Ethena, riding high in popularity: Ponzi or real yield?

TechFlow Selected TechFlow Selected

Ethena, riding high in popularity: Ponzi or real yield?

Ethena delivers "crypto-native yield" to users while maintaining reasonable decentralization of the stablecoin.

Author: MIDAS CAPITAL

Translation: TechFlow

Ethena seems to have stirred up a storm on crypto Twitter. When I visited their website, I was immediately struck by the possibility of a stablecoin yielding 27%. In this article, I attempt to distinguish between Ponzi economics and real yield.

As an industry, when we hear about high-yielding stablecoins—especially after the Anchor & TerraLUNA collapse—it's easy to have an allergic reaction. I must admit that when I first opened Ethena’s landing page, my immediate thought was, “Oh no, here we go again.” Out of curiosity, however, I decided to dive into its mechanism design—and to my surprise, found little trace of Ponzi dynamics.

Mechanism Design Basics

To be fair, it's elegant and simple. In short:

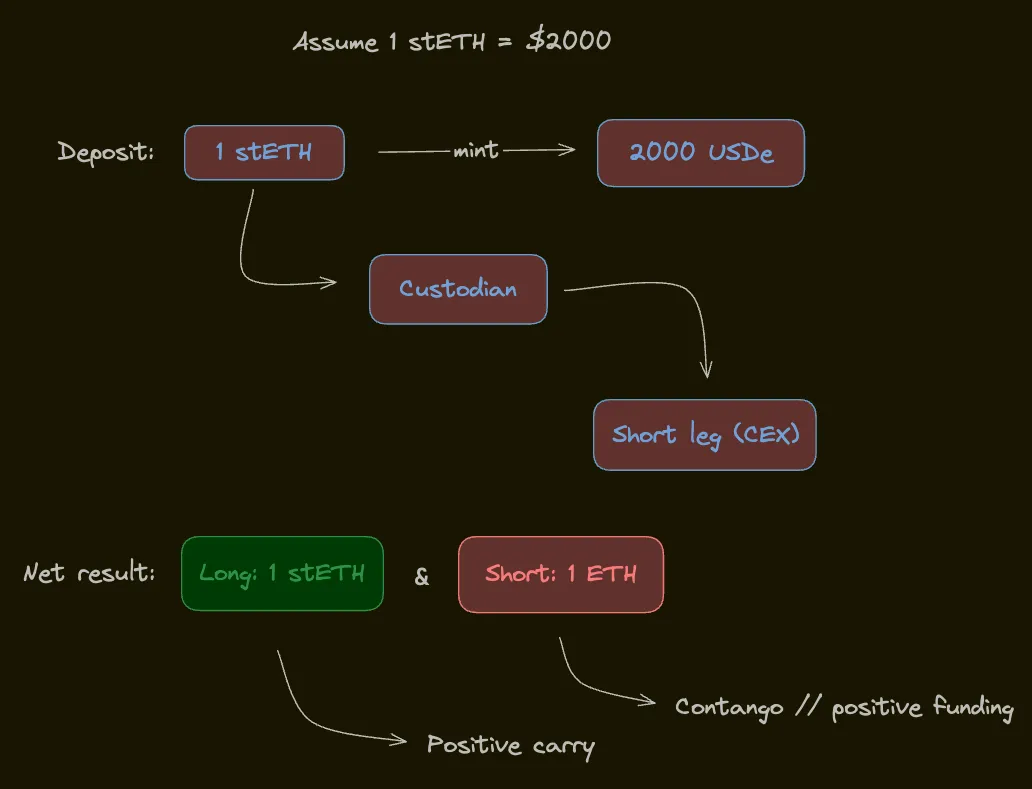

Ethena tokenizes delta-neutral arbitrage trades on ETH by issuing a stablecoin representing the value of such a delta-neutral position. Their stablecoin, USDe, captures the arbitrage yield, leading them to claim it as an "internet-native yield" internet bond.

