Is Karak, the new restaking contender, a vampire attack on EigenLayer?

TechFlow Selected TechFlow Selected

Is Karak, the new restaking contender, a vampire attack on EigenLayer?

Karak Network challenges dominance, leading the restaking赛道 with multi-asset support and unique technical features.

Author: Viee, Core Contributor at Biteye

Editor: Crush, Core Contributor at Biteye

Karak, a fast-moving and newly emerged player, went from announcing a $1 billion valuation funding round to launching an early access staking program, and now supporting various assets—all within about two months.

What is Karak, the rising newcomer in restaking, and how much disruption can it bring to the restaking space? How can one participate early in Karak to maximize chances of an airdrop? This report by Biteye dives deep into Karak Network.

01 The Emergence of Karak, Valued at $1 Billion

Karak Network is a restaking network, similar to EigenLayer and other restaking projects. It also uses a points-based model to incentivize users to restake, enabling them to earn multiple rewards.

In December 2023, Karak announced a $48 million Series A funding round led by Lightspeed Venture Partners, with participation from Mubadala Capital, Coinbase, and others. Mubadala Capital is the second-largest fund in Abu Dhabi. This round valued Karak at over $1 billion.

(Figure: Karak Series A Funding Details)

In February 2024, Karak launched its early access program, allowing users to restake on Karak to earn XP points. In addition to rewards from partner projects, participants can also earn Karak XP. These points are distributed via the protocol and may eventually be converted into tokens through an airdrop.

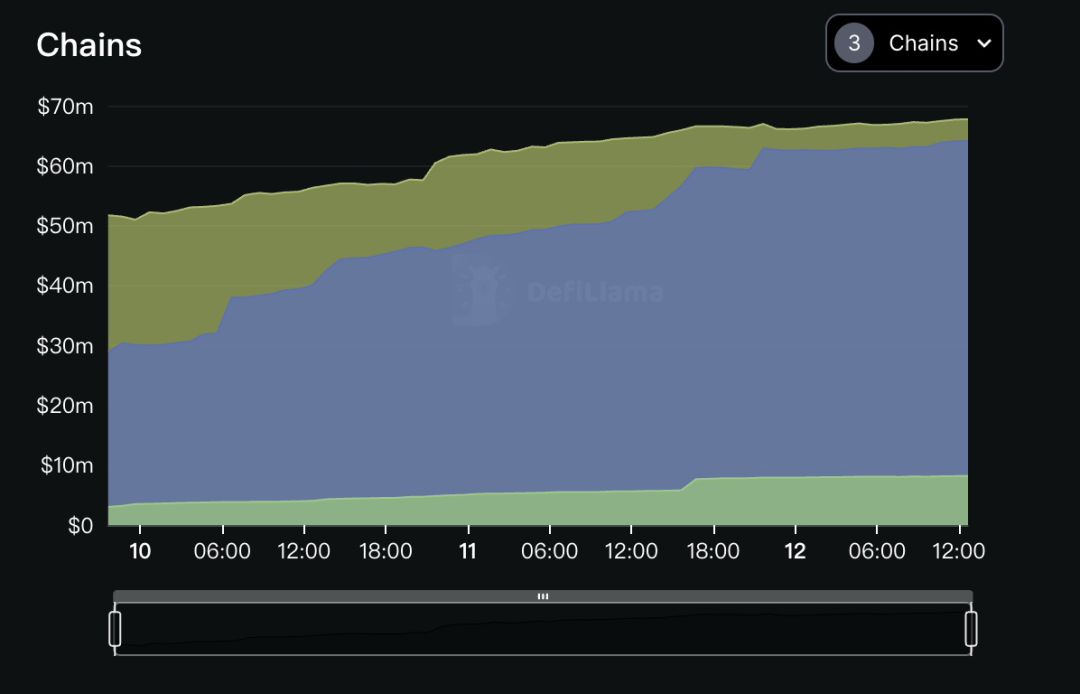

Private access opened on April 8, 2024. As of April 12, the total TVL across different chains supported by Karak reached $140 million, with Karak Network accounting for the largest share at 48.5%, followed by Ethereum at 45.7% and Arbitrum at 5.8%.

(Figure: Karak TVL Across Chains, https://defillama.com/protocol/karak#tvl-charts)

Karak’s emergence has drawn significant market attention. Although its total TVL is still far behind EigenLayer, it brings unique technical innovations that could challenge EigenLayer’s dominance in the restaking sector.

