedging via structured products

- [Short] Basis Traders (e.g., Ethena, etc.)

- [Hybrid] Perpetual Arbitrageurs

Directional longs seek exposure. They are risk-tolerant participants whose demand for risk depends on their individual risk appetite.

Directional short traders include both investors seeking downside exposure and those hedging existing assets in a tax-efficient manner. Venture capital firms and employees compensated in tokens often hedge tokens scheduled to unlock at current prices. For altcoins, many markets suffer from insufficient trading volume to support effective direct hedging—or even lack viable hedging instruments altogether. In such cases, firms like Cumberland, Wintermute, FalconX, Flowdesk, and Amber construct dynamically managed synthetic positions—shorting highly liquid, correlated assets such as Bitcoin and Ethereum—to hedge exposure in less liquid markets (e.g., Monad). Projects like Neutrl adopt similar strategies, treating such hedging as a yield-generating activity.

Basis traders are opportunistic shorts. They show no interest in directional risk exposure but instead step in to fill excess demand from directional longs when market supply-demand imbalances arise. Under most market mechanisms, long demand exceeds short demand, and longs serve to bridge the basis gap. Their position sizes are typically highly elastic.

Perpetual arbitrageurs simultaneously hold both long and short perpetual positions. Their role is to interconnect disparate perpetual markets and correct minor price discrepancies—provided the arbitrage profit exceeds transaction fees. At any given moment, their long and short positions perfectly offset each other.

By construction, all perpetual contracts maintain a strict 1:1 ratio between long and short positions. Therefore, we know:

Directional Longs + Arbitrage Longs = Directional Shorts + Basis Shorts + Arbitrage Shorts

Moreover, the structure of perpetual arbitrage tells us:

Arbitrage Longs = Arbitrage Shorts

Subtracting this term from the first equation yields:

Directional Longs = Directional Shorts + Basis Shorts

Ethena serves as a proxy for all basis shorts—offering valuable insight into the divergence between directional longs and shorts.

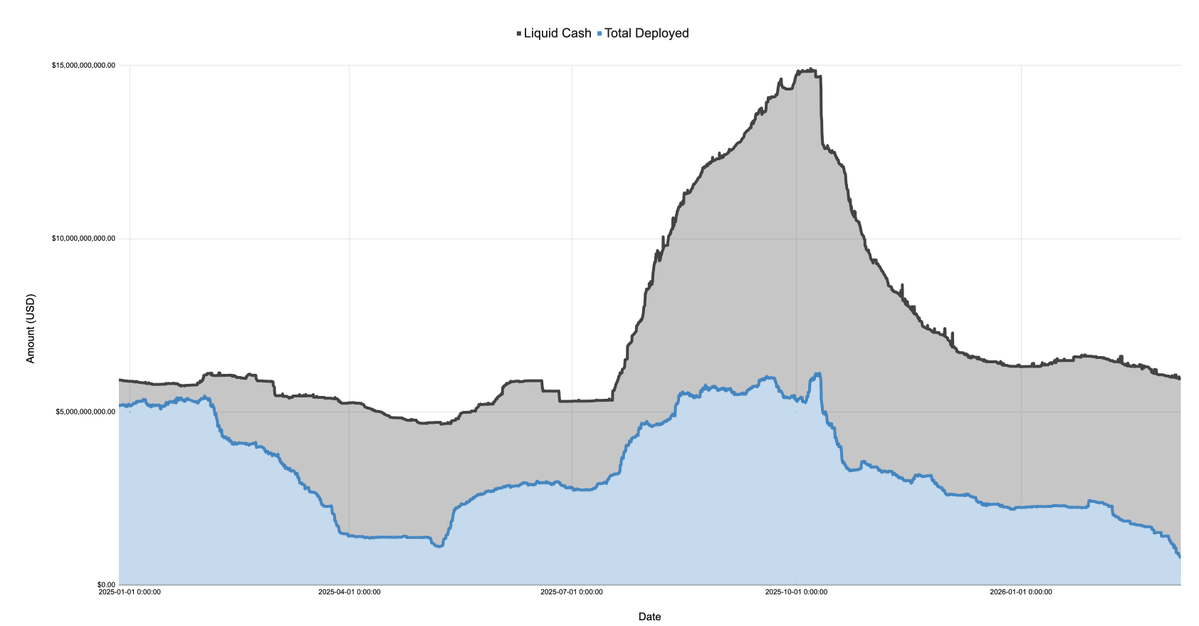

The chart below shows Ethena’s self-reported balance sheet, broken down into cash and deployed capital, covering December 27, 2024, through March 7, 2026:

Markets turned sharply risk-off in January 2025 following the launch of the $TRUMP token, then continued declining amid early tariff discussions and through April’s “Liberation Day.” During this period, Ethena’s deployed capital plummeted from over $5 billion to just $1.108078914 billion—a drop exceeding 75%.

