Crypto CEXs Rush to Offer U.S. Stocks, Traditional Brokers Face Uninvited Competition

TechFlow Selected TechFlow Selected

Crypto CEXs Rush to Offer U.S. Stocks, Traditional Brokers Face Uninvited Competition

The great reshuffle has only just begun.

Author: momo, ChainCatcher

Selling U.S. equities has become the top priority for crypto CEXs.

On one hand, the spillover demand for U.S. equities is simply too enticing. Over the past few years, U.S. equities have remained persistently red-hot, and investors outside the U.S. have shown surging interest in star assets such as NVIDIA, as well as pre-IPO companies like SpaceX and OpenAI. Traditional brokers—constrained by regulatory uncertainty and high compliance costs—are ill-equipped to efficiently serve this global investor base. However, with the SEC’s approval of Nasdaq’s pilot program for tokenized stock trading, Wall Street’s tokenization experiments have opened the door for crypto CEXs to enter the U.S. equity market.

On the other hand, this surge also exposes crypto CEXs’ own traffic challenges. The hotter U.S. equities get, the colder the crypto market becomes—and there is no strong near-term catalyst capable of reversing this trend.

Yet the crypto industry has never been decided during tailwinds, but rather reshaped amid crises and inflection points. The worst of times often mark the best of times for crypto CEXs. The 2017–2018 SEC crackdown cleared out weaker players and cemented Binance’s dominance; today, U.S. equity offerings may be shaping up as the next watershed moment for crypto CEXs.

Looking at recent accelerated moves into U.S. equities, two main approaches have emerged: “direct integration with traditional brokers” and steadfast commitment to “tokenized U.S. equities.” This article uses Binance and Bitget as representative cases of these two paths, comparing them across more than a dozen granular dimensions to examine whether crypto CEXs’ latest foray into U.S. equities can erode traditional brokers’ market share.

I. Why Did Crypto CEXs’ Previous U.S. Equity Products Fail to Gain Traction?

Before diving into the comparison, let’s briefly address why, after most major exchanges launched U.S. equity products last year, CEXs are now collectively rolling out new ones.

The previous generation of U.S. equity products generally fell into two categories: (1) Contracts for Difference (CFDs), where users trade price movements without ever touching the underlying shares; and (2) integrations with RWA/tokenization platforms such as Ondo, packaging U.S. equity exposure as on-chain assets and listing them within exchange interfaces.

These solutions solved the “existence” problem—but not the “usability” problem.

CFDs function more like trading tools, suitable for short-term directional bets, yet remain far removed from actual equity ownership. Early tokenized equities, meanwhile, delivered numerous pain points in practice.

First and foremost, users were deeply concerned about whether the underlying assets truly represented real U.S. equities—and whether those equities offered genuine liquidity. In addition, user experience was riddled with issues. Gracy Chen, CEO of Bitget, highlighted several recurring pain points users reported with earlier-generation tokenized equity products. For example, large orders incurred excessive slippage, making the trading experience feel less like buying blue-chip stocks and more like trading illiquid on-chain assets; dividend processing lacked smoothness—for instance, when underlying stocks issued dividends, the corresponding distribution to token holders felt delayed or inconsistent; corporate actions such as stock splits and reverse splits led to confusing price and position mappings.

Another critical issue was capital efficiency. Early tokenized U.S. equities functioned largely as “tradable assets” only—once purchased, they sat idle in users’ accounts awaiting price movement. They could rarely serve as margin for derivatives or unified accounts, nor integrate into wealth management, lending, or other exchange-native financial ecosystems. For crypto-native users, this significantly undermined the composability and capital efficiency that tokenization was meant to deliver.

The latest CEX U.S. equity solutions are designed precisely to address these pain points. Binance and Bitget’s new initiatives exemplify the two distinct paths: the former leans toward direct broker integration and authentic equity trading; the latter seeks to unify real U.S. equity liquidity, tokenized mapping, and exchange-native ecosystems via Reality/rToken.

We’ll now compare the two models across the key dimensions where users have experienced friction.

