PayPal's PYUSD Goes Live on Chain: How Far Are We from the Stablecoin Spring?

TechFlow Selected TechFlow Selected

PayPal's PYUSD Goes Live on Chain: How Far Are We from the Stablecoin Spring?

PayPal entering the market is just the beginning.

Written by: SAMUEL MCCULLOCH

Compiled by: TechFlow

On the morning of August 7, 2023, payments giant PayPal announced the launch of its stablecoin, PayPal USD (PYUSD). This new stablecoin will connect to PayPal’s existing 431 million users and ultimately demonstrate their commitment to blockchain.

What is PYUSD?

PayPal's PYUSD is the first stablecoin issued by a "non-crypto" company. It represents a shift in corporate attitudes toward stablecoins and reflects confidence in future regulatory acceptance.

PayPal’s stablecoin PYUSD is fully backed by U.S. dollar deposits such as short-term U.S. Treasuries and equivalent assets. Managed by Paxos Trust Company, PYUSD can be exchanged for U.S. dollars at a 1:1 ratio through the PayPal or Venmo apps.

According to PayPal’s press release:

PayPal customers purchasing PayPal USD will be able to:

Transfer PayPal USD between PayPal and compatible external wallets;

Use PYUSD for peer-to-peer payments;

Choose to use PayPal USD for purchases at checkout;

Exchange any cryptocurrency supported by PayPal with PayPal USD.

Why PayPal’s Announcement Has Major Implications for Crypto Adoption

Until now, the only way to access payment stablecoins was through crypto companies like Tether, Coinbase, or Gemini. Now, with PayPal entering the market, millions will gain access to cryptocurrencies through one of the world’s most widely used payment platforms.

Austin Campbell, former Head of Portfolio Management at Paxos and Partner at Zero Knowledge Consulting, said on Leviathan News: “One of the least developed parts of the crypto ecosystem is actual on- and off-ramps. From that perspective, it’s hard to find a better option than PayPal. I think the biggest innovation here is simply adding a native stablecoin to the PayPal platform.”

Campbell further noted that he believed this product had undergone “two and a half years of work.” Rumors about PayPal’s stablecoin development were first reported as early as 2021, when Jose Fernandez da Ponte, PayPal’s Vice President and General Manager of Blockchain, Cryptocurrency, and Digital Currencies, told the media: “It’s still too early.” Further leaks confirmed PayPal’s plans, but in February this year, the payment company announced it was pausing its stablecoin product plans after Paxos came under investigation by the New York Department of Financial Services (NYDFS). Six months later, the company clearly felt the regulatory environment had cooled enough to launch their stablecoin.

PayPal chose Paxos to manage and issue their stablecoin, meaning it will be fully reserved, have segregated funds, and publish regular transparency reports. Additionally, their stablecoin will be monitored by on-chain analytics firms like Chainalysis and TRM to prevent illegal use. If criminal activity is involved, PayPal will be able to freeze funds.

Paxos drew regulatory scrutiny due to its relationship with Binance, with a series of alleged violations ultimately leading the NYDFS to order a halt to BUSD issuance and resulting in a Wells notice from the U.S. Securities and Exchange Commission. The NYDFS stated the order was “due to several unresolved issues regarding Paxos’s oversight of its relationship with Binance.”

“In accordance with guidance from the NYDFS, Paxos will cease issuing new BUSD tokens effective February 21 and end its branded stablecoin relationship with Binance,” Paxos said in a statement.

Paxos CEO Charles Cascarilla said: “The market has changed, and our relationship with Binance no longer aligns with our current strategic focus.”

Binance’s relationship with Paxos allowed them to directly mint BUSD from the exchange and transfer it to any blockchain of their choice.

The NYDFS stated: “The Department did not authorize the use of Binance-Peg BUSD on any blockchain, and Binance-Peg BUSD is not issued by Paxos.”

Now, PayPal is partnering with Paxos, signaling that the investigation has concluded and that this once-controversial issuer can now operate freely after rigorous regulatory review.

PayPal vs Meta

Although this announcement is still fresh, the reaction to it is starkly different from the failed stablecoin Diem developed by Meta. When Facebook first announced its entry into the market in 2021, the social network faced fierce criticism from politicians, economists, and activists before Congress.