Note that Ethena’s deployed capital serves as a proxy for excess long demand in the market. While Ethena is not the sole participant in such trades, its scale—sometimes reaching ~25% of Binance’s or Bybit’s—is substantial enough that, given ample cash reserves, it expands positions to meet any unmet long demand. This suggests that while total long demand may not have fallen 75% by April 2025, the excess demand unmet by directional shorts did indeed fall by 75%.

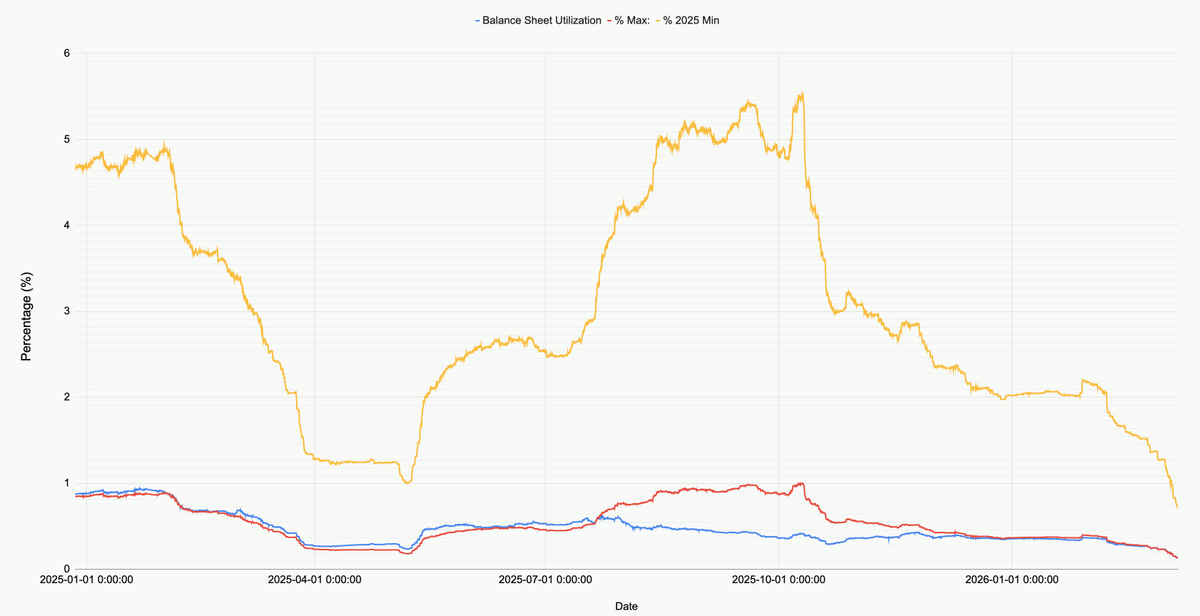

The chart below illustrates Ethena’s deployed capital relative to its total size, its 2025 lows, and its 2025 highs.

Examining the current market, Ethena’s total deployed capital across all markets (BTC, ETH, SOL, BNB, XRP, HYPE) stands at just $791.2415456 million—71% of its 2025 low and only 12.9% of its pre-October 10 peak. This figure is not a criticism of Ethena but rather a reflection of prevailing market conditions: net long demand is at a historic low.

