Gamma: A fee-based APR control protocol, Uniswap V3 concentrated liquidity management protocol

TechFlow Selected TechFlow Selected

Gamma: A fee-based APR control protocol, Uniswap V3 concentrated liquidity management protocol

Gamma is a non-custodial, automated active concentrated liquidity manager that has just migrated from Uni V3 to Arbitrum.

Author: Res, Researcher at Proximity Labs

Translation: TechFlow

Gamma is a non-custodial, automated active concentrated liquidity manager that recently migrated from Uni V3 to Arbitrum.

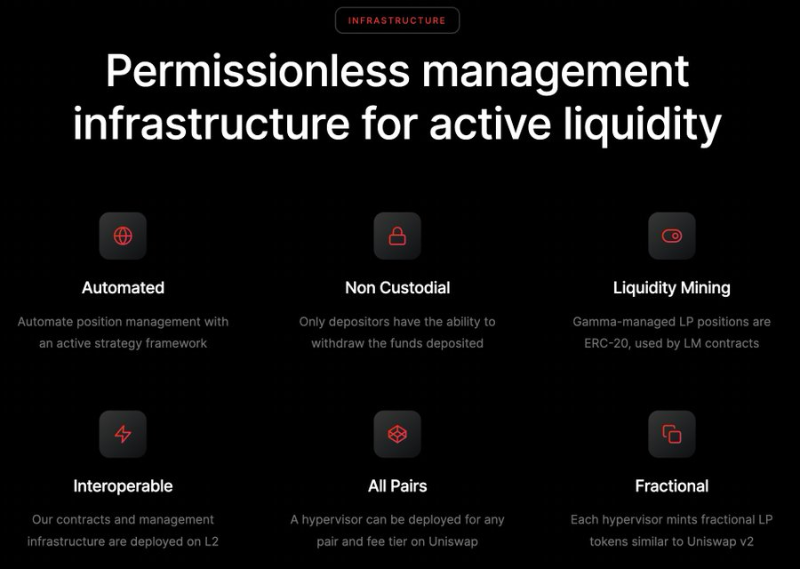

Gamma's supervisor contracts (Hypervisor + input strategies) automatically manage price ranges, rebalance assets, and reinvest earned fees to optimally generate yields.

Gamma transforms complex Uni V3 concentrated liquidity into simple passive strategies.

Moreover, it offers not only retail solutions (public version), but also B2B solutions for enterprises such as DAOs, Treasuries, and Protocols (professional version).

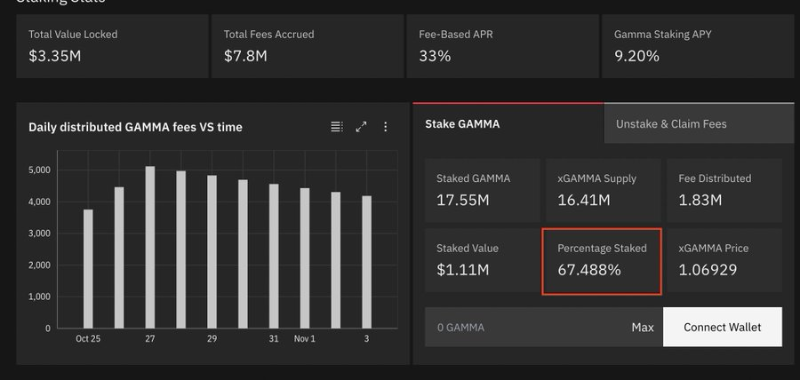

Staking Gamma earns xGamma, which captures 10% of protocol fees. Fees earned from Gamma staking are used to repurchase Gamma tokens from the secondary market.

This creates a positive flywheel: more TVL → more fees → more $GAMMA bought from the market and distributed to stakers.

So far, 67.5% of $GAMMA tokens have been staked. At $3 per token, this means only $950,000 worth of $GAMMA remains in circulation.

