MicroStrategy's Large-Scale BTC Accumulation Hides Leveraged Risks Behind

TechFlow Selected TechFlow Selected

MicroStrategy's Large-Scale BTC Accumulation Hides Leveraged Risks Behind

The hidden concerns of MSTR, the largest publicly traded BTC company.

On August 1, Nasdaq-listed MicroStrategy (MSTR) released its Q2 2023 report, announcing a significant purchase of 12,800 BTC. The market widely expressed concern over the company’s leveraged approach to buying bitcoin, as it has spent a total of $4.53 billion acquiring BTC—over $4 billion of which came from issuing bonds or stocks.

While high leverage is generally risky, for MSTR, this has become a low-cost, low-risk strategy. However, due to limited growth in its software business, the company lacks excess cash flow, and bond market financing appears increasingly difficult. It now relies on equity offerings to roll over debt—effectively tying its fate tightly to BTC price performance. If bitcoin does not rise substantially before its 2025 debt maturity, MSTR’s strategy may no longer be sustainable.

Bitcoin Holdings:

As the largest publicly traded corporate holder of bitcoin, MicroStrategy initially adopted BTC as a defensive strategy to protect its balance sheet, but it has since evolved into a core strategic pillar.

MicroStrategy operates under two main corporate strategies: acquiring and holding bitcoin, and growing its enterprise analytics software business. The company believes these dual strategies differentiate it and deliver long-term value.

Initially, the company stated that any surplus capital exceeding $50 million would be allocated to bitcoin. Subsequent statements indicated it will continue monitoring market conditions to determine whether additional financing will be used to buy more BTC.

MicroStrategy began investing in bitcoin in August 2020, shortly after the onset of the pandemic. As of July 31, 2023, the company held 152,800 bitcoins at an aggregate cost of $4.53 billion, averaging $29,672 per BTC—nearly flat with the current market price ($29,218 on August 1). Of these holdings, 90% are unencumbered, meaning they are not pledged as collateral for any loans or debts.

Figure: MicroStrategy’s BTC holdings over time (MacroStrategy is a subsidiary of MicroStrategy)

Source: MSTR, TrendResearch

We can see that MSTR purchased BTC rapidly before Q1 2022, then largely paused during the subsequent three quarters amid a sharp market downturn. Purchases accelerated again in 2023 as market conditions improved.

Financing Structure:

The company expands its balance sheet primarily through equity issuance, debt, and convertible notes.

