insights4.vc Q3 Crypto Venture Capital Report: Rise of Mid-Sized Funds, AI-Led Innovation, and Shift in Investment Focus Toward Early-Stage Startups

TechFlow Selected TechFlow Selected

insights4.vc Q3 Crypto Venture Capital Report: Rise of Mid-Sized Funds, AI-Led Innovation, and Shift in Investment Focus Toward Early-Stage Startups

The cryptocurrency venture capital landscape in the third quarter of 2024 showed cautious optimism, with a rebound in fundraising activities and growing interest from institutional investors.

Author: insights4.vc

Translation: TechFlow

Over the past decade, the cryptocurrency industry has undergone significant changes, with venture capital emerging as a key driver of innovation and growth. From the 2017 ICO boom to the rise of decentralized finance (DeFi) in 2020, the sector has experienced cycles of rapid expansion followed by periods of correction. Today, as we enter the third quarter of 2024, the crypto venture capital landscape is showing signs of recovery after a challenging period. For a detailed historical overview of the VC landscape, refer to our paper "The Evolution of Crypto Venture Capital: A 15-Year Retrospective."

Fundraising Rebound

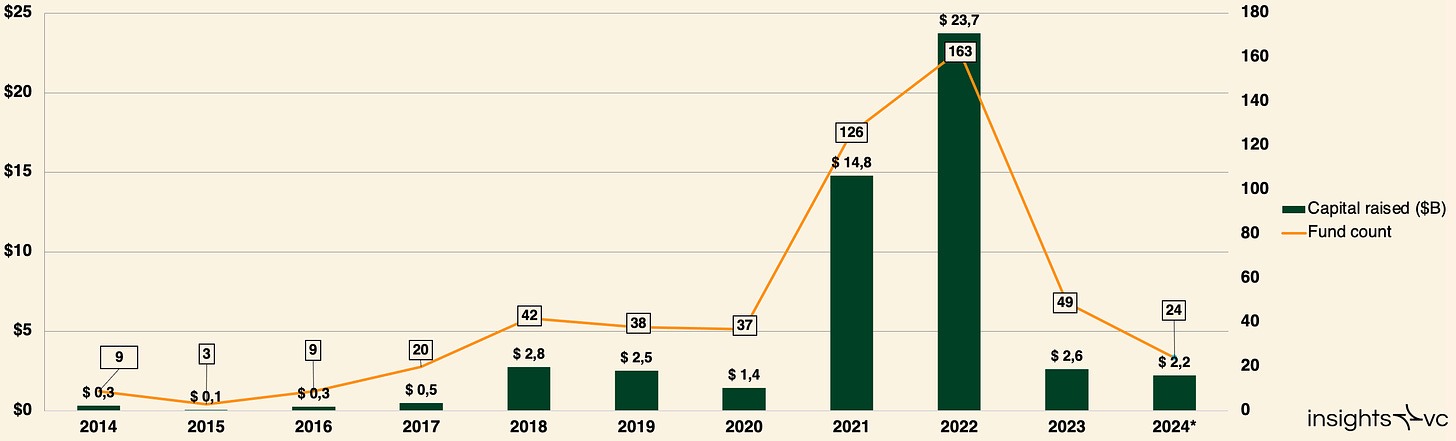

Crypto venture capital fundraising dynamics (as of August 30, 2024)

As of August 30, 2024, 24 funds have raised $2.2 billion collectively, indicating a potential rebound that could surpass 2023’s total fundraising volume. This recovery is primarily driven by:

-

Market stability: In March 2024, the total market capitalization of crypto reached 93% of the previous cycle's peak.

-

Institutional participation: Traditional financial institutions such as BlackRock, Fidelity Investments, and Franklin Templeton have entered the crypto space, bolstering market confidence.

-

Project maturity: Investments made during the 2020–2022 boom are maturing, presenting attractive exit or follow-on investment opportunities.

