A Brief Analysis of GMX's Token Design and Potential Risks

TechFlow Selected TechFlow Selected

A Brief Analysis of GMX's Token Design and Potential Risks

Hidden concerns amid high热度?

Author: DeFi Cheetah

Translated by: angelilu, Foresight News

In this article, you will learn:

1. How GMX differs from other protocols (zero slippage for traders + no impermanent loss for LPs);

2. How value accrues to the GMX token;

3. Potential risks and solutions for GMX.

Protocol Overview

Launched in September 2021, GMX is a decentralized perpetual and spot exchange that enables trading of BTC, ETH, AVAX, UNI, and LINK directly from users' wallets with 0% slippage, 10 bps fees, and up to 30x leverage on fast and low-cost networks—no KYC or geographic restrictions.

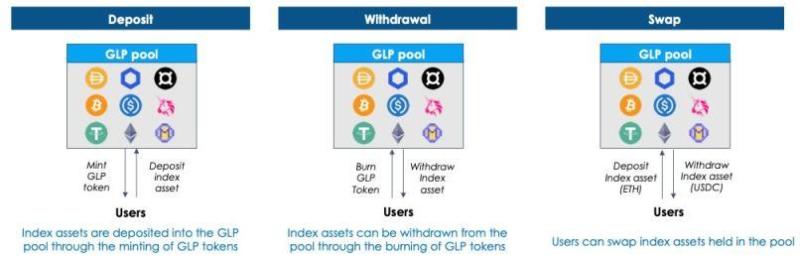

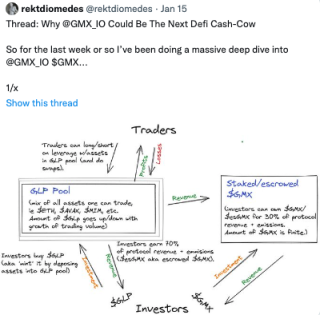

GMX has a liquidity pool called GLP, a multi-asset pool providing liquidity for margin trading: users can go long/short and execute trades by minting and redeeming GLP tokens. The pool earns LP fees from trades and leveraged positions, which are distributed to both GMX and GLP holders.

To trade with leverage, traders deposit collateral into the protocol. They can choose up to 30x leverage—the higher the leverage, the higher the liquidation price, which gradually increases as borrowing fees accumulate.

For example, when going long ETH, a trader is effectively "renting" the upside of ETH from the GLP pool; when shorting ETH, they are "renting" the upside of stablecoins relative to ETH from the GLP pool. However, the assets in the GLP pool are not actually lent out.

Upon closing a position, if the trader was correct, profits are paid from the GLP pool in the form of long tokens; otherwise, losses are deducted from the collateral and paid into the pool. The GLP benefits from traders’ losses and also gains from their profits.

During this process, traders pay trading fees, opening/closing fees, and borrowing fees in exchange for gaining exposure (long/short) to specified tokens (BTC, ETH, AVAX, UNI, and LINK) against USD.

If a trader withdraws a different asset than the one deposited as collateral, it is considered a trading activity and incurs a trading fee based on a percentage of the collateral size.

GLP represents shares in the liquidity pool, similar to an index of assets used for trading and leveraged positions. It can be minted using any asset in the index and redeemed for any asset within the index.

The price of the GLP token equals the total value of all assets in the index—including unrealized P&L from open positions—divided by the total supply of GLP. The fundamental assumption is that every open position could be closed at any moment.

LPs who mint and hold GLP tokens take on delta risk of the asset index—that is, holding a basket of crypto assets—and benefit when the market value of the pool increases after depositing any designated asset.

Because GLP is minted based on the market value of the pool, new minting does not dilute existing LP holders.

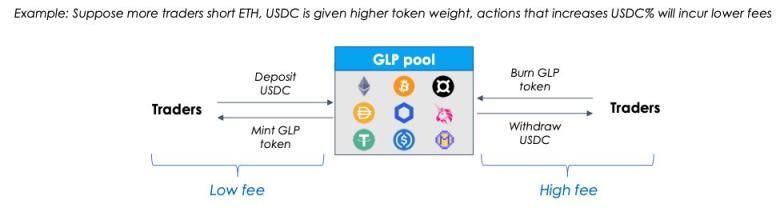

Fees for minting/burning GLP depend on whether an index asset is underweight or overweight—i.e., whether its weight in the index is below or above its target weight. If ETH is underweight, minting GLP by depositing ETH incurs lower fees, thus incentivizing such deposits.

How are target weights set? They are adjusted weekly based on open interest: if many traders are long ETH on Arbitrum, the GLP pool sets a higher target weight for ETH; conversely, if there’s significant shorting, the target weight for stablecoins increases.

DEX aggregators make achieving target weights easier: when certain index assets are underweight, cheaper swap fees combined with zero slippage provide optimal pricing, encouraging large-volume routing to GMX to rebalance the asset weights in the GLP pool.

Holding GLP essentially means:

-

Providing liquidity (with no impermanent loss, as explained below);

-

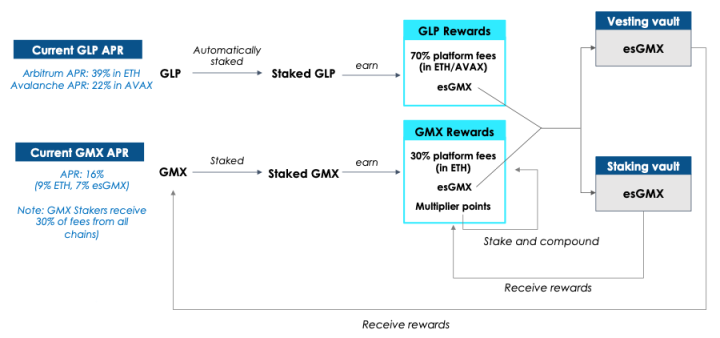

Earning 70% of platform fees paid in ETH or AVAX;

-

Acting as the counterparty to leveraged traders (like the house in a casino) and profiting from their losses;

-

Receiving staking rewards in GMX;

-

Diversified exposure to a crypto index.

