Vitalik: Analyzing Token Sale Models

TechFlow Selected TechFlow Selected

Vitalik: Analyzing Token Sale Models

Over the past few months, the number of innovations in token sale models has been steadily increasing.

Article written on June 9, 2017.

Note: I mention the names of various projects below solely for the purpose of comparing their token sale mechanisms; this should not be construed as an endorsement or criticism of any specific project as a whole. It's entirely possible for any given project to be complete garbage while still having an awesome token sale model.

Over the past few months, there has been an increasing number of innovations in token sale models. Two years ago, the space was simple: capped sales sold a fixed quantity of tokens at a fixed price and thus a fixed valuation, often selling out quickly; uncapped sales sold as many tokens as people were willing to buy. Now we have seen growing interest — both theoretically and in actual implementations — in hybrid capped sales, reverse Dutch auctions, Vickrey auctions, proportional refunds, and many other mechanisms.

Many of these mechanisms have emerged in response to perceived failures in earlier designs. Almost every major sale — including Brave’s Basic Attention Token, Gnosis, upcoming sales like Bancor, older ones like Maidsafe, and even the Ethereum sale itself — has faced substantial criticism, all pointing to one simple fact: so far, we haven’t found a mechanism with all, or even most, of the properties we would desire.

Let us review several examples.

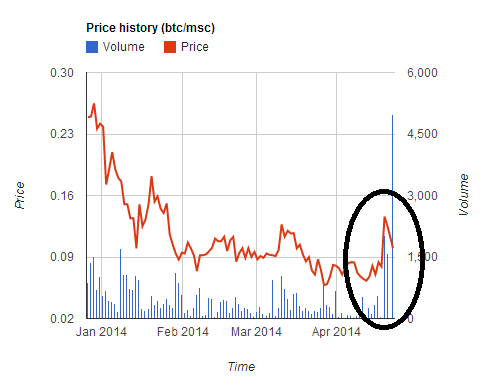

Maidsafe

</IMG>

</IMG>

Decentralized internet platform raised $7 million within five hours. However, they made the mistake of accepting two currencies (BTC and MSC) and giving preferential treatment to MSC buyers. This led to a temporary doubling of the MSC price, as users rushed to buy MSC at the favorable rate to participate in the sale, but the price then dropped sharply after the sale ended. Many users converted their BTC into MSC to join the sale, only to find the sale closed too quickly, leaving them with losses of about 30%.

This sale, along with several others (cough cough WeTrust, TokenCard) following this pattern illustrates a lesson that should now be uncontroversial: conducting a fixed-exchange-rate sale while accepting multiple currencies is dangerous and disadvantageous. Don't do it.

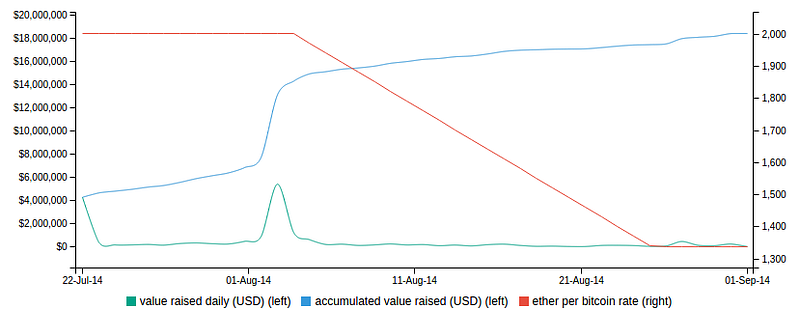

Ethereum

The Ethereum sale was uncapped and ran for 42 days. During the first 14 days, the price was 2000 ETH per 1 BTC, then it increased linearly, ending at 1337 ETH per 1 BTC.

</IMG>

</IMG>

Almost all uncapped sales have been criticized as "greedy" (a critique I have significant reservations about, but we'll return to that later), though there is another, more interesting criticism of such sales: they create high uncertainty for participants regarding the valuation of what they are buying. Consider a sale that hasn't yet started: many people might be happy to spend $10,000 on a batch of Bancor tokens if they knew this represented 1% of all existing Bancor tokens, but if they instead bought 5,000 Bancor tokens without knowing whether the total supply was 50,000, 500,000, or 500 million, many would become very anxious.

