Observation of Global Major Web3 Digital Asset Regulatory Developments and Key Events in the First Half of 2023

TechFlow Selected TechFlow Selected

Observation of Global Major Web3 Digital Asset Regulatory Developments and Key Events in the First Half of 2023

The market's ongoing standardization is further driving Wall Street capital into the space. Once regulations become clearer, a unified global Web3 virtual asset market may emerge in the United States or worldwide.

This article covers the regulatory developments in major Web3 virtual asset jurisdictions—Hong Kong, the European Union, the United Kingdom, the UAE, Japan, South Korea, and the United States—during the first half of 2023, along with observations on key events. We observe that after an initial period of confusion and pain, global regulators are moving toward coordination, gradually establishing their own Web3 virtual asset regulatory frameworks to implement KYC/AML/CTF measures at the Financial Action Task Force (FATF) level, while focusing on investor protection and promoting healthy market development.

In contrast, the U.S. SEC’s lawsuit against Coinbase goes straight to the core of regulation by asking the fundamental question: “Which virtual assets qualify as securities?” Once this issue is clearly defined, the current regulatory uncertainty and opacity will be resolved, including registration requirements for security tokens, exchanges, custody, brokerage, and clearing services, and potentially extending direct oversight to DEXs and DeFi platforms. As markets become increasingly regulated, Wall Street capital is being drawn in. After further regulatory clarity, a unified global Web3 virtual asset market may emerge. Of course, the current fragmentation and growing pains across U.S. executive, judicial, and legislative branches are inevitable. The answer may come into focus during the 2024 election year—let us wait and see.

1. Hong Kong Launches New Virtual Asset Service Provider (VASP) Regime

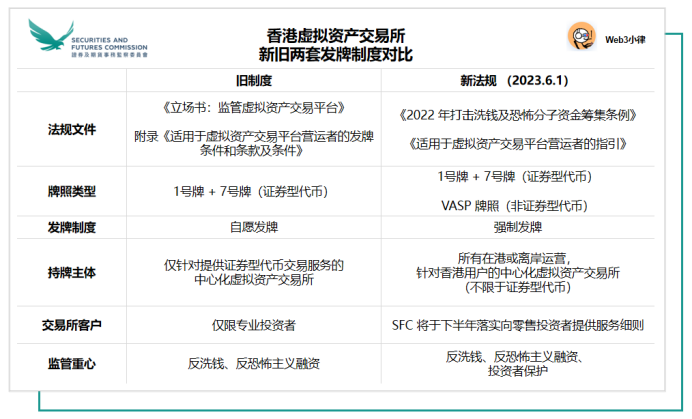

Following the release of the "Policy Statement on the Development of Virtual Assets in Hong Kong" in October last year, Hong Kong's new VASP regime officially came into effect on June 1, 2023—a landmark development for the virtual asset industry in Hong Kong.

As early as 2018, the Securities and Futures Commission (SFC) of Hong Kong had gradually established a "voluntary licensing" system targeting security token offerings, explicitly stating it had no authority to regulate virtual asset trading platforms that solely dealt in non-security tokens. Under this voluntary framework, platforms trading only non-security tokens were not required to obtain a license.

Today, the virtual asset industry has undergone significant transformation. The previous "voluntary licensing" system can no longer accommodate today’s market, which primarily serves retail investors and focuses on non-security tokens. To comprehensively regulate all centralized virtual asset trading platforms in Hong Kong and align with the latest standards from the Financial Action Task Force (FATF), the Hong Kong government amended the Anti-Money Laundering Ordinance and established a new mandatory VASP licensing regime, aiming to strike a better balance between investor protection and market development.

Once fully implemented, the VASP regime will require all centralized virtual asset exchanges operating in Hong Kong or actively marketing their services to Hong Kong investors—regardless of whether they offer security token trading—to obtain a license from the SFC and be subject to its supervision.

The SFC plans to allow licensed virtual asset exchanges to serve retail investors in the second half of the year, but only tokens that are non-securities and highly liquid—listed on traditional financial indices—will be permitted for retail access.

