Nvidia plunged 9.5%, erasing $278.9 billion in market value—the largest single-day decline in U.S. stock market history. What happened?

TechFlow Selected TechFlow Selected

Nvidia plunged 9.5%, erasing $278.9 billion in market value—the largest single-day decline in U.S. stock market history. What happened?

Some analysts say Nvidia is "working through the growing pains," with a still-bright future ahead, while others argue that Nvidia's earnings report has caused the market to question the sustainability of massive investments in AI hardware.

Author: Du Yu, Wall Street Insights

On Tuesday, September 3, the first trading day of September after a long U.S. market weekend, “brutal” was an apt descriptor for Wall Street’s performance, while “plunge” could easily be attributed to Nvidia and its fellow chip stocks leading the decline.

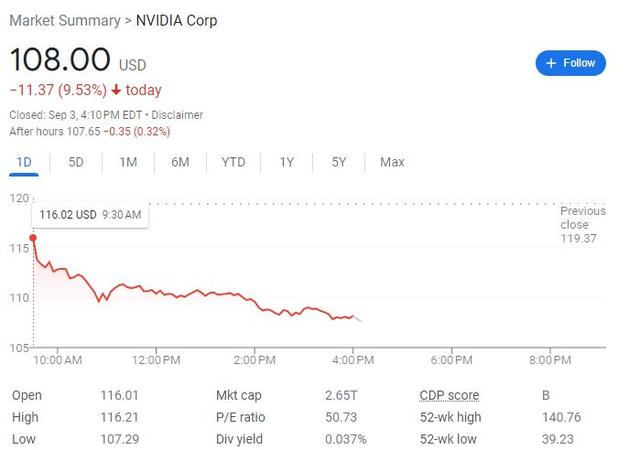

Nvidia opened with a 2.8% gap down and continued lower throughout the session, closing down 9.5%, pushing its share price toward $108—the lowest since August 9—and wiping out $279 billion in market value. Its market cap moved further away from the $3 trillion mark, while the two-times leveraged long ETF on Nvidia fell approximately 19%.

The benchmark Philadelphia Semiconductor Index plunged 7.8%, breaking through key support levels from 5100 down to 4800, hitting its lowest point since August 12. The index-tracking ETF SMH dropped 7.5%, marking its largest single-day decline in over four years.

Other semiconductor stocks also suffered. Intel, Nvidia's direct competitor, fell nearly 9%, retreating from a one-month high; AMD declined almost 8% to a three-week low. TSMC, the world’s largest chip foundry, saw its U.S.-listed shares drop 6.5%, while GlobalFoundries, another major wafer foundry, slid 8.6%. Chip equipment makers KLA Corp lost 9.5%, Applied Materials fell 7%, and ASML dropped 6.5%. Qualcomm declined 6.9%, Broadcom—set to report Q3 earnings Thursday—fell over 6%, and Micron Technology dropped about 8%. Even ARM, which had risen during Nvidia’s prior selloff last Thursday, sank nearly 7%.

Reason One Behind the Chip Stock Plunge: Weak Manufacturing Data and Pre-Employment Report Market-Wide Selloff

Market analysts noted that the sharp decline in chip stocks followed broader weakness across U.S. equities.

All major U.S. indexes posted their largest drops since August 5, when weak July nonfarm payrolls sparked fears of economic recession. This week, two August manufacturing reports remained firmly in contraction territory, reigniting investor concerns about a slowing U.S. economy and triggering broad equity selling.

The tech-heavy Nasdaq-100 Index extended losses to 3%, dragging the Nasdaq Composite below 3% into its lowest level since August 12. The S&P 500 fell more than 2%, reaching its weakest point since August 14. The blue-chip Dow Jones Industrial Average dropped 1.5%, or over 620 points, falling below 41,000 to its lowest since August 22. The CBOE Volatility Index (VIX), known as the "fear gauge," briefly surged over 40% toward 22.

Jordan Klein, strategist at Mizuho Securities, said investors may want to reduce exposure to semiconductor stocks amid rising risks of an economic “hard landing.”

According to Barron’s citing Dow Jones Market Data, the so-called “Magnificent Seven” tech giants briefly fell 7.6% during Tuesday’s session—their worst percentage drop since April 19:

“This sell-off appears part of sector rotation rather than being driven by specific news within the chip industry. September is typically a tough month for equities, and investors seem eager to lighten positions ahead of a series of upcoming economic data releases.”