II. Two New Paths into U.S. Equities: Direct Broker Integration vs. Tokenization-First

1. Underlying Product Architecture: What Does the User Actually Own?

Both Binance and Bitget’s latest offerings fundamentally resolve the core challenge of direct access to U.S. equity liquidity—and both rely on Alpaca as their underlying custodian infrastructure. Alpaca is a compliant U.S. equity brokerage infrastructure provider currently supporting other leading tokenization players, including Ondo Finance, Dinari, and xStocks.

Specifically, Binance adopts a “broker gateway” model: U.S. equity orders are handled by introducing broker Nest Trading, while back-end execution, clearing, and custody are managed by Alpaca.

Bitget pursues a “tokenization-first” model: users hold rTokens, but orders are executed directly against U.S. equity markets via Reality’s on-chain trading desk. Underlying shares are held in custody by Alpaca, while rTokens serve as 1:1 on-chain representations. Thus, rToken pricing and depth do not stem from internal platform matching but instead reflect real U.S. equity market liquidity.

Still, rTokens are not identical to holding shares directly in a traditional broker account—so what safeguards underpin their security? Bitget’s official response cites a three-layer protection framework: custody by licensed brokers, asset segregation, and real-time proof-of-reserves.

Regarding the Common Reporting Standard (CRS), Bitget’s rTokens currently fall outside CRS reporting at the traditional broker account level; Binance’s model, being closer to a broker relationship, may face greater future regulatory scrutiny.

In summary, both models resolve the question of “authenticity” of underlying U.S. equity assets. Binance functions more like a broker gateway; Bitget embeds authentic assets into the on-chain ecosystem, emphasizing on-chain attributes and capital efficiency.

2. Shareholder Rights & Economic Entitlements: Beyond Price Movement

For users, buying U.S. equities isn’t just about capturing price appreciation—it entails dividends, dividend taxes, stock splits, reverse splits, mergers & acquisitions, delistings, voting rights, and other corporate actions. The closer the product mirrors real equity ownership, the more rigorously these details must be addressed.

Public information indicates that neither Binance nor Bitget’s current offerings treat U.S. equities as mere price symbols. Instead, both are actively enhancing foundational economic entitlements tied to real U.S. equities.

Dividends, dividend taxes, stock splits, reverse splits, and other corporate actions all depend on infrastructure providers like Alpaca for execution. Hence, on these core entitlements, both models converge: whenever an underlying U.S. equity issues dividends or undergoes corporate actions, the platform must reflect the corresponding outcomes in users’ accounts.

The difference lies solely in implementation mechanics. Binance reflects adjustments directly within users’ U.S. equity accounts; Bitget maps them onto the token side via Reality/rToken—stock dividends are distributed 1:1 in real time as tokens, while cash dividends are automatically converted to USDT and credited instantly.

Voting rights aren’t a primary differentiator. Whether operating under a broker gateway or rToken model, non-U.S. users with fractional holdings and platform-held structures typically do not exercise direct shareholder voting rights—and voting rights are not a central selling point of such products.

The advantage of Bitget’s tokenization approach is that it replicates all entitlements achievable through direct broker integration—and further transforms those entitlements into highly efficient, composable assets once integrated into the CEX environment.

3. Trading Experience & Capital Efficiency

Next, consider overall trading experience and asset efficiency.