02 Karak's Technical Approach

2.1 Karak Network: A Restaking Layer with Multi-Chain Support Advantage

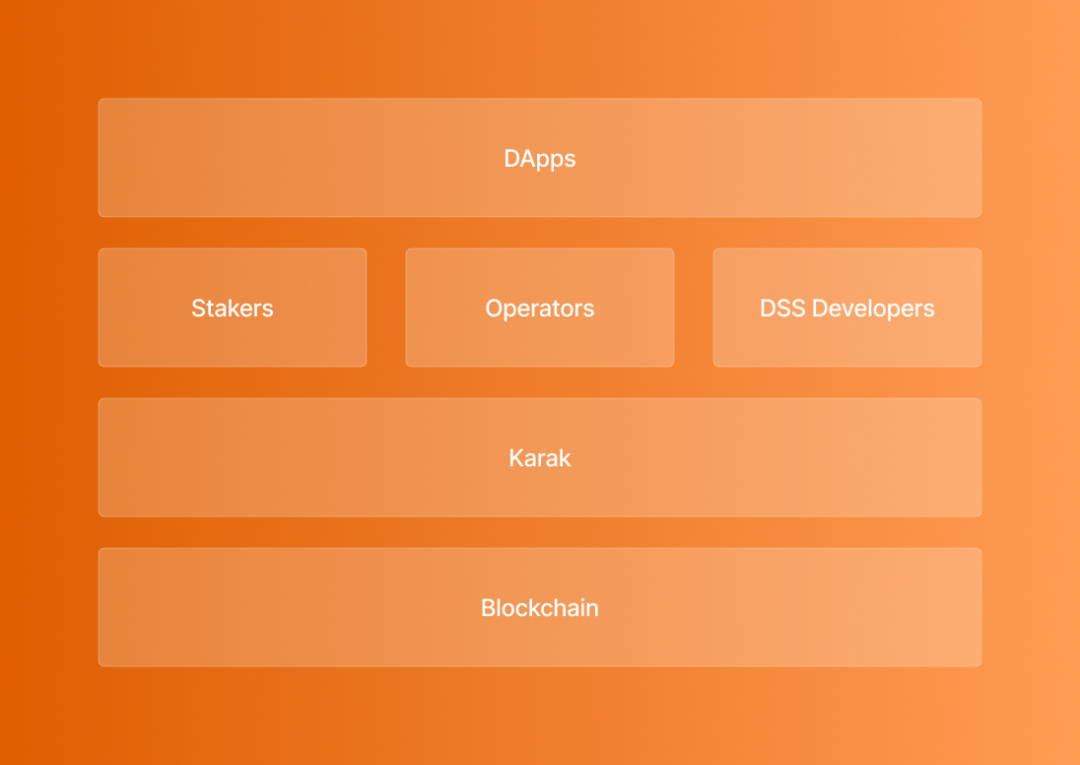

As a restaking platform, Karak differs from EigenLayer, which focuses solely on Ethereum. Karak provides a diversified platform supporting multiple assets—including ETH, Solana, and various Layer 2 tokens—enabling it to deliver security solutions across multiple blockchain ecosystems, offering greater diversity and inclusivity. Currently, Karak supports networks such as Ethereum mainnet, Karak, and Arbitrum.

