Arthur Hayes: How Can Project Teams Avoid the CEX Trap and Use DEX to Stage a Comeback in the Crypto Market?

TechFlow Selected TechFlow Selected

Arthur Hayes: How Can Project Teams Avoid the CEX Trap and Use DEX to Stage a Comeback in the Crypto Market?

Focus on long-term value rather than short-term price fluctuations and market hype.

Written by: Arthur Hayes, Co-founder of BitMEX

Translated by: Ismay, BlockBeats

Editor's Note: In this article, Arthur Hayes dives deep into the current state of token listings in the crypto market, particularly examining how high listing fees charged by centralized exchanges (CEXs) impact both project teams and investors. Using Auki Labs as a case study, the article highlights the advantages of launching on decentralized exchanges (DEXs), emphasizing the importance of focusing on product development and user growth.

For projects blindly chasing CEX listings, Hayes urges them to focus on long-term value rather than short-term price fluctuations and market hype.

Below is the original text:

PvP, or "player versus player," is a term frequently used by shitcoin traders to describe the current market cycle. It conveys a predatory sentiment—victory comes at someone else’s loss. This mindset is common in traditional finance (TradFi). The core purpose of crypto capital markets should be enabling those who risk their precious capital early on to reap rewards as promising projects grow alongside Web3. Yet we have strayed far from the righteous path laid out by the great Satoshi, further advanced by the archangel Vitalik through Ethereum's wildly successful ICO.

In this bull market, Bitcoin, Ethereum, and Solana are shining bright. However, I define “new issuance” as tokens launched this year—these new launches have performed terribly for retail investors. Meanwhile, VC firms remain unaffected. Hence, the label PvP fits this market cycle well. The result has been a series of projects with high FDVs but extremely low circulating supplies. After launch, these token prices flush straight down the toilet like ordinary waste.

While this reflects market sentiment, what does the data say? The sharp analysts at Maelstrom did some deep digging to answer several puzzling questions:

Is it worth paying exchange listing fees for a better chance at price appreciation?

Are projects launching at excessively high valuations?

Before diving into the data to answer these questions, I want to offer unsolicited advice to projects waiting for the market to recover before launching. To strengthen my argument, I’d like to highlight one project in Maelstrom’s portfolio—Auki Labs. They went against the grain, choosing to list first on a DEX instead of a CEX, with a relatively low FDV. They want retail investors to profit alongside them as they succeed in building a real-time spatial computing marketplace. They also despise the exorbitant listing fees charged by major exchanges and believe there’s a better way to return more value to end users—not to big shots living in my neighborhood here in Singapore.

Sample Set

We analyzed 103 projects that listed on major shitcoin trading platforms in 2024. This isn’t an exhaustive list of all listings that year, but it’s a representative sample.

"Pump the price!"

This is something founders often repeat during advisory calls: "Can you help us get on a CEX? That way our token price will skyrocket." Well… I’ve never fully believed that. I think the secret to success for any Web3 project lies in creating a useful product or service and steadily growing paying users. Of course, if you have a garbage project whose value rests solely on Irene Zhao retweeting you, then yes—you need a CEX so you can dump it onto retail. Most Web3 projects fall into this category, but hopefully not those backed by Maelstrom… Akshat, take note!

Post-listing returns refer to days after listing; LTD means performance since going live.

No token price skyrocketed on any exchange. If you were hoping for a moonshot chart after paying hefty exchange listing fees, sorry—but no such luck.

Who won? VCs won. Media token prices rose 31% above the FDV from previous private funding rounds. I call this the "VC extraction premium." Later in this article, I’ll explain in detail the distorted incentives driving VCs to delay liquidity events as long as possible. But for now, just know that most everyone else is simply getting played. That’s why drinks are free at conference networking events… haha.

Now let me stir the pot a bit. First, CZ is a hero in crypto, enduring torment from the devils of TradFi inside a medium-security prison in the United States. I love CZ and respect his skillful ability to funnel money into his pockets across every corner of the crypto capital markets. But… but… paying top dollar for a Binance listing isn’t worth it. Let me clarify: having Binance as your token’s primary listing venue holds little inherent value. What *is* valuable is when Binance picks up your project as a secondary listing—for free—because of strong fundamentals and an active community.