Let’s dig a bit deeper. The process works as follows:

-

Deposit stETH into the protocol and receive an equivalent amount of USDe

-

The stETH is sent to custodians (e.g., Fireblocks or Copper), and its value is relayed to various CEXs

-

The protocol shorts ETH perpetual futures contracts across multiple CEXs using the collateral, effectively offsetting the delta of the deposited collateral

-

The end result is a combined long stETH and short ETH perpetual position

-

This delta-neutral position serves as the collateral backing USDe

The "internet-native yield" is generated by adding staking yield to the basis yield, which is then passed on to USDe holders. Specifically:

-

The deposited asset, stETH, generates yield (it has positive carry)

-

The hedge—shorting ETH perpetuals—is also yield-generating

-

If everything goes according to plan, both legs of this trade earn positive returns, meaning: stETH yield + basis yield > 0

Generally speaking, ETH is a strong base asset because it has network effects, and both sides of the trade can generate yield. As we’ve seen repeatedly, the fastest way to bootstrap a network is by offering yield—participants will do anything for yield. USDe is one of the few stablecoins that returns yield to users, while the dominant players in the space (USDT & USDC) keep all the yield for themselves. I fully support a yield-bearing stablecoin. Moreover, the separation of custody, execution, and clients is an important step toward risk mitigation. Given the FTX incident, minimizing counterparty risk is always valuable.

It's an elegant and simple design. However, astute market participants will point out that for this mechanism to work, numerous assumptions must hold.

Assumptions and Risks

Before beginning this section, it should be noted that the Ethena team has been very transparent about the risks and has made no attempt to obscure them—a practice worthy of praise.

My issue with projects of this nature is that they require a large number of assumptions to function. I think in terms of conditional probability—as the number of assumptions approaches infinity, the probability that all assumptions hold simultaneously approaches zero. Offering an annualized yield 20% above the risk-free rate means you are being compensated 20% extra for taking on these risks. If we view USDe as a tokenized claim on the cash flows of a delta-neutral position, we can begin to speak candidly and understand when the trade breaks down.

Position Risk

This is an umbrella term describing risks related to hedging and assumptions about yield sources.

-

Long stETH: They assume that if the hedge yield turns negative, stETH yield will cover those losses. If not, the collateral decays at the rate of the basis yield (stETH yield). While theoretically sound, stETH yield is only a fraction of the basis yield—these two cannot be viewed as equal balancing forces on a scale.