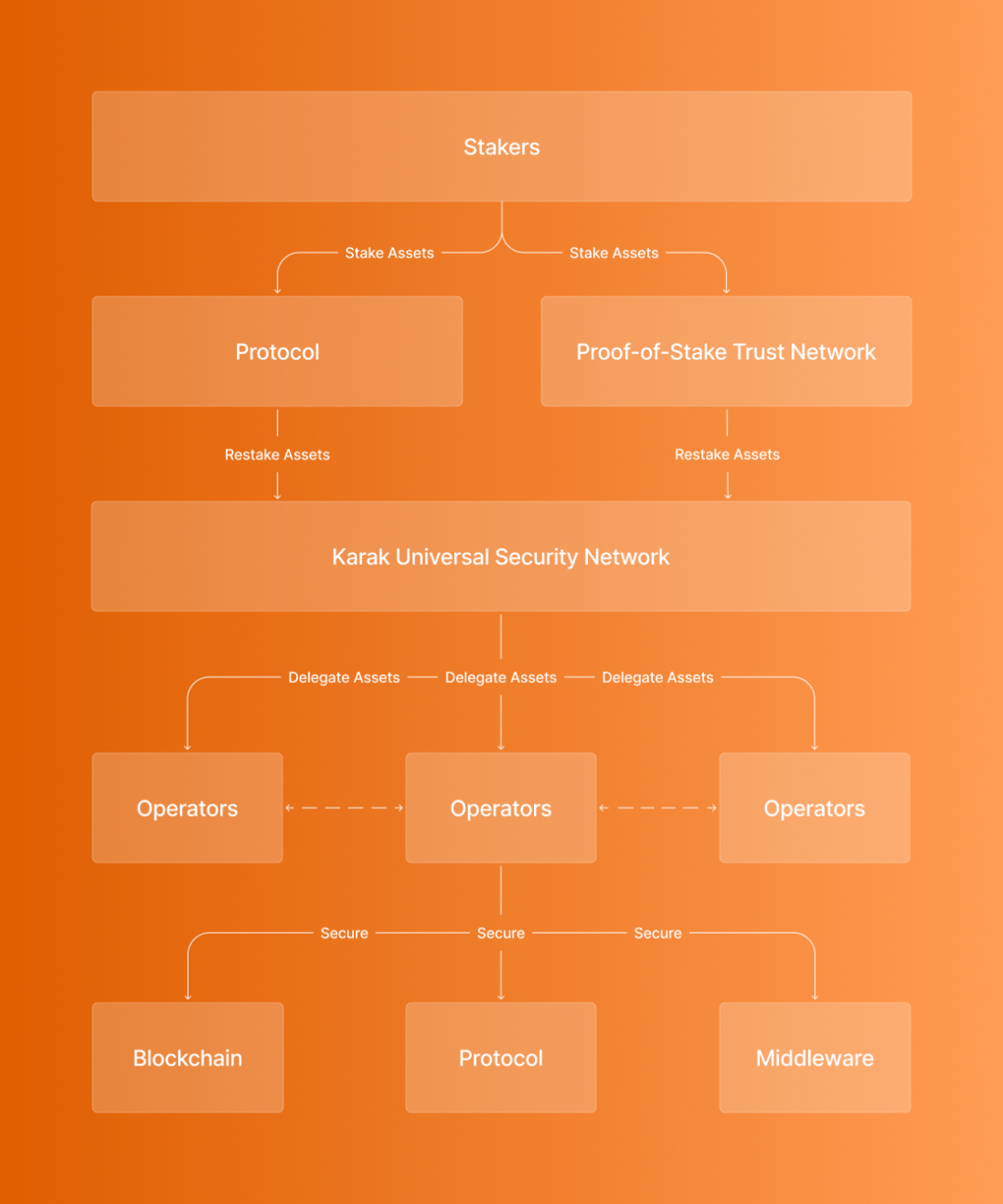

Here’s a simplified breakdown of how Karak works:

-

For validators: Staked assets are allocated to Distributed Security Services (DSS) validators on the Karak network, granting additional execution rights over their staked assets.

-

For developers: Karak enables them to attract validators through simple, non-dilutive incentives. Compared to building a new trust network from scratch, this significantly reduces costs.

Karak acts as a bridge between developers and validators. Developers can attract validators by offering non-dilutive token incentives.

This is because Karak eliminates the need for new protocols to offer highly dilutive rewards to attract and incentivize validators—a mechanism that would otherwise require massive token issuance early on to secure the network, risking token devaluation and harming long-term holders. This setup greatly reduces cost and complexity.

(Source: https://docs.karak.network/karak)

Karak’s technical approach features three key highlights:

1. Multi-asset restaking: Karak introduces multi-asset restaking, a new security mechanism allowing users to restake various assets—such as Ethereum, liquid staking tokens, and stablecoins—to earn rewards. This not only increases potential user returns but also significantly enhances the security of various DApps, protocols, and DSS.

2. Restake anywhere: Karak internalizes the concept of universal restaking, making restaked security infrastructure accessible to anyone on any chain. This convenience allows developers to focus more on innovation and product development rather than spending significant time and resources on initial security measures.

3. Turnkey development environment: Karak enables new systems to tap into a powerful and secure trust network from day one, significantly lowering the barrier for new protocols to secure themselves and allowing them to operate without complex security setups.

(Source: https://docs.karak.network/karak)

In summary, Karak’s innovations not only provide users with opportunities to restake multiple asset types but also greatly simplify the security process for new protocols. These features collectively enhance Karak’s competitiveness and appeal within the sector.

2.2 Karak vs. EigenLayer Comparison

Like EigenLayer, Karak is a restaking protocol—it enables staked assets like ETH to be restaked through validators across multiple networks, allowing validators to earn additional rewards. At first glance, Karak might appear to be a "clone" of EigenLayer, but comparing their technical approaches reveals notable differences.

So why is Karak not simply a “copy” of EigenLayer, and where do they differ?

Reason One: dApps on EigenLayer are called Actively Validated Services (AVS), while those on Karak are known as Distributed Security Services (DSS). This will be explained in detail below.

Reason Two: EigenLayer uses Ethereum mainnet as its execution layer, whereas Karak has its own Layer 2 (called K2) for sandbox testing, allowing DSS to develop and test before launching on Layer 1.