In the Ethereum sale, buyers who cared about valuation predictability typically bought on day 14, inferring it was the last day of the discount period, so they got maximum predictability along with the full discount. But this behavior is hardly economically optimal; such equilibrium resembles everyone buying during the last hour of day 14 — a private trade-off between valuation certainty and gaining a 1.5% profit (or, if certainty is very important, purchases might spread into days 15, 16, and beyond). Thus, the model certainly has some quite strange economic properties — properties we’d really like to avoid if there were a convenient way to do so.

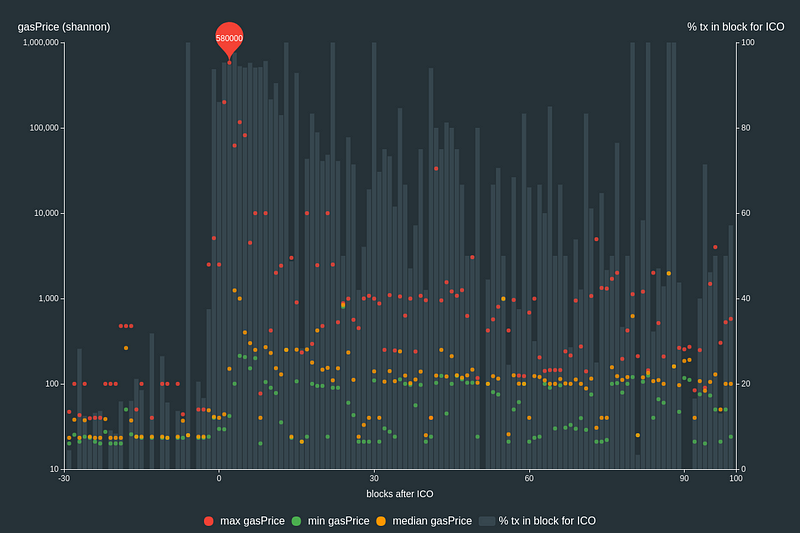

BAT

Throughout 2016 and early 2017, capped sales were most popular. The appeal of capped sales likely stemmed from frequent oversubscription, creating strong incentive pressure. Initially, sales took several hours to complete. However, soon speeds began accelerating. FirstBlood completed a $5.5 million sale in two minutes, generating much publicity — while an active denial-of-service attack against the Ethereum blockchain was underway. However, it wasn't until last month’s BAT sale that the race toward Nash equilibrium reached its peak, when due to massive interest in the project, a $35 million sale was completed in 30 seconds.

</IMG>

</IMG>

The sale was not only completed within two blocks, but also included:

- Total transaction fees paid amounted to 70.15 ETH (> $15,000), with the highest single fee reaching $6,600

- 185 successful purchases, over 10,000 failed attempts

- After the sale began, the Ethereum blockchain remained fully congested for three hours

Thus, we begin to see how capped sales naturally reach equilibrium: people try to outbid each other on transaction fees until potentially millions of dollars in surplus are burned into miners' hands. And this is before the next stage begins: large mining pools hitting the starting line and simply buying up all the tokens themselves before anyone else can.