-

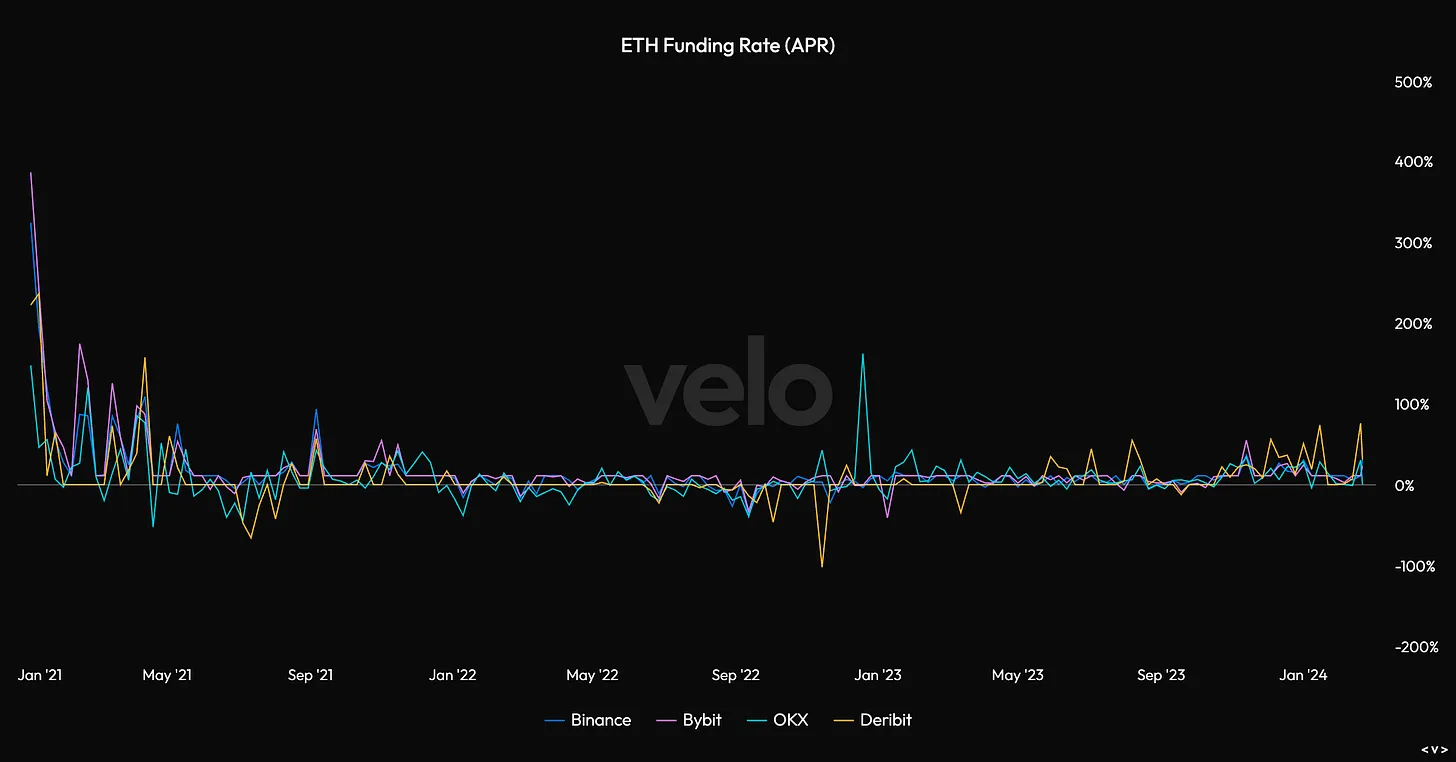

Short ETH: It is assumed that this position will on average generate yield. There is evidence supporting this, yet negative funding rates are not uncommon, turning the hedge from income into an expense. I have not seen a convincing backtest or theoretical framework explaining how Ethena’s volume will impact funding rates.

-

My concern is that as USDe adoption increases, so does demand for long stETH and short ETH perps, meaning their yield sources are squeezed from both sides. That doesn’t sound like a good setup.

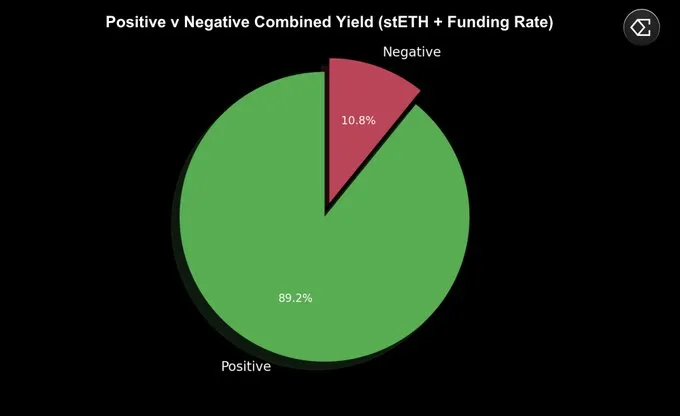

I’ve seen many charts like the one below, showing that the arbitrage trade yields positive returns 89% of the time. Overall, the data appears to support their view.

-

Funding is usually positive, with the longest streak of consecutive positive returns lasting 110 days, versus 13 days for negative streaks.

-

On a quarterly basis, Q3 2022 was the only quarter in recent years where stETH + basis yield was negative. This includes the period when everyone was trading the ETH PoW fork.