Regarding stablecoins, regulatory arrangements will be finalized in 2023–2024, establishing a licensing and authorization regime for stablecoin-related activities. Prior to such regulation, the SFC maintains that stablecoins should not be made available for retail trading.

TechFlow Comments:

The VASP regime aims to channel compliant exchanges into a regulated framework ("channeling the water"), making KYC and AML compliance paramount. After this initial step, we expect a series of detailed rules in the second half of the year governing retail access and investor protection. With great power comes great responsibility—only those exchanges meeting strict regulatory standards will be allowed to participate in this lucrative market and drive long-term growth. Whether Hong Kong can reclaim its former glory as a “crypto hub,” leveraging its strong traditional finance foundations, robust legal system, and proximity to mainland China, remains to be seen.

2. EU Enacts Markets in Crypto-Assets Regulation (MiCA)

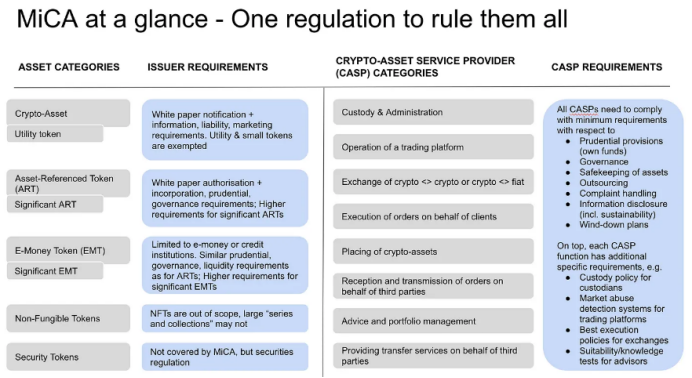

On May 31, the European Union enacted the Markets in Crypto-Assets Regulation (MiCA), published in the Official Journal of the European Union (OJEU) on June 9. This marks the emergence of the world’s most comprehensive and clearly structured unified virtual asset regulatory framework, creating a single market covering 500 million consumers and 27 EU member states. MiCA will enter into force after an 18-month transition period, on December 30, 2024.

MiCA is part of the EU’s broader Digital Finance Strategy, harmonizing rules across member states regarding: transparency and disclosure requirements for crypto-asset issuance and trading; authorization and supervision of crypto-asset service providers and issuers; operational, organizational, and governance rules for asset-referenced tokens (ARTs), e-money tokens (EMTs), and other crypto-asset services; consumer protection; and measures against market abuse and for market integrity.

MiCA fills gaps in the existing EU financial regulatory framework by establishing a dedicated regime applicable to all entities issuing crypto-assets or providing related services within the EU. In summary, MiCA regulates:

(1) Various crypto-assets, including E-Money Tokens, Asset-Referenced Tokens, and other tokens;

(2) Various crypto-asset services and service providers, including wallet custody, deposit/withdrawal, exchange, asset management, and investment advisory services.

from EU Markets in Crypto-Assets (MiCA) Regulation Expected to Enter into Force in Early 2023, Mayer Brown

from:https://paddihansen.substack.com/p/the-eus-mica-framework

3. UK House of Lords Passes Crypto and Stablecoin Regulatory Bill

Following the EU's enactment of MiCA, the UK has accelerated its own crypto-regulatory legislation. On June 19, the UK House of Lords voted to pass the Financial Services and Markets Bill (FSMB), bringing it to the final stage before becoming law. The UK may soon formally regulate virtual assets under this new legal framework.

The bill treats virtual assets as a regulated activity, initially regulating certain stablecoins as payment methods. It proposes extending the scope of Part 5 of the Banking Act 2009 to include payment systems using digital settlement assets, thereby bringing certain stablecoin-related activities under the jurisdiction of the Financial Conduct Authority (FCA).

Secondly, the bill grants regulators new powers to define additional regulated virtual assets and activities, integrating them into the traditional financial regulatory framework. Currently, the FCA only has authority to register virtual asset firms and ensure AML compliance. The bill also seeks to strengthen inter-agency coordination on emerging technologies, data usage, and decentralized technologies such as cryptocurrencies, stablecoins, NFTs, tokenization, and blockchain.