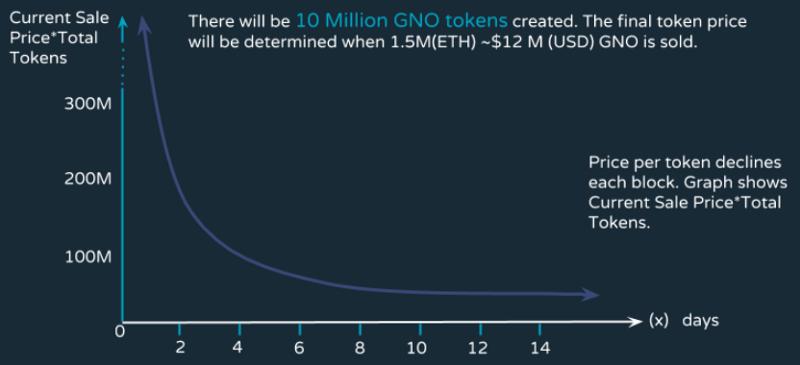

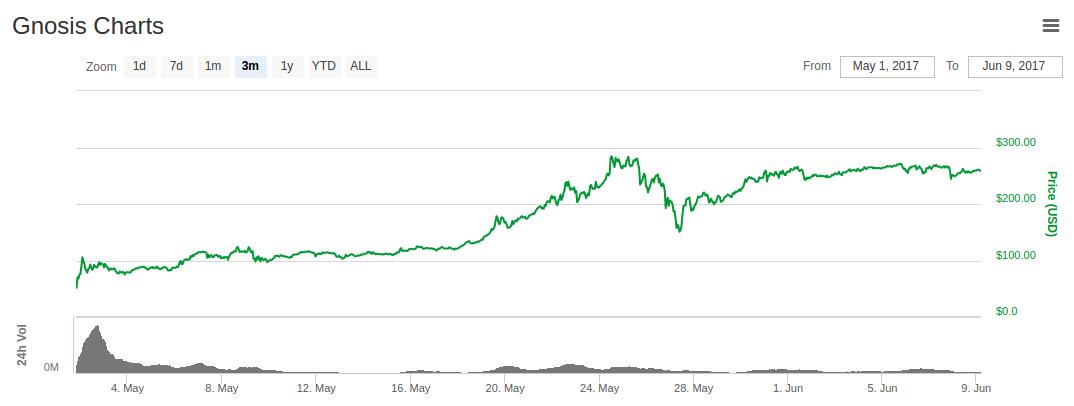

Gnosis

The Gnosis sale attempted to mitigate these issues using a new mechanism: a reverse Dutch auction. The simplified terms are as follows. There was a cap of $12.5 million. However, the portion of tokens actually distributed to buyers depended on when the sale concluded. If it finished on the first day, only about 5% of the tokens would go to buyers, with the rest allocated to the Gnosis team; if it finished on the second day, it would be ~10%, and so on.

The goal was to create a schedule where if you bought at time T, you were guaranteed to buy at a valuation of at most 1/T.

</IMG>

</IMG>

The aim was to create a mechanism with a simple optimal strategy. First, you personally decide the maximum valuation (call it V) at which you’re willing to buy. Then, when the sale starts, you don’t immediately purchase; instead, you wait until the valuation drops below that level, then send your transaction.

There are two possible outcomes:

- The sale ends before the valuation drops below V. Then you're happy because you avoided what you considered a bad deal.

- The sale ends after the valuation drops below V. Then you sent your transaction and are happy because you entered what you considered a good deal.

However, many predicted that due to "fear of missing out" (FOMO), many would "irrationally" buy on the first day without even checking the valuation. That’s exactly what happened: the sale concluded within hours, reaching the $12.5 million cap, selling only 5% of all existing tokens — implying an implicit valuation of over $300 million.

All of this, of course, makes perfect fodder for narratives claiming markets are completely irrational, with people investing large sums without clarity (often with the subtext that the entire space needs to be suppressed to prevent further frenzy), if it weren’t for the inconvenient fact: the traders who bought were correct.

</IMG>

</IMG>

Even under ETH conditions, despite ETH’s significant price increase, the price of 1 GNO has risen from about 0.6 ETH to about 0.8 ETH.

What happened? A few weeks before the sale, facing public criticism that holding most of the coins could give them central-bank-like power to manipulate the GNO price strictly, the Gnosis team agreed to hold 90% of the coins unsold for one year. From a trader’s perspective, long-term locked coins don’t affect the market and may effectively not exist in short-term analysis. This is what initially last July supported Steem’s high valuation and enabled Zcash to reach over $1,000 per coin early on.

Now, one year isn’t long, and one-year locked coins aren’t as permanent as permanently locked ones. However, reasoning goes further. Even after the one-year holding period expires, one could argue it’s only beneficial for the Gnosis team to release the locked coins if doing so increases the price, so if you trust the Gnosis team’s judgment, it means they’ll do something at least as good for the GNO price as permanently locking the coins. Therefore, in effect, the GNO sale was more like a capped sale with a $12.5 million cap but a $37.5 million valuation. And the traders participating in this auction reacted appropriately, leaving dozens of internet commentators baffled.

Of course, there’s a strange bubble around crypto assets, where various obscure assets reach $100 million market caps (including BitBean at $12 million, PotCoin at $22 million, PepeCash at $13 million, and SmileyCoin at just $14.7 million as of writing). Yet here is a clear example where participants during the sale phase did nothing wrong, at least for themselves; rather, since 2015 (and arguably since early 2010), buyers in sales have simply (correctly) anticipated the existence of a persistent bubble.

Moreover, beyond bubble behavior, there is another legitimate criticism of the Gnosis sale: despite their one-year no-sale commitment, eventually they will gain access to all their coins, and will have the ability, to some extent, to act like a central bank and heavily manipulate the GNO price, forcing traders to contend with all the monetary policy uncertainty that entails.

Specifying the Problem

So what would a good sale mechanism look like? One way to start is by reviewing criticisms of existing sale models we’ve seen and compiling a list of desired properties.