Secondly, Nvidia has been under continuous pressure since its post-market earnings release last Wednesday, reflecting growing concerns over its lofty valuation, slowing revenue growth guidance, and doubts about the sustainability of the AI chip investment frenzy—dragging down both chipmakers and AI-related stocks.

Bill Blain, founder and senior strategist at Wind Shift Capital, said Nvidia’s slide is sending a strong “sell” signal to U.S. stock investors. He added that its past massive gains and sky-high valuation might indicate the peak of a 40-year market cycle:

“I’ve just found the best reason to sell Nvidia—confirmation we’re at the top of the market. What comes next? With nations competing for strategic resources, the next two decades will likely see rising inflation, higher interest rates, and a global commodities supercycle that crushes equity markets.”

Reason Two Behind the Chip Stock Plunge: Weak Chip Sales Data Dampens Industry Outlook

Another factor exacerbating the selloff in semiconductor stocks was weaker-than-expected chip sales data released the same day by the Semiconductor Industry Association (SIA), signaling underlying industry weakness.

UBS analyst Timothy Arcuri noted that June-July chip sales declined 11.1%, underperforming both five-year and ten-year historical averages.

Arcuri pointed out:

“Memory chips were the main drag, but key segments including MCUs (microcontrollers), DSPs (digital signal processors), and analog chips all performed worse than seasonal trends over the past five and ten years.”

Morgan Stanley commented that the report showed “nearly every product line weaker than our expectations,” adding:

“The overall market still looks weak. While we believe sales in analog chips, discrete devices, and MCUs may have bottomed in Q2, any recovery ahead appears limited in scope.”

Why Nvidia Dragged Down Chip Stocks: Earnings Report Fuels Doubts Over Sustainability of Massive AI Hardware Spending

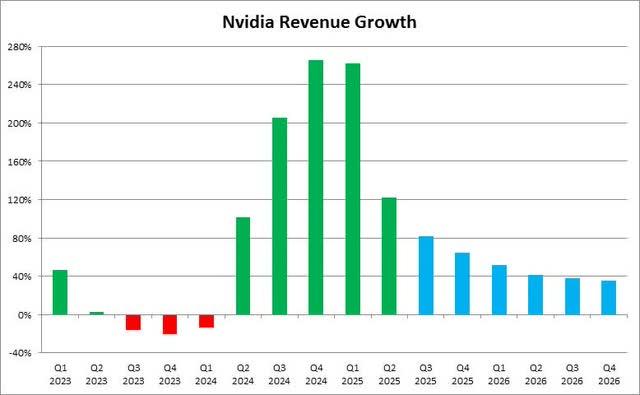

On one hand, despite achieving solid results in its fiscal Q2 ending July 2024—including doubling both revenue and EPS compared to a high base a year earlier, with record-breaking top-line growth—Nvidia guided next quarter’s revenue at $32.5 billion.

This implies year-over-year growth will slow sharply from consecutive quarters of triple-digit percentages to around 80%, interpreted by some as a sign of cooling demand for its AI chips. Following the report, suppliers providing memory and other components to Nvidia saw their shares fall.

Over the past year, chip stocks led by Nvidia have significantly outperformed due to optimism that the rise of artificial intelligence would drive companies to purchase more semiconductors and memory to meet surging computational demands.

However, Paul Nolte, market strategist and senior wealth manager at Murphy & Sylvest Wealth Management, noted it’s not surprising that “market darlings” like Nvidia and popular AI stocks are taking a breather, given that “the return on all this spending remains a big question.” The chip stock decline reflects skepticism about whether massive investments in AI computing hardware can be sustained:

“Revenue for Nvidia and other chipmakers has surged thanks to heavy spending by companies like Microsoft and Alphabet. But these buyers have seen relatively modest revenue growth from their AI investments, raising questions about how long this trend can continue.”

This makes Broadcom’s after-hours earnings report on Thursday particularly important, offering insight into whether enthusiasm for the AI trend is waning.