Let’s address the first question: What are AVS and DSS, and what’s the difference?

AVS stands for Actively Validated Services, a concept within the EigenLayer protocol. You can think of AVS as middleware, providing services like data and validation capabilities to end products. For example, an oracle isn’t an end product itself but offers data services to DeFi platforms and wallets—it’s an AVS.

Understanding EigenLayer’s AVS can be illustrated through a simple analogy:

Imagine Ethereum as a massive shopping mall, and various Rollup L2s (Layer 2 solutions) are stores inside the mall. To operate within the mall, these stores must pay rent—which in the Ethereum world translates to paying gas fees so their transactions and state data can be packaged, validated, and stored on Ethereum’s ledger.

In this analogy, Ethereum not only provides physical space (blockspace) but also handles security (validating transaction legitimacy and consistency), ensuring all store transactions are safe and valid.

EigenLayer’s AVS is like offering a cost-effective version of this service to small vendors who want to set up stalls outside the mall (projects). These vendors either can’t or don’t want to operate inside the mall—like mobile carts (needing liquidity) or roadside shops (good locations)—but still wish to leverage some services from the big mall. AVS can serve them. While perhaps not as comprehensive as the mall’s internal security—meaning slightly lower consensus security—it comes at a lower cost. This provides a solution for dApps that cannot be verified within the Ethereum EVM network, giving even small-scale projects a foothold in the broader Ethereum ecosystem.

This model is particularly suitable for applications with moderate consensus security requirements, such as certain DApp rollups, cross-chain bridges, and oracles. These projects may not need the highest level of security provided by Ethereum mainnet, so by choosing AVS, they can obtain necessary validation services at lower cost while still operating in a relatively secure environment. The emergence of AVS effectively expands the boundaries of the Ethereum ecosystem, enabling more diverse projects to join—especially resource-constrained yet innovative smaller ones.

Similar to EigenLayer, Karak has its own version of AVS, called Distributed Secure Services (DSS). Unlike EigenLayer, which is limited to the Ethereum ecosystem, Karak introduces a novel concept—providing restaking services for multiple assets, enabling anyone to use any asset on any chain.

In an Ethereum-only environment, AVS must compete with every opportunity offering Ethereum yields. Without speculative airdrop expectations, this competition is unsustainable. However, DSS can absorb assets from more chains, leveraging restaked assets to enhance security while reducing operational costs. Compared to ETH, many assets have lower opportunity costs, meaning DSS has simpler and more sustainable yield pathways.

Notably, the first AVS was launched simultaneously on EigenLayer’s mainnet on April 10, followed by six more AVS launches. Karak plans to launch its first DSS in the coming weeks.

Next, we tackle the second question: What is Karak’s Layer 2 K2, and how does it differ from EigenLayer?

K2 is a Layer 2 built on top of the Karak network.

Performing operations on Layer 1 can be costly for developers and users. K2 offers a new solution—an isolated "sandbox" environment where Distributed Security Services (DSS) can be developed and tested on K2 before formal deployment on L1, ensuring stability and security prior to real-world use. Additionally, by adding custom precompiles, K2 allows more validators to verify DSS, improving efficiency, security, and decentralization.

Compared to EigenLayer, which uses Ethereum mainnet as its execution layer, Karak has built its own execution layer (K2) on Layer 2, enabling faster transaction speeds and lower costs without sacrificing security.

Having addressed these two questions, it becomes clear that Karak and EigenLayer pursue divergent technical paths, resulting in obvious differences.

Karak supports a wider range of assets beyond ETH, planning to include Solana, Tia, and Layer 2s like Arbitrum and Optimism, aiming to create a cross-chain, diversified restaking layer. EigenLayer focuses on the Ethereum ecosystem, using ETH as the primary restaking asset, contrasting with Karak’s broader inclusivity.

We can use an analogy to illustrate: Imagine Karak as an international airport connecting multiple countries, welcoming travelers (assets) from around the world—whether large commercial jets (public chain assets like Solana) or private planes (Layer 2 assets like Arbitrum). Karak aims to provide these travelers with a convenient, secure transit hub. In contrast, EigenLayer resembles a metro system designed specifically for one major city (the Ethereum ecosystem), focusing on serving residents and visitors within Ethereum, delivering specialized, efficient transportation services (transactions and operations).

In other words, while Karak shares similarities with EigenLayer, it expands the scope of restakable assets—including Ether, various liquid staking ETH tokens, and stablecoins—broadening user choice.