TechFlow Comments:

As the UK accelerates the clarification of its virtual asset regulatory framework, we observe institutions facing high regulatory uncertainty in the U.S. beginning to shift focus to the UK. For example, a16z recently announced the opening of its first international office in London, and Coinbase—the largest U.S. crypto exchange, recently sued by the SEC—plans to pursue a compliant business path in the UK. After losing many EU financial operations post-Brexit, the UK government is eager to reestablish London as a fintech hub. How Prime Minister Rishi Sunak’s support for the virtual asset industry will overcome the UK’s traditionally conservative political environment remains to be seen.

4. UAE Releases 2023 Virtual Assets and Related Activities Regulations (VARA Regulation)

On February 7, 2023, Dubai’s Virtual Assets Regulatory Authority (VARA) released the Virtual Assets and Related Activities Regulations 2023, effective immediately. All market participants offering virtual asset services in the UAE (excluding the two financial free zones ADGM and DIFC) must now obtain approval and licensing from either the Emirates Securities & Commodities Authority (SCA) or VARA.

The VARA regulations were issued under Dubai’s 2022 Law No. (4) on Virtual Asset Regulation, which established VARA as the world’s first independent government regulator for virtual assets. This creates a robust regulatory framework for virtual assets and blockchain technology in Dubai.

The VARA regulations grant VARA the authority to issue rules, directives, or guidelines concerning virtual asset activities. Any entity planning to conduct virtual asset activities in Dubai must obtain a VARA license prior to operation. Covered activities include consulting, broker-dealer services, custody, trading, lending, payments and remittances, and asset management/investment services. The regulations also cover: (1) classification and licensing of virtual assets; (2) mandatory registration of large proprietary traders; (3) rulebooks for VASPs; (4) AML/CFT; (5) marketing and promotion; (6) market misconduct; and (7) fines and penalties.

Additionally, on May 31, the Central Bank of the UAE issued new AML/CFT guidance for licensed financial institutions, aimed at helping them understand risks associated with virtual assets and service providers. Aligned with FATF standards, the guidance applies to banks, financial companies, exchanges, payment providers, money transfer services, insurers, agents, and brokers, and takes effect one month after issuance.

According to reports, OKX Middle East has obtained a pre-license MVP permit from VARA. OKX stated that once the Minimum Viable Product (MVP) license becomes fully operational, OKX Middle East will offer spot, derivatives, and fiat services, including USD and AED deposits, withdrawals, and spot trading pairs.

5. South Korea Passes Virtual Asset Investor Protection Act

It was reported that on May 11, the South Korean National Assembly passed the first phase of its virtual asset legislation—the Virtual Asset Investor Protection Act. The core of this phase is introducing legal rules to protect customer assets and prevent unfair trading. When international standards are set, the second phase will introduce supplementary rules on issuance and disclosure to improve market order.

The Act standardizes terminology, unifying terms like cryptocurrency, crypto asset, and digital asset under the term “virtual asset,” defined as “electronic tokens with economic value that can be traded or transferred.” Central bank digital currencies (CBDCs) are excluded. Under the Act, users can file claims for damages caused by unfair trading practices. Unfair acts such as insider trading, market manipulation, and illegal transactions will be penalized—offenders face at least one year in prison or fines up to five times the illicit gains, with penalties escalating based on profit/loss amounts.

The Act empowers the Financial Services Commission (FSC) to supervise and audit virtual asset operators. The National Assembly may also establish a Virtual Asset Committee to provide policy advice. The second phase of legislation, focusing on issuance and market information disclosure, will follow later. Chairperson Baek Hye-ryun of the National Assembly’s Political Affairs Committee remarked: “Virtual assets have finally entered the legal realm.”

6. Japan’s Largest Bank Negotiating Global Stablecoin Launch

Japan’s largest bank, Mitsubishi UFJ Financial Group (MUFG), is reportedly in talks with global stablecoin issuers and other firms to launch its own stablecoin. Tatsuya Saito, MUFG’s Vice President of Products, said the bank is discussing using its blockchain platform Progmat to issue foreign currency-pegged stablecoins (including USD) for global use. He noted that with Japan’s recent legislation, both issuers and users now have greater confidence in stablecoins. However, he declined to name specific partners.

