Why haven't cryptocurrency applications been widely adopted on a large scale yet?

TechFlow Selected TechFlow Selected

Why haven't cryptocurrency applications been widely adopted on a large scale yet?

Where are the real users of encrypted dApps? Why haven't all these "use cases" taken off? Why are most dApps unused?

Author: shivsak

Translation: TechFlow

We talk a lot about real-world use cases for cryptocurrency, but if we were to ask our friends and family whether they've ever used crypto, 99% of them haven't interacted with any dApp at all.

And aside from crypto casinos, they likely have little interest in other dApps. So where are the real users of crypto dApps? Why haven't all these "use cases" taken off? Why are most dApps unused?

In this article, I’ll explore some potentially useful crypto applications and explain why they remain largely ignored.

Why haven’t crypto use cases taken off?

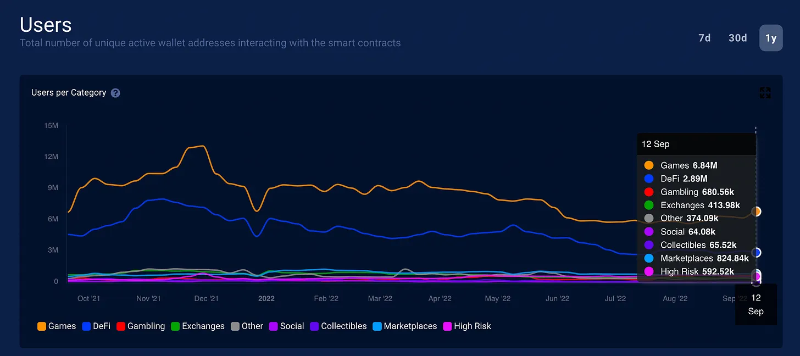

First, let’s quickly review the data. According to DappRadar, around 15 million users today interact with dApps.

Let’s assume DappRadar's data is incomplete—say actual usage is five times higher, totaling 75 million users. That still represents less than 1% of the global population. Is that “mass adoption”? Not quite.

Let’s examine several use cases and understand why they haven’t gained traction.

Payments

Here are the reasons I believe crypto payments haven’t gone mainstream:

Web2 solutions are already good enough

For the general public, existing Web2 solutions are already “good enough”:

- Credit or debit cards are sufficiently convenient for retail or online purchases;

- Venmo, PayPal, Zelle, Apple Pay, etc., work well for everyday peer-to-peer transfers;

- Transfers via Web2 apps are instant, and their interfaces are very user-friendly.

Traditional systems aren’t compatible with crypto

You can’t pay your mortgage with stablecoins (at least not yet).

Part of this is due to regulatory uncertainty. Over time, as regulations become clearer, more traditional providers will gain the confidence and ability to start accepting or using crypto.

Complex tax implications

Crypto payments are taxable events—adding significant complexity to your life.

Crypto debit cards sound great in theory. But would you really want to report a taxable event every time you buy coffee? There’s no need, and no added benefit.

Merchants are unwilling to accept crypto

Merchants save 2–3% by avoiding credit card fees, but tax complications and regulatory uncertainty make accepting crypto impractical.

Also, far more people own credit cards than hold crypto, so merchants expect most customers to pay with credit cards rather than crypto.

But what about other use cases? For example...

Tokenization of Real-World Assets

There is significant value in tokenizing real-world assets like real estate.

Tokenization makes assets investable, liquid, accessible, verifiable, and portable. There are also secondary benefits, such as integrating tokenized assets into other smart contracts for lending, etc.

But effectively tokenizing these assets is extremely difficult.

First, there are legal limitations. In most jurisdictions, NFTs and tokens are not recognized as legal representations of real estate or other RWAs (real-world assets).

To get around this, most tokenized real estate projects today involve holding companies that issue NFTs representing shares in those companies.

But this is a flawed model because you must always trust the holding company.

The company could go bankrupt, or founders might manipulate corporate structures, rendering your NFT worthless.

The free market might also lose confidence in the NFT, making it illiquid and valueless.

Beyond typical risks associated with real estate investment, there are numerous additional risks.

Stock Tokenization

Stock tokenization offers many benefits but faces similar issues as real estate tokenization.

I’ve seen two main models for stock tokenization:

1. A trusted centralized entity buys and sells real stocks when you trade their tokens—same problem as with real estate tokenization.

2. Over-collateralized synthetic stocks.But the downsides of over-collateralized stocks are:

- You must deposit more collateral than the value of the stock you want to purchase, making it highly inefficient. For example, depositing $150 in collateral to buy $100 worth of stock.

- If the stock price rises significantly, you risk losing your collateral. This isn’t ideal for long-term holders; generally, this model only helps short-term traders or hedgers.

Lending

Loans can be either over-collateralized or under-collateralized.

Over-collateralized loans require you to deposit more collateral than the loan amount. So to borrow $100, you might need to deposit $150 worth of collateral (similar to over-collateralized synthetic stocks).

This makes over-collateralized lending highly inefficient and suitable only for a narrow set of users.

Most people who want or need loans don’t seek over-collateralized ones.

Under-collateralized loans resemble traditional bank loans. You want to borrow $100 without posting any margin or collateral. But if wallets are anonymous, users can simply run off with the funds. Therefore, you need some form of identity and credit verification system, just like in TradFi.

Goldfinch uses centralized intermediaries like banks and fintech firms to perform credit assessments and distribute funds to borrowers.

TrueFi primarily lends to crypto-native institutions.

For instance, here’s a $10 million loan issued to Bastion Trading for 180 days at an 8.8% annual interest rate.

But these aren’t fully decentralized, and this type of lending doesn’t truly help drive mass crypto adoption.

The lending use case has some merits—anyone can deposit into DeFi lending pools and earn solid yields backed by real loans—but this alone is certainly insufficient for mass adoption.

Gaming

Many people don’t understand why gaming should be linked to crypto.

Crypto and NFTs enable game assets that are unique, tradable, valuable, useful, and portable—integrated into a broader blockchain gaming ecosystem.

But currently, the crypto gaming space looks quite bleak.

Most people play crypto games primarily to earn money.

In bear markets, rewards dry up quickly. Most games that raised tens of millions during bull runs now have fewer than a few thousand active users.

Building games people genuinely enjoy requires massive capital and engineering effort—and top-tier success takes years of development.

It may take several more years before the crypto gaming ecosystem matures into something meaningful.

Conclusion: Why dApps Haven’t Been Rapidly Adopted

I believe the slow adoption can largely be attributed to:

- Regulatory uncertainty

- Failure to solve real problems

- Lack of innovative use cases that meaningfully improve upon existing solutions

- Excessive complexity in usage

So how and when will real users begin adopting crypto?

As Miles Deutscher put it perfectly: “Mass adoption will only happen when dApps are built that retail users actually want to use… Protocols need to create intrinsic user benefits by leveraging blockchain.”

I believe certain use cases have strong potential to drive mass adoption, such as: crowdfunding, NFT domains, NFT ticketing, gambling, gaming, cross-border payments, etc.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News