Understanding Sturdy Finance: How Does an Interest-Free Lending Protocol Balance the Relationship Between Lenders and Borrowers?

TechFlow Selected TechFlow Selected

Understanding Sturdy Finance: How Does an Interest-Free Lending Protocol Balance the Relationship Between Lenders and Borrowers?

SturdyFinance has shifted the priority of the current interest rate model, and this interest-free lending protocol establishes a win-win relationship between lenders and borrowers, potentially becoming the next new narrative in the lending market.

Written by: Tindorr

Compiled by: TechFlow

Money markets are a hidden frontier currently being developed by genuine builders. SturdyFinance redefines the priorities of current interest rate models—this interest-free lending protocol establishes a win-win relationship between lenders and borrowers, potentially becoming the next narrative in the lending market.

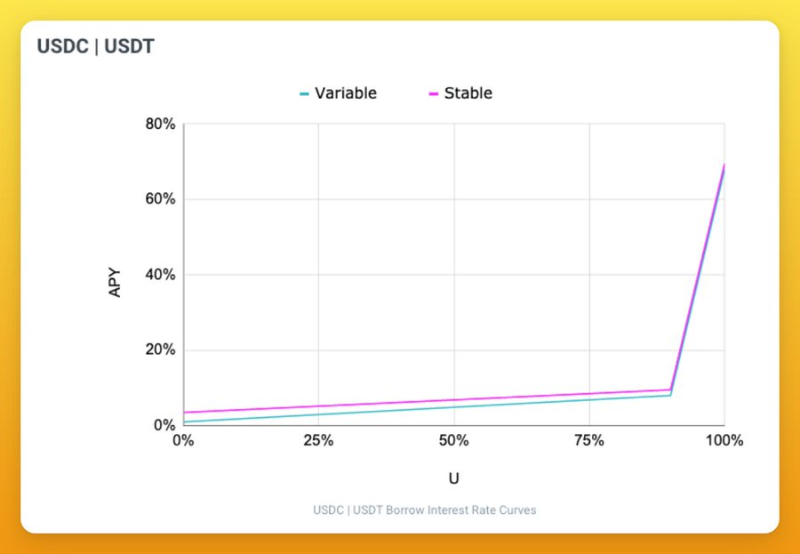

The core problem with current interest rate models stems from the imbalance between lenders and borrowers. The primary issue lies in their impracticality—borrowers must consistently outperform the market just to offset borrowing costs, effectively limiting borrower participation under this model.

Let’s consider this from the borrower’s perspective—for example, when using borrowed funds for yield farming:

-

Obtaining additional capital from money markets to generate higher returns.

-

Acquiring extra funds while paying high borrowing rates.

-

Forced to exit certain positions due to volatile interest rates.

-

Incurring losses when rates spike.

Due to inefficient borrowing rates, borrowers’ yields can easily turn negative. As a DeFi degen myself, I feel the pain—despite our best efforts, we still end up losing money.

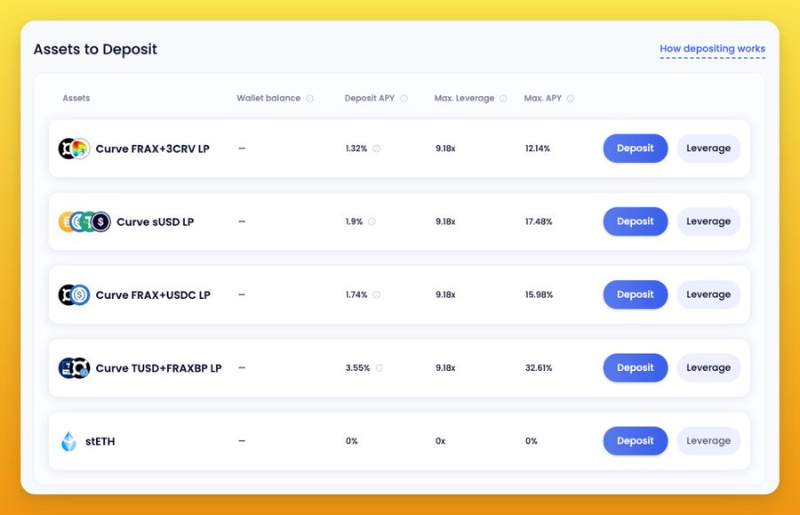

Sturdy offers three products that address this pain point:

• Creating leveraged LP positions for borrowers—enhancing capital efficiency.

• Optimizing the interest rate model—unlocking more possibilities for degens.

• Sharing yield with lenders—balancing incentives.