Japan passed the world’s first stablecoin law—the amendment to the Funds Settlement Act—in June 2022, classifying stablecoins as virtual currencies and allowing licensed banks, registered transfer agents, and trust companies to issue them. In December 2022, Japanese regulators lifted restrictions on overseas stablecoins being traded domestically. Seen as a bridge between fiat and crypto, stablecoins are considered a critical component for Web3 development. They can be pegged to the yen, enabling domestic users to purchase various tokens.

7. Crypto-Friendly Banks Silvergate Bank and Signature Bank Taken Over by FDIC

On March 1, 2023, Silvergate Bank announced it would fail to submit its annual 10-K report to the SEC and might face “capital inadequacy.” Based in California, Silvergate positioned itself as a gateway to the virtual asset industry, accepting deposits from crypto exchanges and institutions, and operating its own real-time payment network—the Silvergate Exchange Network (SEN)—for converting between fiat and crypto.

The November 2022 collapse of FTX exposed Silvergate to over $1 billion in risk. Worse, FTX’s downfall triggered a severe bank run—Silvergate processed over $8.1 billion in withdrawals. To meet demand, it was forced to sell around $5.2 billion in assets at steep losses and borrow $4.3 billion from the Federal Home Loan Bank. On March 8, 2023, Silvergate filed with the SEC announcing it would cease operations and voluntarily liquidate. Its plan included full repayment of all deposits and maximizing residual asset value, including proprietary technology and tax assets. Subsequently, the Federal Deposit Insurance Corporation (FDIC) took control.

On March 10, amid rising interest rates, Silicon Valley Bank (SVB)—the 16th largest U.S. bank with a 40-year history—faced a 48-hour bank run leading to severe liquidity issues and seizure by the FDIC. This became the second-largest bank failure in U.S. history since Washington Mutual collapsed in 2008. On March 12, the Treasury, Federal Reserve, and FDIC jointly declared SVB’s resolution would fully protect all depositors. Starting March 13, customers could access all their funds, with losses borne by SVB’s shareholders and creditors—not taxpayers.

Affected by SVB’s collapse, on March 12, the U.S. Treasury, Federal Reserve, and FDIC invoked “systemic risk” to shut down crypto-friendly Signature Bank, preventing further contagion. NYDFS appointed the FDIC as receiver to manage its assets—even though Signature Bank had recovered from SVB’s impact and maintained a sound balance sheet.

TechFlow Comments:

U.S. banking regulators—federal-level OCC and state-level bodies like NYDFS—can revoke licenses due to poor management or insolvency. When a bank ceases operations, the FDIC is typically appointed as receiver, playing a crucial role in protecting depositors and minimizing systemic fallout. The closures of Silvergate Bank and Signature Bank have pushed the virtual asset industry back to a time when crypto firms lacked formal banking access—new entrants now have little chance of quickly obtaining bank charters.

from Crypto’s Last Stand in the US: USDC, Silvergate, Silicon Valley and Signature Banks Collapse in One Week

8. U.S. Regulatory Enforcement Against Binance and Founder CZ

8.1 NY Regulator Orders Paxos to Halt BUSD Issuance

On February 13, 2023, Binance CEO CZ announced that the New York State Department of Financial Services (NYDFS) instructed stablecoin issuer Paxos to stop minting new BUSD tokens (fully owned and managed by Paxos). Paxos confirmed it had received notice from the SEC regarding potential charges related to its BUSD product.

Paxos, licensed under New York’s BitLicense and directly supervised by NYDFS, issues BUSD on Ethereum and holds 1:1 USD reserves per NYDFS’ June 2022 stablecoin guidelines. NYDFS can order Paxos to halt BUSD issuance—or revoke its license—for failing to conduct proper risk assessments and due diligence to prevent illicit activities like money laundering. NYDFS stated the action aims to clarify unresolved complexities between Paxos and Binance.