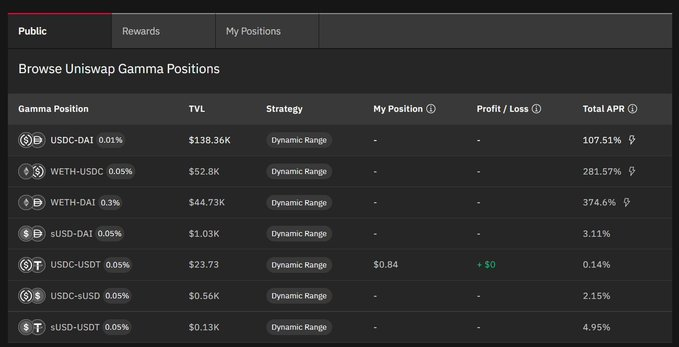

The remaining 90% of revenue goes directly to specific LPs. The APR LPs receive is based on fees rather than TVL—a key difference from other protocols in the market. Gamma essentially has no competitors; the only comparable project is Arrakis Finance, which lacks a token.

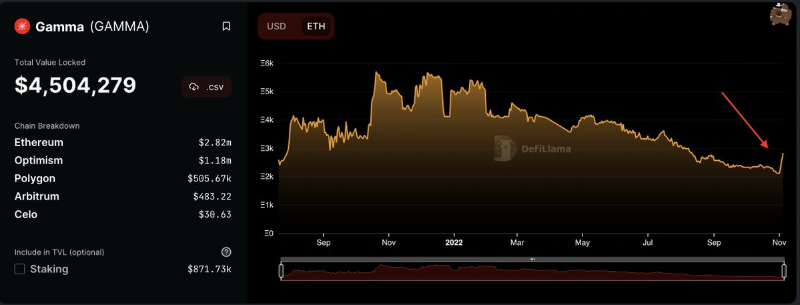

Arrakis has $700 million in TVL (peaked at $1.8 billion), while Gamma currently holds around $4 million in TVL—still very early stage.

Assuming Gamma captures the same $700 million TVL as Arrakis, 10% of its 33% fee-based APR would be used to repurchase $GAMMA for stakers. This would generate $23 million/year in $GAMMA buybacks and staker rewards.

Even with a more realistic average APR of 10–20%, the impact on token price would still be substantial.

One more thing: platform fees generated by Gamma > $GAMMA market cap.

Fees = $7.8 million distributed to stakers since January 2022 (includes部分 fees from 2021), while Mcap is only $3 million.

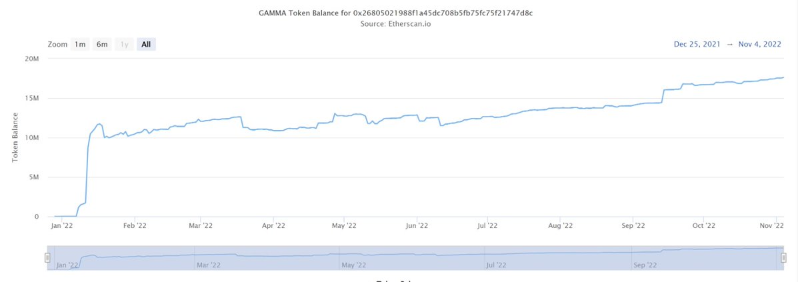

Gamma’s TVL is now surging—increasing by 1,000 $ETH (+50%) within days.

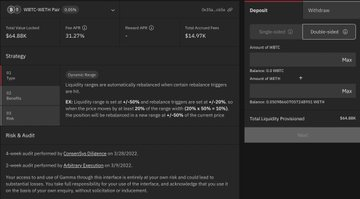

Current WBTC-WETH annual yield is 31%. Where are the miners?

They’ve also partnered with Rocket Pool, offering $RPL incentives for the rETH-ETH 0.05% pool.

Looks like their BD team is truly strong, signaling that more TVL may flow into their LP and staking pools in the coming weeks, along with additional partnerships.

Charts appear bottomed out, and as TVL grows and awareness of its potential spreads, trading volume is picking up.

They’ve raised funding from DCG, Electric Capital, Maven 11, Spartan Group, GSR, DeFi Alliance, Tribe Capital, and others, and have solid tokenomics.

As the market recovers and the broader DeFi sector grows, Gamma—with no real competition—is poised for strong performance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News