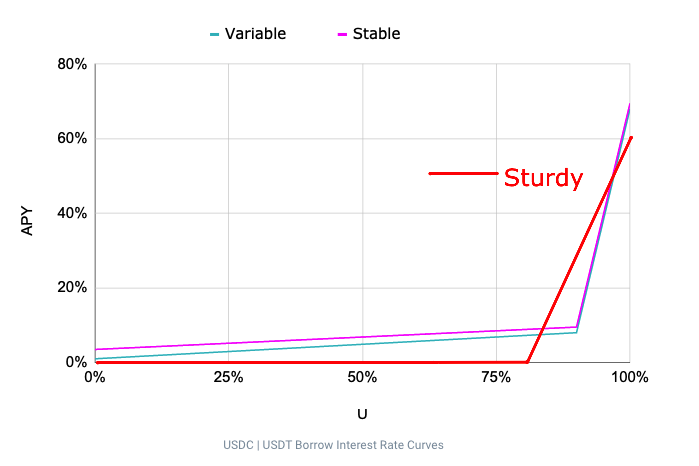

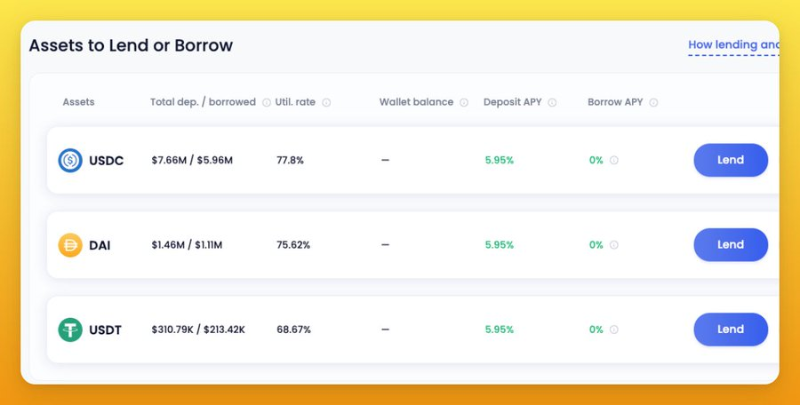

For borrowers, when utilization of a lending pool is below 80%, Sturdy sets the interest rate to 0%. This allows borrowers to leverage more independently and maximize capital efficiency thanks to zero borrowing costs.

For example: If you want to use 9x leverage on Curve’s sUSD LP, you could achieve a maximum APY of 36% (before sharing rewards with lenders + 0% loan cost). With this, you no longer need to worry about future borrowing expenses.

When utilization stays between 0–80%, Sturdy maintains a 0% interest rate. Beyond 80%, for every 1% increase in utilization, the rate increases by 3%, meaning at 100% utilization, borrowers would pay a 60% annual interest rate.

This optimization benefits both borrowers and lenders—when utilization is <80%, borrowers can freely experiment with strategies, while lenders receive additional benefits through shared rewards.

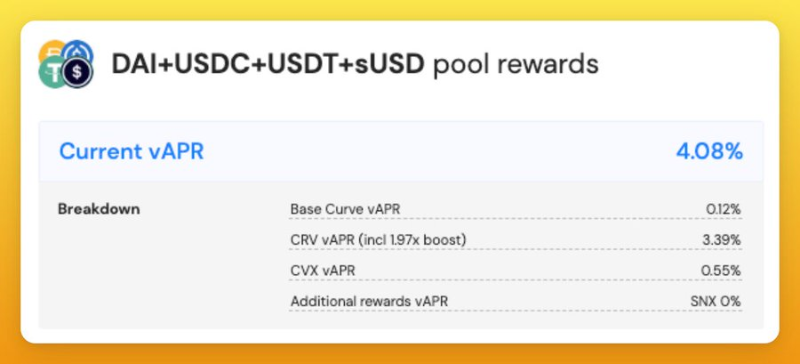

What are shared rewards? For instance, when you stake on Convex, you earn reward tokens—such as CRV generated from depositing LP tokens. A portion of these rewards is shared with lenders, as they are essential enablers of these strategies.

This enables stablecoin lenders to earn approximately 6% APY risk-free, as borrowers actively generate yield on their behalf. As you can see, this design significantly outperforms existing interest rate models.

To truly capture these gains, you should monitor the following metrics:

- TVL

- Lending pool utilization

- Actual APY of leveraged positions

However, I’m still waiting for real-world testing of the model, as I haven’t yet seen funding utilization rise above 80%. In such scenarios, some borrowers may face negative returns, and I’d like to observe how the market reacts under those conditions.

TL;DR

• This optimized interest rate model unlocks immense potential within money markets.

• Lenders can earn a portion of degen-generated yield risk-free (approximately 6% APY on stablecoins).

• Borrowers can generate higher returns with 0% borrowing costs.

• Still requires real-world stress-testing of the model.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News