Investor Sentiment

According to a survey by Coinbase Institutional, 64% of existing institutional investors plan to increase their crypto allocations over the next three years, while 45% of non-investors expect to begin investing in the same timeframe. Additionally, nearly 60% of respondents believe crypto prices will rise within the next year.

Shift Toward Mid-Sized Funds

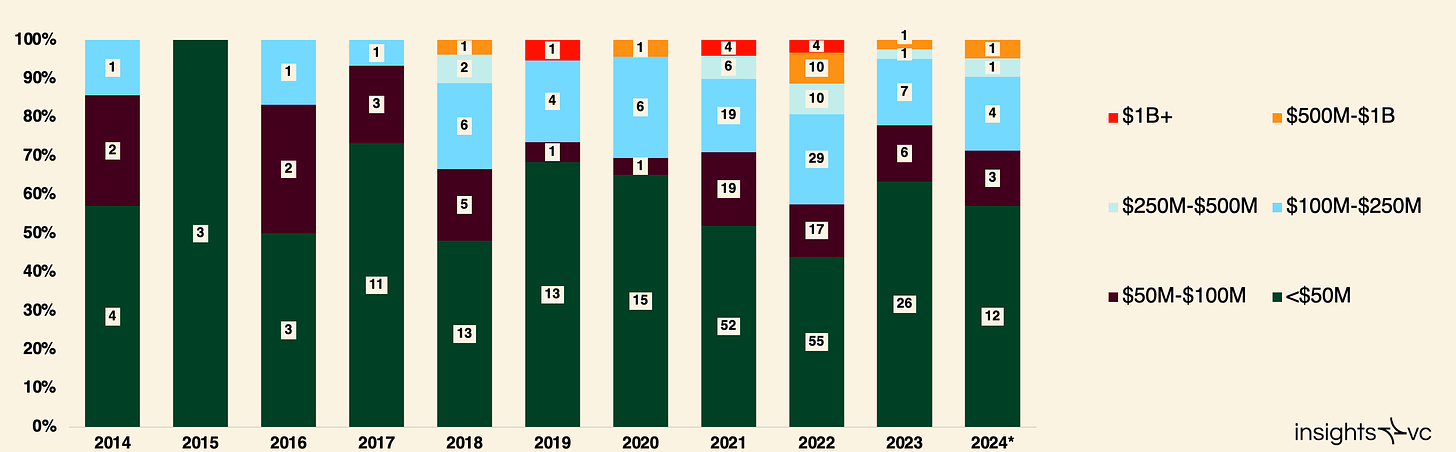

Number of crypto venture capital funds by size (as of August 30, 2024)

In the past, the crypto venture capital space was dominated by small funds (valued at $100 million or less), reflecting the industry’s early-stage nature. However, since 2018, capital has gradually shifted toward mid-sized funds ($100 million to $500 million). The median fund size increased by 76.0% from $25 million in 2023 to $41.3 million in 2024.

Large funds (valued at $1 billion or more) saw significant growth between 2019 and 2022 but have shown little activity in 2023 and 2024. Key challenges include:

-

Difficulty deploying capital: Large funds struggle to find startups requiring substantial funding.

-

Valuation pressure: The need for large investments drives up valuations, increasing risk. Nevertheless, funds like Pantera Capital (targeting $1 billion) and Standard Crypto (targeting $500 million) remain active. These firms are expanding their investment scope beyond crypto into areas such as artificial intelligence (AI) to deploy capital more effectively.

Dominance of Emerging Managers

In terms of fund count, emerging managers continue to dominate, raising between 77% and 87% of total funds annually over the past five years. This trend stems from:

-

Technical specialization: The crypto domain demands deep technical expertise, which emerging managers often possess.

-

Niche focus: Due to the specialized nature of crypto, generalist VCs rarely launch new crypto-specific funds.