Let’s do that. Some natural properties include:

- Valuation certainty – If you participate in a sale, you should at least have certainty about the upper bound of the valuation (in other words, the percentage of all tokens you are getting).

- Participation certainty – If you attempt to participate in a sale, you should usually be able to rely on succeeding.

- Funds raised limit – To avoid appearing greedy (or possibly reduce regulatory scrutiny risk), the sale should cap the amount it collects.

- No central bank – The token sale issuer shouldn’t be able to control the market with an unexpectedly large share of tokens.

- Efficiency – The sale should not lead to economic inefficiencies or deadweight loss.

Sounds reasonable?

Well, here comes the less fun part.

- (1) and (2) cannot be fully satisfied simultaneously.

- (3), (4), and (5) cannot be satisfied simultaneously without very clever tricks.

These can be called the “first token sale dilemma” and the “second token sale dilemma.”

The proof of the first dilemma is simple: suppose you have a sale that gives users certainty of a $100 million valuation. Now suppose users try to invest $101 million into the sale. At least some will fail. The proof of the second dilemma is a straightforward supply-and-demand argument. If you satisfy (4), then you are selling either all or a fixed large fraction of the tokens, so the valuation at which you sell is proportional to the price you set. If you satisfy (3), then you are setting a price ceiling. However, this means the equilibrium price for your sale quantity might exceed your set price ceiling, leading to shortages, which inevitably result in (i) digital equivalents of queuing four hours for a popular restaurant, or (ii) digital equivalents of ticket scalping — both involving significant deadweight loss, contradicting (5).

The first dilemma is unavoidable; some valuation uncertainty or participation uncertainty is inevitable. But when a choice exists, aiming for participation uncertainty over valuation uncertainty seems better. The closest we can come is a compromise of full participation with guaranteed partial participation. This can be achieved via proportional refunds (e.g., if $101 million is invested for a $100 million valuation, everyone gets a 1% refund). We could also view this mechanism as an uncapped sale where part of the payment takes the form of locked capital rather than spent money; but from this viewpoint, it’s clear that the locked capital requirement creates efficiency loss, so this mechanism cannot satisfy (5). If ether holdings aren’t sufficient, it could harm fairness by favoring wealthier stakeholders.

The second dilemma is harder to overcome, and many attempts to circumvent it easily fail or backfire. For example, the Bancor sale is considering limiting gas prices for purchase transactions to $50 (equivalent to 12 times normal gas prices). However, now the buyer’s optimal strategy becomes creating numerous accounts and sending transactions from each to trigger the contract, then attempting to purchase (indirectly, to ensure the buyer doesn’t accidentally buy more than desired and reduce capital requirements). The more accounts a buyer sets up, the higher their chance of entry. Thus, in equilibrium, this could cause the Ethereum blockchain to be more congested than BAT-style sales, where at least $6,600 went to a single transaction rather than a network-wide denial-of-service attack. Moreover, any form of on-chain transaction spam race severely harms fairness, as the cost to participate is constant while rewards scale with how much money you have, disproportionately favoring wealthy stakeholders.

Moving Forward

There are three smarter things we can do. First, conduct a reverse Dutch auction like Gnosis, but with a twist: instead of holding unsold tokens, allocate them to some public good. Simple examples include: (i) airdrops (i.e., redistribution to all ETH holders), (ii) donations to the Ethereum Foundation, (iii) donations to Parity, Brainbot, Smartpool, or other individuals and companies independently building Ethereum ecosystem infrastructure, or (iv) some combination of all three, possibly weighted by votes from token buyers.

Second, you can retain unsold tokens but address the “central bank” issue by committing to a fully automated plan. The reasoning here is similar to why many economists are interested in rule-based monetary policy: even if a centralized entity controls powerful resources, if the entity credibly reduces much of the resulting political uncertainty by committing to apply them according to a set of programmed rules, outcomes improve. For example, unsold tokens could be deployed into a market-making agent tasked with maintaining token price stability.

Third, you can conduct a capped sale with limits on how much each person can buy. Doing this effectively requires a KYC process, but the upside is that a KYC provider could do it once, whitelist a user’s address after confirming it represents a unique individual, and then reuse those addresses across every token sale, as well as other applications benefiting from sybil-resistant per-person systems like Akasha’s quadratic voting. There is still deadweight loss (i.e., inefficiency) here, as it leads to token participation by parties with no personal interest, knowing they can quickly flip tokens for profit. However, this arguably isn’t so bad: it creates a form of crypto universal basic income, and if behavioral economics assumptions like the endowment effect are more valid, it could successfully achieve broad ownership distribution.