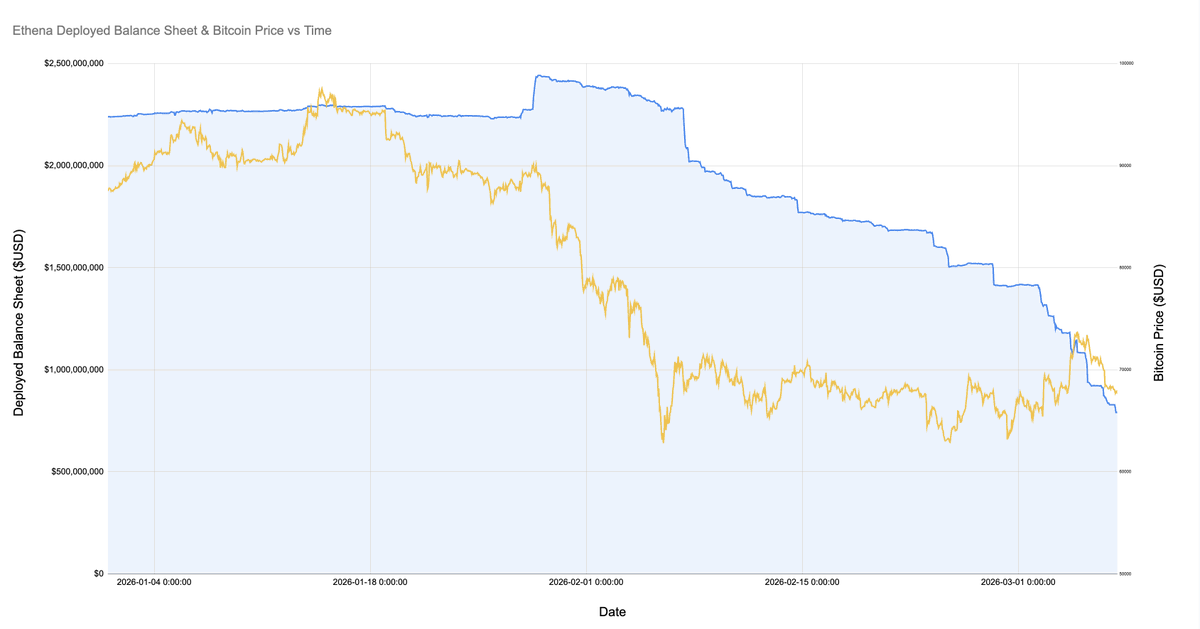

Notably, during the market crash when Bitcoin fell to $60,000, Ethena deployed over $2 billion. Since February 8, 2026—just one month ago—Ethena’s deployed capital has plunged a staggering 60%!

The chart below zooms in on Ethena’s deployed capital alongside Bitcoin’s price action since January of this year.

Since Bitcoin’s price dropped to $60,000, Ethena’s basis position has shrunk over 60%—from over $2 billion to under $800 million. This decline is puzzling, given the relative market calm during this period. Contributing factors include:

1. Gradual unwinding of profitable but unsustainable basis trades established after the February selloff (where basis turned negative, yet funding rates also turned negative).

2. Increased hedging activity from directional shorts and price-insensitive participants, squeezing out opportunistic basis traders.

3. Insufficient long demand seeking leveraged exposure.

In my view, factors 1 and 2 jointly explain the majority of this phenomenon, while factor 3 plays a negligible role. As shown above, overall open interest in Bitcoin (and other major cryptos) has remained relatively stable during Ethereum’s gradual exit phase. Meanwhile, funding rates have stayed persistently negative, with cumulative funding rates across multiple exchanges turning negative for many cryptos—including SOL. This signals growing demand to short or hedge some form of risk exposure.

If I were to speculate, I’d say both mid- and small-cap crypto firms and venture capital firms are facing crises. Consider small-cap projects like Eigen, Grass, and Monad. Hundreds of such tokens exist—each representing dozens of VCs and a company with capital and staff. VCs need to limit losses and lock in gains to meet fund objectives, while companies need to preserve liquidity and retain employees. This creates a situation where all participants strive to extract maximum value from every “rock”—achieving this via actively managed structured products executing relatively crowded trades that short baskets of correlated assets.

We observed these structured products during Ethereum’s explosive rally days—triggering short squeezes across numerous mid- and small-cap cryptos. Another piece of evidence is the significant displacement of opportunistic basis trading—such as Ethena’s.

Regardless of the precise cause, one thing is certain: this marks the first time in crypto market history that directional longs and directional shorts have reached near-equilibrium. There is no compelling reason why this state cannot become the new normal, nor proof that this market regime must change—but across other asset classes and markets, such sustained equilibrium would be highly unusual.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News