-

Exchanges often have a baseline funding rate, implying that in stagnant markets, funding tends to revert to +10% APY.

The assumption is that if aggregate yield turns negative, users will withdraw funds, reducing the supply of USDe. Once enough short ETH positions are closed, the position becomes profitable again. Additionally, there is an insurance fund running alongside the protocol, designed to absorb losses during negative yield periods. This fund will be seeded with venture capital and supplemented during positive yield periods by withholding a portion of returns. However, if book yield remains negative and the insurance fund is depleted, participants must redeem USDe—or else USDe will become undercollateralized. Notably, in such a scenario, redemption becomes necessary, and the protocol can do little—it’s beyond their control.

The chart above shows the annualized yield of shorting ETH perpetuals over the past three years. At a glance, it's unclear whether shorting this contract is a good idea.

General Risks

Below is a brief overview of some general risks.

-

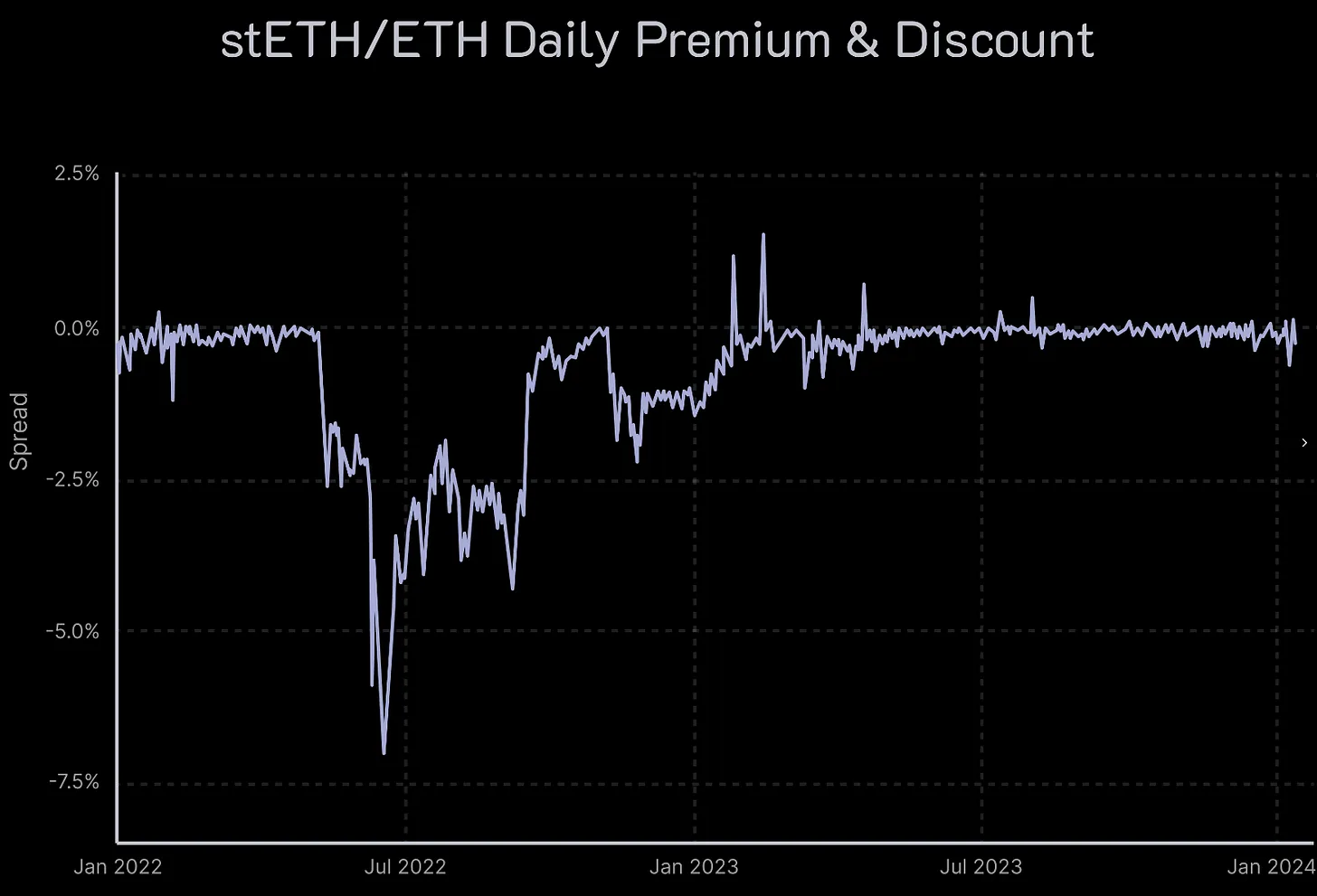

Liquidation Risk: Ethena uses derivatives on spot ETH to hedge the secondary short ETH position, but stETH and ETH are not 100% interchangeable. This can be seen as a "dirty hedge": stETH and ETH trade at par 99% of the time, but there is no mechanical link between them. If the stETH/ETH exchange rate drops significantly, the short hedge could be liquidated. More details on the specific liquidation mechanism can be found here.

-

Custody Risk: Ethena relies on off-exchange settlement providers to custody assets backing the protocol, depending on their operational capabilities. Broadly, this includes accessibility and availability risks, operational duty fulfillment risks, and custodial counterparty risks.

-

Exchange Failure Risk: Ethena uses CEXs to hedge long stETH positions. If an exchange fails, the book may not be fully hedged, and unrealized P&L could be lost.

-

Collateral Risk: Ethena uses stETH as collateral. Loss of confidence in LidoDAO could have wide-ranging consequences—for example, Lido suffering slashing events or smart contract vulnerabilities.

Conclusion

As an honest solution to the decentralized dollar problem, I find this a very interesting project, with Ethena leading the industry. They've devised a clever mechanism to pass "crypto-native yield" to users while maintaining reasonable decentralization of the stablecoin.