Bond Issuance

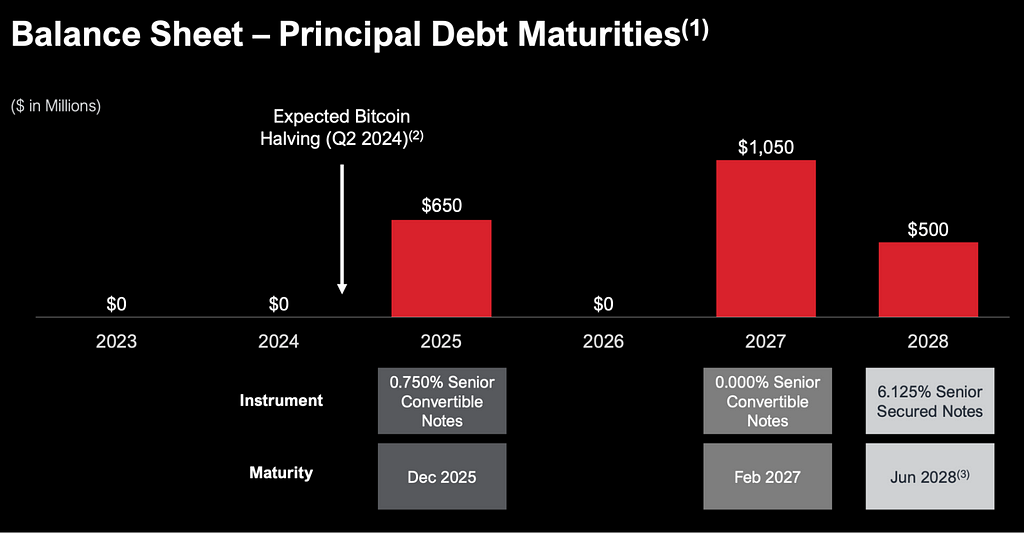

Although MSTR has continued to accumulate bitcoin each quarter, and BTC prices have declined significantly since late 2021, the company's debt structure remains relatively stable. It carries approximately $2.2 billion in total debt, with an average fixed annual interest rate of 1.6%, resulting in about $36 million in annual fixed interest expenses. This favorable position is largely due to its use of convertible notes for financing.

According to the latest Q2 2023 financial report, the company’s major outstanding debts include:

-

$500 million in senior secured notes due in 2028, bearing 6.125% interest (collateralized by 15,731 BTC), issued in June 2021. Annual interest expense is approximately $30.6 million.

-

$650 million in 0.75% convertible senior notes due December 2025, issued in December 2020. Annual interest expense is approximately $4.9 million.

-

$1.05 billion in zero-coupon convertible senior notes due February 2027, issued in February 2021. No annual interest payments are required.

MicroStrategy has no debt maturities between 2023 and 2024. Its first debt repayment comes in 2025, with the last due in 2028. This means MicroStrategy should remain financially stable through the 2024 Bitcoin halving event.

Source: MSTR, TrendResearch

Among these, convertible notes are hybrid financial instruments combining features of both bonds and stocks. Taking the $1.05 billion convertible note issued in 2021 as an example:

-

Issue amount: $900 million, with initial purchasers having the option to buy an additional $150 million within 13 days.

-

Note characteristics: Unsecured senior debt with no regular interest payments; principal does not accrue value. Matures on February 15, 2027.

-

Redemption: MicroStrategy may redeem the notes in cash after February 20, 2024, at 100% of principal plus any accrued special interest.

-

Conversion: Notes can be converted into cash, shares of MicroStrategy Class A common stock, or a combination thereof. Initial conversion rate is 0.6981 shares per $1,000 principal, equivalent to an initial conversion price of ~$1,432.46 per share—approximately 50% above the $955 closing price on Nasdaq on February 16, 2021. Noteholders may convert early if the stock trades above 130% of the strike price (~$1,400).

By issuing convertible bonds, MicroStrategy raised capital without incurring large interest burdens, while also limiting immediate equity dilution.

Why do investors accept zero-coupon convertible notes? Two primary reasons:

-

Upside potential in stock price: Convertible notes can be exchanged for company stock. If the stock price rises above the conversion threshold, investors benefit from equity appreciation—this is a key incentive.

-

Capital protection: Compared to direct stock investment, convertible notes offer downside protection. Even if the stock price falls, investors retain the right to receive par value upon redemption, with higher priority than shareholders in liquidation. This allows participation in upside while reducing risk.

Thus, convertible notes function like holding both a bond and a call option on MSTR stock. However, given MSTR’s current stock price of $434, the share price would need to increase by over 3.3x by February 2027 for investors to profit. Therefore, unless MSTR’s stock—or more precisely, bitcoin’s price—rises over 3x from current levels, MSTR effectively obtains six years of interest-free capital.

