SEC Issues First Penalty on NFT Industry: What Kind of NFT Constitutes a Security?

TechFlow Selected TechFlow Selected

SEC Issues First Penalty on NFT Industry: What Kind of NFT Constitutes a Security?

By examining the SEC's regulatory enforcement actions against Impact Theory and the dissenting opinions of SEC commissioners, we can analyze what types of NFTs the SEC might classify as "securities."

On August 28, 2023, the U.S. Securities and Exchange Commission (SEC) took its first regulatory enforcement action against the NFT industry, charging Los Angeles-based entertainment company Impact Theory, LLC with selling unregistered securities. The company ultimately settled with the SEC.

This marked the SEC’s first regulatory enforcement action targeting the NFT sector. The key factor in classifying these NFTs as “securities” was Impact Theory’s promises to investors of increasing value for the NFTs, the company, and their shared wealth. This article examines the SEC’s enforcement action against Impact Theory and the dissenting opinions from SEC commissioners to explore what kinds of NFTs may be deemed “securities” by the SEC.

1. Background of the Impact Theory NFT Case

According to the SEC, between October and November 2021, Impact Theory offered and sold three different types of NFTs under the "Founder’s Keys" collection to investors. Prior to the NFT launch, Impact Theory hosted online events on Discord and promoted the offering through its website and social media channels.

The SEC alleged:

(1) Impact Theory represented to investors that purchasing the NFTs constituted an investment in the company’s business, and that investors would profit if Impact Theory succeeded;

(2) Impact Theory told potential investors it was “trying to build the next Disney,” implying that the NFTs’ value would rise accordingly;

(3) Impact Theory also stated that the fortunes of NFT investors were tied directly to the success of Impact Theory and its founders.

Impact Theory sold 13,921 NFTs to investors, raising over $29 million worth of ETH. Additionally, Impact Theory earned approximately $978,000 worth of ETH in royalties from a 10% cut on each secondary market resale of the NFTs.

Based on these facts, the SEC concluded: “Potential and actual investors in the Impact Theory NFTs viewed the NFTs as investments expected to appreciate.” The SEC charged Impact Theory with violating Sections 5(a) and (c) of the Securities Act, which prohibit the offer and sale of unregistered securities.

Prior to settling with the SEC, Impact Theory took certain remedial actions, including repurchasing approximately $7.7 million worth of NFTs from investors. As part of the settlement, Impact Theory agreed to (1) destroy all NFTs it owns or controls within 10 days of the order; (2) post notice of the enforcement action on its website and social media; (3) modify its NFT smart contracts to eliminate royalty payments; and (4) disgorge ill-gotten gains and pay a civil penalty totaling approximately $6.1 million.

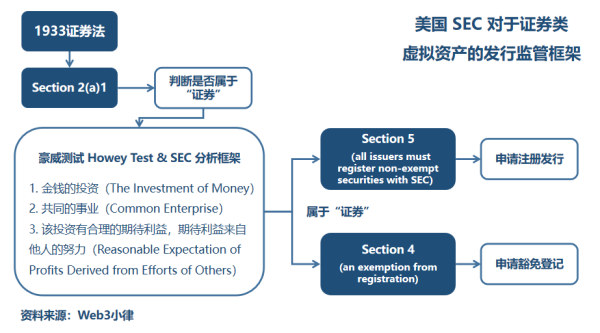

2. What Is a “Security”? — The Howey Test

Following the SEC v. Ripple case, the U.S. regulatory framework for determining whether an asset qualifies as a “security” relies on the Howey Test. Although the SEC did not explicitly explain how this particular NFT met the Howey criteria in its enforcement filing, we can still infer the SEC’s logic in treating the NFT as a security based on the facts surrounding Impact Theory’s issuance and sale.

For a detailed explanation of the Howey Test, please refer to prior articles: Understanding SEC v. Ripple: Clarifying Regulatory Uncertainty, and Not All NFTs Are Securities: Lessons from SEC v. Yuga Labs.

In this case, we can observe that Impact Theory’s NFTs superficially meet the criteria of the Howey Test: (1) there was an investment of money (in ETH); (2) the investment was in a “common enterprise,” where investors’ financial interests were aligned with those of Impact Theory; and (3) investors expected profits derived from the entrepreneurial or managerial efforts of Impact Theory—specifically, its ambition to “build the next Disney.”

Critically, Impact Theory’s explicit promise to investors that the NFTs, the company, and their collective wealth would grow was the key factor leading to the classification of these NFTs as “securities.”

3. Dissenting Statements from SEC Commissioners

Shortly after the enforcement order was issued, SEC Commissioners Hester Peirce and Mark Uyeda issued dissenting statements, arguing that this first enforcement action against the NFT industry raised significant unresolved questions that should be clarified before future cases.