The share of first-time funds has declined from approximately 58% in 2020 to 45.8% in 2024. However, with market recovery underway, we anticipate a "barbell effect," where both first-time managers and established native crypto fund managers achieve notable fundraising success.

Lengthening Fundraising Cycles

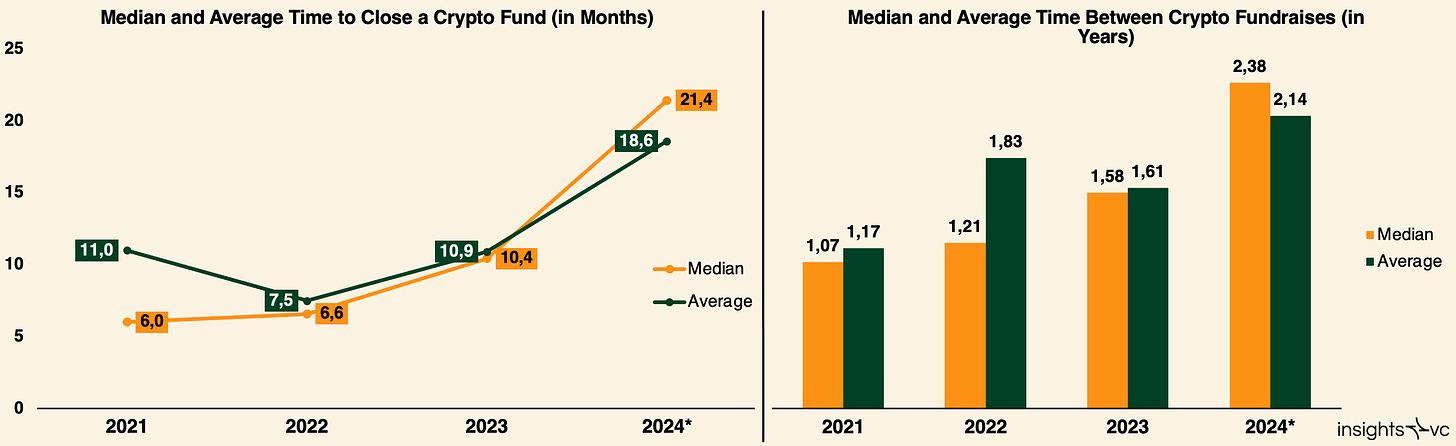

Note: Data as of August 30, 2024

From 2021 to 2024, the median interval between fund raises increased from 1.1 years to 2.4 years, while the median time to close a fund rose from 6 months to 21.4 months. Contributing factors include:

-

Increased investor caution: Limited partners (LPs) have become more selective, requiring thorough due diligence.

-

Market conditions: During bear markets, fund managers slow capital deployment. Without meaningful returns distributed to LPs, crypto-savvy investors may remain cautious. Fund managers holding tokens might begin liquidating positions—even at a loss—to demonstrate some realized returns.