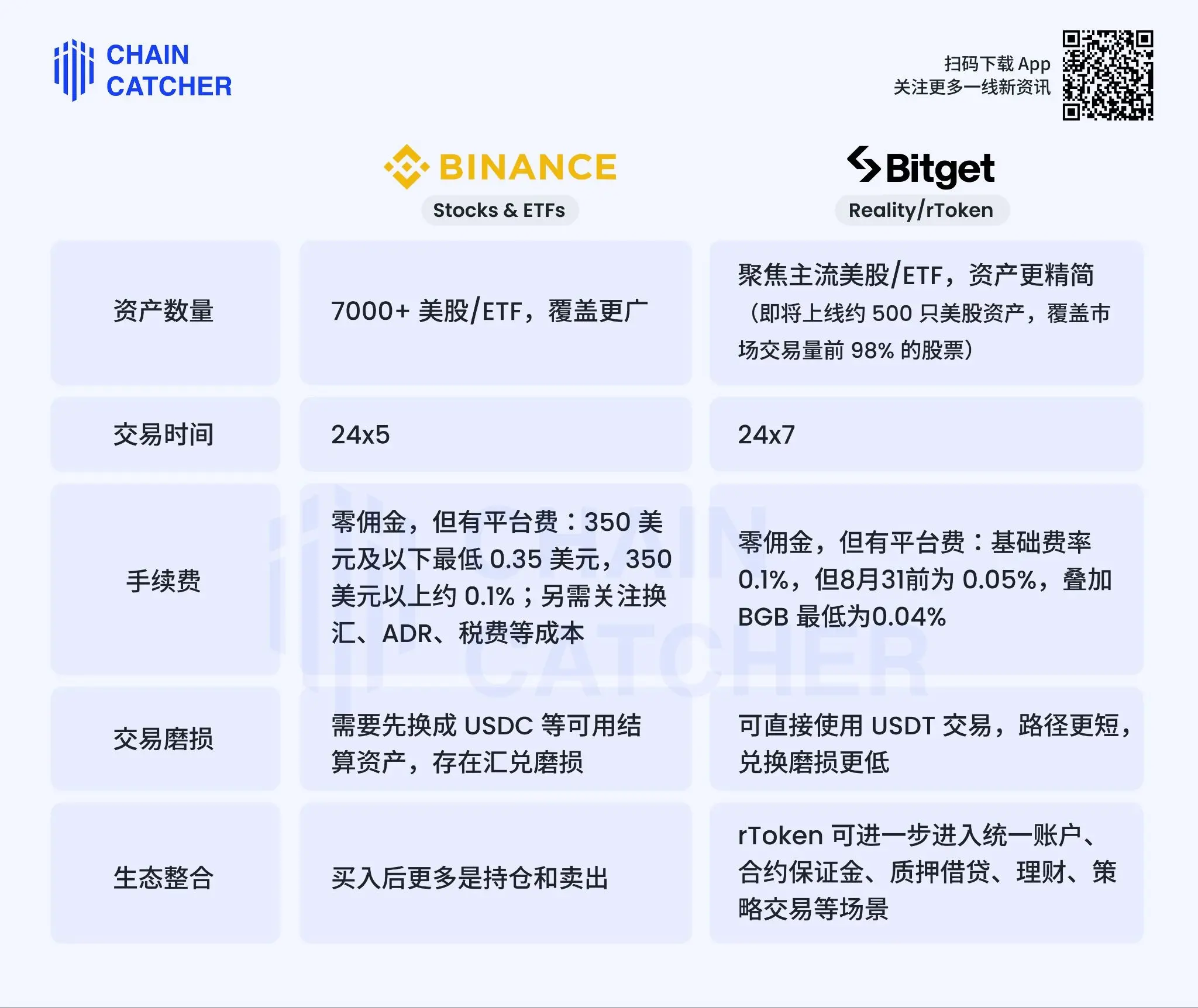

In terms of asset coverage, Binance offers broader selection; Bitget focuses on mainstream equities—planning to list ~500 stocks representing 98% of total U.S. equity trading volume—emphasizing curation and liquidity coverage.

Regarding trading hours, Binance broadly aligns with traditional U.S. equity market hours; Bitget enables 7×24 trading via tokenization—better aligned with crypto-native user expectations.

Some may ask: Where does liquidity come from when U.S. markets are closed? Bitget’s CEO responded on X (formerly Twitter) that third-party market makers supply liquidity by holding physical inventory to meet buy/sell demand. This implies liquidity outside regular U.S. equity hours is finite: weekend or extreme-market unilateral buy orders may inflate prices, causing significant volatility upon Monday’s market open.

On fees, Bitget currently offers comparatively lower rates. Both charge zero commissions, but Bitget applies a platform fee: base rate is 0.1%, reduced to 0.05% until August 31, and further lowered to 0.04% when paid in BGB—making it especially attractive for high-frequency traders.