Paxos responded via its website, confirming it would cease issuing new BUSD tokens from February 21, cooperate closely with NYDFS, and terminate its partnership with Binance. It plans to replace BUSD with Pax Dollar (USDP). Later, Bloomberg reported that the halt may stem not from securities concerns, but from Circle’s complaint about mismanagement of Binance-Peg BUSD reserves.

8.2 CFTC Accuses Binance and CZ of Evading U.S. Laws, Illegally Operating Derivatives Exchange

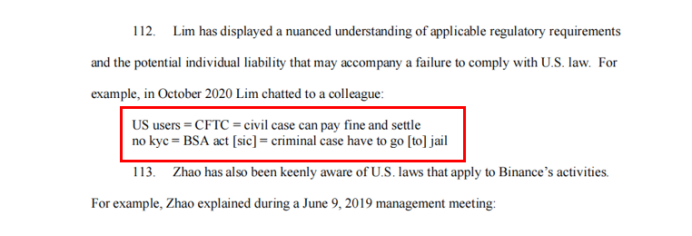

On March 27, 2023, the U.S. Commodity Futures Trading Commission (CFTC) filed a civil lawsuit alleging that CZ and three Binance entities repeatedly violated the Commodity Exchange Act (CEA) and CFTC rules. According to the complaint, since July 2019, Binance has offered and executed virtual asset derivatives to U.S. persons—including despite IP blocking—under CZ’s direction, employees and clients used VPNs and shell companies to evade compliance controls, deliberately circumventing U.S. laws through opaque operations, disregarding CEA and CFTC requirements, and engaging in systematic regulatory arbitrage for profit.

The CFTC argues that entities like Binance offering virtual asset derivatives in the U.S. must register as Futures Commission Merchants (FCMs), fulfilling KYC and other AML/CTF compliance obligations. Depending on its derivatives activities, Binance should also register as a Designated Contract Market (DCM) or Swap Execution Facility (SEF). Yet Binance has never registered with the CFTC.

Therefore, the CFTC seeks civil penalties and permanent injunctions against CZ and affiliates for violating futures trading laws, operating unregistered FCMs/DCMs/SEFs, failing to implement KYC/AML procedures, and maintaining inadequate compliance programs.

CFTC Chair Rostin Behnam stated: “Today’s enforcement action shows that no region or claim of jurisdictional immunity can shield actors from CFTC oversight. I’ve made clear that the CFTC will continue using all its tools to uncover and stop misconduct in the volatile and high-risk virtual asset sector… For years, Binance knowingly violated CFTC rules while actively working to keep money flowing and avoid compliance. This should serve as a warning to everyone in the crypto world: the CFTC will not tolerate deliberate evasion of U.S. law.”

from CFTC v. Zhao et al, legal opinion provided by former Binance Chief Compliance Officer Samuel Lim

8.3 SEC Files 13 Charges Against Binance, Affiliates, and CZ

On June 5, 2023, the SEC filed 13 charges against Binance, multiple affiliated entities, and founder CZ, including operating unregistered exchanges, broker-dealers, and clearing agencies; conducting deceptive trading; ineffective oversight of Binance.US; and issuing/selling unregistered securities.

This action followed a similar March lawsuit by the CFTC. In a 136-page complaint [14], the SEC accused CZ and Binance of: illegally soliciting U.S. investors to buy, sell, and trade crypto without restricting access to Binance.com; issuing and selling unregistered securities, including BNB, BUSD, and products like “Simple Earn” and “BNB Vault,” as well as staking programs where Binance secretly controlled user-staked assets; misleading investors by freely mixing or transferring customer assets—including to Merit Peak Limited, controlled by CZ—echoing allegations against FTX and Sam Bankman-Fried; operating as unregistered securities exchanges, broker-dealers, and clearing agencies; and lying about market manipulation safeguards on Binance.US, allowing an undisclosed market-making firm, Sigma Chain (also owned by CZ), to conduct wash trading.

SEC Chair Gary Gensler criticized CZ and Binance for “building a web of deception, conflicts of interest, lack of disclosure, and intentional avoidance of the law.” “As alleged, CZ and Binance misled investors about risk controls and false trading volumes, actively concealed platform operations, manipulated affiliated market makers, and even used customer custodial funds,” Gensler said in a press release. “They tried to fake control to evade U.S. securities laws so they could retain high-value American customers on their platform. The public should beware of investing any hard-earned assets on these illegal platforms.”