Venture Capital in Q3 2024

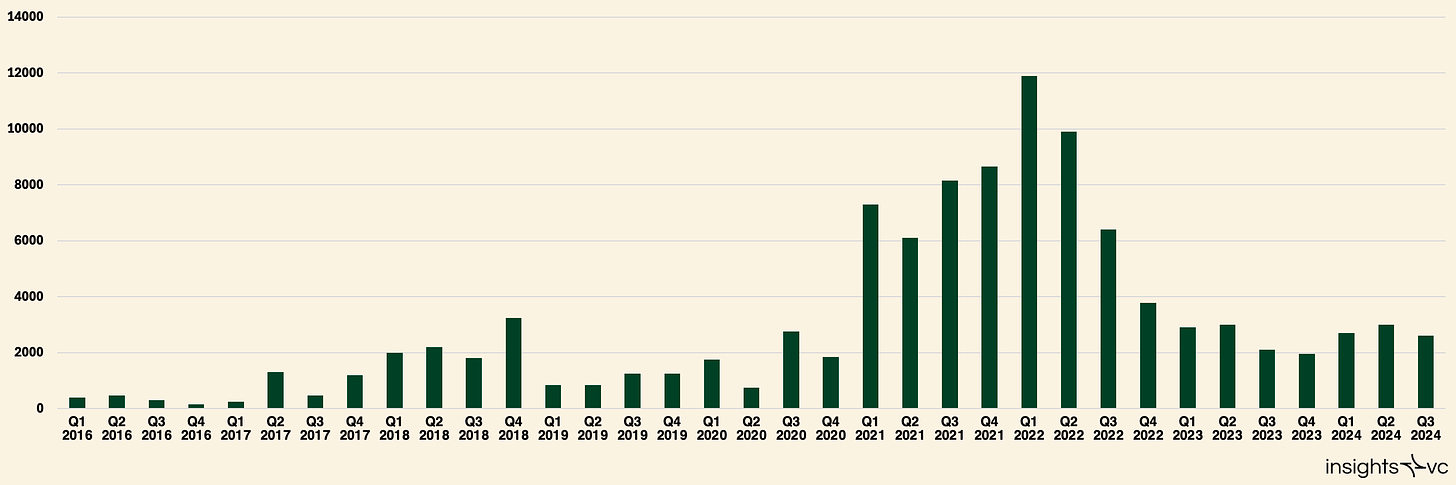

Crypto venture capital by quarter (2016–2024)

In Q3 2024, venture capitalists invested approximately $2.7 billion in crypto and blockchain startups, down 10% from $3.0 billion in Q2 2024. This decline reflects a more cautious investment approach amid ongoing market uncertainty.

Despite the quarterly dip, total venture investment in 2024 is still on track to meet or slightly exceed 2023 levels. This suggests that while short-term fluctuations occur, overall interest in crypto and blockchain venture investments remains stable on an annual basis.

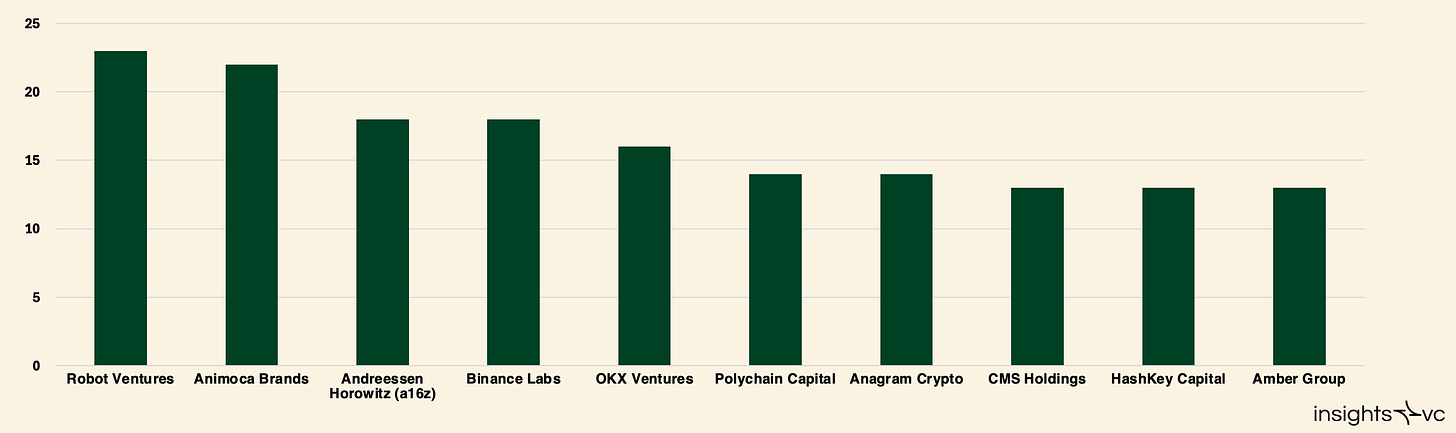

Most Active Investors

Most active investors (July 1, 2024 – October 15, 2024)

