Reddit U.S. Stock Discussion: Is the Second Wave of AI Stocks Here? Capital Is Rotating from Infrastructure Stocks to These Application Stocks

TechFlow Selected TechFlow Selected

Reddit U.S. Stock Discussion: Is the Second Wave of AI Stocks Here? Capital Is Rotating from Infrastructure Stocks to These Application Stocks

Didn’t see that coming, did you? Reddit’s own stock, $RDDT, is also benefiting.

Author: Select-Leading-4542

Compiled by: TechFlow

Recently, a heated discussion has erupted on Reddit’s U.S. stock community r/stocks—following the completion of the primary upward wave in AI infrastructure stocks such as NVIDIA (NVDA), more and more investors are turning their attention to application-layer companies that are truly monetizing AI, believing a new sector rotation is quietly underway.

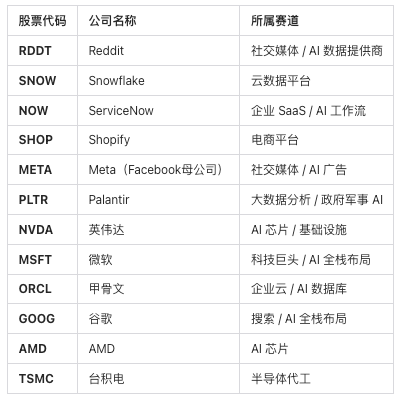

The stocks most frequently mentioned in this round of discussion include:

Original post:

NVDA and all other AI infrastructure stocks have clearly completed their major rallies.

I’m starting to wonder whether capital is finally rotating into companies that are genuinely leveraging AI to boost their own profitability.

My current focus is on RDDT, SNOW, NOW, and SHOP.

RDDT is clearly at the core as a data provider, with fundamentals appearing exceptionally strong. SNOW’s explosive rally following its earnings report shows the market strongly endorses its new AI products. Both NOW and SHOP are aggressively integrating AI into their platforms—purely from a chart perspective, both appear to be forming solid rebound patterns.

What other names fitting this logic are on your watchlist? Any worth deeper research?

Selected representative comments:

DeathStar_81 (10 hours ago): RDDT is literally breaking out right now. Its fundamentals are simply too strong to suppress—70% revenue growth, 90% profit margins, and a PEG ratio below 1.

Ambitious_Traffic530 (11 hours ago): Reddit has surged significantly lately—still worth buying now, or better to wait for a pullback?

tobybells: Reddit has been trading in a tight range—dropping from 120–130, consolidating around 140–150, then rallying to 160–170. Any entry point within this range works fine. I’m a long-term holder of RDDT—2,000 shares at an average cost of $170—so you’re buying cheaper than I did.

ShowerMotor (12 hours ago): Call me conservative if you like, but I think the second wave will still be semiconductors, and the third wave will be hyperscale cloud providers and the Magnificent Seven… boring stuff. I plan to shift most of my portfolio into the Nasdaq-100 next year and hold it indefinitely.

AloneStaff5051 (11 hours ago): Additional context: All LLMs are trained on Reddit data. Anthropic and Perplexity haven’t paid for it—and there’s clearly an ongoing lawsuit targeting them.

PotatoAjacent104937 (12 hours ago): If you follow this logic, Palantir should definitely be on your list. I hold Palantir, but feel government contract adoption is slowing. Last quarter, government revenue grew 84% YoY, while commercial revenue surged 133% YoY.

Last year, headlines about new Palantir contracts seemed to appear daily—but numbers don’t lie!

Zipski577: Defense/AI spending increases annually, and Palantir’s market share keeps rising. I used to think the commercial segment offered the biggest opportunity and considered the stock severely overvalued—but after deep diving into government contracts and historical data and rebuilding my model, a target price above $200 looks very realistic.

Hoosier2016: META, too—its AI-powered ad targeting is already highly profitable.

🔴 Bullish consensus: RDDT represents the strongest thesis in this rotation

Discussions about Reddit (RDDT) are the most animated within the community, with bullish arguments centered on its data moat—nearly all mainstream large language models (LLMs) have been trained using Reddit data, while companies like Anthropic and Perplexity have yet to pay, and related litigation is progressing. Supporters argue:

- Revenue up 70% YoY, gross margins as high as 90%, and a PEG ratio approaching—or even below—1, suggesting significant undervaluation

- As LLMs penetrate e-commerce use cases, Reddit’s role as the “trust layer of authentic human feedback” means its data value will continue rising

- The stock is currently consolidating between $140–$170, exhibiting technical breakout signals

Key point of contention: How deep is Reddit’s data moat, really?

Some investors remain skeptical, arguing that volume doesn’t equal quality—many newer models are shifting toward fine-tuning smaller language models (SLMs) on existing datasets, and Reddit content itself raises reliability concerns; thus, Reddit’s bargaining power vis-à-vis Big Tech may be overstated.

For example:

TyrannosPyros (8 hours ago): I’ve fully exited RDDT because its underperformance prevented me from allocating more capital to AMD and TSMC. The data moat is vastly overhyped. Most new models are created by fine-tuning LLMs on pre-existing datasets. Their ad revenue is solid, but I don’t believe they hold meaningful pricing power over Big Tech.

Fireballsdude: I genuinely don’t understand why people assume that because LLMs have already scraped Reddit’s existing dataset, freshly generated data no longer matters. LLMs won’t be enterprise-only—they’ll also serve e-commerce, becoming another monetization channel for these massive investments.

🟢 Views on other popular names

- META: AI-assisted ad targeting is already dramatically improving monetization efficiency. Some investors believe the market has over-penalized the company due to Meta’s metaverse setbacks and high CapEx, presenting an undervaluation opportunity

- Palantir (PLTR): Latest earnings show government revenue up +84% YoY and commercial revenue up +133% YoY—strong figures, though some investors perceive a disconnect with recent headline momentum

- Snowflake (SNOW): Surged over 30% in a single day post-earnings; its AI data products gained strong market validation—though others lament having “missed the boat”

- Semiconductors & hyperscale cloud providers: Some traditional investors believe the second wave remains semiconductors, and the third wave will rotate to Google, Apple, and other Magnificent Seven members—recommending direct, long-term investment in the Nasdaq-100

Professional perspective: What do options markets say about this rotation?

One commenter offered a more sophisticated analysis based on the volatility surface: Infrastructure stocks (e.g., NVIDIA, Dell) exhibited volatility compression following their earnings reports, signaling market consensus around CapEx expansion trajectories;

Meanwhile, application-layer names (RDDT, SNOW, SHOP) face two-way uncertainty, and their implied volatility structures haven’t skewed upward like those of infrastructure stocks. Thus, rather than using options to leverage exposure to application-layer stocks, it’s cleaner to buy the underlying shares outright.

This discussion reflects the market’s core divide today: The money from AI infrastructure has already been made—where’s the next 10x?

Most participants lean toward the view that application-layer monetization logic is gradually crystallizing—but catalysts have yet to fully materialize. RDDT stands out as the most watched name due to its unique data assets, while META and Palantir gain stronger fundamental support from AI monetization already delivered in practice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News