Why Did Nvidia Keep Falling Despite Solid Earnings? Analysts Say It’s ‘Digesting Growth Pains’

For Nvidia itself, shares have fallen nearly 14% since its earnings announcement on August 28—less than a week ago—mainly because although its financials were solid, they were “not spectacular,” especially relative to the sky-high expectations set by Wall Street.

Ken Mahoney, CEO of asset management firm Mahoney Asset Management, said the “angry reaction” to Nvidia’s earnings reflects investor habituation to the company not only beating expectations but utterly exceeding them—having witnessed its stock surge over 700% since early 2023. As a result, Nvidia shares are now “priced for perfection,” leaving little room for error.

Bill Maurer, a columnist at Seeking Alpha, said Nvidia’s post-earnings decline reflects it “digesting some growth pains.” With its stock having doubled over the past year, investor and analyst expectations became excessively high, making even solid beats on revenue and profit appear underwhelming—the smallest margin of beat in five quarters—highlighting the immense challenge of meeting ever-rising forecasts.

Moreover, Nvidia’s current share price sits far above its 200-day moving average—“quite expensive from a long-term perspective”—and combined with potential “buy the rumor, sell the fact” dynamics following the expected Fed rate cut in September, creates headwinds for such a highly valued stock:

“One key metric investors and analysts will focus on in coming quarters is gross margin. Non-GAAP gross margin declined over 3 percentage points sequentially in Q2, and further declines are expected in the second half of the fiscal year. Current margins are pressured by the ramp-up costs of Blackwell production.

Looking ahead, Nvidia’s overall revenue growth will begin to moderate slightly, as each subsequent quarter faces increasingly difficult year-over-year comparisons. Maintaining 100% or higher revenue growth over the long term is extremely challenging.

Whether Nvidia meets future targets hinges on the production ramp of Blackwell, whose mass production has been delayed by a quarter—to start in fiscal Q4 this year and extend into fiscal 2026.

During the earnings call, management projected Blackwell will generate “billions of dollars” in revenue in Q4, with substantial growth expected next year. However, analysts received less detailed information than hoped, which may have contributed to downward pressure on the stock.”

Mainstream Analysts Still Bullish on Nvidia’s Long-Term Outlook; Musk Hints at Continued Large-Scale AI Chip Purchases

Despite recent share price weakness, most analysts maintain “buy” ratings on Nvidia, with target prices implying meaningful upside. The majority remain confident in Nvidia’s “strong long-term prospects.”

For example, Tesla CEO Elon Musk recently emphasized that despite investor jitters, demand for Nvidia’s existing product lineup remains robust. His AI startup xAI successfully launched the Colossus AI training infrastructure in just 122 days, powered by 100,000 Nvidia H100 GPUs, positioning it to become “the world’s most powerful AI training system.” Future integration of Nvidia’s H200 chips will enable the system to double in scale within months.

The Motley Fool argued that sellers may be overlooking the fact that beyond data centers, every one of Nvidia’s business lines posted year-over-year growth—even its previously struggling gaming division. In contrast, AMD’s gaming chip sales plummeted nearly 60% year-on-year in Q2, underscoring Nvidia’s ability to maintain strong demand even in markets where rivals falter:

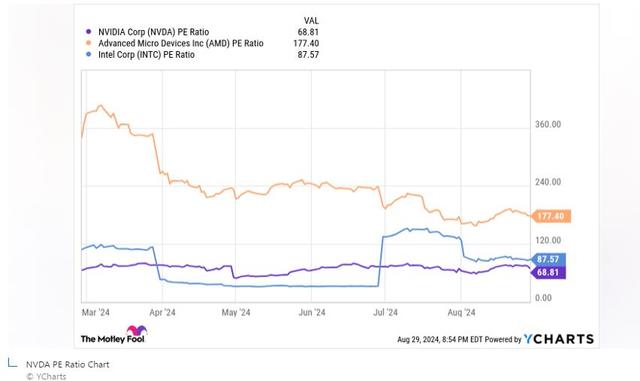

“Additionally, based on price-to-earnings (P/E) ratios, Nvidia doesn’t appear overly expensive compared to key competitors AMD and Intel.

The strength demonstrated in its earnings report reinforces confidence that Nvidia will capture between 70% and 95% of the AI GPU market. With the AI industry expected to grow from $136 billion last year to $826 billion by 2030, long-term investors stand to benefit from years of sector expansion and returns from holding Nvidia shares.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News