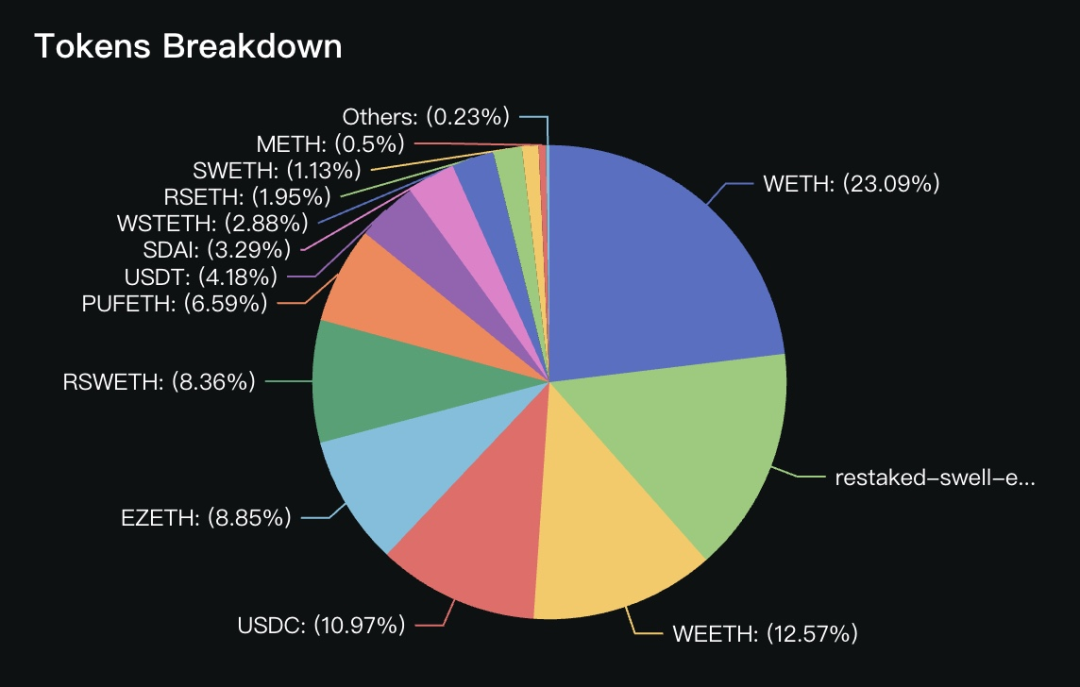

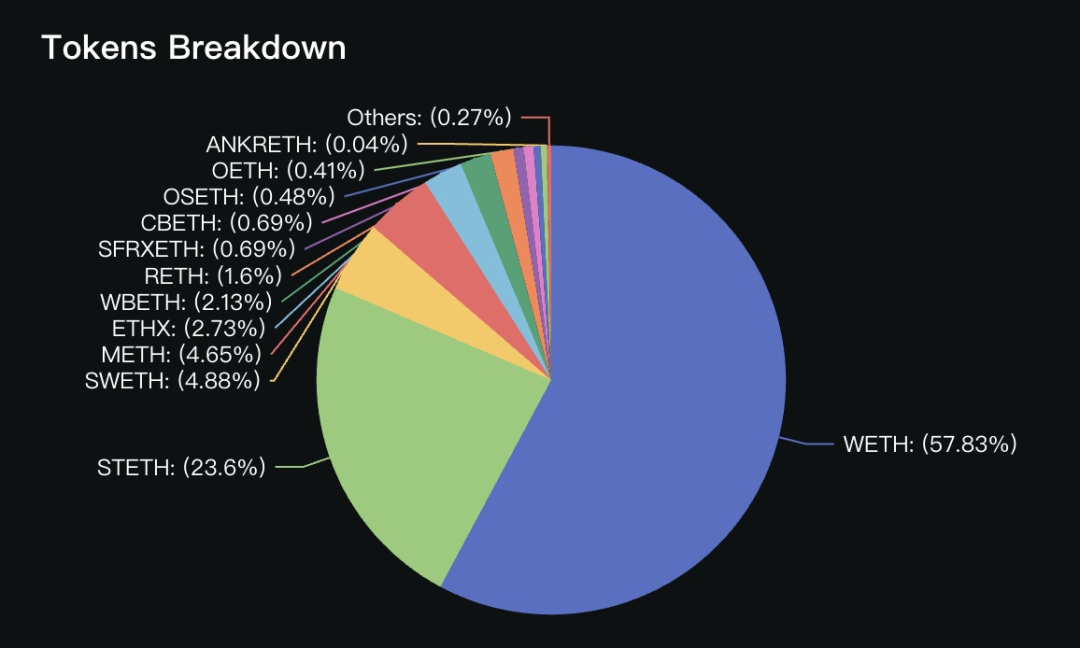

Evidence shows Karak’s approach is effective. According to DefiLlama data, for example, stablecoins make up about 19% of Karak’s restaked crypto assets, compared to less than 0.27% on EigenLayer. The pie charts below highlight further differences.

