PayFi Revolution: 5 Top Web3 Payment Projects That Will Disrupt Traditional Finance

TechFlow Selected TechFlow Selected

PayFi Revolution: 5 Top Web3 Payment Projects That Will Disrupt Traditional Finance

One major advantage of Web3 is enabling secure, low-cost, and nearly instantaneous global transactions.

Author: dpycm.eth

Translation: TechFlow

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The views expressed in this article are solely those of the author and should not be taken as investment advice, recommendations, or a basis for investment decisions.

Over the past decade, cryptocurrencies have experienced rapid development, evolving from niche technological experiments into mainstream financial tools. Web3 payment systems, built on blockchain technology, ensure transparency, security, and immutability in transactions. These systems are increasingly being integrated into e-commerce platforms, point-of-sale systems, and peer-to-peer payment applications, making cryptocurrency usage more convenient in daily life.

As of 2023, the Web3 payments market was valued at $1.2 billion and is projected to grow at a compound annual growth rate (CAGR) of over 15% from 2024 to 2032. Web3 payments are poised to become a key pillar of the digital economy—just like traditional payment systems—bringing new opportunities and challenges to the global financial ecosystem.

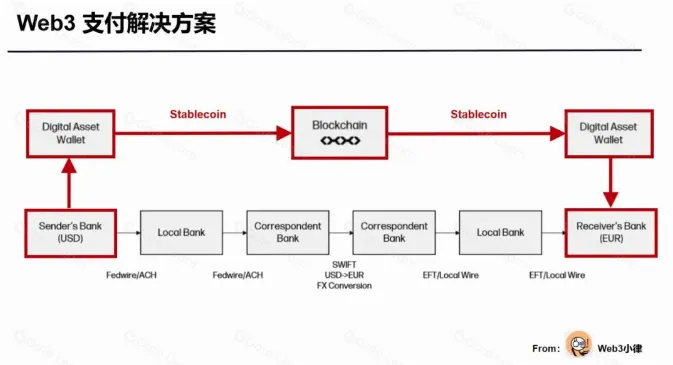

Current Web3 Payment Infrastructure

Web3 Payment Infrastructure

Existing Web3 payment infrastructure has greatly simplified traditional payment processes. Typically, a payment transaction involves just three parties: the payer, the payee, and the blockchain (as the intermediary). Since the blockchain itself is non-sentient, effectively only two active participants are required, giving such transactions advantages in speed and cost. All Web3 payment protocols operate on the same foundational infrastructure, though implementations may vary slightly depending on each protocol's on-off ramping requirements.

Sphere Pay and Loopcrypto.xyz are two unique payment infrastructure protocols that enable businesses to integrate Web3 payment capabilities—features we will explore in detail later.

What is PayFi?

As payments converge with decentralized finance (DeFi), PayFi has emerged—a financial market centered around the time value of money. PayFi offers a way to meet present needs using future funds, something traditional finance cannot easily achieve.

PayFi encompasses various forms of payment:

-

Payment tokens, such as tokens representing the time value of tokenized U.S. Treasuries or yield-generating stablecoins;

-

Financing real-world assets (RWAs) through DeFi lending, enabling on-chain yields in real-world payment scenarios;

-

New Web3 payment systems seamlessly integrated with DeFi protocols;

-

Moving traditional payment logic onto blockchains to build a comprehensive Web3 payment framework.

A prime example of PayFi is Ondo Finance. This protocol aims to democratize access to institutional-grade financial products by tokenizing U.S. Treasuries. Ondo brings low-risk, yield-bearing, and scalable financial instruments—such as U.S. Treasuries and money market funds—onto the blockchain, allowing stablecoin holders to earn returns on their assets.

Ondo Finance offers two products: OUSG and USDY. OUSG is a tokenized U.S. Treasury fund, while USDY is a yield-bearing stablecoin backed by short-term U.S. Treasuries. As of August 23, 2024, the total value locked (TVL) in these two products reached $556 million.

With USDY, holders can maintain dollar-denominated exposure while earning yield. Thus, Ondo adds tangible utility to payment tokens, further advancing PayFi within Web3.

Innovative Payment Developments

This section highlights some interesting or lesser-known innovations in the payments space, excluding crypto cards and on-off ramping features.

Karrier One (Payments x DePIN)

The convergence of payments and DePIN finds strong application in telecom networks. Karrier One is an operator-grade decentralized network integrating both payment and DePIN functionalities. The Karrier One network consists of three modules: telecommunications, blockchain, and the Karrier Number System (KNS). By partnering with global telecom providers, it delivers seamless worldwide communication coverage. The network is governed by the Karrier DAO, where token holders participate in governance decisions.

Through KNS, users receive a Web3 wallet directly linked to their phone number. This integration enables users to engage in DeFi activities, send and receive cryptocurrencies, and enjoy smooth payment experiences—effectively combining PayFi and DePIN. With 7.1 billion mobile phone users globally, there’s immense potential for the growth of Web3 telecom networks.