Founders often ask me on calls: "Do you have connections with Binance? We *must* list there, otherwise our token won’t go up." This "Binance-or-bust" mentality benefits Binance immensely, allowing them to charge the highest all-inclusive listing fees in the industry.

Returning to the table above, while tokens listed on Binance outperformed those on other major platforms on a relative basis, they still declined in absolute terms. Therefore, a Binance listing doesn’t guarantee price appreciation.

A project must give or sell tokens—often scarce in supply—to exchanges in exchange for listing. Some exchanges are even allowed to invest in projects at extremely low FDVs regardless of the latest private round valuation. These tokens could have instead been distributed to users completing growth-driving tasks. A simple example: trading apps rewarding traders with tokens upon reaching certain volume targets—aka liquidity mining.

Selling tokens to listing exchanges is a one-time transaction. But a positive flywheel created by boosting user engagement delivers ongoing returns. So if you’re sacrificing precious tokens just for a listing and gaining only a few percentage points over peers, you, as a founder, are wasting valuable resources.

The Price Isn't Right

As I often tell Akshat and his team: the reason you all have jobs at Maelstrom is because I believe you can build a portfolio of top-tier Web3 projects that outperform my core holdings in Bitcoin and Ethereum. Otherwise, I’d just keep buying BTC and ETH with my spare cash instead of paying salaries and bonuses. As you can see here, if you bought newly listed tokens at or shortly after launch, you would have significantly underperformed Bitcoin—the hardest money ever created—and two leading Layer-1 decentralized computing platforms, Ethereum and Solana. Given these results, retail investors should absolutely avoid buying freshly listed tokens. If you want exposure to crypto, just hold Bitcoin, Ethereum, and Solana.

This tells us that projects need to reduce their valuations by 40% to 50% at listing to become relatively attractive. Who loses when tokens list at lower prices? VCs and CEXs.

You might assume VCs aim for positive returns, but the most successful ones understand they’re actually playing an asset accumulation game. If you can charge management fees—typically 2%—on a large nominal fund size, you earn money regardless of whether investments appreciate. When investing in illiquid assets like early-stage token projects—essentially future promises of tokens—how do you inflate their value? You convince founders to keep raising private rounds at ever-higher FDVs.

When private round FDVs rise, VCs can revalue their illiquid portfolios upward, showing huge unrealized gains. These impressive track records allow them to raise subsequent funds, charging higher management fees based on larger fund sizes. Plus, VCs don’t get paid unless they deploy capital. But it’s not easy—especially since many Western-based VCs aren’t allowed to buy liquid tokens. They can only invest in equity of a management company and attach agreements granting investors warrants for tokens from developed projects. This is exactly why SAFTs ("Simple Agreements for Future Tokens") exist. If you want VC funding and they have ample dry powder, you must play along.

For many VCs, a liquidity event is harmful. When it happens, gravity kicks in and token values rapidly revert to reality. For most projects, the reality is they haven’t built products or services compelling enough for users to pay real money for—rendering their sky-high FDVs unjustifiable. At that point, VCs must write down their book values, negatively impacting reported returns and fee bases. Thus, VCs push founders to delay token launches as long as possible and continue raising successive private rounds. The end result? When projects finally list, token prices crash like stones—as we’ve just witnessed.

Before I completely bash VCs, let’s talk about the "anchoring effect." Sometimes human thinking is really dumb. If a shitcoin opens trading at a $10 billion FDV but is actually worth $100 million, you might sell, causing massive selling pressure that drops the price 90% to $1 billion, after which trading volume dries up. Still, VCs can book-value this illiquid shitcoin at $1 billion—a figure usually far above what they originally paid. Even amid collapse, opening at an unrealistic FDV still benefits VCs.

CEXs have two reasons to favor high FDVs. First, trading fees are calculated as a percentage of the token’s notional value. Higher FDV means more revenue and fees for the exchange, regardless of whether the project goes up or down. Second, high FDV with low circulation benefits exchanges because vast amounts of unallocated tokens can be directed to them. According to our sample data, the median circulating supply ratio across projects was 18.60%.