Between July 1 and October 15, 2024, the most active investors in the crypto space demonstrated continued commitment to fostering innovation, particularly in early-stage ventures. Leading the pack was Robot Ventures, completing 23 investments. Animoca Brands followed closely with 22 investments, while Andreessen Horowitz (a16z) and Binance Labs each made 18 investments. OKX Ventures participated in 16 deals, and Polychain Capital and Anagram Crypto each joined 14 investments. CMS Holdings, HashKey Capital, and Amber Group each completed 13 investments, solidifying their positions as top players in the crypto investment arena.

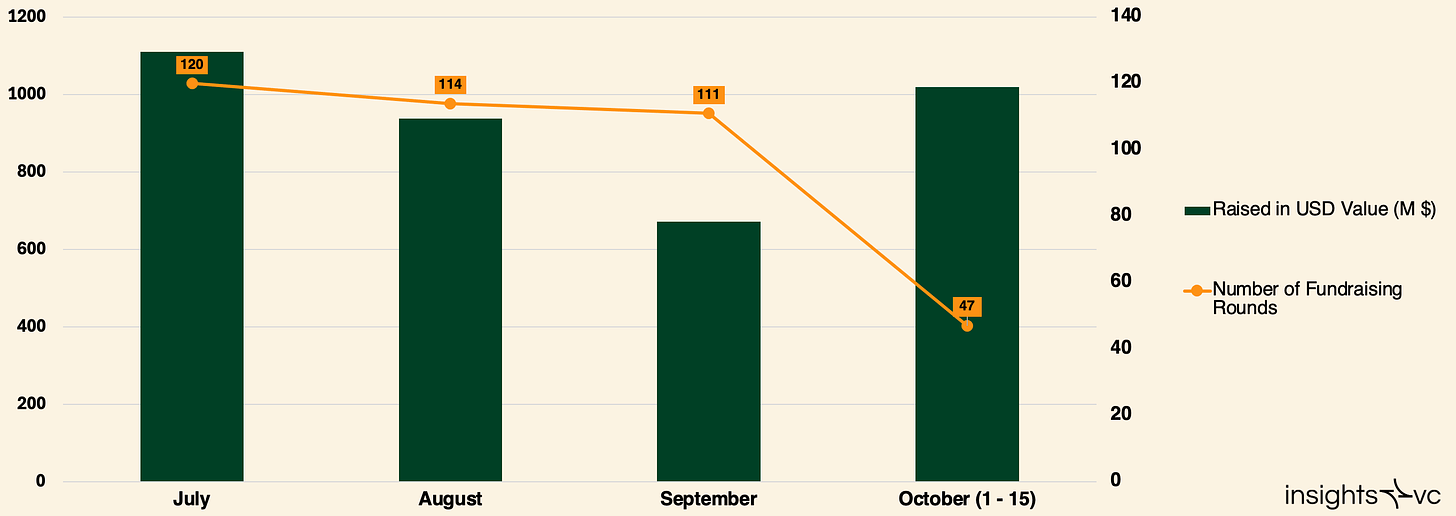

Funding Rounds: July 1 – October 15, 2024

Total raised and number of funding rounds (July 1 – October 15, 2024)

Despite an overall decline in venture investment, several major funding rounds between July 1 and October 15, 2024 highlighted sustained interest in high-potential projects. Praxis Society stood out by raising $525 million in an undisclosed round, backed by prominent figures including Dan Romero, Fred Ehrsam, Brian Armstrong, and Erik Voorhees.