On transaction friction, Binance settles trades in USDC (and others), requiring users holding USDT to perform extra conversions; Bitget accepts USDT directly—shortening the path.

The most pronounced difference lies in ecosystem integration. Binance’s U.S. equity offering remains isolated from its broader ecosystem; Bitget’s rTokens plug directly into its unified account system, enabling use as futures margin, staking collateral, and more—boosting capital efficiency. Currently, rTokens for 15 equities—including NVIDIA and Micron—are supported as futures margin.

Finally, let’s summarize the relative strengths and weaknesses of each path.

Binance’s direct-broker-integration model excels in delivering an experience closely mirroring traditional U.S. equity trading: underlying assets are real, liquidity flows from authentic U.S. markets, and coverage is extensive—enhancing trust for users unfamiliar with crypto trading. Its limitation, however, lies in simplicity: it fails to unlock users’ full capital efficiency potential.

Bitget’s tokenization model preserves the core advantages of direct broker integration—namely, liquidity and dividend distribution—while adding higher capital efficiency: enabling 7×24 trading, allowing tokenized equities to serve as margin and fuel diverse trading strategies, and offering lower fees. Yet for more risk-averse users, holding physical shares may still feel safer than holding tokens. That said, as Bitget continues refining this tokenized U.S. equity experience, user concerns are expected to gradually diminish.