Listing Costs

I’d like to briefly discuss the cost of listing on CEXs. The biggest issue in current token issuance is inflated initial pricing. As a result, almost no project can achieve a successful launch regardless of which CEX secures the primary listing right. And to make matters worse, overpriced projects must pay large quantities of tokens and stablecoins just for the privilege of “listing garbage.”

Before commenting on these fees, let me emphasize: I don’t think it’s wrong for CEXs to charge listing fees. Exchanges invest heavily in building user bases and need to recoup costs. If you’re a CEX investor or token holder, you should appreciate their business acumen. However, as an advisor and token holder, if my project gives tokens to CEXs instead of users, it harms the project’s future potential and negatively impacts its trading price. Therefore, I either advise founders to stop paying listing fees and focus on acquiring more users—or urge CEXs to drastically lower their prices.

CEXs extract value from projects in three main ways:

-

Directly charging listing fees.

-

Requiring projects to post a deposit, refundable if the project delists.

-

Mandating that projects spend a specified amount on marketing via the platform.

Typically, each CEX’s listing team evaluates projects. The worse the project, the higher the fee. As I often tell founders: if your project lacks users, you need a CEX to dump your “garbage” into the market. But if your project has product-market fit and a healthy, growing ecosystem of real users, you don’t need a CEX—your community will support your token price anywhere.

Listing Fees

Among premium CEXs, Binance charges up to 8% of a project’s total token supply as a listing fee. Most other CEXs charge between $250,000 and $500,000, typically paid in stablecoins.

Deposit

Binance employs a clever strategy requiring projects to purchase BNB and stake it as collateral. If the project delists, the BNB is returned. Binance demands up to $5 million worth of BNB as deposit. Most other CEXs require deposits of $250,000 to $500,000 in stablecoins or the exchange’s native token.

Marketing Spend

Binance mandates at the high end that projects distribute 8% of their token supply through platform airdrops and other activities targeting Binance users. Mid-tier CEXs require up to 3% of supply. At the lower end, CEXs demand marketing expenditures of $250,000 to $1 million, payable in stablecoins or project tokens.

All told, listing on Binance could cost you 16% of your token supply plus $5 million in BNB purchases. Even if Binance isn’t the primary exchange, projects still face nearly $2 million in token or stablecoin expenses.

To any CEX challenging these figures, I strongly recommend publishing transparent accounts of every fee or mandatory expense. I gathered this data from multiple projects that evaluated major CEX costs—some numbers may be outdated. Let me reiterate: I don’t believe CEXs are doing anything wrong. They own a valuable distribution channel and are maximizing its worth. My complaint is that post-listing token performance fails to justify the fees paid by project founders.

My Advice

The game is simple: ensure your users or token holders become wealthy as your project succeeds. I’m speaking directly to you—project founders.

If you must, conduct only a small private seed round to build a product for a very limited use case. Then launch your token. Since your product is far from achieving true product-market fit, the FDV should be very low. This sends signals to your users. First, it’s risky—that’s why they’re getting in so cheap. You might fail, but your users stick with you because they entered at rock-bottom prices. They believe in you, giving you more time to figure things out. Second, it shows you want your users to join you on a wealth-building journey. This motivates them to spread the word about your product or service, knowing that broader adoption could yield substantial returns.

Currently, due to poor performance of most newly listed projects, many CEXs are under pressure to accept only “high-quality” projects. Given how easy it is to “fake it till you make it” in crypto, identifying truly outstanding projects is extremely difficult. Garbage in, garbage out. Each major CEX has preferred metrics they view as leading indicators of success. Generally, very young projects won’t meet their standards. Screw it—there’s something called a DEX.

On DEXs, creating a new trading market is permissionless. Imagine you’re a project that raised $1 million in USDe (Ethena USD) and want to release 10% of your token supply to the market. You can create a Uniswap liquidity pool consisting of $1 million USDe and 10% of your token supply. Click a button, and the automated market maker sets the clearing price based on market demand. You pay nothing for this. Now your loyal users can immediately buy your token, and if you truly have an active community, the price can surge quickly.