In Q3 2024, Celestia led the pack by raising $100 million for its modular data availability network. This was followed by Sentient, which raised $85 million for its open-source AI development platform. Story Protocol secured $80 million for blockchain-based intellectual property management, while Infinex raised $65.2 million for its decentralized exchange. Chaos Labs, focused on securing crypto protocols, raised $55 million, and Sahara AI raised $37 million for its decentralized AI network. Other notable raises included Drift Protocol ($25 million), Helius ($21.7 million), B3 Fun ($21 million), and Caldera ($15 million) for modular blockchain development.

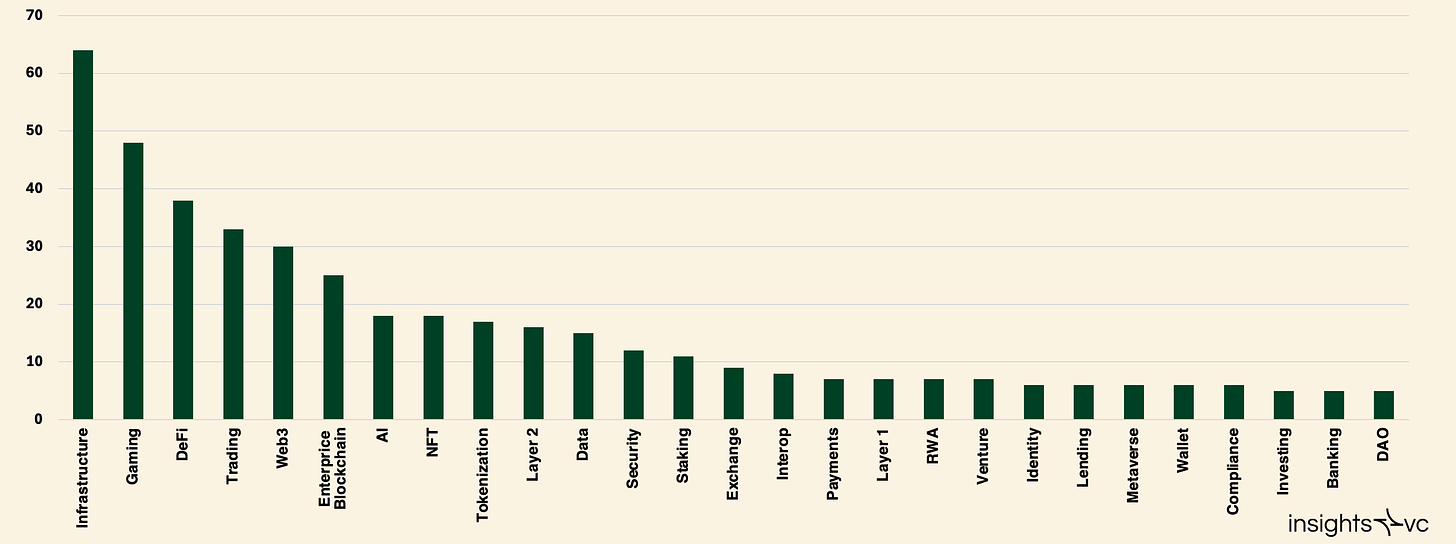

Overview of crypto venture capital deals in Q3 2024 by category

Analysis shows infrastructure projects led in deal count with 64 transactions, followed by gaming with 48 and DeFi with 38. This indicates strong market focus on infrastructure and blockchain development, alongside growing interest in gaming and decentralized finance.

Capital Investment vs. Bitcoin Price

Historically, there has been a strong correlation between Bitcoin’s price and the amount invested in crypto startups. However, since January 2023, this relationship has significantly weakened. Despite Bitcoin reaching new all-time highs, venture investment activity has failed to grow correspondingly.

Possible reasons:

-

Diminished investor interest: Regulatory uncertainty and market volatility may have made institutional investors more cautious.

-

Shift in market focus: The current market emphasis on Bitcoin may be overshadowing other crypto investment opportunities.

-

VC market conditions: A broader downturn in the venture capital market has also impacted crypto investments.