At the time, Facebook was still reeling from the Cambridge Analytica scandal, which had become a focal point of the 2020 election. The company had not yet restored its reputation, so the reaction to Diem news was intense.

Senator Elizabeth Warren strongly opposed Facebook’s “re-launching of cryptocurrency and digital wallet initiatives.” She and Senators D-HI and D-OH wrote in a letter: “Facebook is again pursuing a digital currency initiative and has already launched a pilot for a payment infrastructure network, despite these plans being incompatible with the actual financial regulatory environment—not just for Diem specifically, but for stablecoins generally.”

According to Campbell, Facebook faced two problems.

First, unlike PayPal, Diem was an entirely new business line for the company. Facebook was a social network used by over 2 billion people globally, also owning brands like WhatsApp and Instagram. Adding payment services would instantly make Facebook a massive quasi-bank capable of absorbing all its users overnight. Legislators and regulators feared Facebook would further abuse its already substantial power by leveraging data collected from users.

This social giant could already access your friend lists, likes, posts, direct messages, and geolocation data—adding Diem could potentially give Facebook unprecedented access to personal financial information. For a company whose image was already damaged by scandals, Diem was simply too big a step.

The second issue was that Diem wasn’t just a dollar-backed stablecoin; the protocol also planned to issue a currency similar to Special Drawing Rights (SDR), backed by a basket of foreign currencies including the euro, yen, Australian dollar, and Swiss franc. Economists were furious about this proposal. In their view, giving global citizens easy access to a basket of currencies would weaken central banks’ control over domestic monetary transmission. If citizens could easily access a more stable global stablecoin, who would buy their worthless bonds?

Diem never escaped regulatory entanglement. Meanwhile, PayPal shines brightly.

Interest Rates Rule Everything

In 2023, every major fintech company is a quasi-bank, with a significant portion of its revenue coming from net interest income. Companies like Coinbase, Robinhood, and many others have enjoyed outsized profits from rising interest rates.

Adding stablecoins to their offerings is tempting because they are, by design, akin to zero-interest bonds. Stablecoin issuers issue tokens but retain all yield generated from short-term Treasuries. In a perfectly rational world with unfettered competitive markets, no one would hold stablecoins or cash. What benefit is there in holding an asset that generates no interest income? Briefly… none.

But we live in a world full of massive regulatory barriers, sanctions, foreign exchange restrictions, domestic capital controls, and securities laws. For some, mere access to the U.S. dollar is sufficient. In the crypto space, demand for leverage has long outweighed demand for imported Treasury yields—until recently. With short-term yields exceeding 5% and showing no signs of cooling, a new paradigm has emerged.

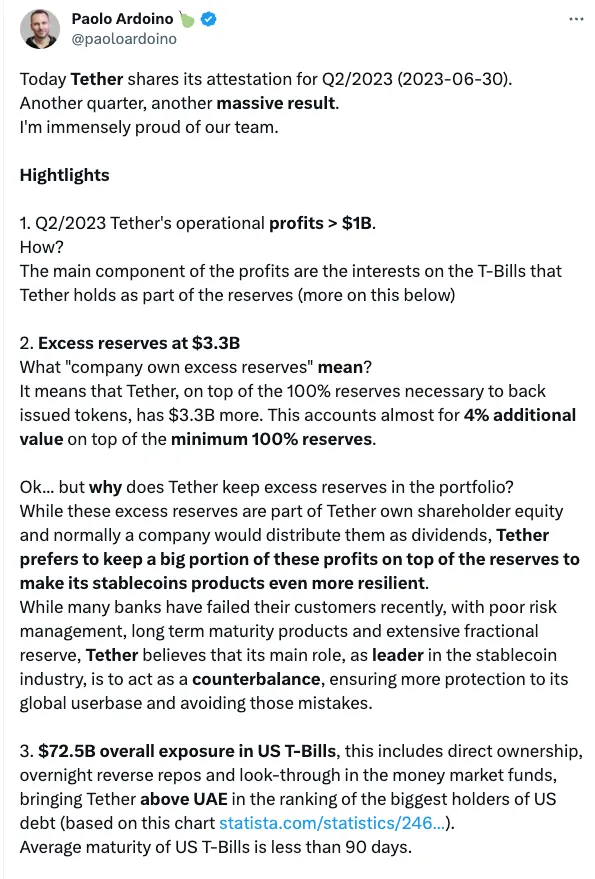

Enter Tether...