Beyond Binance, the complaint listed several tokens as securities, including but not limited to: BNB, BUSD, SOL, ADA, MATIC, FIL, ATOM, SAND, MANA, ALGO, AXS, COTI. Notably absent were high-volume tokens like ETH, USDC, USDT, and LTC. Previously, SEC Chair Gensler suggested all virtual assets except Bitcoin may have securities characteristics.

9. SEC Regulatory Enforcement Against Coinbase, the Largest U.S. Listed Compliant Exchange

Less than a day after suing Binance and CZ, on June 6, the SEC filed another lawsuit—this time against Coinbase, the largest U.S. compliant crypto exchange. Unlike the Binance case, this reflects deeper structural challenges and legal compliance issues faced by regulated exchanges.

Coinbase became the first integrated crypto financial services provider listed in the U.S. in April 2021. Known for compliance, it holds a New York BitLicense and trust charter, MTL licenses across U.S. states, and e-money licenses from the UK FCA and Ireland’s Central Bank, enabling fiat on/off-ramps and spot trading.

According to the SEC, Coinbase combines traditional financial functions—exchange, brokerage, and clearing. Since it trades crypto asset securities, it must register with the SEC. Thus, Coinbase allegedly violated regulations by:

(1) Operating as an unregistered broker, including soliciting investors, handling client funds, and charging fees;

(2) Operating as an unregistered exchange, providing a marketplace matching multiple buyers and sellers;

(3) Operating as an unregistered clearing agency, holding customer assets in wallets controlled by Coinbase and settling trades via debit entries.

The SEC also alleges Coinbase offered unregistered securities through its staking-as-a-service program, which pools and lends user assets to generate returns. Such products constitute unregistered securities offerings. Coinbase never registered this product with the SEC. Earlier in February, the SEC took similar action against Kraken, resulting in a $30 million penalty and termination of its staking services for U.S. users.

Additionally, the SEC identified 13 tokens on Coinbase as securities: SOL, ADA, MATIC, FIL, SAND, AXS, CHZ, FLOW, ICP, NEAR, VGX, Dash, NEXO. The SEC emphasized this is a non-exhaustive list.

TechFlow Comments:

Although the two SEC cases differ—one involving deliberate evasion, the other proactive compliance—one thing is shared: because certain tokens on the platform are deemed “securities,” the platforms are charged with failing to register as exchanges, brokers, or clearing agencies. The classification of virtual assets as “securities” remains the biggest unresolved issue in the U.S.

Precisely because of this ambiguity, the SEC has broad regulatory discretion. It avoids deeply defining “security,” instead using token classification as leverage to investigate deeper violations—such as money laundering, market manipulation, or investor deception. The current case against Binance and CZ exemplifies this strategy.

Thus, whether a single token is classified as a security (as in SEC v. Ripple) matters less. What matters is that after enforcement, beyond paying fines, the SEC often requires companies to implement internal controls. As more projects adopt these controls, they effectively become de facto regulations. This is how Gary Gensler “squeezed out” rules at the CFTC—and now appears to be repeating the process at the SEC.

10. U.S. Regulators Exploring Regulatory Pathways for DeFi

On April 6, 2023, the U.S. Department of the Treasury released the 2023 DeFi Illicit Finance Risk Assessment [17]—the world’s first official assessment of illicit finance risks in DeFi, responding to the White House’s March 2022 Executive Order on Digital Asset Regulation. Both FinCEN (under the Treasury) and OFAC are key regulators with extraterritorial reach. FinCEN combats money laundering and terrorist financing and analyzes financial data; OFAC enforces U.S. economic and trade sanctions based on national security and foreign policy.