Investment Trends

In Q3 2024, 85% of venture capital flowed into early-stage companies, with only 15% going to late-stage companies. This suggests investors are prioritizing startups with high growth potential, likely due to lower valuations and higher return prospects. While pre-seed deal activity dipped slightly, it remains robust compared to prior cycles, reflecting sustained interest in early-stage ventures.

Valuations for VC-backed crypto companies hit a low at the end of 2023 but began recovering in Q2 2024 as Bitcoin reached new highs. In Q3 2024, the median pre-money valuation was $23 million, with an average deal size of $3.5 million.

In terms of capital allocation by stage, most investments in Layer 1, enterprise blockchains, and DeFi were concentrated in early-stage companies, highlighting a focus on innovation. In contrast, mining companies attracted more late-stage funding, likely due to their capital-intensive operations.

Industry maturity analysis shows early-stage investments still dominate across most categories, underscoring the market’s continued emphasis on new entrants and innovative ventures. Late-stage investments are more concentrated in mining and infrastructure, where mature companies require substantial capital for expansion.

The proportion of early-stage deals remains high across categories, consistent with trends seen in Q2 2024. Late-stage deal counts remained stable compared to the previous quarter, indicating steady investment in mature companies.

Emerging Trends in Q3 2024

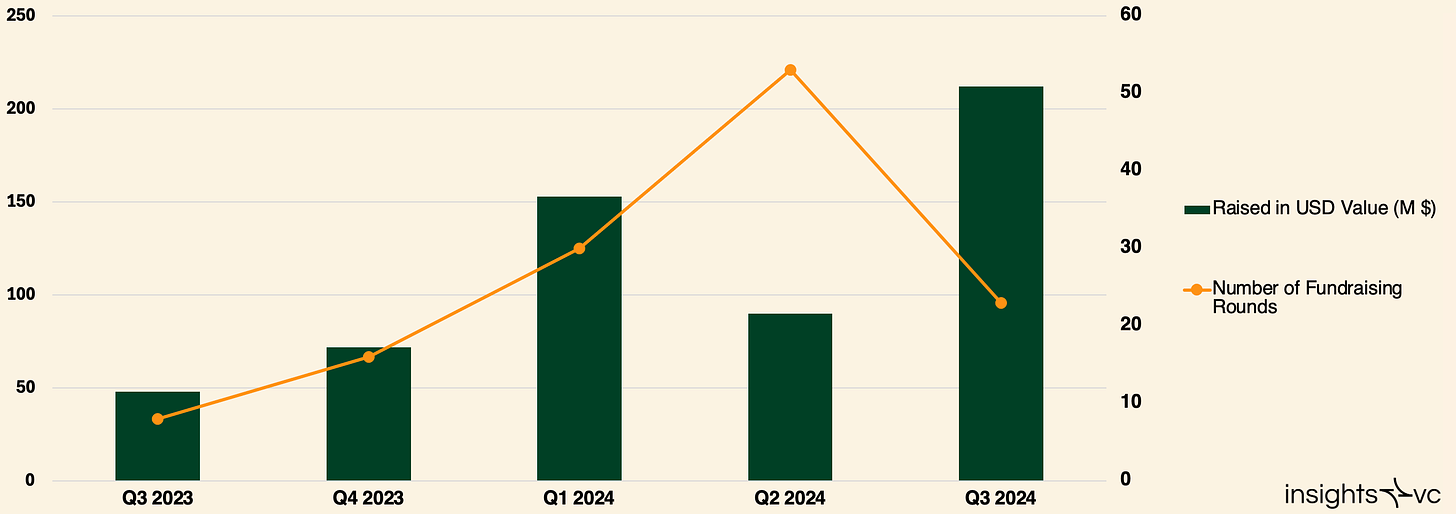

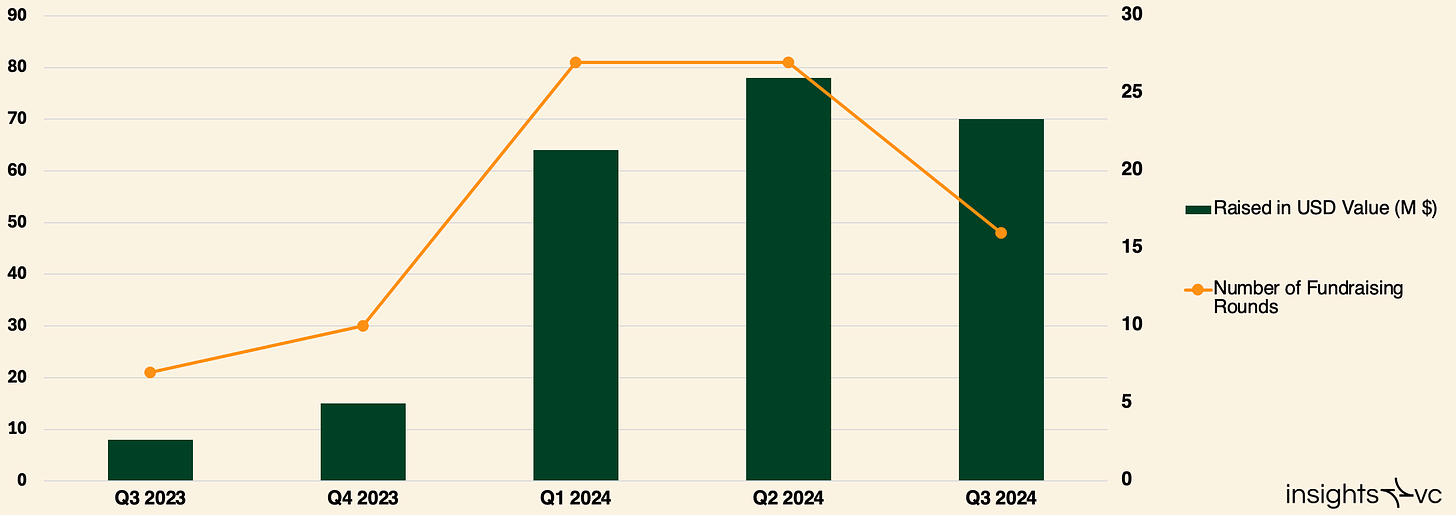