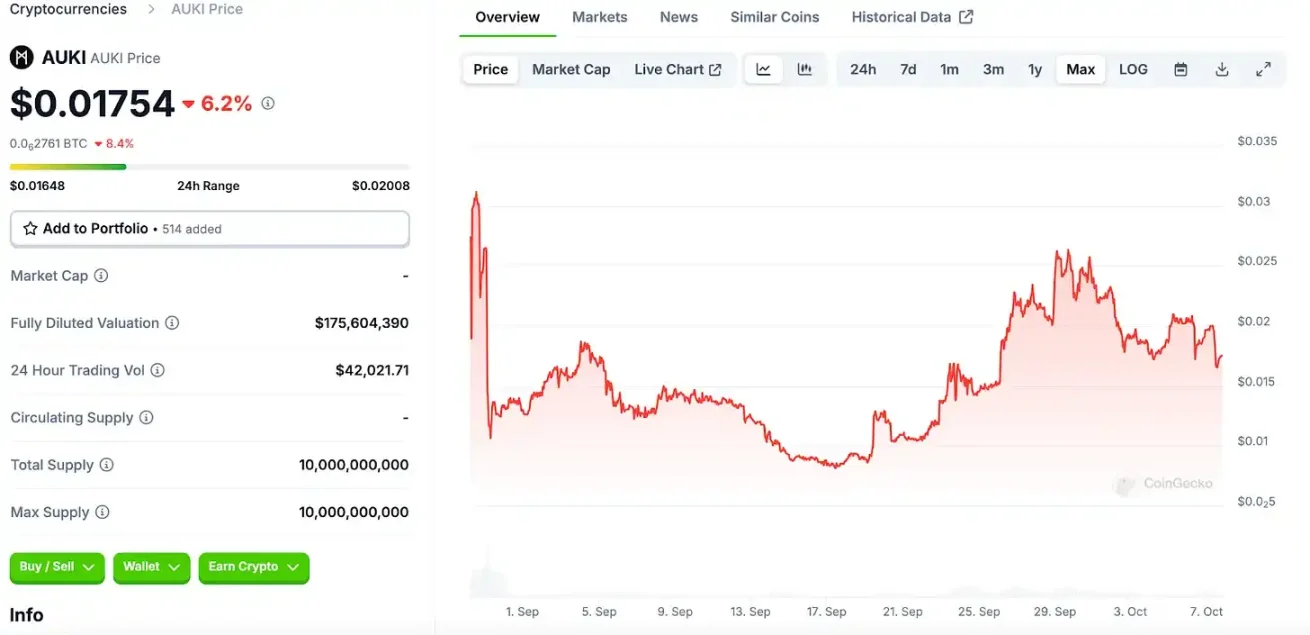

Let’s examine what Auki Labs did differently at token launch. The image above is a screenshot from CoinGecko. As you can see, Auki’s FDV and 24-hour trading volume are both relatively low. That’s because it listed first on a DEX, followed later by a CEX listing on MEXC. So far, Auki’s token price has increased 78% compared to the last private round.

For Auki’s founders, token listing was just another day. Their real focus remains building their product. Auki’s token debuted on August 28 on Uniswap V3 via the AUKI/ETH pair on Base, Coinbase’s Layer-2 solution. They then had their first CEX listing on MEXC on September 4. They estimate saving approximately $200,000 in listing fees through this approach.

Auki also adopted a fairer token vesting schedule. Team members and investors receive daily unlocks over periods ranging from one to four years.

Sour Grapes?

Some readers may suspect I'm merely bitter because I don’t own a mainstream CEX profiting from new token listings. That’s true—I earn income when tokens in my portfolio increase in value.

If the projects I back price their tokens too high, pay massive fees to list on exchanges, yet fail to outperform Bitcoin, Ethereum, and Solana, I have a duty to speak up. That’s my stance. I fully support CEXs listing Maelstrom’s projects—if they do so because of strong user growth and compelling products or services. But I want the projects we back to stop worrying about which CEX will accept them, and start focusing on their daily active user metrics.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News