(Figure: Breakdown of Karak Restaked Crypto Assets https://defillama.com/protocol/karak#tvl-charts)

(Figure: Breakdown of EigenLayer Restaked Crypto Assets https://defillama.com/protocol/eigenlayer#tvl-charts)

03 Is Karak a Vampire Attack on EigenLayer?

Looking back at SushiSwap’s vampire attack on Uniswap, what would happen if Karak launched its token before EigenLayer?

First, let’s understand what a “vampire attack” is. In crypto, a vampire attack is a strategy where one project (in this case, SushiSwap) attempts to capture users and liquidity share from a similar project (like Uniswap) by offering better incentives—for instance, higher LP rewards for liquidity providers.

Simply put, a “vampire attack” involves siphoning off liquidity share from a target to boost one’s own liquidity and value—essentially “draining blood.”

In 2020, SushiSwap successfully attracted substantial liquidity by forking Uniswap’s code and introducing SUSHI as its native token. Given the similarity between Karak and EigenLayer, a vampire attack cannot be ruled out. If Karak launches its token first, here are several possible outcomes:

1. Karak supports multiple assets, potentially attracting prospective restakers seeking asset diversification. If it executes a vampire attack, this could pose a challenge to EigenLayer.

2. Once both Karak and EigenLayer are running mainnets with multiple AVS/DSS, Karak could potentially execute a vampire attack by migrating deposited EigenLayer LRT assets from EigenLayer to Karak. (Note: Karak allows restaking of LRTs already restaked on EigenLayer—essentially enabling nested restaking, somewhat like a matryoshka doll.)

If Karak launches its token first, it could indeed attract LRTs across the market. More importantly, Karak already has its own chain operational, with decent speed and low fees. After all, one of Karak’s standout advantages is having its own execution layer—this positions it not as EigenLayer’s junior, but as a competitor.

04 How to Become an Early Participant in Karak

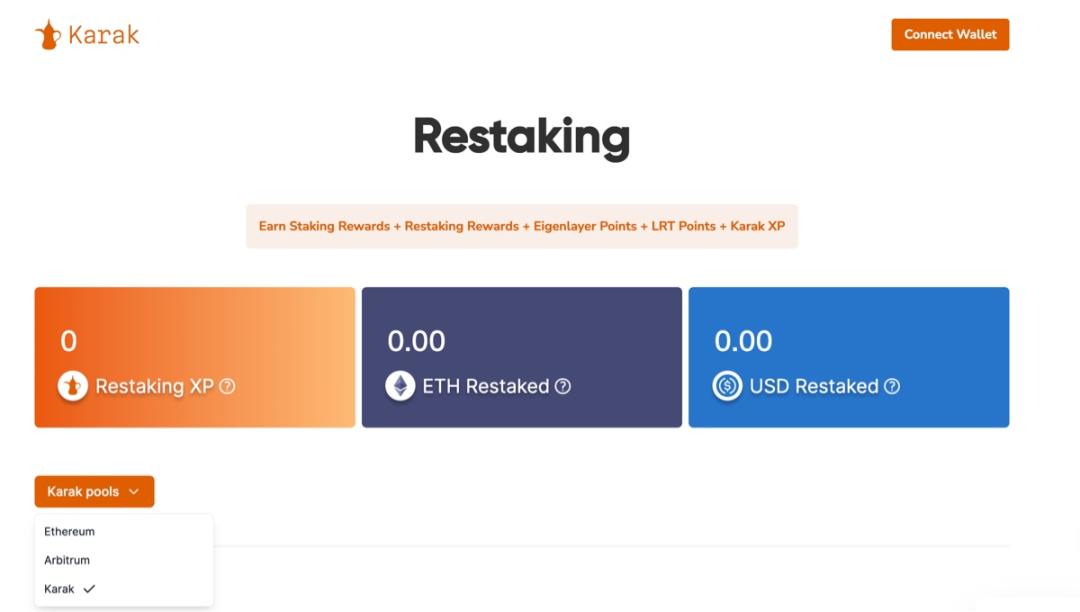

Currently, Karak is still in an early stage. Users can stake via the official website to earn XP points. Future Karak airdrops are likely to convert these points into tokens. The amount of XP earned may depend on how early and how long you restake, as well as the number of new users referred via your referral code.

Access the Karak staking interface

Official staking link: https://app.karak.network/

Currently supported staking networks on Karak: Ethereum mainnet, Arbitrum (L2), Karak (L2).