III. Can Crypto Exchanges Eat Into Traditional Brokers’ Market Share?

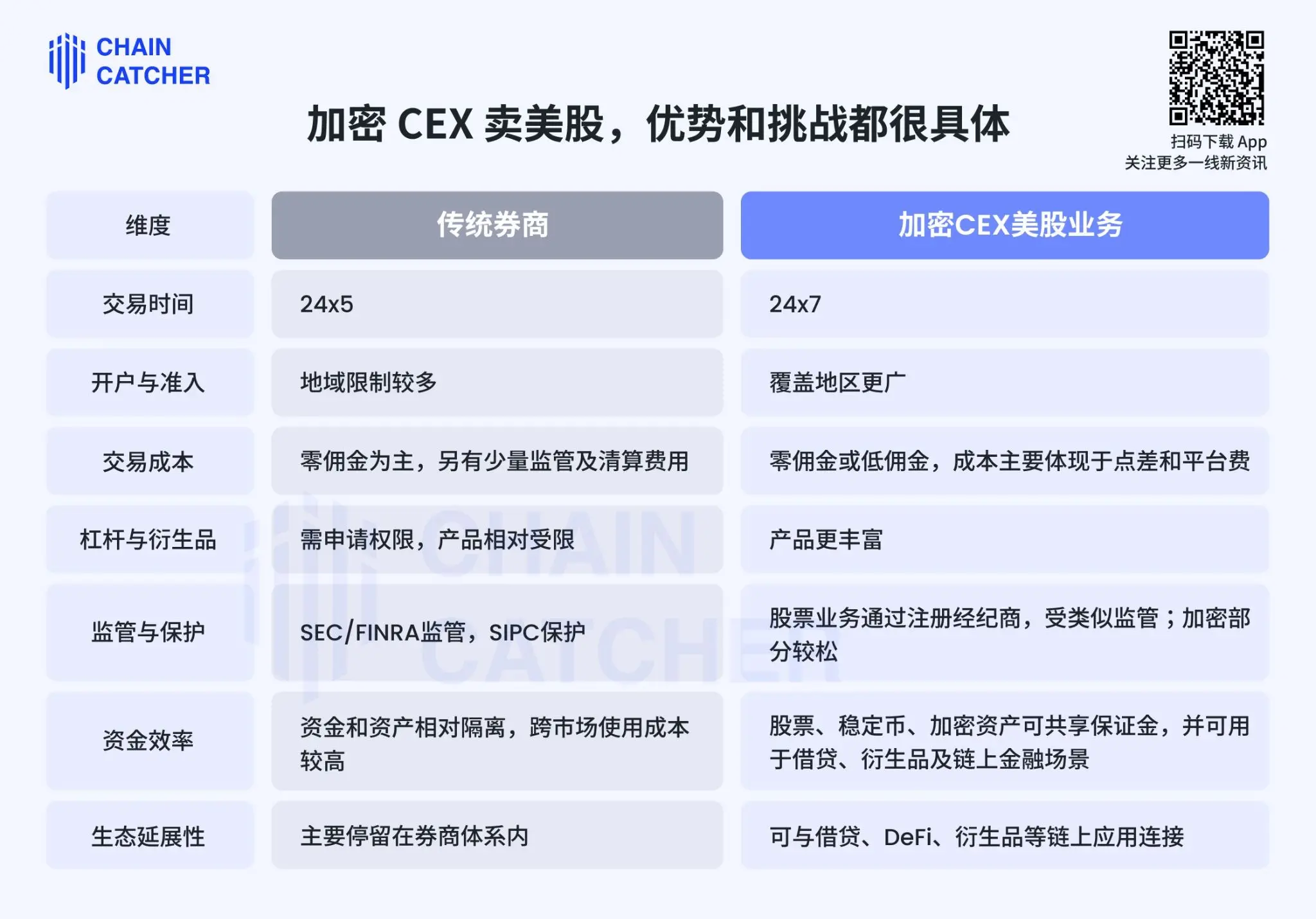

U.S. equity trading has never been merely a contest among crypto CEXs. Long term, crypto CEXs must ultimately compete head-to-head with traditional brokers.

1. Concrete Advantages—and Concrete Challenges—of Crypto CEXs Selling U.S. Equities

Across several key dimensions, crypto CEXs hold clear advantages over traditional brokers: First, trading hours—crypto CEXs achieve 24/7 availability via tokenization, better meeting investor demand. Second, onboarding and accessibility—traditional brokers face geographic restrictions, whereas crypto CEXs operate globally.

But the most fundamental advantage lies in capital efficiency and ecosystem extensibility. In traditional broker accounts, equity capital remains siloed from other assets, making cross-market usage costly; crypto CEXs allow equities, stablecoins, and crypto assets to share margin and participate in lending, derivatives, and on-chain finance. This is likely why Bitget insists on the tokenization path—to bring U.S. equities on-chain as 7×24 tradable, pledgeable, and reusable assets—the clearest current differentiator from traditional brokers.

Of course, the challenges are equally concrete. The closer a product gets to real equity markets, the more users expect it to meet traditional financial standards. Platforms must prove underlying shares exist, demonstrate transparent custody and reserves, and flawlessly handle dividends, splits, taxation, and liquidity. Tokenized products face particular scrutiny: during off-hours or extreme market conditions, price stability and liquidity adequacy directly determine user trust.

2. The Endgame May Not Be Substitution—But Convergence Toward the Universal Exchange

Currently, the dominant trend is convergence between traditional and crypto finance.

On one side, crypto CEXs are moving beyond simple crypto-to-crypto trading. Binance has already integrated directly with brokers for U.S. equities; Bitget explicitly champions the Universal Exchange (UEX) vision—aiming to unify equities, gold, forex, and crypto assets under a single account. On the other side, traditional platforms are embracing tokenization: Robinhood has launched tokenized stocks, and the NYSE is advancing 24/7 tokenized equity trading.

This signals that U.S. equity tokenization isn’t just a product-level competition—it’s a transformation in financial account architecture. Boundaries between broker accounts, crypto accounts, and bank accounts will continue blurring.

In the short term, whether CEXs can erode traditional brokers’ market share hinges on product experience and regulatory boundaries; in the long term, the real competition is about who first evolves into a higher-efficiency multi-asset financial platform.

That’s why crypto CEXs’ U.S. equity strategy merits close attention. As Bitget CEO Gracy Chen put it: this isn’t merely adding another trading pair—it’s leveraging blockchain technology to integrate traditional assets into the crypto ecosystem, empowering crypto CEXs to ascend to broader financial platforms and begin competing with traditional institutions for pricing power over global mainstream assets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News