Are Single-Round Sales Even Good?

Let’s return to the topic of “greed.” I don’t think many people fundamentally oppose development teams spending $500 million to build a truly amazing project worth $500 million. Rather, objections stem from (i) brand-new, untested teams receiving $50 million simultaneously, and (ii) more importantly, a mismatch in timing between developer incentives and token buyer interests. In a single-round sale, developers get funding only once, near the beginning of development. There’s no feedback mechanism where a team first receives small funds to prove itself, then earns increasingly larger funding as it demonstrates reliability and success. During the sale, little information filters good from bad teams, and once the sale concludes, developers have relatively low motivation to continue working compared to traditional companies. “Greed” isn’t about raising large funds, but about raising large funds without demonstrating the ability to spend them wisely.

If we want to solve the core of this problem, how would we do it? I’d say the answer is simple: move beyond single-round sales.

I can offer several examples for inspiration:

- Angelshares – This project conducted a sale in 2014, selling a fixed percentage of all AGS daily over several months. Each day, people could contribute unlimited amounts to the crowdfunding, and AGS allocation for that day would be distributed among all contributors. Essentially, it was like having hundreds of “uncapped” sales over most of a year; I’d argue the duration could be extended further.

- Mysterium held a major promotional micro-sale campaign six months before a major event.

- Bancor recently agreed to convert all funds above the cap into a market maker that maintains price stability while preserving a floor price of 0.01 ETH. These funds cannot be withdrawn from the market maker for two years.

It may seem hard to see how Bancor’s strategy relates to solving the timing mismatch in incentives, but one element of the solution is present. To understand why, consider two scenarios. First, suppose the sale raises $30 million with a $10 million cap, but after one year, everyone considers the project a failure. In this case, the price would try to fall below 0.01 ETH, the market maker would lose all funds maintaining the floor, so the team only accesses $10 million. Second, suppose the sale raises $30 million with a $10 million cap, and after two years, everyone is happy with the project. In this case, the market maker isn’t triggered, and the team gains access to the full $30 million.

A related proposal is Vlad Zamfir’s “safe token sale mechanism”. The concept is highly general and can be parameterized in many ways, but one parameterization involves selling coins at a maximum price cap, setting a price floor slightly below that cap, letting both diverge over time, and gradually releasing capital for development if the price remains stable.

Arguably, none of the above three fully solve the issue. We’d like sales to be spread over longer periods, giving us more time to identify which development teams are most valuable before giving them most of the funds. But this seems like the most productive direction to explore.

Beyond the Dilemmas

From the above, while there’s no way to resist the dilemmas and trilemmas ahead, there are ways to sidestep the edges and tackle problems involving variables that aren’t obvious from a simplistic view. We can somewhat guarantee participation certainty by using time as a third dimension to mitigate impact: if you don’t get in during round N, you can wait for round N+1, coming in a week, where prices may not differ much.

We can have an overall uncapped sale composed of distinct phases, each individually capped; this way, the team won’t receive large funds without first proving they can manage smaller rounds. We can sell only a small portion of token supply upfront, merging the remainder into contracts that automatically sell according to pre-specified formulas, eliminating the political uncertainty such demands create.

Below are some possible mechanisms following the spirit of the above ideas:

- Hold a low-threshold Gnosis-style reverse Dutch auction (e.g., $1 million). If less than 100% of the token supply sells, automatically initiate another auction two months later with a 30% higher cap. Repeat until the entire token supply is sold.

- Sell unlimited tokens at price $X, placing 90% of proceeds into a smart contract guaranteeing a price floor of $0.9*X. The price ceiling hyperbolically approaches infinity, while the price floor linearly declines to zero over five years.

- Do exactly what AngelShares did, though stretched over five years instead of months.

- Hold a Gnosis-style reverse Dutch auction. If less than 100% of the token supply sells, allocate the remainder to an automated market maker aiming to ensure token price stability (note: if prices keep rising, the market maker sells tokens, and some revenue can go to the development team).

- Immediately place all tokens into a market participant with parameters + variables X (minimum price), s (fraction of all tokens sold), t (time since sale start), T (expected sale duration, e.g., 5 years), priced at

k / (t/T - s)tokens (this formula is odd and likely needs more economic research).

Note that other mechanisms should aim to solve additional token sale problems; for instance, directing proceeds into multi-curated escrows that release funds only upon milestone achievement is a very interesting idea worth pursuing further. However, the design space is highly multidimensional, and much more remains to be explored.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News