Supported staking assets on Karak: Multiple LST assets like mETH, multiple LRT assets like pufETH, and three stablecoins—USCT, USDC, and sDAI. Note that available tokens vary by network; please confirm carefully.

In short, staking on Karak earns you “staking rewards + restaking rewards + EigenLayer points + LRT staking points + Karak XP.”

Currently, Karak is not a “double-dipping” model like EigenLayer. Instead, amid EigenLayer’s “saturation,” Karak seeks higher returns by staking into other protocols—but higher returns come with higher risks.

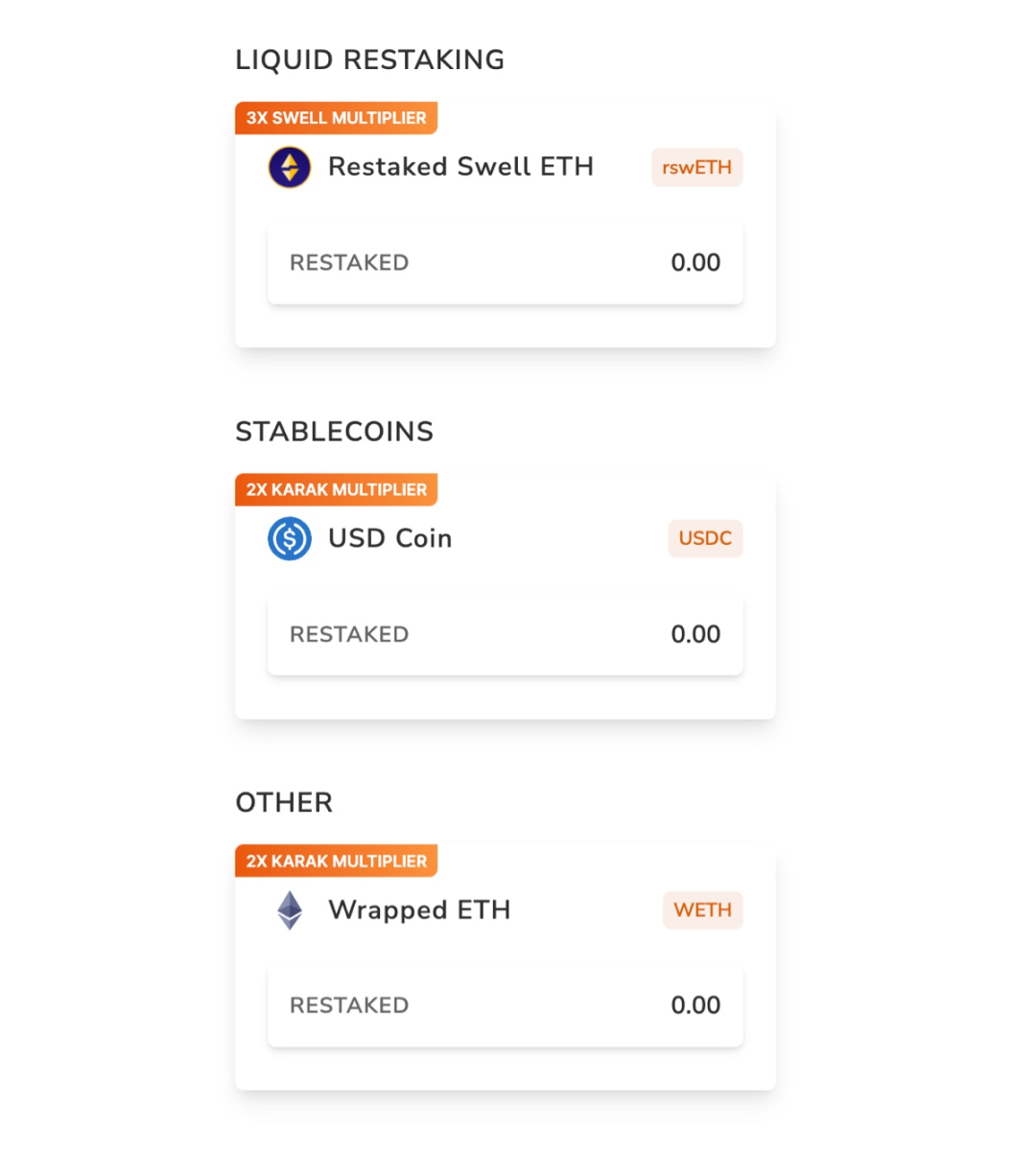

We recommend staking directly on the Karak chain (the L2 mentioned earlier) to earn double Karak points. Steps are as follows.