Equity Issuance

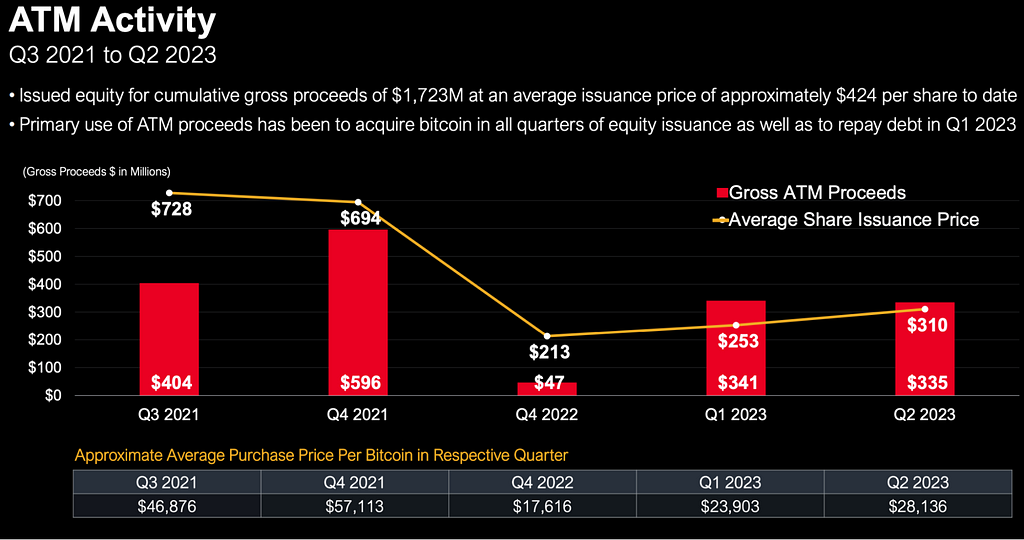

MicroStrategy raised $1.723 billion through issuance of Class A common stock in 2021, 2022, and 2023, at an average price of $424 per share. These funds were primarily used to purchase bitcoin every quarter, and partially to repay debt in Q1 2023.

The timing and details of these stock offerings:

-

Q3 2021: Raised $404 million via at-the-market (ATM) offering, average price $728/share

-

Q3 2021: Raised $596 million, average price $694/share

-

Q4 2022: Raised $47 million, average price $213/share

-

Q1 2023: Raised $341 million, average price $253/share

-

Q2 2023: Raised $335 million, average price $310/share

Figure: MSTR Stock Issuance Size and Price (2021–Present)

Source: MSTR, TrendResearch

On August 1, 2023, coinciding with the release of its Q2 report, MSTR announced a new $750 million ATM equity offering—the largest in its history—aimed at further supporting its strategy of large-scale bitcoin acquisition and holding.

Financial Health Analysis

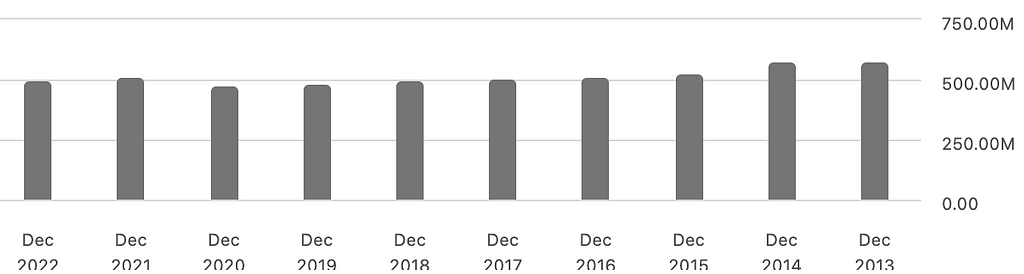

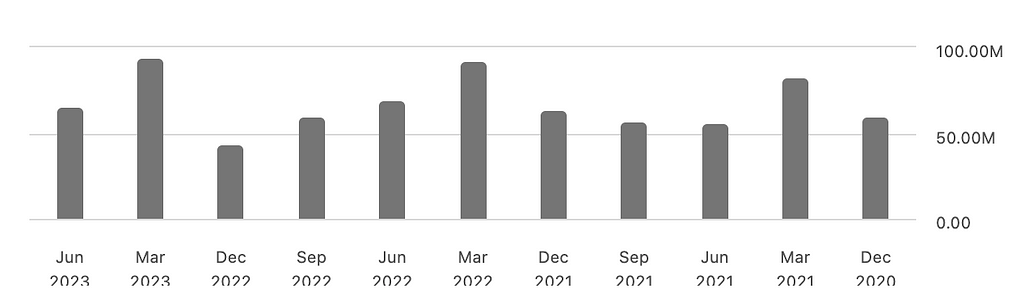

MicroStrategy’s annual revenue has remained relatively stable over recent years, reaching $499 million in 2022. However, since 2013, revenues have largely plateaued around $500 million, which is concerning for a software company failing to grow sales during a period of broader tech sector expansion.