Instead of using the standard AMM model (x*y=k), GMX uses dynamic aggregated Chainlink oracles (pulling prices from Binance and FTX) to determine the “true” price of assets. This enables zero-slippage execution of market orders.

This works because GMX simply pulls real-time prices from CEXs, offering traders optimal execution without relying on arbitrageurs to adjust price discrepancies across DEXs. LPs are also protected from impermanent loss since they don’t bear the cost of price discovery.

Token Design

GLP holders, as compensation for taking on delta risk and counterparty risk (when traders win), receive 70% of platform fees, profits from traders’ losses, and esGMX—a reward token.

Staking GMX tokens grants access to 30% of platform fees, esGMX, and multiplier points. esGMX follows a vesting model similar to CurveFinance’s ve model, but without a hard lock. Instead, if rewards are claimed, esGMX is linearly released over one year.

esGMX rewards have two uses:

-

They can be staked like regular GMX to earn rewards,

-

They can vest into GMX tokens over one year, as described above.

By immediately staking esGMX rewards, users earn the same rewards as regular staked GMX—more esGMX, multiplier points, and ETH/AVAX from platform fees.

To vest esGMX over one year, no additional rewards are earned during the period, and the underlying staked token (GLP or GMX) cannot be withdrawn; otherwise, esGMX rewards will be proportionally reduced. For example, withdrawing 50% of the principal tokens results in a 50% reduction in rewards.

What are Multiplier Points (MPs)? MPs are not GMX, but they boost yield similarly to staking (though MPs themselves do not generate more MPs), thereby rewarding long-term GMX holders. MPs are earned at a fixed rate of 100% per second.

Boost percentage = 100 × (staked multiplier) / (staked GMX + staked esGMX); i.e., MPs represent the user’s share of total staked GMX & esGMX.

GMX earns fees through the following:

-

Trading fees: 0.1% of position size for opening/closing;

-

Swap fees: Dynamic 0.2–0.8% of collateral size if a swap is required upon closing;

-

Borrowing fees: (borrowed asset / total assets in GLP) × 0.01%, accrued at the start of each hour;

-

Dynamic fees for minting GLP, burning GLP, or executing swaps: depend on whether the action helps achieve the target weight of a specific asset in the GLP index.

Fees returned to GLP holders and GMX stakers each week are collected from trading activity in the prior week starting from Wednesday noon. The actual APR for the week depends on the previous week’s trading volume.

Potential Risks of GMX

Bear Market Short Skew

The biggest risk is that during sharp market downturns, some short traders profit significantly, causing the GLP pool to shrink due to delta exposure, forcing it to pay out profits in stablecoins, further reducing the pool size.

A bear market short skew could lead to substantial losses for GLP holders, making GLP less attractive to LPs and potentially leading to declining TVL. However, empirically, the delta risk of the GLP pool is somewhat offset (or compensated) by traders’ losses.

One reason is that short selling is inherently difficult, which is why most people lose money in bear markets.

Draining the GLP Pool

Another risk is that traders collectively profit enough to drain the GLP pool. This may occur if net open interest (OI) constitutes a large portion of the platform’s available liquidity, especially on the short side during bear markets.

To prevent this, dynamic OI caps could be implemented based on real-time net exposure of all long/short positions across assets on GMX.

Long-Tail Asset Risk

The oracle pricing model works well for liquid assets like ETH but less so for illiquid ones.

In particular, during extreme market conditions, Chainlink oracles may stop providing prices for certain tokens, potentially causing significant losses to GMX.

Since most perpetual trading volume comes from liquid assets, reducing long-tail trading pairs would not significantly impact GMX’s business. Centralized exchanges face the same issue, which is why perpetual trading pairs are always far fewer than spot pairs.

Potential Risk Mitigation Solutions

Recently, an incident occurred where traders on Avalanche exploited GMX’s oracle pricing model and the thin liquidity of AVAX on CEXs to manipulate AVAX’s off-chain price and extract $566,000 from the GLP pool.

Many people became overly concerned and spread FUD about GMX. But I don’t share that view.

How did this happen? For example, a large ETH whale familiar with GMX buys $50 million worth of ETH via GMX, then goes to major CEXs like Binance and FTX to buy $40 million of ETH, pushing the price up by about 2%. The net exposure of $10 million × 2% becomes profit. Slippage and trading fees are the costs.

How to avoid draining the GLP pool due to zero slippage?

GMX could incorporate more data, such as order book depth (or implied DEX slippage), to more accurately pass costs/fees onto traders. GMX could lower OI caps for less liquid tokens and automatically set OI caps based on CEX liquidity.

If AVAX has $20 million in liquidity on Binance and FTX, the OI cap on GMX should be around $20 million. If new open positions exceed this cap, slippage fees should be charged and returned to the GLP pool to ensure traders cannot achieve better outcomes than justified by market conditions.

Some might ask: if slippage fees are charged, what becomes of @GMX_IO's value proposition? Briefly, even with slippage, the available liquidity for zero-slippage trading on the platform at any given time interval may still exceed that of any single CEX.

Additional Resources

I highly recommend checking out @Riley_gmi’s comprehensive report, from which I’ve also drawn some references.

Flood Capital has also published several high-quality tweets.

@rektdiomedes also wrote an excellent summary worth your time.

GMX team members include @xdev_10, @xhiroz, @vipineth, @xm92boi, @0xAtomist, etc.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News