Tether is poised to earn $4 billion in net interest income this year—more than BlackRock. Simply by issuing dollar-denominated debt, every fintech company and bank should issue its own stablecoin; for them, it’s nearly “free” money.

Theoretically, PayPal should be able to compete with Tether and Circle thanks to its massive user base and broader global access channels. In our interview, Campbell suggested that PYUSD’s market cap could reach $500 billion within 5–10 years. At that scale, PayPal would become one of the largest holders of U.S. Treasuries in the world, generating over $25 billion in gross interest income annually.

Will PayPal Join the “Curve Wars™”?

Short answer: No. Or rather, it depends on jurisdiction.

In the United States and Europe, there are strict restrictions or outright bans on paying interest income to the general public. If PayPal starts conducting OTC deals with Michael to bribe their liquidity pools, Gary Gensler himself might show up at PayPal’s doorstep. In Europe, under MiCA (E-money Tokens or EMT), new stablecoin issuers are prohibited from offering interest “to reduce the risk of e-money tokens being used as stores of value.” When governments extract seigniorage rights that are no longer functional conduits, economics breaks down.

Beyond these two continents, competitive markets will drive regimes in the Middle East and Asia to attract new holding companies with a single mission: passing on interest. We’ve already seen this with Zunami Dollar (USZ), a Japan-based stablecoin that directly deposits its net interest income into the Votium liquidity pool to boost Curve liquidity. Campbell believes PayPal could set up operations in one of these regions—they’re “very global” and “don’t necessarily need to operate through a U.S. entity.”

If Michael’s vision comes true, Curve will become the leader in foreign exchange markets. PYUSD is just one of thousands of international stablecoin currencies in the market. Traders will need liquidity, and obtaining liquidity on Curve requires bribes. If PYUSD truly scales, it wouldn’t be absurd for a non-U.S. PayPal subsidiary to enter the Curve wars.

Banks Under Threat

Payment stablecoins in their current form pose a threat to banks’ inherent leveraged lending model. After Silicon Valley Bank’s collapse, depositors were forced to reassess the business models underpinning their savings. If a company like PayPal offers a stablecoin usable in DeFi, why keep funds in a bank beyond FDIC insurance and layers of regulation?

When I convert my dollars into PYUSD, I can monthly view the exact amount of investments and holdings backing my stablecoin. And Paxos holds only cash and short-term Treasuries—no long-term bond exposure, which was what caused Silicon Valley Bank’s collapse.

Campbell said: “If I want to use a debit card, I’m also participating in commercial real estate loans. People don’t think of it this way, but when you give your money to a bank, that’s how they use it. They lend that money out.”

As the SEC and Elizabeth Warren do everything possible to hinder bank growth, JPMorgan Chase will likely be the last institution to receive regulatory approval to issue a stablecoin. As retail depositors move savings from banks to DeFi, bank deposits face growing threats.

If fintech companies are allowed to operate as they currently do, structural changes are inevitable. Campbell said: “If this model continues to spread, let me clarify—I believe banks face an existential question: What does our funding model look like? What is the true cost of borrowing, and how should we structure this model? Because as we discovered in 2008, we may have been overly biased toward lending at all costs, possibly because we forced all deposits to be lent out in risky ways, regardless of whether people wanted that.”

Stablecoins Are Poised for Takeoff

PayPal’s market entry is just the beginning. Reports indicate more major payment and credit companies—such as Visa, Mastercard, and Square—have been exploring integrating stablecoins into their product lines. Today’s announcement gives a green light to competitors developing similar products. PayPal took the lead, but its rivals will closely monitor both market and Washington reactions.

If no major objections arise and PayPal’s stablecoin gains traction, these tech firms will accelerate their entry, marking the dawn of a new monetary regime. Congress has yet to pass a unified stablecoin bill, and this moment could become the catalyst forcing Washington to break the deadlock on the long-awaited stablecoin legislation. Once clarity is reached, the industry may enter a “stablecoin spring,” unleashing capital efficiency off-chain while injecting liquidity on-chain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News