Figure: MSTR Annual Total Revenue (Yearly)

Source: TrendResearch, SeekingAlpha

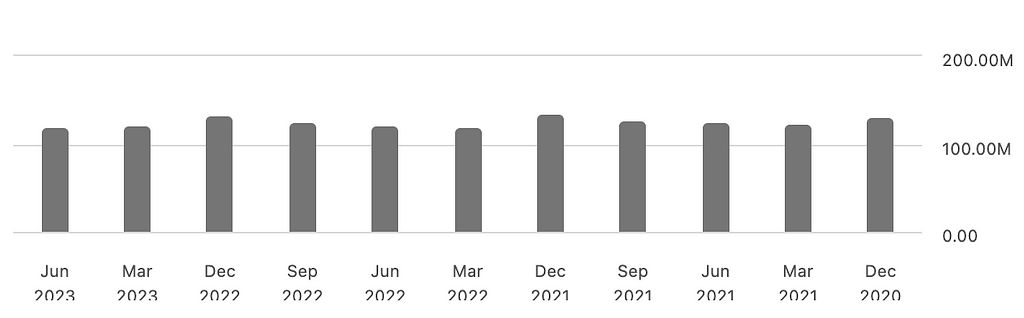

Revenue in the first two quarters of this year has shown little change, hovering around $120 million.

Figure: MSTR Annual Total Revenue (Quarterly)

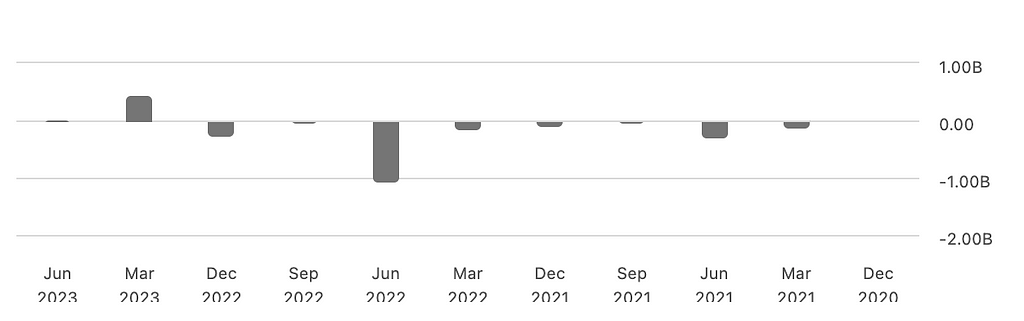

Figure: MSTR Net Profit (Annual)

Source: TrendResearch, SeekingAlpha

Although MicroStrategy reported a net profit of $483 million in the first half of 2023, its software operations remain unprofitable, with an operating loss of $30 million. The reported net profit stems primarily from a $513.5 million income tax benefit.

This tax benefit does not represent actual cash inflow but rather accounting adjustments—such as tax credits and carryforwards derived from prior BTC impairments. Under accounting rules, asset write-downs and operating losses can generate deferred tax assets, allowing companies to offset future tax liabilities.

Figure: MSTR Net Profit (Quarterly)

Source: TrendResearch, SeekingAlpha

Moreover, despite generating around $500 million in revenue, the company has no meaningful excess cash flow. Although average debt costs are only 1.6%, the $36 million in annual interest consumes over half of its cash reserves, forcing continued issuance of new debt or equity to cover interest payments. If cash reserves deplete, software investments could be jeopardized, further undermining operational revenue.