Huma Finance

Huma Finance is an income-based lending protocol. It allows borrowers to secure loans by pledging future income, matched with global on-chain investors. The protocol includes standard credit facilities, along with decentralized signal processors and evaluation agents—critical infrastructure for integrating income sources, conducting credit assessments, and managing ongoing risk.

As of August 23, 2024, Huma has facilitated nearly $900 million in loans, with $883 million successfully repaid and a current default rate of 0%.

Sphere Pay

Sphere is a payment API designed specifically for digital currencies. By offering an all-in-one payment experience, Sphere connects everyday users with stablecoins, accelerating the adoption of Web3 payment systems.

Sphere provides merchants with customizable or pre-built front-ends and user experiences, enabling flexible use of Sphere Pay. Additionally, it offers multiple pricing models to suit varying merchant needs. Sphere charges no software fees; instead, it takes a flat 0.3% fee per transaction, making the software free to use for all. This makes Sphere an ideal choice for small businesses, especially those with low transaction volumes or limited startup capital.

Loopcrypto.xyz

Loop is a Web3 payment infrastructure that helps companies schedule or automate collections and payments. Through automated payments, Loop improves operational efficiency and reduces customer churn. The platform supports all ERC-20 tokens and allows settlement in either cryptocurrency or fiat, reducing complexity in fund conversion for businesses.

Loop offers plug-and-play software, minimizing implementation friction. It also integrates with top-tier platforms like Stripe, Zapier, and Xero, enabling business owners to seamlessly incorporate Loop into existing financial management systems. As a result, companies using traditional invoicing systems can easily add cryptocurrency as an additional payment option for customers without major system overhauls.

Orbita

Orbita is a decentralized Layer 1 payment protocol built on Cosmos, currently under development with no testnet yet launched. As the team may still be finalizing documentation and whitepapers, these materials are not publicly available.

Orbita’s core features will include irreversible direct payments, reversible payments, decentralized subscriptions, and e-commerce integration. As a Layer 1 protocol focused exclusively on payments, this represents a novel direction in the payments industry and could bring about intriguing changes.