Let’s be clear.

Ethena.fi uses stETH as collateral and shorts ETH perpetuals against it—a classic cash-and-carry trade with a positive spread from the long leg. They tokenize the "delta-neutral" book via USDe, which entitles holders to cash flows generated by the "risk-free spread" position. This protocol is closer to a structured product than a conventional stablecoin.

Most people who’ve spent enough time in this space can see through the marketing—that’s an important skill. If we view Ethena + USDe as a tokenized cash-and-carry trade, we can more honestly assess the risks and assumptions. And frankly, earning a 27% annualized yield for tokenizing numerous risks might be fair compensation.

I believe the core issue with the protocol revolves around the sustainability of yield—they rely on large short-side returns, which are far from guaranteed. I don't find historical data persuasive because Ethena itself would bring significant changes to the market landscape. If successful, their impact would be difficult to predict in advance. The reality is, they introduce massive demand for long stETH and short ETH, compressing the trade’s yield. Their adoption means their yield sources are squeezed on both ends—there’s no free lunch.

Moreover, suppose their adoption reaches high levels, compressing their yield to 10%—would that still adequately compensate for all the aforementioned risks? What if the risk-free rate is 5%? I intuitively believe that their success eventually leads to failure—they won’t be able to compensate USDe holders sufficiently for the risks taken. Most of the time, the risks on paper are manageable, but when volatility eventually spikes and systemic risk rises, this isn’t an easy position to maintain. Furthermore, they can’t simply exit positions; they must actively manage and remain delta-neutral under all future scenarios.

So is Ethena Ponzi economics or real yield? My stance is that it’s real yield—no matter how risky that yield may be.

It’s an ambitious project, and they deserve credit for their innovation and for being upfront about the risks faced by holders. The risks are substantial, and holders are compensated accordingly. It will be an interesting journey—I wish them success.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News