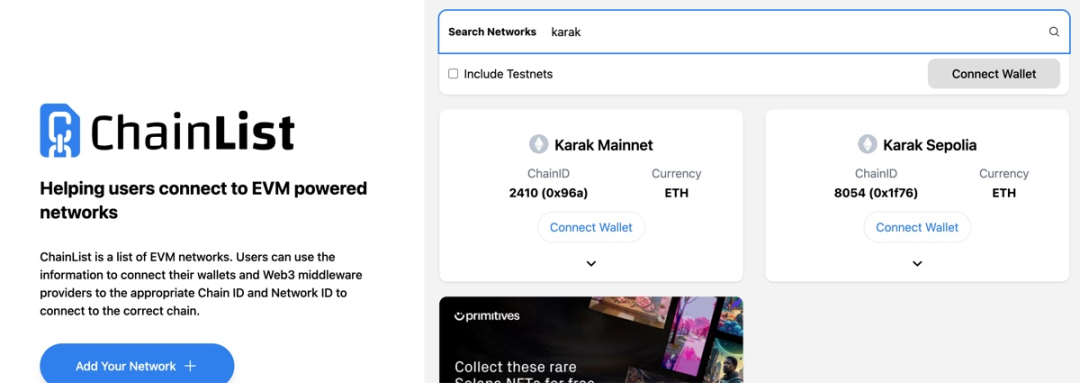

First, add the Karak network

Go to Chainlist and select Karak Mainnet on the left

https://chainlist.org/?search=karak

Next, bridge assets to the Karak chain. If choosing to stake via the Karak chain, currently three tokens are supported: rswETH, USDC, wETH.

Staking rswETH has two scenarios

1. If you already hold rswETH, you can bridge it to the Karak chain via Karak’s official bridge.

2. If you don’t hold rswETH, stake ETH on Swell to receive rswETH (note: Swell only accepts ETH staking on mainnet; do not first bridge ETH to Karak chain before staking), then bridge it to the Karak chain via Karak’s official bridge.

Swell staking address:

https://app.swellnetwork.io/restake

Staking wETH also has two scenarios

1. If you already hold wETH, you can bridge it to the Karak chain via Karak’s official bridge.

2. If you don’t hold wETH, you can bridge ETH from mainnet to Karak via Karak’s official bridge or MiniBridge. When staking, just enable Auto-Wrap ETH.

Karak official bridge and MiniBridge links:

https://karak.network/bridge

https://minibridge.chaineye.tools/?src=arbitrum&dst=karak

Finally, complete staking in Karak Pools.

Since the three supported tokens are not ETH, you’ll still need ETH for gas fees after bridging. Especially with WETH: if you bridge ETH over and choose “max” deposit, the first contract call is a Deposit function, which wraps ETH—this could leave your wallet with no ETH, causing the second deposit step to fail.

We recommend the following:

1. For staking rswETH and USDC, use the MiniBridge tool to transfer a small amount of ETH as gas.

2. For staking wETH, leave some ETH un-staked—don’t click “max.” But if you accidentally stake all, you can always bridge a bit more ETH over via MiniBridge.

🔗 MiniBridge supports ETH bridging from mainnet to Karak chain, ideal for small transfers with low fees—perfect for covering gas costs when staking on Karak. Click the link below.

https://minibridge.chaineye.tools/?src=arbitrum&dst=karak

05 Risk Warning

Currently, debates surrounding Karak mainly center on two aspects.

-

First, after securing funding at the end of 2023, the team “rushed” to launch its product in February this year. As a restaking project, there’s been little discussion around its technology so far, with marketing tactics like “points campaigns” taking precedence in capturing market attention.

-

Second, the team’s previous project has faced community criticism for alleged “self-bailout” behavior, with some influencers accusing it of being a rug pull. In response to these concerns, the team addressed the issue during a DC session on April 9.

In short, blockchain projects always carry smart contract and team-related risks, especially restaking protocols that routinely absorb hundreds of millions of dollars. Yet in today’s market environment, new users tend to favor projects backed by reputable investors and large funding rounds, while veteran users pay closer attention to a team’s past track record.

06 Conclusion

Balancing risk and reward remains a central concern for users.

As a rising star in the restaking space, Karak’s $1 billion valuation and distinctive technical strengths make it a credible challenger to EigenLayer’s dominance in restaking. Moreover, Karak supports restaking of multiple LRT tokens—including but not limited to Swell, Puffer, Renzo, EtherFi, and KelpDAO—further promoting the prosperity of the Ethereum staking ecosystem.

Perhaps sensing the “threat,” EigenLayer announced it would lift all deposit limits and reopen deposits at 00:00 Beijing time on April 17.

Will users play it safe with EigenLayer, or bet on Karak for higher returns? That decision now rests in the hands of the users.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News