Market Data & Updates

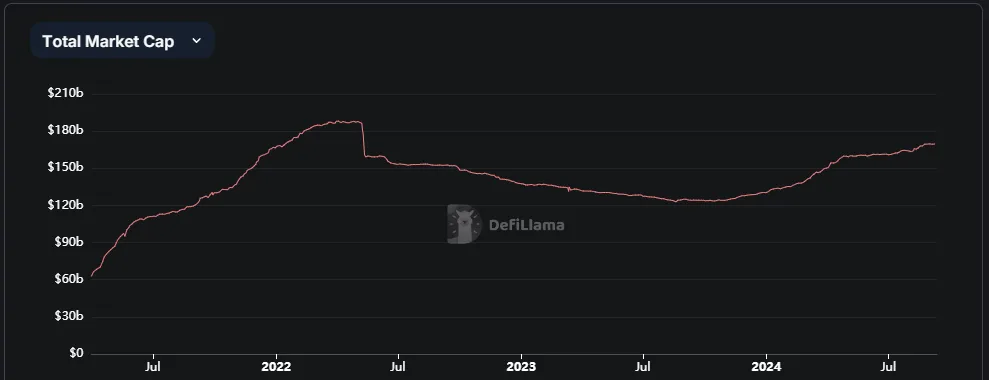

Total Market Cap of Stablecoins

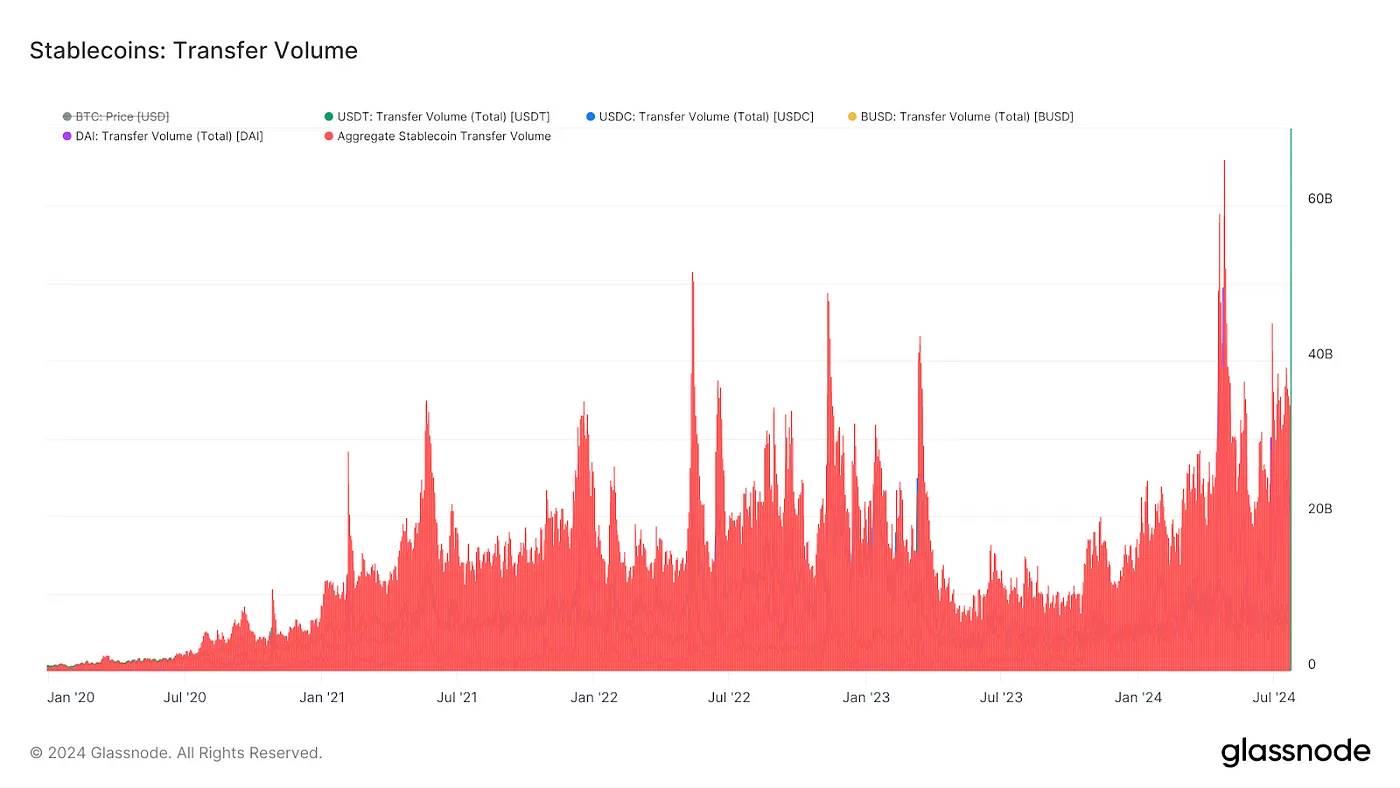

Stablecoins: Transfer Volume

Alongside the cryptocurrency boom of the past decade, stablecoins have also grown rapidly. The total market cap of stablecoins surged from $20 million in 2017 to $170 billion in 2024. By 2024, stablecoin transfer volume peaked at 60 billion. As transfer volume continues to rise, the use of stablecoins in payments and other applications becomes increasingly common. With wider acceptance of stablecoins, demand for robust payment systems will grow accordingly.

Major stablecoin issuers are actively expanding their markets. Tether recently announced plans to launch a UAE dirham-backed stablecoin fully supported by local reserves, aiming to become the preferred digital payment token in the UAE. Circle CEO Jeremy Allaire stated they plan to develop a tap-to-pay USDC feature for iPhones—an initiative made possible after Apple opened its secure payment chip to third-party developers. This would make paying with USDC as simple and seamless as using traditional banks or credit cards.

Since entering the stablecoin market in August 2023, PayPal has aggressively promoted PYUSD. Roughly one year after launch, PYUSD has risen to become the sixth-largest stablecoin, surpassing established tokens like FRAX and BUSD. PayPal’s expansion on Solana and incentive programs with Kamino have also proven highly attractive. Furthermore, PayPal’s recent collaboration with Anchorage Digital to offer rewards for institutions holding PYUSD has further drawn capital inflows.

Reflections: The Impact of Web3 Payments

One major advantage of Web3 is its ability to enable secure, low-cost, and near-instant global transactions. While the Web3 industry is still in its early stages, institutions, enterprises, and individuals are already beginning to use blockchains for payments.

However, how will banks react if Web3 payments go mainstream and cut into their intermediary fees? We’re already seeing banks build private blockchains to compete, but even then, their revenue would likely remain far below current fee levels. Resistance is inevitable, and widespread retail adoption may still take time. Clearly, the opacity and centralization of private blockchains will perpetuate traditional banking characteristics.

Moreover, Web3 payments hold particular advantages in global transactions—especially imports and exports—but have limited impact on the average local consumer. If paying with cryptocurrency at my local grocery store feels no different than using a traditional bank card, why would I choose crypto? Self-custody appeal? For most people, such marginal benefits aren’t compelling enough. Therefore, switching costs may hinder mainstream user adoption in the short term.

I believe that as Web3 and the payments market evolve, the stablecoin market will continue growing over the next decade. Innovations like Karrier One’s telecom network and Huma Finance’s future-income financing will undoubtedly inspire further breakthroughs and drive broader adoption. With favorable regulatory developments acting as catalysts, the flourishing of Web3 payments seems inevitable. In fact, as we’ve seen in recent years, the market may continue growing regardless of regulatory clarity. I remain optimistic and look forward to a future where Web3 payments are simply the default—no longer questioned or doubted.

What does your vision of Web3’s future look like?

Hope you enjoyed this article,

Best regards!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News