In Q3 2024, AI emerged as a major theme in venture capital, particularly in year-over-year growth, though it did not dominate in the number of announced rounds. Interest in AI surged, driven by open-source models, AI’s impact on content creation, and the potential of decentralized inference. Funding for AI crypto projects grew by 340% compared to Q3 2023, reflecting strong investor enthusiasm. Leading this trend were Sentient ($85 million), Sahara AI ($37 million), and Balance ($30 million).

Amount raised by AI crypto projects from Q3 2023 to Q3 2024

One of the most notable growth areas was Decentralized Physical Infrastructure Networks (DePIN), which saw a 691% increase in fundraising in Q3 2024 compared to the same period in 2023. Key deals included $18 million raised by DAWN Internet (for detailed analysis, click here), $12 million granted to Project Zero 2050, $10 million each to Mawari XR and Pipe Network, and $9 million to Daylight Energy.

DePIN project fundraising from Q3 2023 to Q3 2024

Conclusion

The crypto venture capital environment in Q3 2024 reflects cautious optimism, with fundraising activity rebounding and institutional interest rising. The shift toward mid-sized funds and the continued dominance of emerging managers indicate the industry’s adaptability and gradual maturation. Although venture investment declined slightly in the short term and fundraising cycles have lengthened, sustained focus on early-stage ventures and emerging trends like AI integration highlight the ecosystem’s resilience and readiness for future growth. Overall, the sector demonstrates underlying strength, signaling potential momentum ahead.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News