First, they argued that Impact Theory’s vague and ambiguous promises to NFT investors do not sufficiently satisfy the Howey Test. Under U.S. securities law, the principle of full disclosure requires issuers to provide relatively clear and specific plans regarding fund usage and profit expectations—similar to disclosures in IPO prospectuses or ICO whitepapers. Peirce and Uyeda further noted: “The SEC does not bring enforcement actions against sellers of watches, paintings, or collectibles merely because they make vague promises about increasing value—such as gradually building brand recognition to enhance resale value of tangible items.”

Moreover, due to Impact Theory’s exaggerated marketing and unclear messaging, investors may have been misled into believing these NFTs had intrinsic financial value linked to the company. As Peirce and Uyeda pointed out: “In reality, these NFTs have no connection whatsoever to company equity or corporate valuation. Could this misrepresentation potentially constitute fraud charges?”

Second, even if the Howey Test were satisfied, Peirce and Uyeda questioned whether such aggressive enforcement was necessary. Typically, violations related to unregistered securities offerings can be remedied through a rescission offer—a right already exercised by Impact Theory via its buyback program.

Finally, Peirce and Uyeda outlined several critical questions the SEC should address before pursuing future NFT-related enforcement actions:

-

Is the Securities Act an appropriate legal framework for regulating NFTs? Is there a viable path for NFT regulation under securities law?

-

Beyond the NFT asset itself, could the manner of its issuance or secondary market royalty arrangements also constitute a “security” offering?

-

Should the compliance measures required in this settlement—such as destroying NFTs and eliminating royalties—become standard requirements in future enforcement cases? Are they appropriate?

4. What Types of NFTs Could Be Classified as Securities?

Let us first attempt to address Peirce and Uyeda’s fundamental question about how NFTs should be regulated.

4.1 How Should NFTs Be Regulated?

At their core, NFTs are a type of token whose value is derived from the underlying asset they represent. The source of value varies depending on the nature of the underlying asset, and the economic characteristics of an NFT are inherently tied to those of its underlying asset.

Referencing the Hong Kong Securities and Futures Commission (SFC)'s June 6, 2022 warning to investors about NFT risks, the SFC stated that if an NFT is a genuine digital representation of a collectible (e.g., artwork, music, or video), related activities generally fall outside the SFC’s regulatory scope. However, some NFTs may cross the boundary between collectibles and financial assets and possess characteristics defined as “securities” under the Securities and Futures Ordinance, thereby becoming subject to regulation.

Accordingly, NFTs can be categorized into three scenarios based on the nature of their underlying assets:

(1) NFTs backed by securities—subject to securities regulations;

(2) NFTs backed by commodities—subject to commodity or virtual asset regulations;

(3) NFTs representing various rights—evaluated on a case-by-case basis depending on the nature of the rights involved.

Likewise, the required disclosures for NFT offerings should be determined based on the attributes of the underlying asset.

4.2 Can the Manner of NFT Issuance and Sale (Including Secondary Market Transactions) Constitute a Security Offering?

Based on the economic substance of the transaction, NFTs may fall under “security” regulation in two ways:

(1) The underlying asset itself is a security—for example, issuing company equity as an NFT;

(2) Regardless of whether the underlying asset is a security, the method of NFT issuance constitutes a “security” offering.

Regarding point (2), in the SEC v. Ripple case, the court held that: the underlying assets of most “investment contracts” are merely standalone commodities and do not necessarily qualify as “securities,” similar to the orange groves in SEC v. W.J. Howey Co., or other commodities like gold or crude oil. Determining whether a transaction constitutes an “investment contract” requires analyzing the economic substance of the transaction to assess whether the method of distribution qualifies as a “security” offering.

In the Ripple case, XRP tokens themselves may not inherently qualify as “securities,” but Ripple’s marketing, promotion, and sale of XRP to early investors constituted an “investment contract,” thus bringing the offering under securities regulation.

Similarly, in this case, the NFTs themselves may not possess inherent “security” characteristics, but Impact Theory’s marketing and promotional activities—telling potential investors it was “trying to build the next Disney” and that NFT values would increase as a result—transformed the NFT offering into a potential “investment contract,” thereby falling under the definition of a “security.”

In summary, a “security” exists when an investor passively participates in another party’s enterprise solely through monetary investment, expecting profits derived from the efforts of that third party. If the third party fails or ceases efforts, the investor faces the risk of losing their investment.

5. Final Thoughts

Although the SEC’s enforcement action lacks judicial precedent, the outcome remains highly significant—it marks the first time the SEC has identified an NFT offering as violating the Securities Act’s prohibition on unregistered securities sales.

In an environment of regulatory uncertainty, agencies like the SEC and CFTC continue to challenge and deepen their oversight of the crypto industry. Following high-profile lawsuits against major players like Binance and Coinbase, this first enforcement action against the NFT sector signals that the SEC is not slowing down.

Previously, in our article “Legal Compliance Considerations for Brand NFT Projects Operating Overseas,” we covered key compliance points for NFT projects. However, as regulatory scrutiny intensifies, crypto companies must continue working closely with experienced legal counsel to navigate litigation, regulation, and compliance challenges.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News