Figure: MSTR Cash and Cash Equivalents (Quarterly)

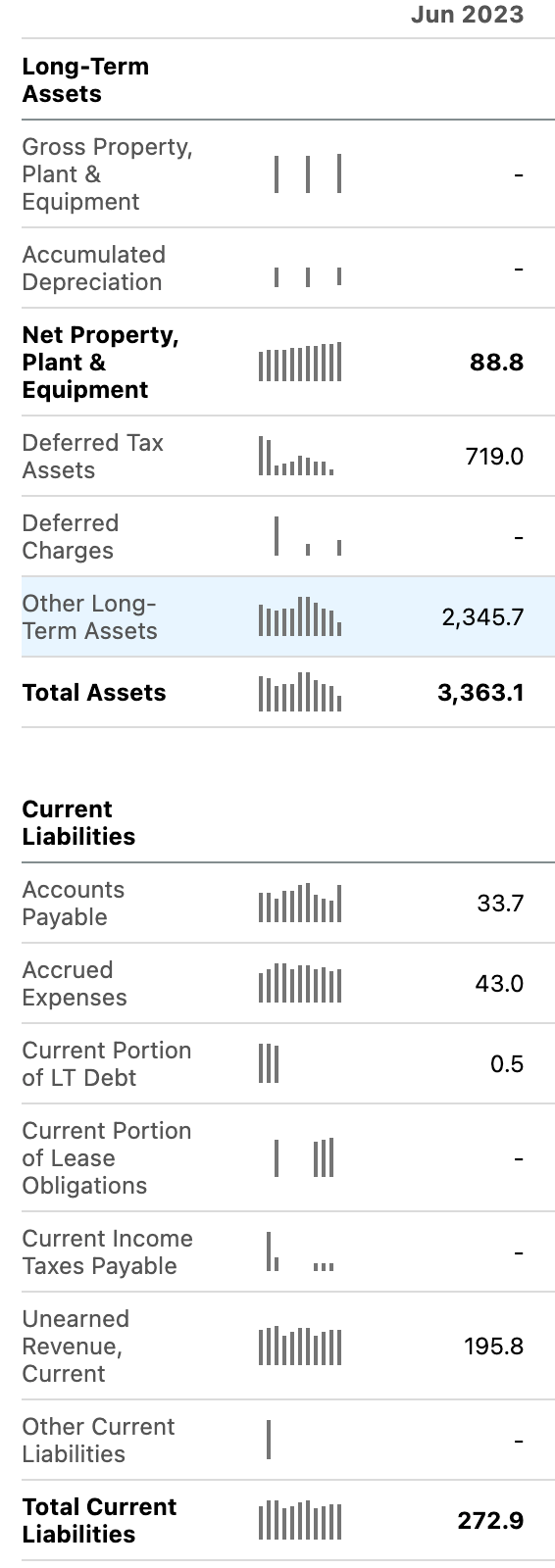

Based on MSTR’s current balance sheet, total assets stand at $3.363 billion ($2.346 billion in BTC), but this figure is understated. Under current accounting rules, BTC is valued based on historical cost minus impairment, and even if prices recover, unrealized gains are not recognized. As a result, the company reports a $2.2 billion non-permanent impairment loss. At today’s BTC price near $30,000, MSTR’s true asset value should be approximately $5.56 billion against $2.73 billion in debt.

Figure: MSTR Balance Sheet (Q2 2023)

Source: TrendResearch, SeekingAlpha

Although MSTR has minimized debt pressure through its financing model, its weak core software business ties the company’s overall prospects directly to bitcoin’s price performance. If BTC fails to sustainably appreciate from current levels, MSTR’s ability to raise further capital may falter. For instance, the recently announced $750 million ATM offering—the largest in its history—faces uncertainty. Following the announcement, the company’s stock dropped 6.4% the next day.

Given MicroStrategy’s circumstances, issuing new equity is currently cheaper than traditional bonds. Issuing convertible notes is more challenging and requires carefully structured terms to attract investors—particularly difficult in the current crypto bear market.

Notably, MSTR’s three major bond issuances all occurred during the previous BTC bull market peak (December 2020 to June 2021). Since Q3 2021, the company has relied primarily on equity offerings, reflecting difficulties in accessing bond markets or facing prohibitively high borrowing costs. With U.S. junk bond yields now above 8%, refinancing existing debt at such rates would be unsustainable. MSTR’s survival now hinges on a substantial rise in BTC price before its 2025 debt maturity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News