The report defines DeFi services broadly—DEXs, lending protocols, yield farms, cross-chain bridges, liquid staking, algorithmic stablecoins—but excludes peer-to-peer wallet transfers. It notes most so-called DeFi platforms remain centralized, often controlled by a single entity with centralized governance. It demonstrates how criminals exploit DeFi for ransomware, theft, fraud, drug trafficking, and proliferation financing. Key vulnerabilities include lack of AML/CFT and sanctions compliance, disintermediation risks, and regulatory gaps in offshore jurisdictions failing to meet international AML/CFT standards. The report recommends strengthening AML/CFT oversight and enforcement over DeFi activities to improve compliance with Bank Secrecy Act (BSA) obligations.

TechFlow Comments:

Since August 2022, when OFAC sanctioned the DeFi mixer Tornado Cash for AML/CTF reasons, U.S. regulators have expanded their reach. The CFTC’s successful case against Ooki DAO [18] marked a turning point—defining a DAO as an unincorporated association liable under law, setting a precedent that on-chain DAOs can be sued. More alarmingly, individual governance participants may face joint liability. Once DAOs become legally actionable, on-chain spaces are no longer beyond the law—regulators can now target DeFi, DEXs, and DAOs directly.

DeFi poses challenges to financial stability (its ties to both crypto and traditional finance), suffers from anonymity-driven opacity, lacks market integrity, and faces cybersecurity threats. Regulators urgently need to address: who bears responsibility in DeFi projects? How to tackle centralization in supposedly decentralized systems? And how to close regulatory arbitrage loopholes?

11. SEC Custody Rules Pave Way for Wall Street Capital Entry

On February 15, 2023, the SEC proposed amendments to the definition of “qualified custodian” for investment advisers, raising custody standards for virtual assets and extending the requirement to fund managers and advisers—they must now use qualified custodians to hold client crypto assets.

SEC Chair Gary Gensler emphasized that existing rules (from 2009) already cover a wide range of virtual assets. While some trading and lending platforms claim to custody investor assets, they are not necessarily qualified custodians. Many fail to properly segregate client assets, commingling them so that during a “bank run,” investor funds become part of a failed company’s estate—seriously harming investor interests. These enhanced custody rules will better protect both investors and advisers.

In his August 2022 video “What Are Crypto Trading Platforms?”, Gensler outlined the SEC’s regulatory philosophy:

(1) Build on the 90-year-old U.S. securities framework to protect investors;

(2) Require separation of exchange functions—brokerage, clearing, and custody—to prevent conflicts of interest and self-custody abuses.

TechFlow Comments:

The SEC’s custody rules will encourage investors to entrust their virtual assets to licensed custodians or major banks. It also enables banking regulators to scrutinize crypto activities. In practice, custodial firms typically hold state-level trust charters and are supervised by state regulators. Anchorage Digital Bank went further, obtaining federal approval from the Office of the Comptroller of the Currency (OCC), becoming a true federally chartered digital asset bank.

One major concern for traditional finance entering crypto is asset custody safety—mainstream institutions won’t place funds in black-hole exchanges like FTX. Regulated professional custodians like Anchorage Digital Bank solve security concerns and provide auditing and insurance solutions, making them a safe choice for institutional adoption.

We see a new crypto exchange, EDX Markets, backed by Wall Street giants like Citadel Securities, Fidelity Investments, and Charles Schwab, preparing to launch. It has also raised funding from Sequoia Capital, Paradigm, and Virtu Financial, serving institutional investors with spot trading in BTC, ETH, LTC, and BCH—none of which the SEC currently classifies as securities.

EDX Markets CEO Jamil Nazarali said the platform will partner with third-party custodians and plans to launch EDX Clearing later this year to handle trade settlements. Its roadmap is clear: build a transparent, compliant, non-custodial matching platform focused on institutional clients.

Earlier, SEC Chair Gary Gensler noted that crypto exchanges bundle multiple roles—unlike traditional finance, where the NYSE doesn’t act as a hedge fund. His implication: current exchanges are too big, combining trading, market-making, and custody. This concentration was evident in collapses like FTX, Celsius, and DCG/Genesis. Hence the SEC’s new custody proposal echoes past reforms: the 1933 Glass-Steagall Act (separating commercial and investment banking) and the 2010 Dodd-Frank Act (curbing speculative trading and enhancing derivatives oversight)—both born from painful financial crises.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News